Copyright © 2015 Pearson Education, Inc.

4-38

(20-30 min.) P4-42A

Req. 1

Robotic Construction Toys Corp

Predicted Quality Cost Savings

Activity

Predicted

Reduction In

Activity Units

×

Activity Cost

Allocation

Rate

=

Predicted

Reduction

In Activity

Costs

Inspection of incoming materials

305

$17

$ 5,185

Inspection of finished goods

305

$31

9,455

Number of defective units discovered in-house

3,200

$16

51,200

Number of defective units discovered by customers

900

$36

32,400

Lost sales to dissatisfied customers

330

$61

20,130

Total predicted quality cost savings

$118,370

Req. 2

Robotic Construction Toys Corp.

Net Benefit of Design Engineering Effort

Total predicted quality—cost savings

$118,370

Less: Cost of design engineering

(80,000)

Net benefit of design engineering

$ 38,370

Req. 3

Measuring the cost of quality-related activities is difficult. As an alternative, they could monitor nonfinancial measures

of quality and attempt to improve them.

1,200

$140,000

Total indirect costs allocated

$420,000

$140,000

÷ Number of units

Managerial Accounting 4e Solutions Manual

(continued) P4-43A

Req. 3

The activity-based costing system is more accurate than the single-rate system in assigning the costs of the resources

each job consumes. The single rate allocates all overhead cost based on direct labor hours. Job A units require 90 direct

income.

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Problems (Group B)

(40 min.) P4–44B

Req. 1

Plantwide

overhead rate

=

Total manufacturing overhead

Total direct labor hours

=

$1,090,000

19,500* direct labor hours

=

$56 per direct labor hour (rounded)

*When calculating plantwide overhead rates, all direct labor

hours incurred in the plant are used.

Req. 2

Department allocation rate

=

Department overhead cost

Department allocation base

Machining

=

$650,000

4,000 machine hours

=

$163 per machine hour (rounded)

Assembly

=

$440,000

16,000 direct labor hours

=

$28 per direct labor hour (rounded)

Managerial Accounting 4e Solutions Manual

(continued) P4-44B

Req. 5

Overhead allocation based on departmental rates:

Job 500

Job 501

Machining Department:

Departmental allocation rate

$163/ MH

$163/ MH

× Machine hours used by Job

× 5 MH

× 10 MH

Overhead allocation

$815

$1,630

Assembly Department:

Departmental allocation rate

$28/ DL hr

$28/ DL hr

× DL hours used by Job

× 13 DL hrs

× 13 DL hrs

Overhead allocation

$364

$364

Total overhead allocation

$1,179

$1,994

Req. 6

The single plantwide overhead rate assigned the same amount of overhead to both jobs. The departmental rates assign

more overhead cost to Job 501 than Job 500 due to the extra machine hours used. This seems fairer.

Req. 7

Manufacturing cost and sales price using current costing system:

Job 500

Job 501

Direct Materials

$1,800

$1,800

Direct Labor (16 DL hours × $20)

320

320

Manufacturing overhead (from req. 4)

896

896

Total manufacturing cost

$3,016

$3,016

Markup for pricing (%)

× 125%

× 125%

Sales price (rounded)

$3,770

$3,770

Req. 8

Gross profit using current costing system:

Job 500

Job 501

Sales Price (from Req. 7)

$3,770

$3,770

Less: Total manufacturing cost

3,016

3,016

Gross profit / (loss)

$754

$754

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) P4–44B

Gross profit using departmental rate costing system:

Job 500

Job 501

Sales price (from Req. 7)

$ 3,770

$ 3,770

Less: Total mfg. cost

Direct Materials

$ 1,800

$ 1,800

Direct Labor [(3+13) x $20]

320

320

Manufacturing overhead (from req. 5)

1,179

3,299

1,994

4,114

Gross profit (loss)

$ 471

$(344)

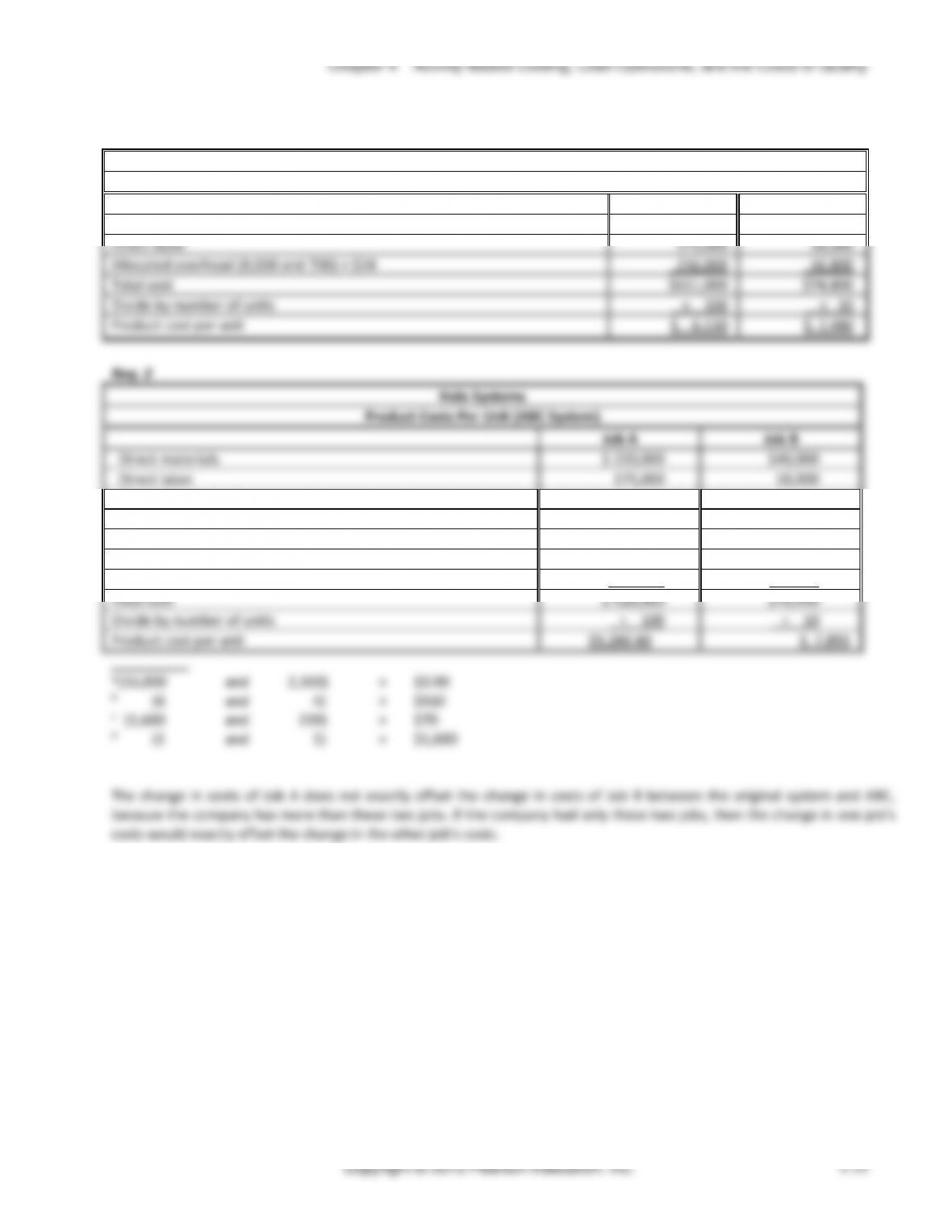

(20-30 min.) P4–45B

Req. 1

Russell Corp.

Per-Unit Manufacturing Costs

Standard

Desk

Unpainted

Desk

Direct materials

$ 95,000

$23,000

Materials handling (119,500 and 29,500) x $0.90

107,550

26,550

Assembling (5,900 and 600) × $19

100,300

10,200

Painting (5,500 × $5.10)

28,050

0

Total manufacturing costs

$330,900

$59,750

Number of units

÷ 5,500

÷ 3,000

Manufacturing cost per unit

$ 60

$ 20

Req. 2

Russell Corp.

Full Product Costs

Standard

Desk

Unpainted

Desk

Premanufacturing activities

$ 4

$ 3

Manufacturing product costs (from req. 1)

60

20

Postmanufacturing activities

20

19

Full product cost per unit

$84

$42

Managerial Accounting 4e Solutions Manual

(continued) P4–45B

Req. 3

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

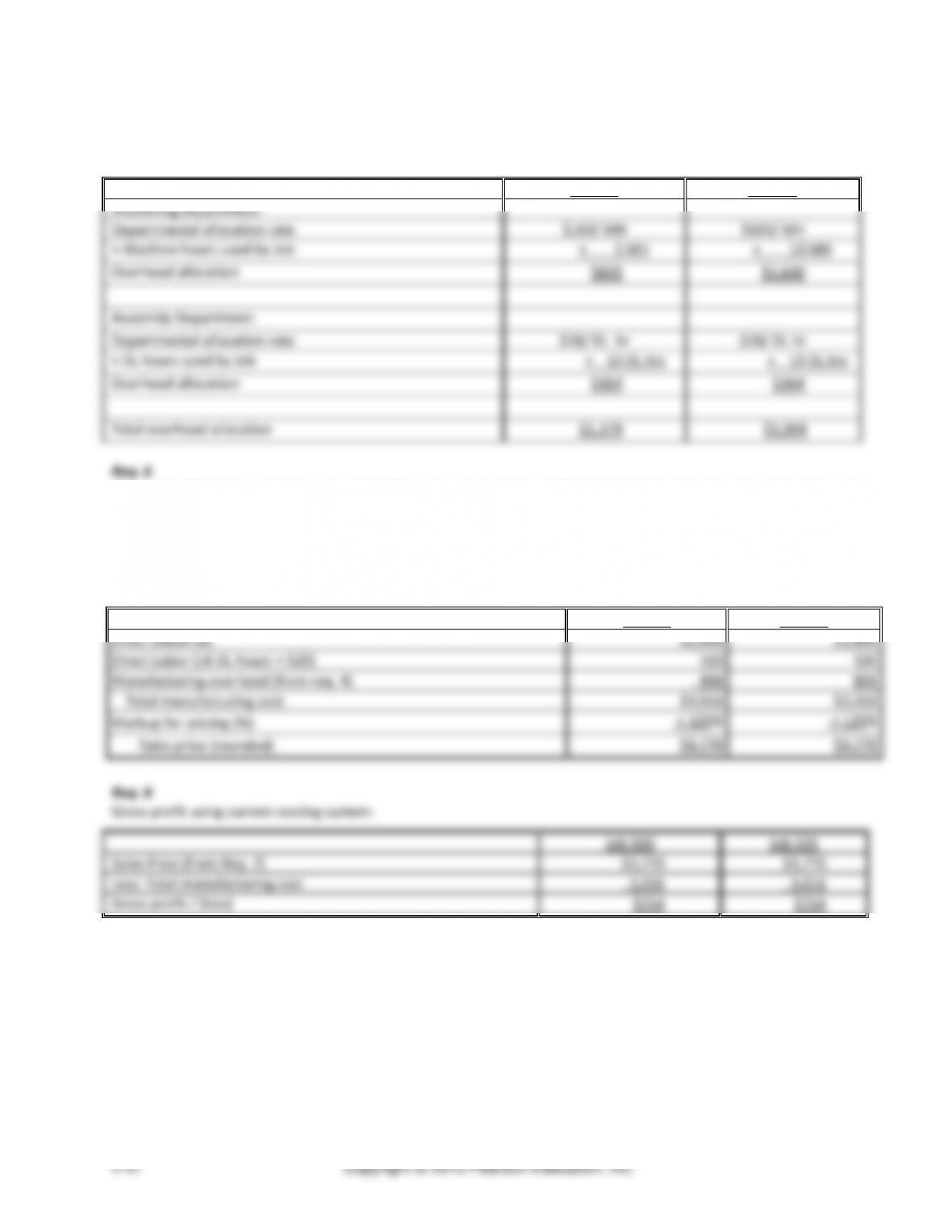

(continued) P4-46B

Req. 3

Product

Cost allocation rate

x

Actual qty. of allocation

base

=

Indirect cost allocated

Commercial

$450

x

900

=

$405,000

Travel

$450

x

300

=

$135,000

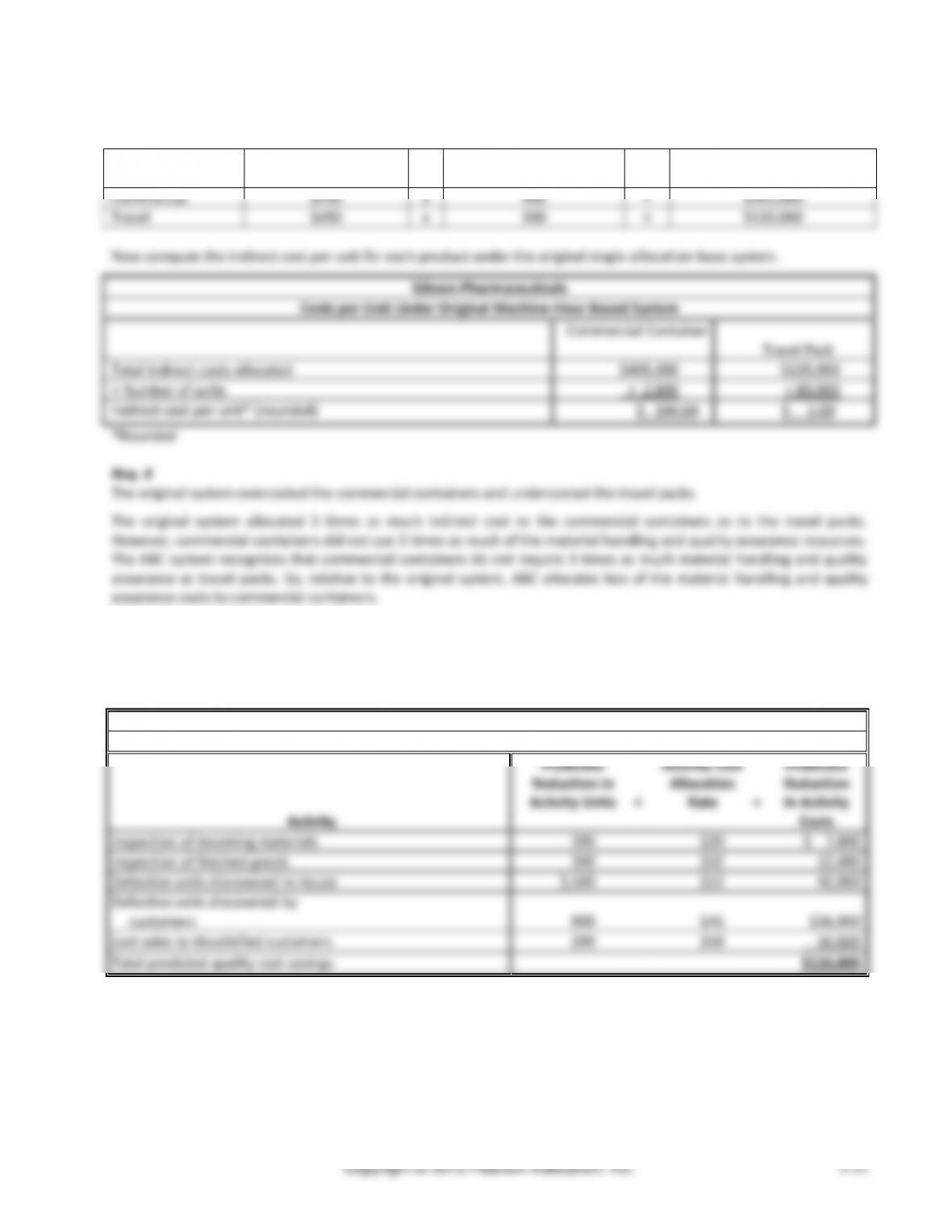

Now compute the indirect cost per unit for each product under the original single-allocation-base system.

Gibson Pharmaceuticals

Costs per Unit Under Original Machine-Hour Based System

Commercial Container

Travel Pack

Total indirect costs allocated

$405,000

$135,000

÷ Number of units

÷ 2,800

÷ 80,000

Indirect cost per unit* (rounded)

$ 144.64

$ 1.69

*Rounded

Req. 4

The original system overcosted the commercial containers and undercosted the travel packs.

The original system allocated 3 times as much indirect cost to the commercial containers as to the travel packs.

However, commercial containers did not use 3 times as much of the material handling and quality assurance resources.

The ABC system recognizes that commercial containers do not require 3 times as much material handling and quality

assurance as travel packs. So, relative to the original system, ABC allocates less of the material handling and quality

assurance costs to commercial containers.

(20-30 min.) P4–47B

Req. 1

Large Construction Toys Corp.

Predicted Quality Cost Savings

Activity

Predicted

Reduction In

Activity Units

×

Activity Cost

Allocation

Rate

=

Predicted

Reduction

In Activity

Costs

Inspection of incoming materials

390

$20

$ 7,800

Inspection of finished goods

390

$32

12,480

Defective units discovered in-house

3,500

$12

42,000

Defective units discovered by

customers

900

$41

$36,900

Lost sales to dissatisfied customers

290

$58

16,820

Total predicted quality cost savings

$116,000

Managerial Accounting 4e Solutions Manual

(continued) P4-47B

Req. 2

Large Construction Toys Corp.

Net Benefit of Design Engineering Effort

Total predicted quality cost savings

$116,000

Cost of design engineering

(65,000)

Net benefit of design engineering

$ 51,000

Req. 3

Measuring the cost of quality-related activities is difficult. An alternative approach to measure quality improvement is

to monitor nonfinancial measures of quality and attempt to improve them.

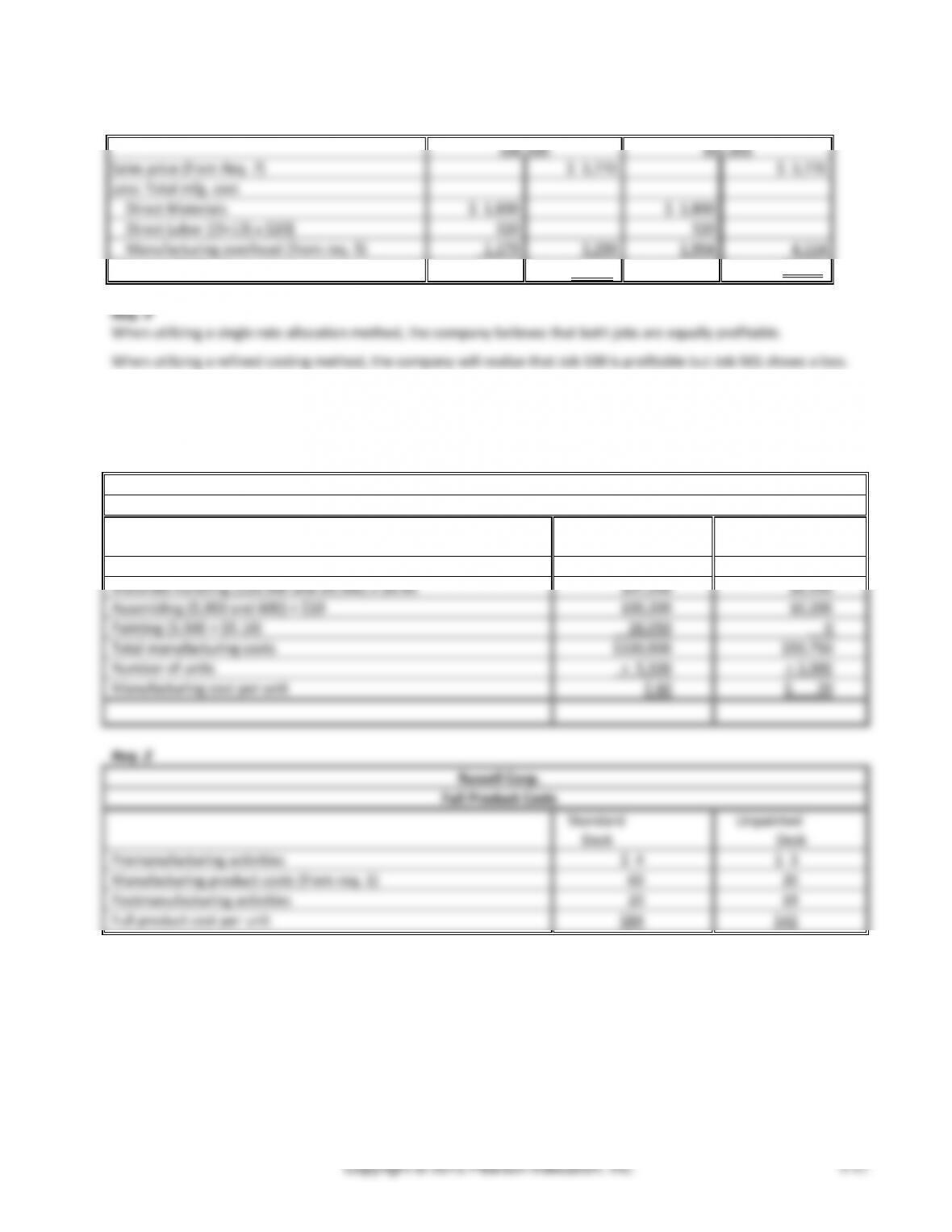

(20-40 min.) P4–48B

Req. 1

Axis Systems

Product Costs per Unit (Original Cost System)

Job A

Job B

Direct materials

$210,000

$30,000

Direct labor

160,000

12,000

Allocated overhead (8,000 and 600) × $22

176,000

13,200

Total cost

$546,000

$55,200

Divide by number of units

÷ 100

÷ 10

Product cost per unit

$ 5,460

$ 5,520

Req. 2

Axis Systems

Product Costs Per Unit (ABC System)

Job A

Job B

Direct materials

$ 210,000

$30,000

Direct labor

160,000

12,000

Allocated overhead:

Materials handlinga

12,750

1,700

Machine setupb

3,000

2,000

Assemblingc

120,000

16,000

Shippingd

1,500

1,500

Total cost

$ 507,250

$63,200

Divide by number of units

÷ 100

÷ 10

Product cost per unit

$5,072.50

$ 6,320

__________

a (15,000

and

2,000)

×

$0.85

b (6

and

4)

×

$500

c (1,500

and

200)

×

$80

d (1

and

1)

×

$1,500

The change in costs of Job A does not exactly offset the change in costs of Job B between the original system and ABC,

because the company has more than these two jobs. If the company had only these two jobs, then the change in one job’s

costs would exactly offset the change in the other job’s costs.

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) P4-48B

Req. 3

The activity-based costing system is more accurate than the single-rate system in assigning the costs of the resources

each job consumes. The single rate allocates all overhead cost based on direct labor hours. Job A units require 80 direct

Copyright © 2015 Pearson Education, Inc.

4-48

A4–49 Discussion & Analysis Questions

1. Explain why departmental overhead rates might be used instead of a single plantwide overhead rate.

A single plantwide overhead rate doesn’t always do a good job of matching the cost of overhead resources with

2. Using activity-based costing, why are indirect costs allocated while direct costs are not allocated?

Since direct costs can be traced to products, they are not allocated. Indirect costs, such as overhead, cannot be

3. How can using a single predetermined manufacturing overhead rate based on a unit-level cost driver cause a

high-volume product to be overcosted?

4. Assume a company uses a plantwide predetermined manufacturing overhead rate that is calculated using direct

labor hours as the cost driver. The use of this plantwide predetermined manufacturing overhead rate has

resulted in cost distortion. The company’s high-volume products are overcosted and its low-volume products are

5. A hospital can use activity-based costing (ABC) for costing its services. In a hospital, what activities might be

considered to be value-added activities?

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

What activities at that hospital might be considered to be non-value-added?

6. A company makes shatterproof, waterproof cases for iPhones. The company makes only one model and has

been very successful in marketing its case; no other company in the market has a similar product. The only

customization available to the customer is the color of the case. There is no manufacturing cost difference

7. Compare a traditional production system with a lean production system. Discuss the similarities and the

differences.

Some of the differences between a traditional production system and a lean production system are

• like machines grouped together vs. production cells

8. Think of a product with which you are familiar. Explain how activity-based costing could help the company that

9. It has been said that external failure costs can be catastrophic and much higher than the other categories. What

are some examples of external failure costs?

• Lost sales

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Application & Analysis

A4–50

1. Describe the company selected, including its products or services.

1. Process customer purchases

3. Handle customer inquiries

5. Stock shelves

7. Close out cash registers daily

3. For each of the key activities, list a potential cost driver for that activity and describe why this cost driver would

be appropriate for the associated activity.

2. special orders

4. training sessions held

6. events scheduled

8. bookkeeper’s hours

Student responses will vary.

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Copyright © 2015 Pearson Education, Inc.

4-53

(20–30 min.) A4-52

Ethics Mini-Case

1. The ethical issues in this situation are:

a. Competence: “Perform professional duties in accordance with relevant laws, regulations, and technical

standards.” By burying the cost for the silver line, he would be violating technical standards.

b. Competence: “Provide decision support information and recommendations that are accurate, clear, concise,

2. This does not influence the analysis of whether Jacob has violated any ethical principles. Even though it cannot be

3. I do not agree that no one is hurt by burying the cost in general cost pools; by burying the cost there, it is shared

4. Jacob’s responsibilities as a management accountant are to report information ethically, objectively, and

(20–30 min.) A4-53

Real Life Mini-Case

1. Think about the value chain for a carton of eggs that is sold in the grocery store. List as many steps in the value

chain as you can imagine. At what points in the value chain does waste most likely occur.

2. In this chapter, the eight wastes of traditional operations were discussed. Which types of waste are in the value

chain that you identified in question 1?

3. Answer the following questions from the standpoint of Cal-Maine Foods, Inc., and its egg farms:

Managerial Accounting 4e Solutions Manual

To individually stamp each egg, the company will have to create a new stamp for each egg batch, which may not

Foods.

4. Now answer the following questions from the standpoint of Walmart:

a. What costs might decrease as a result of purchasing eggs that are stamped individually with grade, size,

traceability code and freshness date information?

5. Who should bear the cost of individual egg stamping operations: Cal-Maine Foods, Walmart, or the consumer?

Because of the tremendous amount of waste involved with the current system of discarding entire cartons,

should individual egg stamping be mandated by the government? Why or why not?

Cal-Maine should bear the cost of the individual egg stamping operations because it is probably the one who it