Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) E4–28B

Req. 4

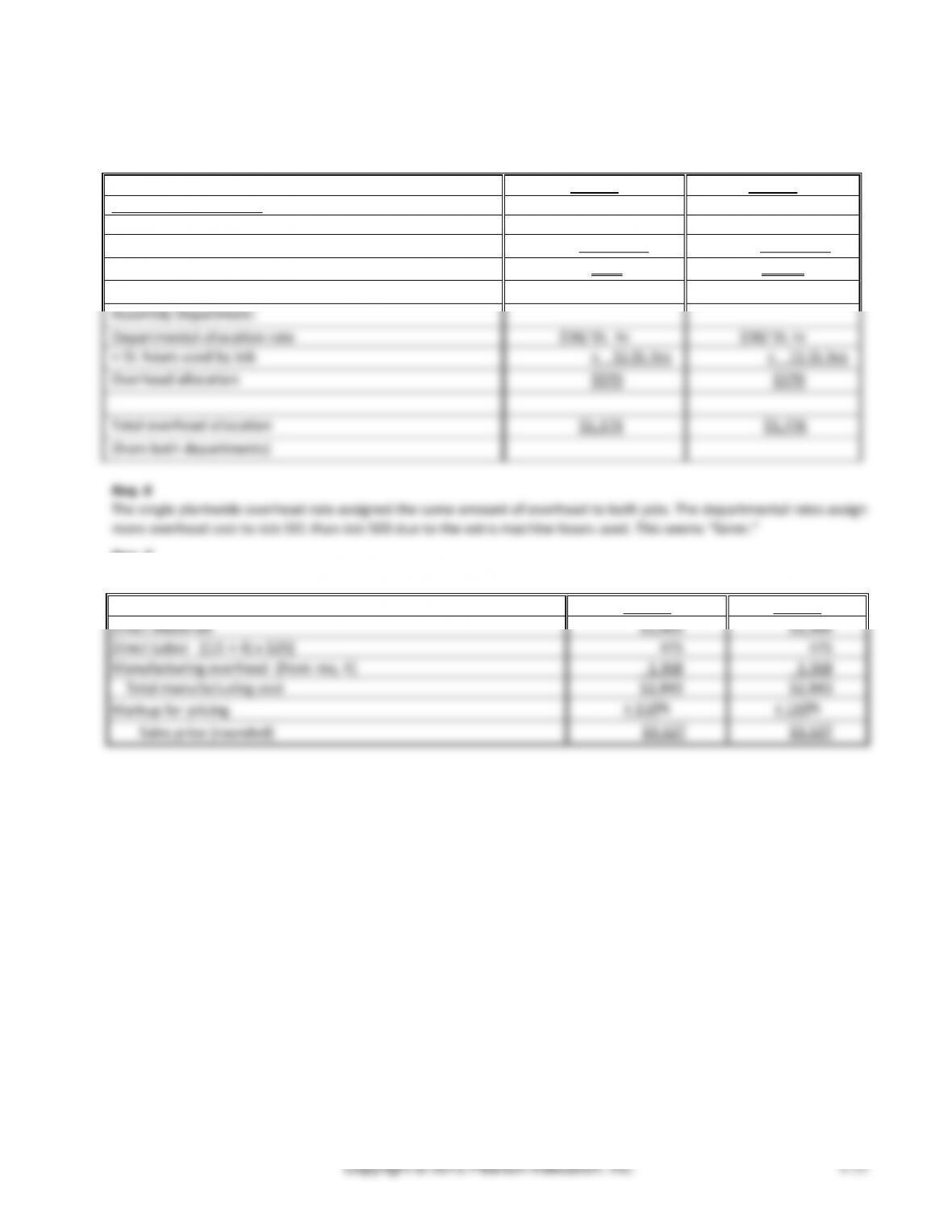

Overhead allocation based on departmental rates:

Job 450

Job 455

Machining Department:

Departmental allocation rate

$41/ MH

$41/ MH

× Machine hours used by Job

× 1 MH

× 7 MH

Overhead allocation

$41

$287

Finishing Department:

Departmental allocation rate

$28/ DL hr

$28/ DL hr

× DL hours used by Job

× 4 DL hrs

× 3 DL hrs

Overhead allocation

$ 112

$ 84

Total overhead allocation (from

both departments

$153

$371

Req. 5

Since the company sets its sales price at 125% of cost, and the job cost is affected by the allocation system used, its

sales price will also be affected by the allocation system it uses.

(15-20 min.) E4–29B

Req. 1

Northstar Company

Computation of Indirect Cost Allocation Rates

Activity

Total Estimated

Cost

Estimated Quantity of

Cost Allocation Base

Activity

Cost Allocation Rate

Materials handling

$ 12,000

÷

3,000 parts

=

$ 4 per part

Machine setups

$ 3,400

÷

10 setups

=

$340 per setup

Insertion of parts

$48,000

÷

3,000 parts

=

$ 16 per part

Finishing

$80,000

÷

2,000 hours

=

$ 40 per hour

Managerial Accounting 4e Solutions Manual

(continued) E4–29B

Req. 2

The amount of manufacturing overhead to be assigned to Job 420 is computed as follows

Job 420

Manufacturing overhead allocation

Activity

Actual Quantity of Cost

Allocation Base Used

Cost Allocation Rate

MOH assigned

Materials handling

150 parts

×

$4 / part

=

$ 600

Machine setups

2 setups

×

$340 / setup

=

680

Insertion of parts

150 parts

×

$16 / part

=

2,400

Finishing

100 hours

×

$ 40 / hr.

=

4,000

Total

$ 7,680

Req. 3

The amount of manufacturing overhead to be assigned to Job 510 is computed as follows

Job 510

Manufacturing overhead allocation

Activity

Actual Quantity of Cost

Allocation Base Used

Cost Allocation Rate

MOH assigned

Materials handling

500 parts

×

$4 / part

=

$ 2,000

Machine setups

4 setups

×

$340 / setup

=

1,360

Insertion of parts

500 parts

×

$16 / part

=

8,000

Finishing

310 hours

×

$ 40 / hr

=

12,400

Total

$23,760

(15-20 min.) E4–30B

Req. 1

Total overhead

$1,560,000

Divided by: Total machine hours

13,000

Predetermined MOH rate

$ 120

Req. 2

Cost of Job #356

Machine hours used

100

Multiplied by: Predetermined MOH rate

$120

Total MOH

$ 12,000

Job #356—traditional plantwide overhead rate

Direct material (270 lbs. ×$60/lb.)

$ 16,200

Direct labor (50 hrs. ×$15/hr.)

$750

MOH

$12,000

Total cost of job

$ 28,950

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) E4–30B

Job #356—ABC

Direct material (270 lbs. ×$60 per lb.)

$ 16,200

Direct labor (50 DL hours. ×$15 per DL hour)

$750

Machine hours 100 x $10 per machine hour

$1,000

No. of engineering changes 5 x $60 per change order

$300

Pounds of hazardous waste

generated 50 x $340 per lb of hazardous

$17,000

Total cost of job

$ 35,250

(15-20 min) E4–31B

Req. 1

Operating

overhead

Total professional hours

Current operating overhead allocation rate

$231,500

÷

10,000

=

$23.15 per

professional hour

Req. 2

Billing Calculations

Based on current allocation system

Professional time (27hours × $65 per hour)

$1,755.00

Operating overhead (27 hours × $23.15 per professional hour)

+ 625.05

Total cost of job

$2,380.05

Markup on cost

× 129%

Bill to client

$3,070.26

Req. 3

Activity

Cost

Total activity allocation base

Activity allocation rate

Transportation to clients

$ 10,500

÷

15,000 miles driven (6,000 +

9,000)

=

$0.70 per mile

Blueprint copying

35,000

÷

1,000 copies (550 + 450)

=

$35 per copy

Office support

186,000

÷

5,000 secretarial hours (2,300 +

2,700)

=

$37.20 per secretarial hour

To calculate the activity cost allocation rates, you must use the total activity for the year.

Managerial Accounting 4e Solutions Manual

(continued) E4–31B

Req. 4

Total cost of job

x

Markup percentage

=

Amount billed

$2,577.00*

x

129%

=

$3,324.33

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(15-20 min.) E4–32B

Req. 1

Total pharmacy cost allocation rate (using number of prescriptions):

Cost pools

Total annual

estimated cost

Pharmacy occupancy costs (utilities, rent, and other costs)

$96,000

Packaging supplies (bottles, bags, and other packaging)

$35,000

Professional training and insurance costs

$96,000

Total pharmacy overhead

$227,000

Divide by number of prescriptions

25,000

Total pharmacy cost allocation rate per prescription

$ 9.08

Req. 2

Cost assigned using traditional overhead allocation

Customer order #1102

5 prescriptions × $9.08

$45.40

Req. 3

Cost assigned using traditional overhead allocation

Customer order #1103

3 prescriptions × $9.08

$27.24

Req. 4

Cost Pools

Estimated Cost

Cost Drivers

Estimated Cost

Driver Activity

Cost

Allocation

Rate

Pharmacy Occupancy Costs

$96,000

Technician Hours

80,000

$1.20

Packaging Supplies

$35,000

Number of

Prescriptions

25,000

$1.40

Training and Insurance Costs

$96,000

Pharmacist Hours

24,000

$4.00

Req. 5

Customer order #1102

Used:

Used by this

order

Allocation

Rate

ABC assigned cost

Technician hrs. for order

0.5

$1.20

$ 0.60

Number of prescriptions

5

$1.40

$ 7.00

Pharmacist hours

2

$4.00

$ 8.00

Total ABC Cost

$ 15.60

Managerial Accounting 4e Solutions Manual

(continued) E4–32B

Req. 6

Customer order #1103

Used:

Used by this

order

Allocation

Rate

ABC assigned cost

Technician hrs. for order

0.5

$1.20

$ 0.60

Number of prescriptions

3

$1.40

$ 4.20

Pharmacist hours

2.5

$4.00

$ 10.00

Total ABC Cost

$ 14.80

Req. 7

The activity-based costing (ABC) allocation method would produce a more accurate product cost because this method

takes into account the specific resources used by each order.

Managerial Accounting 4e Solutions Manual

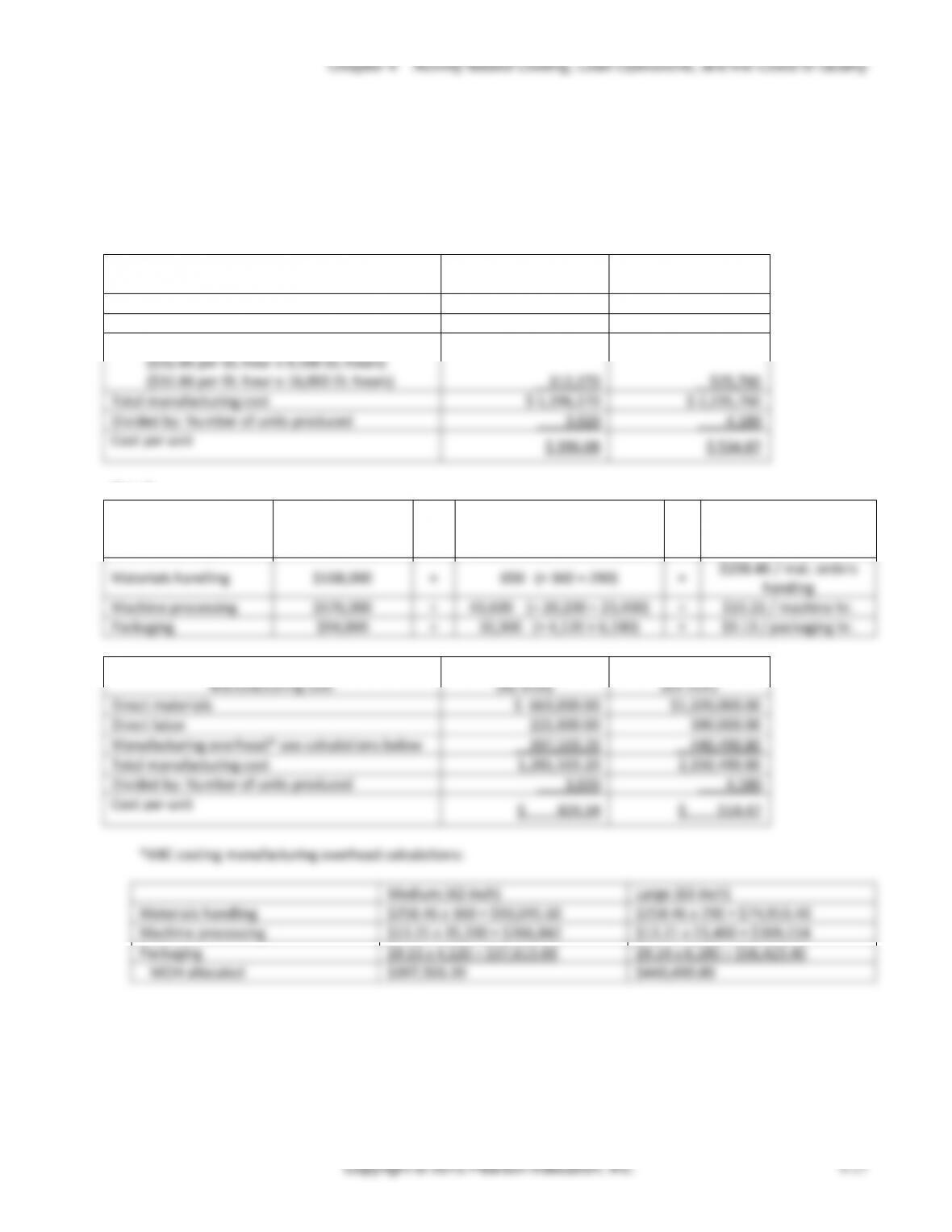

(continued) E4–33B

Req. 3

Medium

(42-inch)

Large

(63-inch)

Cost/unit using current system

$ 396.08

$534.87

Cost/unit using ABC

424.34

514.47

Overcosting/(Undercosting)

$(28.26)

20.40

Number of units produced

3,020

4,180

Total cost distortion

$(85,345.20)

$85,272.00

The Medium units had been undercosted and the Large units had been overcosted. Since the company sets its sales

price at 300% of manufacturing cost, the resulting sales price should have been about higher for the Medium units and

lower for the Large units than if ABC costing had been used.

(20-30 min.) E4–34B

Req. 1

Trudell Corp.

Total Budgeted Indirect Manufacturing Costs

Activity

Budgeted Quantity of

Cost Allocation Base

Activity Cost

Allocation Rate

Total Budgeted

Indirect Cost

Materials handling [(6.0 x 1,000) + (8.0 x 1,000)]

14,000

$ 3.78

$ 52,920

Machine setups 10 + 10

20

$305.00

6,100

Insertion of parts [(6.0 x 1,000) + (8.0 x 1,000)]

14,000

$ 31.00

434,000

Finishing [(1.2 x 1,000) + (3.2 x 1,000)]

4,400

$ 58.00

255,200

Total budgeted indirect cost

$748,220

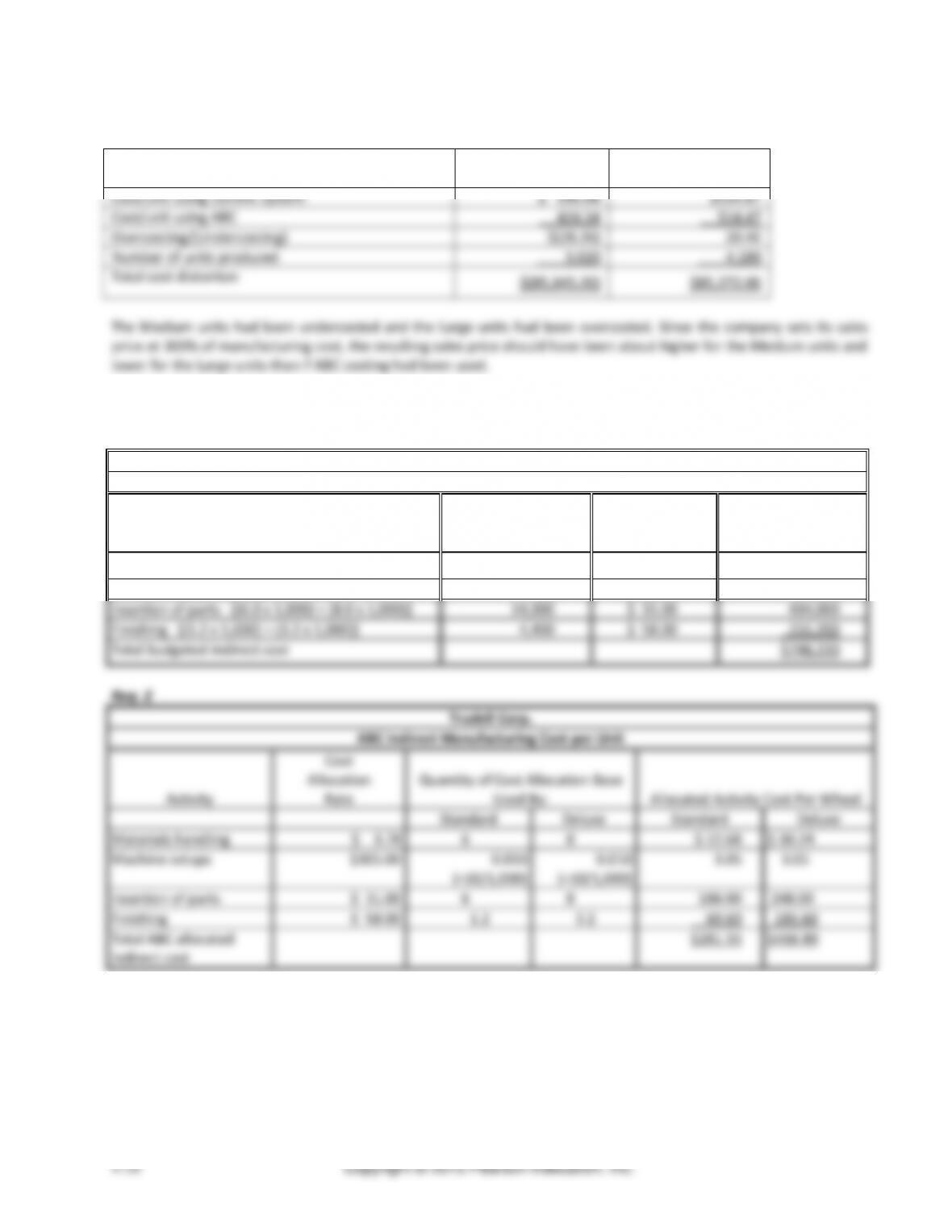

Req. 2

Trudell Corp.

ABC Indirect Manufacturing Cost per Unit

Activity

Cost

Allocation

Rate

Quantity of Cost Allocation Base

Used By:

Allocated Activity Cost Per Wheel

Standard

Deluxe

Standard

Deluxe

Materials handling

$ 3.78

6

8

$ 22.68

$ 30.24

Machine setups

$305.00

0.010

(=10/1,000)

0.010

(=10/1,000)

3.05

3.05

Insertion of parts

$ 31.00

6

8

186.00

248.00

Finishing

$ 58.00

1.2

3.2

69.60

185.60

Total ABC allocated

indirect cost

$281.33

$466.89

__________

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) E4–34B

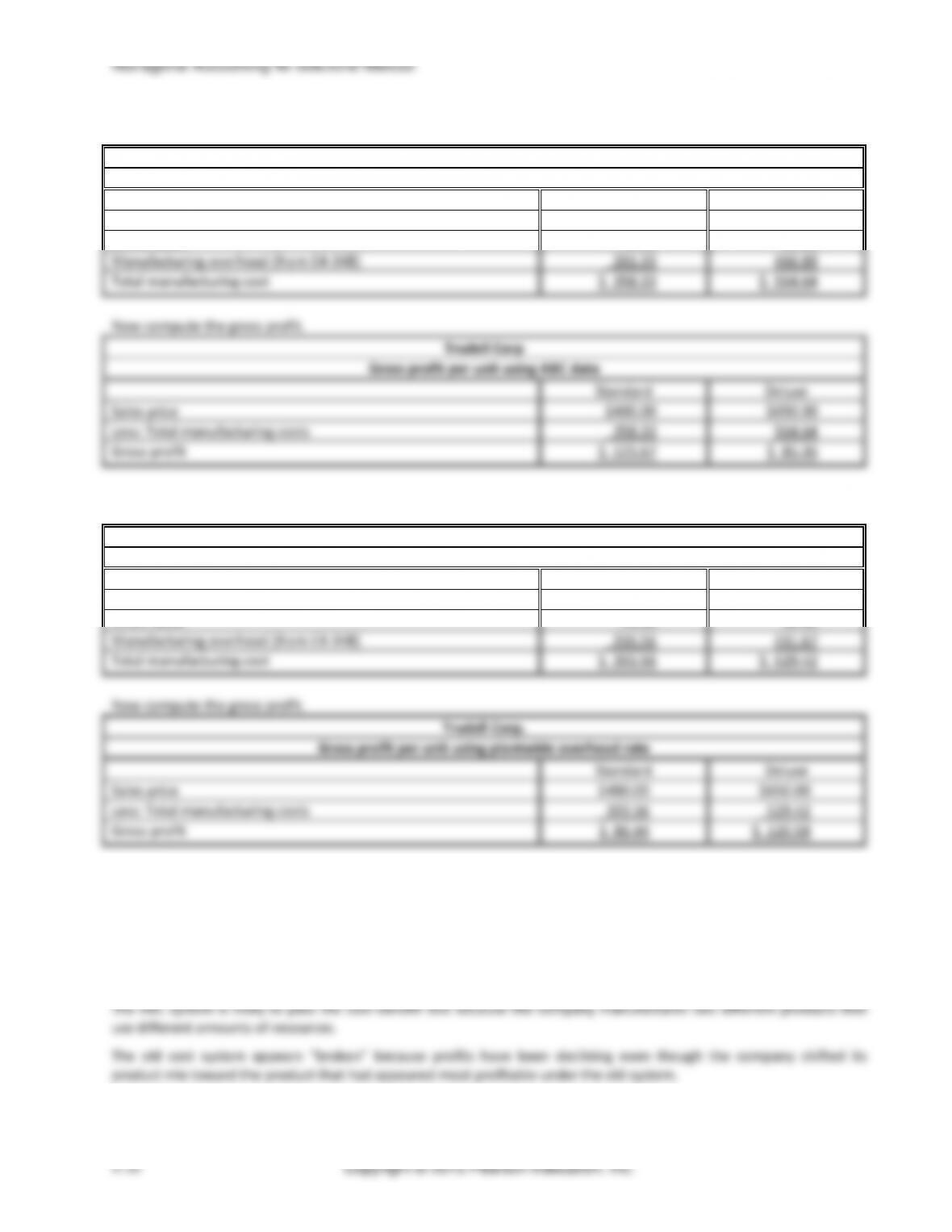

Req. 3

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(15-20 min) E4–36B

2. Traditional organization

4. Lean organization

6. Lean organization

8. Lean organization

10. Lean organization

12. Traditional organization

Managerial Accounting 4e Solutions Manual

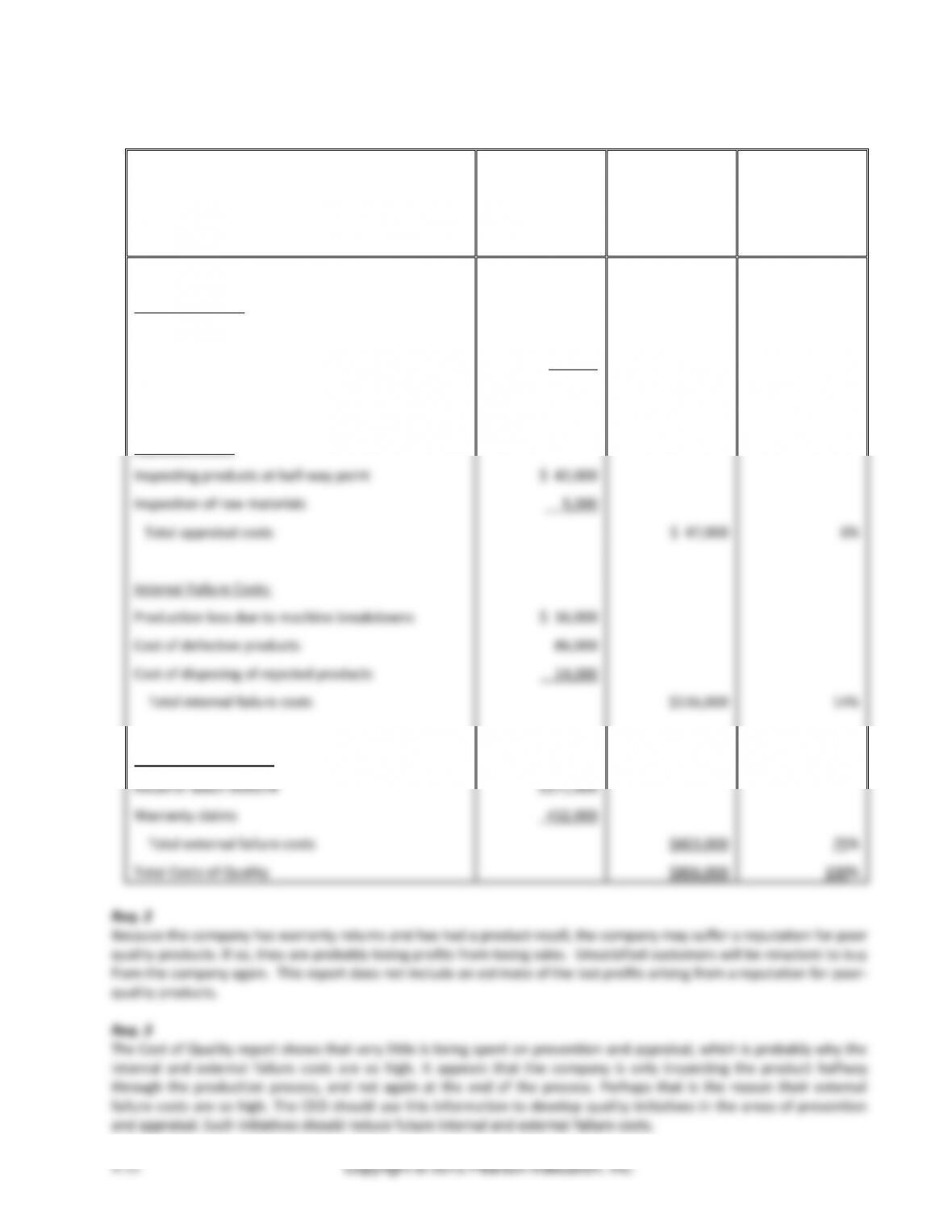

(15-20 min) E4–37B

Req. 1

Cost of Quality Report

Total Costs of

Quality

Percentage of

total costs of

quality (rounded)

Prevention Costs:

Personnel training

$ 34,000

Preventative maintenance

6,000

Total prevention costs

$ 40,000

5%

Appraisal Costs:

Inspecting products at half-way point

$ 42,000

Inspection of raw materials

5,000

Total appraisal costs

$ 47,000

6%

Internal Failure Costs:

Production loss due to machine breakdowns

$ 16,000

Cost of defective products

86,000

Cost of disposing of rejected products

14,000

Total internal failure costs

$116,000

14%

External Failure Costs:

Recall of Batch #59374

$171,000

Warranty claims

432,000

Total external failure costs

$603,000

75%

Total Costs of Quality

$806,000

100%

Req. 2

Because the company has warranty returns and has had a product recall, the company may suffer a reputation for poor

quality products. If so, they are probably losing profits from losing sales. Unsatisfied customers will be reluctant to buy

from the company again. This report does not include an estimate of the lost profits arising from a reputation for poor–

quality products.

Req. 3

The Cost of Quality report shows that very little is being spent on prevention and appraisal, which is probably why the

internal and external failure costs are so high. It appears that the company is only inspecting the product halfway

through the production process, and not again at the end of the process. Perhaps that is the reason their external

failure costs are so high. The CEO should use this information to develop quality initiatives in the areas of prevention

and appraisal. Such initiatives should reduce future internal and external failure costs.

Managerial Accounting 4e Solutions Manual

Problems (Group A)

(40 min.) P4–39A

Req. 1

Plantwide

overhead rate

=

Total manufacturing overhead

Total direct labor hours

=

$1,120,000

15,500* direct labor hours

=

$72 per direct labor hour (rounded)

*When calculating plantwide overhead rates, all direct labor

hours incurred in the plant are used.

Machining

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) P4-39A

Req. 5

Overhead allocation based on departmental rates:

Job 500

Job 501

Machining Department:

Departmental allocation rate

$67/ MH

$67/ MH

× Machine hours used by Job

× 9 MH

× 18 MH

Overhead allocation

$603

$1,206

Assembly Department:

Departmental allocation rate

$38/ DL hr

$38/ DL hr

× DL hours used by Job

× 15 DL hrs

× 15 DL hrs

Overhead allocation

$570

$570

Total overhead allocation

$1,173

$1,776

(from both departments)

Req. 7

Manufacturing cost and sales price using current costing system:

Job 500

Job 501

Direct Materials

$1,000

$1,000

Direct Labor [(15 + 4) x $25]

475

475

Manufacturing overhead (from req. 4)

1,368

1,368

Total manufacturing cost

$2,843

$2,843

Markup for pricing

× 110%

× 110%

Sales price (rounded)

$3,127

$3,127

Managerial Accounting 4e Solutions Manual

(continued) P4-39A

Req. 8

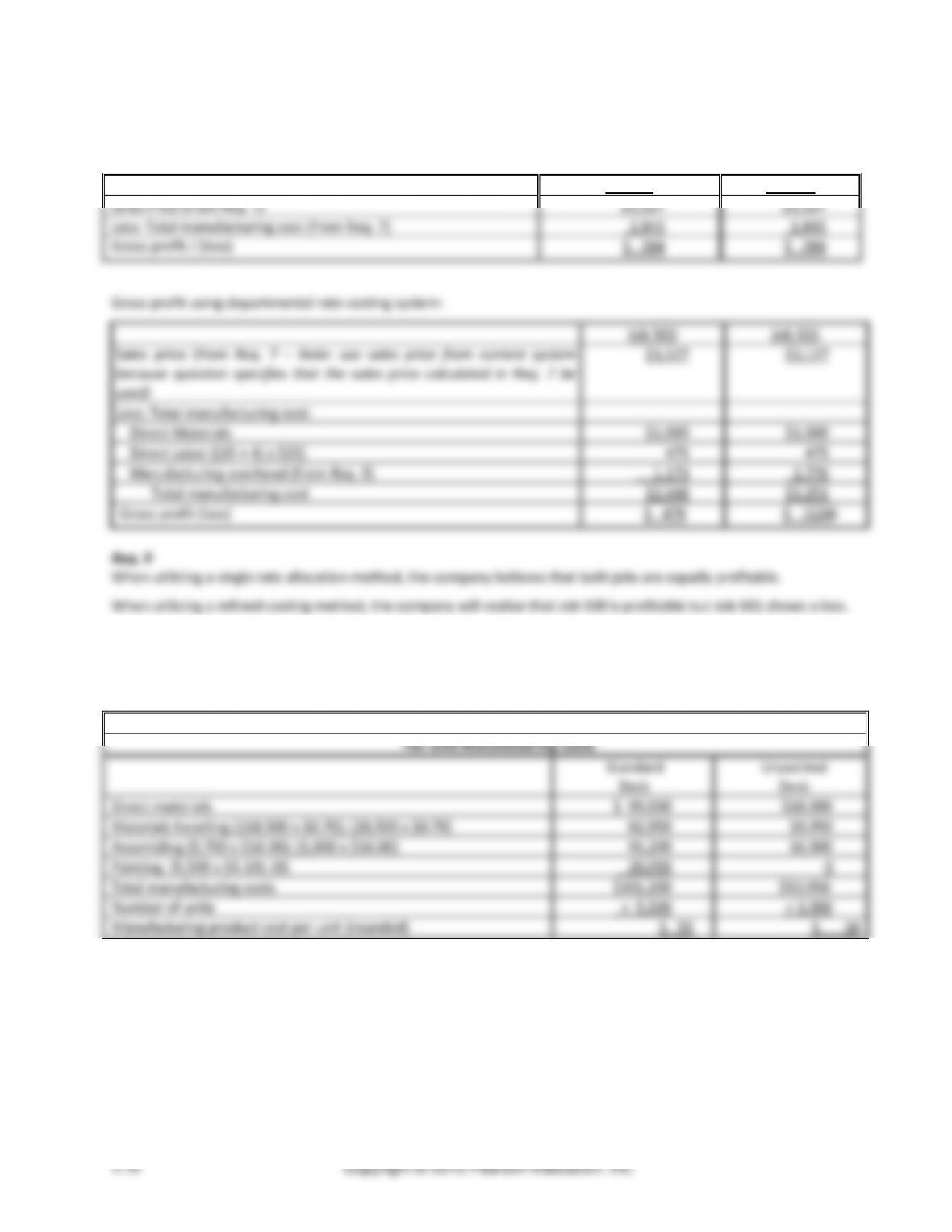

Gross profit using current costing system:

Job 500

Job 501

Sales Price (from Req. 7)

$3,127

$3,127

Less: Total manufacturing cost (from Req. 7)

2,843

2,843

Gross profit / (loss)

$ 284

$ 284

Gross profit using departmental rate costing system:

Job 500

Job 501

Sales price (from Req. 7 – Note: use sales price from current system

because question specifies that the sales price calculated in Req. 7 be

used)

$3,127

$3,127

Less: Total manufacturing cost:

Direct Materials

$1,000

$1,000

Direct Labor [(15 + 4) x $25]

475

475

Manufacturing overhead (from Req. 5)

1,173

1,776

Total manufacturing cost

$2,648

$3,251

Gross profit (loss)

$ 479

$ (124)

Req. 9

When utilizing a single rate allocation method, the company believes that both jobs are equally profitable.

When utilizing a refined costing method, the company will realize that Job 500 is profitable but Job 501 shows a loss.

(20-30 min.) P4–40A

Req. 1

Prescott Corp.

Per-Unit Manufacturing Costs

Standard

Desk

Unpainted

Desk

Direct materials

$ 99,000

$18,000

Materials handling (118,500 x $0.70); (28,500 x $0.70)

82,950

19,950

Assembling (5,700 x $16.00); (1,000 x $16.00)

91,200

16,000

Painting (5,500 x $5.10); (0)

28,050

0

Total manufacturing costs

$301,200

$53,950

Number of units

÷ 5,500

÷ 3,000

Manufacturing product cost per unit (rounded)

$ 55

$ 18

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(continued) P4–40A

Req. 2

Full Product Costs

Standard

Desk

Unpainted

Desk

Premanufacturing activities

$ 4

$ 3

Manufacturing product costs

55

18

Postmanufacturing activities

23

22

Full product cost per unit

$82

$43

Req. 3

Manufacturing product costs are reported in the financial statements.

Managers use full product costs for decisions, such as pricing and product emphasis.

Full product costs are reported in the costs of premanufacturing activities and postmanufacturing activities that are

expensed as incurred for external reporting. However, these costs often are assigned to products for internal decisions.

Req. 4

Full product cost………………………

$ 82.00

Plus: Desired profit…………………………..

41.00

Sales price per unit – standard desk

$123.00

(30-40 min.) P4–41A

Req. 1

Sawyer Pharmaceuticals

ABC Cost Allocation Rates

Materials Handling

Packaging

Quality Assurance

Estimated indirect

activity costs

$180,000

$460,000

$116,000

÷ Estimated cost

allocation base

÷ 18,000 kilos

÷ 2,600 hours

÷ 1,500 samples

Activity overhead rate (rounded)

$ 10 / kilo

$ 177 / hour

$ 77 / sample

Req. 2

Sawyer Pharmaceuticals

Activity Costs Per Unit

Commercial Container

Travel Pack

Materials handling (8,500 and 6,000) × $10

$ 85,000

$ 60,000

Packaging (1,200 and 400) × $177

212,400

70,800

Quality assurance (240 and 340) × $77

18,480

26,180

Total indirect costs

$314,880

$156,980

÷ Number of units

÷ 2,500

÷ 80,000

Indirect activity cost per unit (rounded)

$ 126.35

$ 1.96