Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Chapter 4

Activity-Based Costing, Lean Operations, and the Costs of

Quality

Quick Check

Answers:

Managerial Accounting 4e Solutions Manual

(continued) S4–2

Req. 2

The manufacturing cost of Job 484 is determined by summing the three manufacturing costs assigned to the job.

Direct materials

$2,350

Direct labor ($25 per hour × 12 hours)

300

Manufacturing overhead

216

Total Job Cost

$2,866

(5-10 min) S4-3

Req. 1

Manufacturing Overhead

Machine Hours

Plantwide Overhead Rate

$3,315,000

÷

17,000

=

$195 per machine hour

Req. 2

Production

Departments

Departmental

Manufacturing Overhead

Machine Hours

Departmental Overhead

Rates

Potato Chips

$2,014,000

÷

10,600

=

$190 per machine hour

Corn Chips

$672,000

÷

3,000

=

$224 per machine hour

Cheese Puffs

$ 629,000

÷

3,400

=

$185 per machine hour

TOTAL

$3,315,000

17,000

Req. 3

(5 min.) S4-4

Activity

Manufacturing Overhead

Cost Driver

Activity Cost Allocation Rate

Preparation

$572,000

÷

13,000 preparation

hours

=

$44 per preparation hour

Cooking and Draining

$925,000

÷

25,000 cooking and

draining hours

=

$37 per cooking and draining

hour

Packaging

$300,000

÷

6,000,000 packages

=

$0.05 per package

(5-10 min.) S4-5

Req. 1 and 2

The total amount of manufacturing overhead allocated to the order (and the amount of manufacturing overhead per

bag) is computed as follows:

Activity Cost Allocation Rate

Use of Cost Driver

Allocated Manufacturing

Overhead

$44 per preparation hour

16 preparation hours

$ 704

$37 per cooking and draining hour

30 cooking and draining hours

1,110

$0.05 per package

16,000 bags

800

TOTAL

$2,614

Number of bags

÷ 16,000

Manufacturing overhead per bag

$ 0.16 (rounded)

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Copyright © 2015 Pearson Education, Inc.

4-3

(continued) S4-5

Req. 3

In addition to the costs previously listed, the company needs to consider direct materials and direct labor.

(5-10 min.) S4-6

Req. 1

Activity

Estimated Total

Manufacturing Overhead

Costs

(A)

Estimated Total Usage of

Cost Driver

(B)

Activity Cost Allocation Rate

(A ÷ B)

Machine setup

$ 159,500

2,900 set-ups

$ 55 per setup

Machining

$ 720,000

4,800 machine hours

$150 per machine hour

Quality control

$ 264,000

4,400 tests run

$ 60 per QC test

Req. 2

Job Cost Record

JOB #557

Manufacturing Costs

Direct Materials

$1,250

Direct Labor:

John: 12 × $25 = $300

Allison: 4 × $28 = $112

412

Manufacturing Overhead: [(2 x $55) + (4 x $150) + (3 x $60)]

890

TOTAL JOB COST

$2,552

(15-20 min.) S4-7

a. Product-level

b. Batch-level

c. Product-level

(15-20 min.) S4-8

1. Facility-level

3. Product-level

5. Facility-level

7. Batch-level

9. Facility-level

Managerial Accounting 4e Solutions Manual

(5 min) S4-9

2. The company operates in a very competitive industry — more likely

likely

4. In bidding for jobs, managers lose bids they expected to win and win bids they expected to lose — more likely

6. The company produces high volumes of some of its products and low volumes of other products — more likely

(10-15 min.) S4–10

a. Value added

b. Value added

(5 min.) S4–11

a. Lean production system

b. Lean production system

c. Traditional production system

(10-15 min.) S4–12

1. Incremental cost of using a higher grade raw material — prevention

3. Lost productivity due to machine breakdown — internal failure

5. Warranty repairs — external failure

7. Legal fees from customer lawsuits — external failure

9. Redesigning the production process — prevention

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

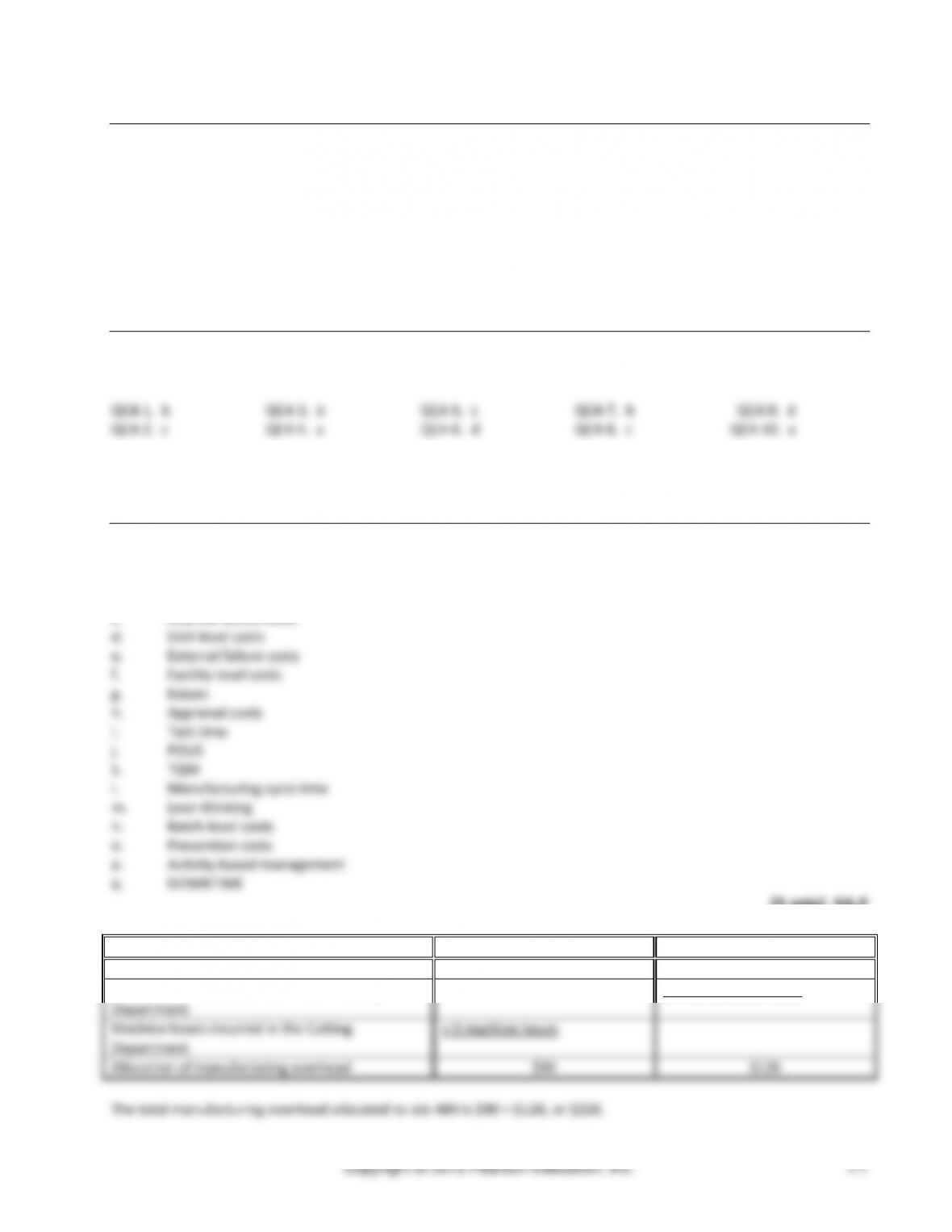

(10-15 min.) S4–13

Req. 1

Cost (Benefit)

Analysis

Costs (Savings)

Prevention costs:

Negotiating with and training suppliers to obtain higher quality materials and on-time

delivery

$ 550,000

Redesigning the speakers to make them easier to manufacture

1,405,000

Appraisal costs:

Additional 20 minutes of testing for each speaker

604,000

Avoid inspection of raw materials

(404,000)

Internal failure costs:

Rework avoided because of fewer defective units

(656,000)

Avoid lost profits from lost production due to rework

(309,000)

External failure costs:

Reduced warranty repair costs

(208,000)

Avoid lost profits from lost sales due to disappointed customers

(858,000)

Net cost (benefit) from implementing quality program

$ 124,000

Req. 2

The company should not implement the new quality program. The company would lose $124,000 by implementing the

new program.

(5-10 min.) S4–14

1. Internal failure cost

2. Appraisal cost

(15-20 min) S4–15

a. Defects

b. Overproduction

Managerial Accounting 4e Solutions Manual

(5 min) S4–16

1.

Shawn, an accountant at the Booth Corporation,

did not attend the training for the new activity-

based costing system because he figures it will not

be much different from the current allocation

system.

Competence – Maintain an appropriate

level of professional expertise by

continually developing knowledge and

skills.

2.

Joanna receives an iPod from a salesman at a lean

consulting group. She keeps the iPod, even though

she knows that her department will be responsible

for hiring a consulting firm to come in to offer lean

training sessions next year.

Integrity – Mitigate actual conflicts of

interest, regularly communicate with

business associates to avoid apparent

conflicts of interest. Advise all parties of

any potential conflicts.

3.

Noah, the plant manager, does not disclose the

quality issues he is aware of in the current

production process. He figures that he can get

them resolved in the next few months.

Credibility – Disclose all relevant

information that could reasonably be

expected to influence an intended user’s

understanding of the reports, analyses, or

recommendations.

4.

Connery Corporation has an activity-based costing

system. Percy prepares reports each month that

are long and full of facts. The reports are hard to

understand for anyone but Percy.

Competence – Provide decision support

information and recommendations that are

accurate, clear, concise, and timely.

5.

Perkins Company operates in highly competitive

environment and has developed some proprietary

processes that allow it to maintain a market lead.

Simon, the CFO, does not have employees sign

non-disclosure agreements because he feels that

they are all family. He avoids talking about the

topic.

Confidentiality – Inform all relevant parties

regarding appropriate use of confidential

information. Monitor subordinates’

activities to ensure compliance.

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Exercises (Group A)

(15-20 min.) E4–17A

Req. 1

Plantwide

overhead rate

=

Estimated total manufacturing costs

Estimated cost allocation base

=

$1,450,000

21,000* direct labor hours

=

$69 per direct labor hour (rounded)

*When calculating plantwide overhead rates, all direct labor

hours incurred in the plant are used.

Req. 2

Departmental overhead rate

=

Total department overhead

Cost allocation base (estimated)

Machining Dept. overhead rate

=

$625,000

15,300 machine hours

=

$41 per machine hour (rounded)

Finishing Dept. overhead rate

=

$825,000

17,800** direct labor hours

=

$46 per direct labor hour (rounded)

**When calculating the finishing departmental rate, only the direct labor hours incurred in the finishing department

are used.

Managerial Accounting 4e Solutions Manual

(continued) E4-17A

Req. 3

Overhead allocation based on single, plantwide rate:

Job 450

Job 455

Cost allocation base (actual)

7 DL hours

7 DL hours

× Plantwide cost allocation

rate

× $69/ DL hour

× $69 / DL hour

Overhead allocation

$ 483

$ 483

Req. 4

Overhead allocation based on departmental rates:

Job 450

Job 455

Machining Department:

Departmental allocation rate

$41/ MH

$41/ MH

× Machine hours used by Job

× 1 MH

× 6 MH

Overhead allocation

$41

$246

Finishing Department:

Departmental allocation rate

$46/ DL hr

$46/ DL hr

× DL hours used by Job

× 6 DL hrs

× 5 DL hrs

Overhead allocation

$276

$230

Total overhead allocation (from

both departments

$ 317

$ 476

Req. 5

The single plantwide rate overcosts Job 450 and overcosts Job 455. Since the company sets the sales price at 125% of

cost, and the job cost is affected by the allocation system used, the sales price will be affected by the allocation system

used.

Managerial Accounting 4e Solutions Manual

(15-20 min.) E4–19A

Req. 1

Total overhead

$ 2,190,000

Divided by: Total machine hours

15,000

Predetermined MOH rate

$ 146

Cost of Job #356

Machine hours used

90

Multiplied by: Predetermined MOH rate

$ 146

Total MOH

$ 13,140

Job #356—traditional plantwide overhead rate

Direct material

300 lbs. × $70/lb.

$ 21,000

Direct labor

20 hrs. ×$25/hr.

500

MOH

13,140

Total cost of job

$ 34,640

Req. 2

Job #356—ABC

Direct material

300 lbs. × $70 per lb

$ 21,000

Direct labor

20 DL hours × $25 per DL

hour

500

Machine hours

90 x $40 per machine hour

3,600

No. of engineering change orders

9 x $90 per change order

810

Pounds of hazardous waste

generated

50 x $330 per lb of hazardous

16,500

Total cost of job

$ 42,410

ABC cost allocation rates:

Machine maintenance: $600,000 / 15,000 = $40 per machine hour

Engineering: $270,000 / 3,000 = $90 per change order

Hazardous waste: $1,320,000 / 4,000 = $330 per pound of hazardous waste

Req. 3

The cost estimate based on the activity-based costing (ABC) rates would provide more useful information because this

cost estimate takes into account the specific resources used by each product. This information can be used to price

jobs based on more accurate costs.

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

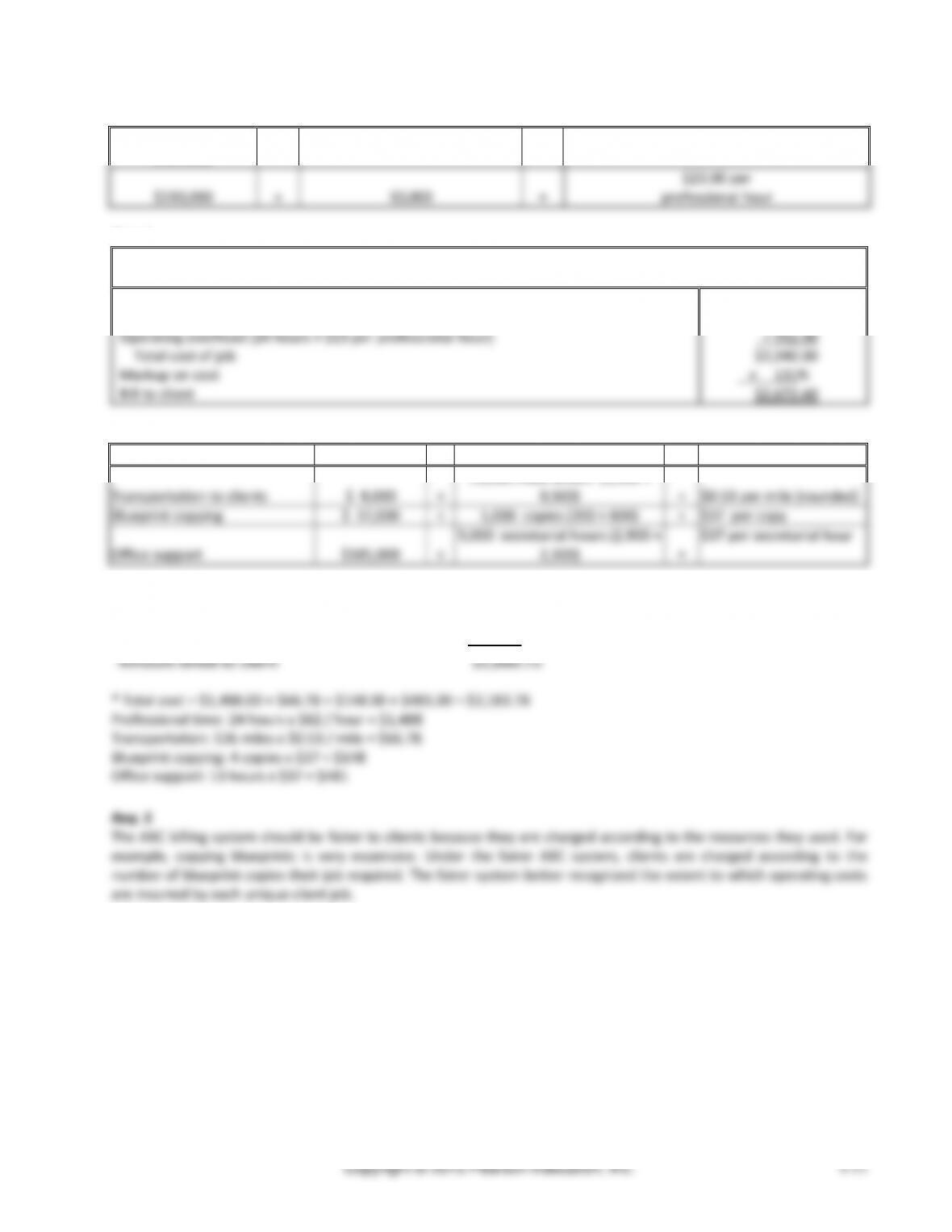

(15-20 min) E4–20A

Req. 1

Operating

overhead

Total professional hours

Current operating overhead allocation rate

$230,000

÷

10,000

=

$23.00 per

professional hour

Req. 2

Billing Calculations

Based on current allocation system

Professional time (24 hours × $62 per hour)

$1,488.00

Operating overhead (24 hours × $23 per professional hour)

+ 552.00

Total cost of job

$2,040.00

Markup on cost

× 131%

Bill to client

$2,672.40

Req. 3

Activity

Cost

Total activity allocation base

Activity allocation rate

Transportation to clients

$ 8,000

÷

15,000 miles driven (5,500 +

9,500)

=

$0.53 per mile (rounded)

Blueprint copying

$ 37,000

÷

1,000 copies (200 + 800)

=

$37 per copy

Office support

$185,000

÷

5,000 secretarial hours (2,900 +

2,100)

=

$37 per secretarial hour

Req. 4

Total cost of job

$2,183.78 *

Multiplied by: Markup percentage

131%

Amount billed to client

$2,860.75

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

Req. 7

The activity-based costing (ABC) would produce a more accurate product cost because this method takes into account

the specific resources used by each order.

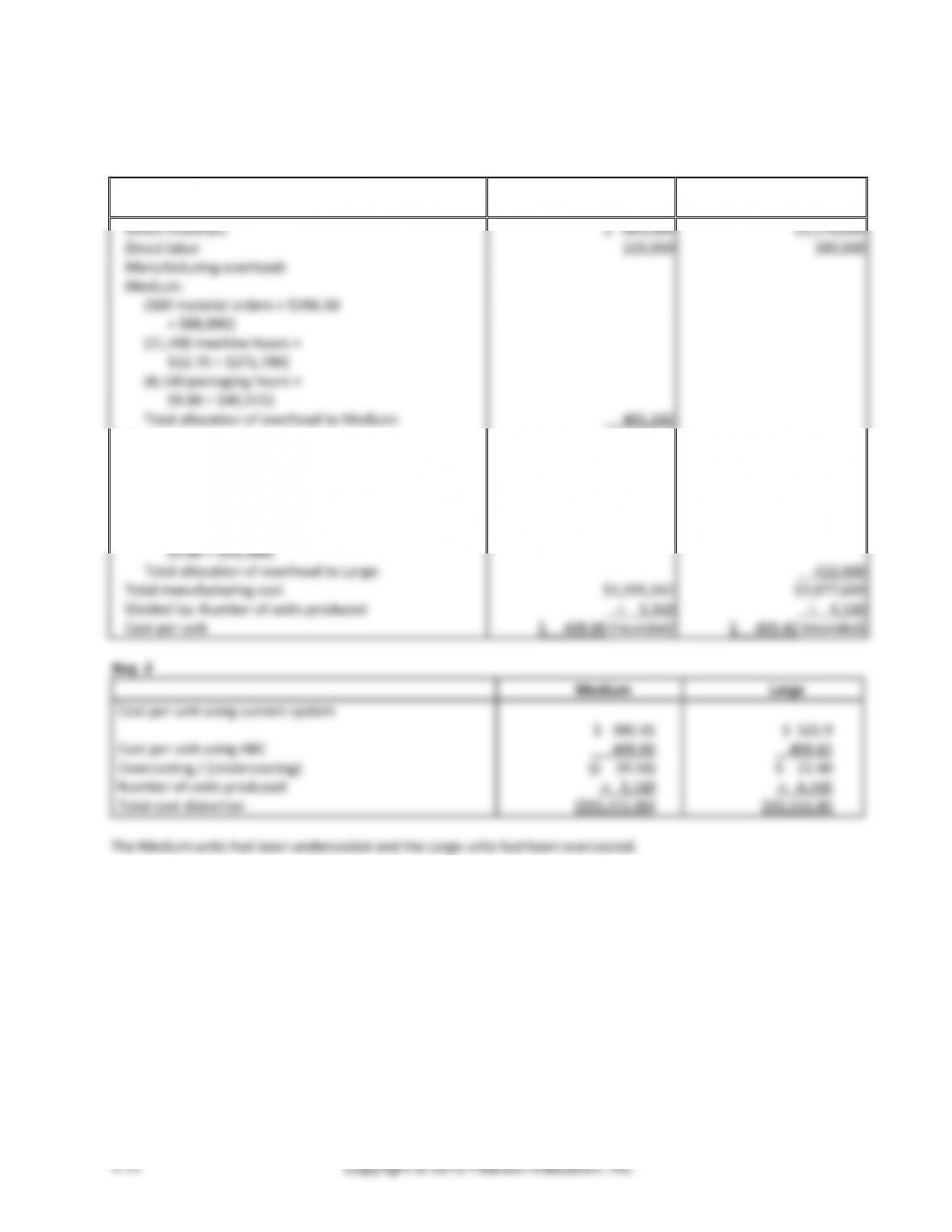

(20-25 min.) E4–22A

Managerial Accounting 4e Solutions Manual

(continued) E4–22A

Req. 2 (continued)

Then, apply them to the two products:

Manufacturing Cost

Medium

(42-inch)

Large

(63-inch)

Direct materials

$ 669,000

$1,270,000

Direct labor

225,000

385,000

Manufacturing overhead:

Medium:

(300 material orders × $296.30

= $88,890)

(21,400 machine hours ×

$12.70 = $271,780)

(4,140 packaging hours ×

$9.80 = $40,572)

Total allocation of overhead to Medium:

401,242

Large:

(240 material orders × $296.30

= $71,112)

(23,000 machine hours ×

$12.70 = $292,100)

(6,060 packaging hours ×

$9.80 = $59,388)

Total allocation of overhead to Large:

422,600

Total manufacturing cost

$1,295,242

$2,077,600

Divided by: Number of units produced

÷ 3,160

÷ 4,160

Cost per unit

$ 409.89 (rounded)

$ 499.42 (rounded)

Req. 3

Medium

Large

Cost per unit using current system

$ 380.31

$ 521.9

Cost per unit using ABC

409.89

499.42

Overcosting / (Undercosting)

($ 29.58)

$ 22.48

Number of units produced

× 3,160

× 4,160

Total cost distortion

($93,472.80)

$93,516.80

The Medium units had been undercosted and the Large units had been overcosted.

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

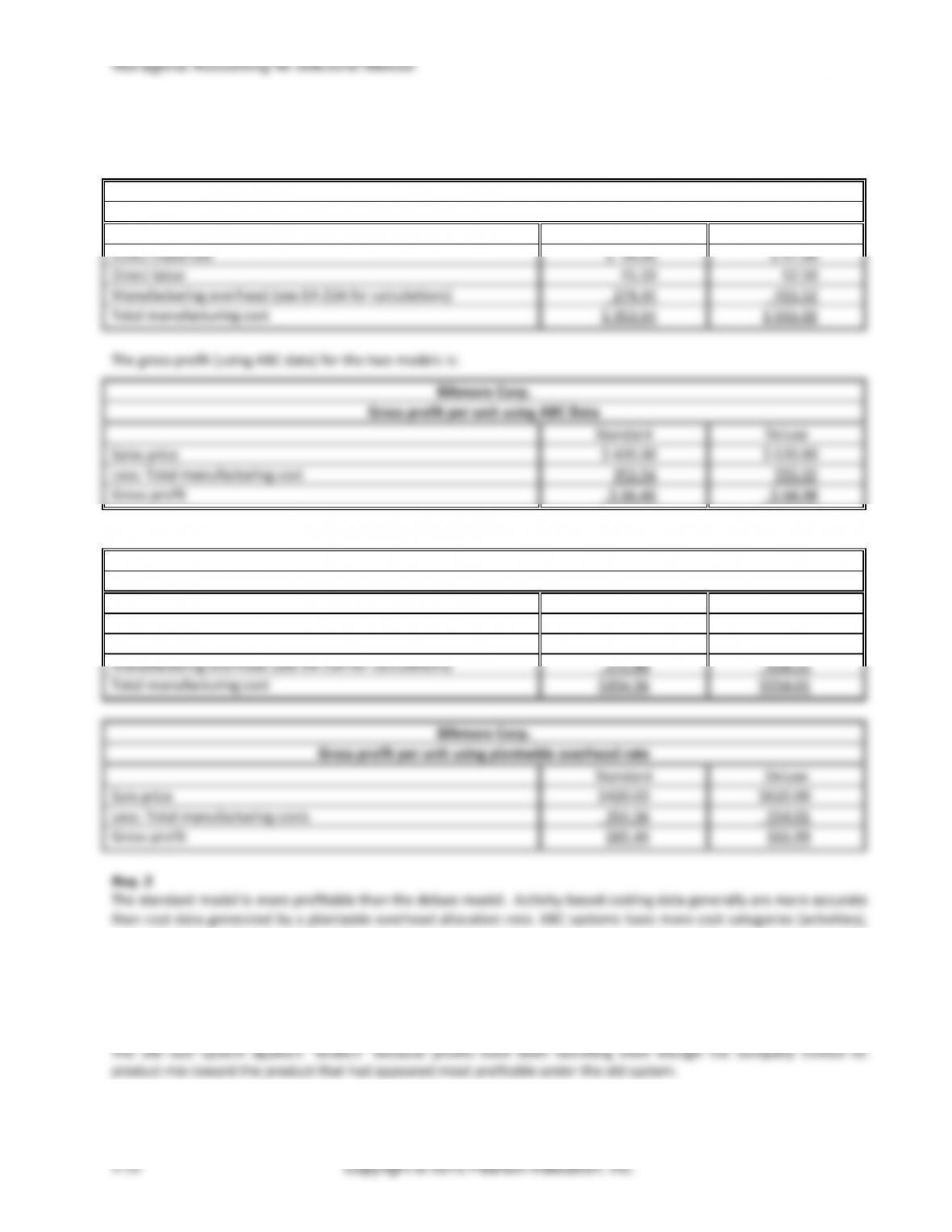

(20-30 min.) E4–23A

Req. 1

Biltmore Corp.

Total Budgeted Indirect Manufacturing Costs

Activity

Budgeted Quantity of

Cost Allocation Base

Activity Cost

Allocation Rate

Total Budgeted

Indirect Cost

Materials handling [(6 x 1,000) + (8 x 1,000)]

14,000

$ 3.84

$ 53,760

Machine setups 20 + 20

40

$330.00

13,200

Insertion of parts [(6 x 1,000) + (8 x 1,000)]

14,000

$ 30.00

420,000

Finishing [(1.2 x 1,000) + (3.3 x 1,000)]

4,500

$ 54.00

243,000

Total budgeted indirect cost

$729,960

Req. 2

Biltmore Corp.

ABC Indirect Manufacturing Cost per Unit

Activity

Cost

Allocation

Rate

Quantity of Cost Allocation Base

Used By:

Allocated Activity Cost Per

Wheel

Standard

Deluxe

Standard

Deluxe

Materials handling

$ 3.84

6

8

$ 23.04

$ 30.72

Machine setups

$330.00

0.020

(=20/1,000)

0.020

(=20/1,000)

6.60

6.60

Insertion of parts

$ 30.00

6

8

180.00

240.00

Finishing

$ 54.00

1.2

3.3

64.80

178.20

Total ABC allocated

indirect cost

$274.44

$455.52

Req. 3

Total budgeted manufacturing overhead

=

$729,960 (Req. 1)

Total budgeted direct labor hours [(2.0 x 1,000) + (3.3 x 1,000)]

=

5,300

Plantwide overhead rate

=

$137.73 / DL hour

(rounded)

Chapter 4 Activity-Based Costing, Lean Operations, and the Costs of Quality

(15-20 min) E4–25A

1. Roles of plant employees — At lean producers, plant employees tend to have broader roles. They are cross–

the job.

2. Manufacturing cycle times — Lean producers put great emphasis on shortening their manufacturing cycle

3. Quality — Lean producers stress high quality in every aspect of production. Since lean producers do not carry

4. Inventory levels — Lean production systems strive to maintain low inventory levels. Lean producers try to

5. Batch sizes — Lean production systems produce units in much smaller batches than traditional production

6. Set-up times — Lean production systems stress short set-up times so that they can produce and deliver the

7. Workplace organization — Lean companies use a workplace organization system called “5s” (sort, set in order,

shine, standardize, sustain) to keep their work cells clean and organized. The goal of workplace organization

Managerial Accounting 4e Solutions Manual

(15-20 min) E4–26A

Req. 1

Cost of Quality Report for Healthy Snacks Corp

Total Costs of

Quality

Percentage of

total costs of

quality (rounded)

Prevention Costs:

Personnel training

$ 36,000

Preventative maintenance

9,000

Total prevention costs

$ 45,000

6%

Appraisal Costs:

Inspecting products at halfway point

$ 55,000

Inspection of raw materials

5,000

Total appraisal costs

$ 60,000

7%

Internal Failure Costs:

Production loss due to machine breakdowns

$ 16,000

Cost of defective products

80,000

Cost of disposing of rejected products

11,000

Total internal failure costs

$107,000

13%

External Failure Costs:

Recall of Batch #59374

$175,000

Warranty claims

416,000

Total external failure costs

$591,000

74%

Total Costs of Quality

$803,000

100%

Req. 2

Because the company has warranty returns and has had a product recall, the company may suffer a reputation for poor

quality products. If so, they are probably losing profits from losing sales. Unsatisfied customers will be reluctant to buy

from the company again. This report does not include an estimate of the lost profits arising from a reputation for poor–

quality products.

Req. 3

The Cost of Quality report shows that very little is being spent on prevention and appraisal, which is probably why the

internal and external failure costs are so high. It appears that the company is only inspecting the product halfway

through the production process, and not again at the end of the process. Perhaps that is the reason their external

failure costs are so high. The CEO should use this information to develop quality initiatives in the areas of prevention

and appraisal. Such initiatives should reduce future internal and external failure costs.

Managerial Accounting 4e Solutions Manual

Exercises (Group B)

(15-20 min.) E4–28B

Req. 1

Plantwide

overhead rate

=

Total manufacturing overhead

Cost allocation base (estimated)

=

$1,100,000

21,000 direct labor hours

=

$ 52 per direct labor hour

Req. 2

Department overhead rate

=

Total department overhead

Cost allocation base (estimated)

Machining Dept. overhead rate

=

$600,000

14,500 machine hours

=

$41 per machine hour*

Finishing Dept. overhead rate

=

$500,000

17,900 direct labor hours

=

$28 per direct labor hour*

*Rounded to the nearest dollar.

Req. 3

Overhead allocation based on single, plantwide rate:

Job 450

Job 455

Total direct labor hours

5 DL hours

5 DL hours

× Plantwide allocation rate

× $52/ DL hour

× $52/ DL hour

Overhead allocation

$260

$260