Chapter 3 Job Costing

Job Cost Record

Job Number: 1102

Customer: Wild Birds, Inc.

Job description: 24 Model 3F (platform bird feeders)

Date Started: Sep. 14 Date Completed: ________

Manufacturing Cost Information:

Cost Summary

Direct Materials

Req. #1250

$221

Direct Labor

No. #912 (4 hours) $44

No. #913 (5 hours) $35

$ 79

Manufacturing Overhead

9 hours x $3 per direct labor hour

$ 27

Total Job Cost

$327

Number of units

÷ 24

Cost per Unit

$ 13.63

(10 min.) E3-32B

Req. 1

Calculate the predetermined overhead rate:

Predetermined

=

$63,750

overhead rate

4,250 direct labor hours

=

$15 per direct labor hour

Chapter 3 Job Costing

(continued) E3-34B

Req. 2

Job #308

Total job cost

$22,600

25% markup

× 125%

Total price to charge

$28,250

Job #308

Total job cost

$22,600

Add 25% Mark-up on manufacturing cost

(25% × $22,600)

+ 5,650

Total price to charge

$28,250

Virgin materials

150

$ 4.40

$ 660.00

Recycled-content materials

350

$ 3.20

1,120.00

Direct labor

20

$15.00

300.00

Manufacturing overhead (based on DLH)

20

$8.00

160.00

Total job cost

$2,240.00

Req. 2

Virgin materials

150

Recycled-content materials

350

70% (=350/500)

Total pounds

500

This job meets the 40% recycled-content requirement.

Managerial Accounting 4e Solutions Manual

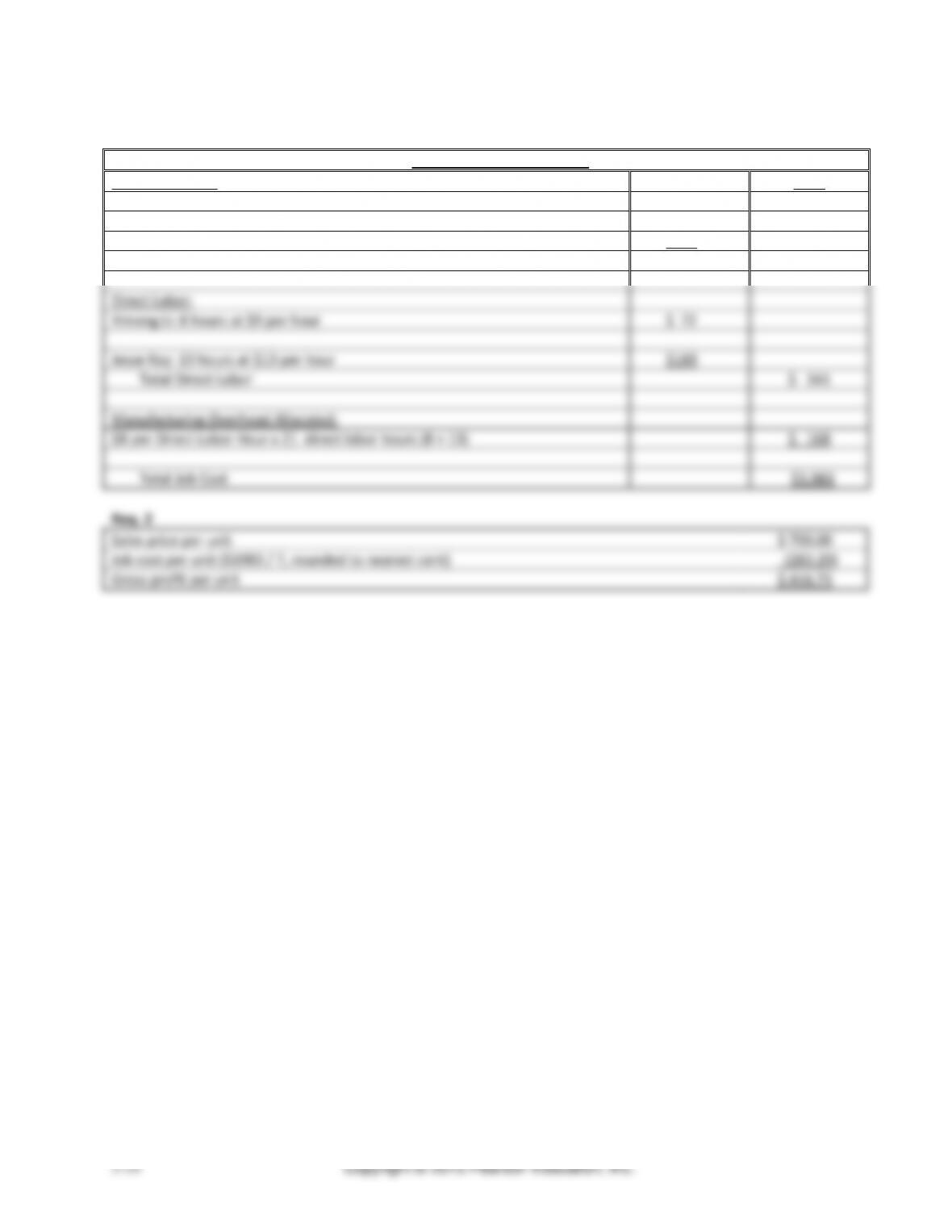

(15 min.) E3–36B

Req. 1

Job Cost Record for Job 310

Direct Materials:

Total

Lumber: 51 units at $9 per unit

$459

Padding: 15 yards at $21 per yard

$315

Upholstery fabric: 32 yards at $25 per yard

$800

Total Direct Materials

$1,574

Direct Labor:

Yimeng Li: 8 hours at $9 per hour

$ 72

Jesse Ray: 13 hours at $13 per hour

$169

Total Direct Labor

$ 241

Manufacturing Overhead Allocated:

$8 per Direct Labor Hour x 21 direct labor hours (8 + 13)

$ 168

Total Job Cost

$1,983

Req. 2

Sales price per unit

$ 700.00

Job cost per unit ($1983 / 7, rounded to nearest cent)

(283.29)

Gross profit per unit

$ 416.71

Chapter 3 Job Costing

(10 min.) E3–37B

Req. 1

First, calculate the predetermined overhead rate:

Predetermined manufacturing

=

$348,950

overhead rate

9,970 direct labor hours

=

$35 per direct labor hour

Next, calculate the total job cost:

Direct materials

$ 25,400

Direct labor

(1,500 direct labor hours × $13 per direct labor hour)

19,500

Manufacturing overhead

(1,500 direct labor hours × $35 per direct hour)

52,500

Total job cost

$97,400

Total job cost

$97,400

30% markup

× 130%

Bid price

$126,620

or, alternatively:

Total job cost

$97,400

Add 30% markup on manufacturing cost

(30% × $97,400)

+ 29,220

Bid price

$126,620

Req. 2

First, calculate the predetermined overhead rate:

Predetermined manufacturing

=

$348,950

overhead rate

13,958 machine hours

=

$25 per machine hour

Next, calculate the total job cost:

Direct materials

$25,400

Direct labor

(1,500 direct labor hours × $13 per direct labor hour)

19,500

Manufacturing overhead

(2,000 machine hours × $25 per machine hour)

50,000

Total job cost

$94,900

Managerial Accounting 4e Solutions Manual

(continued) E3–37B

Then, compute bid price:

Total job cost

$ 94,900

30% markup

× 130%

Bid price

$123,370

Total manufacturing cost of job

$ 94,900

Add 30% markup on manufacturing cost

(30% × $94,900)

+ 28,470

Bid price

$123,370

(15-20 min.) E3–38B

Req. 1

Predetermined manufacturing overhead rate

=

$580,000

72,500 machine hours

=

$8 per machine hour

Req. 2

Allocated manufacturing overhead

=

57,000 machine hours ×

$8 per machine hour

=

$456,000

Chapter 3 Job Costing

(10-15 min.) E3–39B

Req. 1

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Manufacturing Overhead

$434,500

Accumulated Depreciation — plant and equipment

405,000

Property Tax Payable

21,500

Wages Payable

8,000

Req. 2

Note: Predetermined overhead rate $8

per MH

=

$580,000

72,500 machine hours

Journal Entry

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory

456,000

Manufacturing Overhead

456,000

To record manufacturing

overhead allocated

DATE

21,500

21,500

Managerial Accounting 4e Solutions Manual

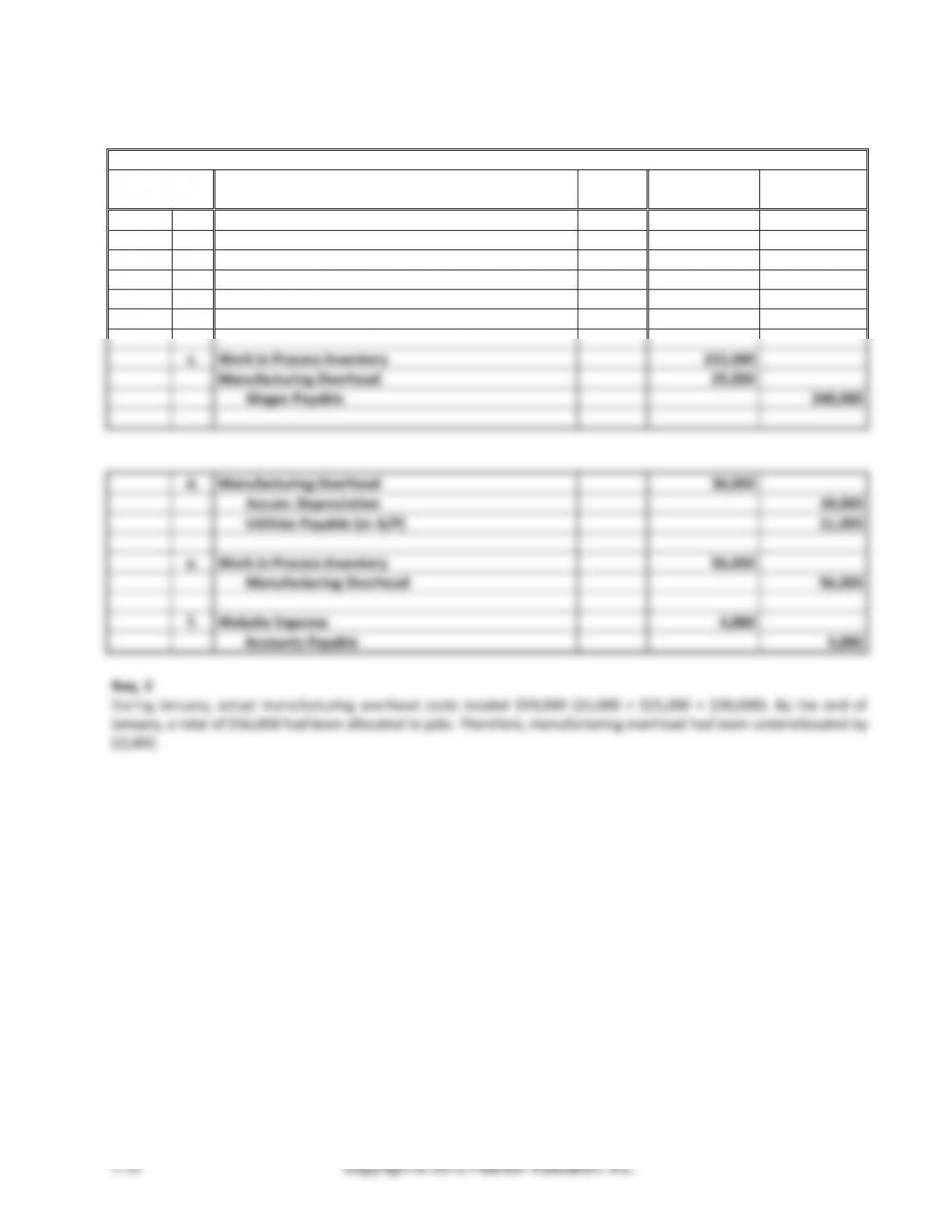

(10 min.) E3-40B

Req. 1

Journal Entry

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

a.

Raw Materials Inventory

180,000

Accounts Payable

180,000

b.

Work in Process Inventory

158,000

Manufacturing Overhead

4,000

Raw Materials Inventory

162,000

c.

Work in Process Inventory

215,000

Manufacturing Overhead

25,000

Wages Payable

240,000

d.

Manufacturing Overhead

30,000

Accum. Depreciation

19,000

Utilities Payable (or A/P)

11,000

e.

Work in Process Inventory

56,000

Manufacturing Overhead

56,000

f.

Website Expense

4,000

Accounts Payable

4,000

Req. 2

During January, actual manufacturing overhead costs totaled $59,000 ($4,000 + $25,000 + $30,000). By the end of

January, a total of $56,000 had been allocated to jobs. Therefore, manufacturing overhead had been underallocated by

$3,000.

Chapter 3 Job Costing

(10 min.) E3–41B

1.

Direct materials used…………………

$ 28,500

2.

Indirect materials used………………

$ 6,500

3.

Direct labor………………………………

$ 64,000

4.

Indirect labor…………………………….

$ 10,000

5.

Cost of goods manufactured…………

$126,000

6.

Cost of goods sold……………………

$115,500

7.

Actual manufacturing overhead

($6,500 + $10,000 + $38,000)……….

$ 54,500

8.

Allocated manufacturing overhead….

$ 42,000

9.

Predetermined manufacturing

overhead rate, as a % of direct

labor cost; $42,000 / $64,000………… (rounded)

66%

10.

Manufacturing overhead is

($54,500 actual − $42,000 allocated) = $ 12,500 underallocated

Chapter 3 Job Costing

(10 min.) E3-43B

Req. 1

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

a.

Raw Materials Inventory

190,000

Accounts Payable

190,000

b.

Work in Process Inventory

152,000

Manufacturing Overhead

22,000

Raw Materials Inventory

174,000

c.

Work in Process Inventory

190,000

Manufacturing Overhead

35,000

Wages Payable

225,000

d.

Manufacturing Overhead

30,000

Accum. Depreciation

20,000

Utilities Payable (or A/P)

10,000

e.

Work in Process Inventory

81,000

Manufacturing Overhead

81,000

Req. 2

During January, actual manufacturing overhead costs totaled $87,000, while only $81,000 had been allocated to jobs.

Therefore, by the end of January, manufacturing overhead had been underallocated by $6,000.

Note: T-account not required.

Manufacturing Overhead

(Actual)

(Allocated)

(2) 22,000

(4) 35,000

(5) 30,000

(6) 81,000

6,000

Copyright © 2015 Pearson Education, Inc.

3-32

(25-30 min.) P3-44A

Req. 1

Estimated yearly overhead costs*

=

$173,000

Estimated yearly machine hours

6,920 machine hours

Predetermined overhead rate

=

$25 per machine hour

* $50,000 + $64,000 + $41,000 + $18,000 = $173,000

Req. 2

Actual machine hours…………………….

6,400

Predetermined overhead rate…………….

x $25 per machine hour

Manufacturing overhead allocated….…

$160,000

Req. 3

Manufacturing Overhead

Actual

Allocated

51,000

160,000

65,000

43,000

19,000

18,000

Journal Entry

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Cost of Goods Sold

13,000

Manufacturing Overhead

13,000

Req. 4

To help control manufacturing overhead, managers compare the actual line item amounts for manufacturing overhead

with the budgeted amounts. Managers also investigate only large differences between actual and budgeted amounts

to identify the reasons why actual costs differ from planned or budgeted costs.

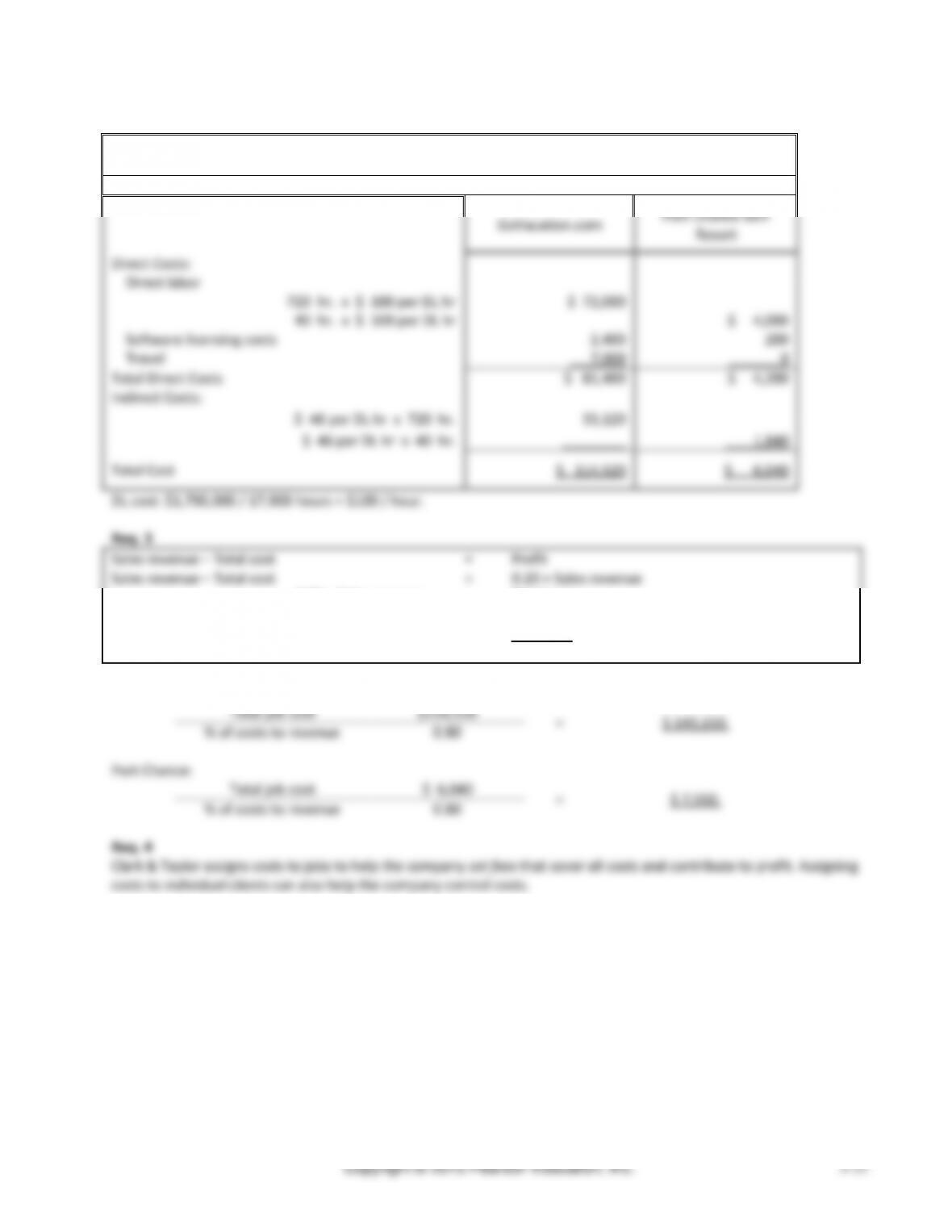

(20-25 min.) P3-45A

Req. 1

Total estimated indirect costs

=

$823,400 *

Direct labor hours

17,900 direct labor hours

Predetermined Indirect Cost

Allocation Rate

=

$46 per direct labor hour

* $160,000 + $95,000 + $505,400 + $63,000 = $823,400

Chapter 3 Job Costing

(continued) P3-45A

Req. 2

Clark & Taylor

Estimated Cost of Jobs

GoVacation.com

Port Chance Golf

Resort

Direct Costs:

Direct labor

720 hr. x $ 100 per DL hr

$ 72,000

40 hr. x $ 100 per DL hr

$ 4,000

Software licensing costs

2,400

200

Travel

7,000

0

Total Direct Costs

$ 81,400

$ 4,200

Indirect Costs:

$ 46 per DL hr x 720 hr.

33,120

$ 46 per DL hr x 40 hr.

1,840

Total Cost

$ 114,520

$ 6,040

DL cost: $1,790,000 / 17,900 hours = $100 / hour.

Req. 3

Sales revenue − Total cost

=

Profit

Sales revenue − Total cost

=

0.20 × Sales revenue

0.80 × Sales revenue

=

Total cost

Sales revenue

=

Total cost

0.80

GoVacation.com:

Total job cost

$114,520

=

$ 143,150.

% of costs to revenue

0.80

Port Chance:

Total job cost

$ 6,040

=

$ 7,550.

% of costs to revenue

0.80

Req. 4

Clark & Taylor assigns costs to jobs to help the company set fees that cover all costs and contribute to profit. Assigning

costs to individual clients can also help the company control costs.

Managerial Accounting 4e Solutions Manual

(20-25 min.) P3-46A

Req. 1

Total estimated indirect costs

=

$ 315,000*

=

21%

Direct labor cost

$1,500,000

(30-35 min.) P3-47A

Req. 1

Job Cost Record

JOB NO. 298

CUSTOMER NAME AND ADDRESS ATV Corporation

JOB DESCRIPTION 170 TX tires

DATE PROMISED 10-10

DATE STARTED 9-30

DATE COMPLETED 10-3

DATE

DIRECT MATERIALS

DIRECT LABOR

MANUFACTURING OVERHEAD ALLOCATED

REQUISITION

NO.

AMOUNT

LABOR TIME RECORD

NO.

AMOUNT

DATE

RATE

AMOUNT

20

XX

9

30

437

$960

1896

$216

10

3

$22 per direct

10

2

439

400

labor houra

$924

3

501

1,200

1904

600

OVERALL COST SUMMARY

DIRECT MATERIALS.…………

$2,560

DIRECT LABOR…………………

816

MANUFACTURING OVERHEAD

ALLOCATED……

924

Totals

$2,560

$816

TOTAL JOB COST…….…..

$4,300

aPredetermined

=

$396,000

=

$22 per direct labor hour

mfg. overhead rate

18,000

Overhead allocated

=

(12 hrs + 30 hrs) × $22 per DL hour

=

$924

Managerial Accounting 4e Solutions Manual

(30-45 min.) P3-48A

Req. 1

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

a.

Raw Materials Inventory

470,000

Accounts Payable

470,000

b.

Work in Process Inventorya

83,200

Manufacturing Overhead

35,800

($119,000 – $83,200)

Wages Payable

119,000

c.

Work in Process Inventory

227,600

Raw Materials Inventoryb

227,600

d.

Manufacturing Overhead

6,300

Accum. Depr. — Equipment

6,300

e.

Manufacturing Overhead

14,100

Cash

10,100

Prepaid Insurance

4,000

f.

Work in Process Inventory

($83,200 × 0.60)

49,920

Manufacturing Overhead

49,920

a: $14,100 + $28,700 + $19,400 + $21,000

b: $41,900 + $56,600 + $62,200 + $66,900

Chapter 3 Job Costing

(continued) P3-48A

Req. 1

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

g.

Finished Goods Inventoryc

258,200

Work in Process Inventory

258,200

h.

Accounts Receivable ($99,000 + $146,000)

245,000

Sales Revenue

245,000

Cost of Goods Sold ($63,660 + $100,260)

164,960

Finished Goods Inventory

164,960

Work in Process Inventory

Finished Goods Inventory

(b)

83,200

(g)

258,200

(g)

258,200

(h)

164,960

(c)

227,600

(f)

49,920

Bal.

102,520

Bal.

93,240

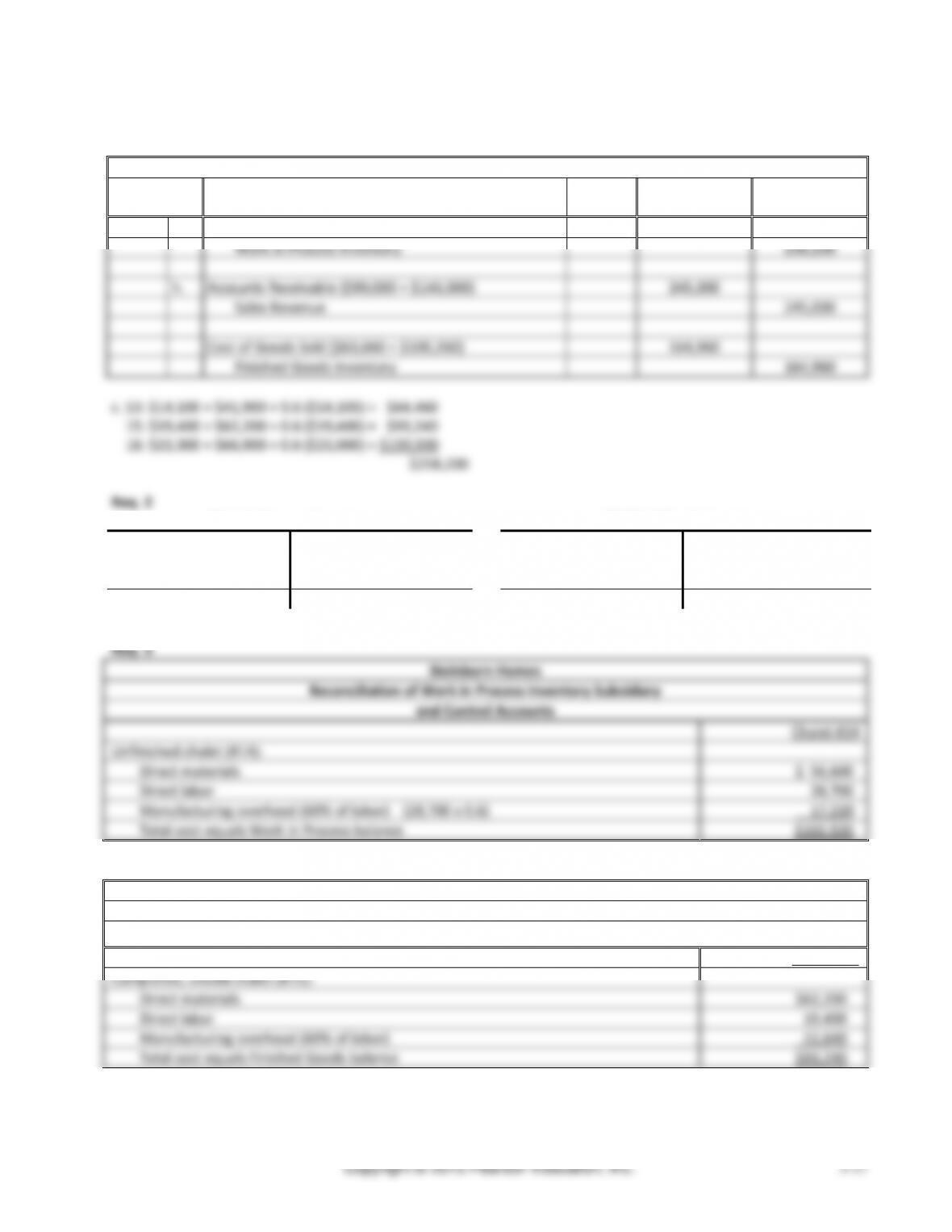

Steinborn Homes

Reconciliation of Work in Process Inventory Subsidiary

and Control Accounts

Chalet #14

Unfinished chalet (#14):

Direct materials

$ 56,600

Direct labor

28,700

Manufacturing overhead (60% of labor) (28,700 x 0.6)

17,220

Total cost equals Work in Process balance

$102,520

Req. 4

Steinborn Homes

Reconciliation of Finished Goods Inventory Subsidiary

and Control Accounts

Chalet #15

Completed, unsold chalet (#15):

Direct materials

$62,200

Direct labor

19,400

Manufacturing overhead (60% of labor)

11,640

Total cost equals Finished Goods balance

$93,240