Chapter 3 Job Costing

Chapter 3

Job Costing

Quick Check Questions

Answers:

(5-10 min.) S3-6

Note: The predetermined manufacturing overhead rates shown below are from the solutions to S3–5.

Req. 1

Total manufacturing

overhead allocated

=

Actual use of cost allocation base × Predetermined manufacturing overhead

rate

=

62,550 hours × $25 per direct labor hour

=

$1,563,750

Req. 2

Total manufacturing

overhead allocated

=

Actual use of cost allocation base × Predetermined manufacturing overhead

rate

=

$1,245,000 × 125%

=

$1,556,250

Req. 3

Total manufacturing

overhead allocated

=

Actual use of cost allocation base × Predetermined manufacturing overhead

rate

=

38,000 machine hours × $40 per machine hour

=

$1,520,000

Req. 4

The total amount of manufacturing overhead allocated during the year is dependent upon two factors: the allocation

base used and the actual manufacturing overhead for the year.

As a result, a company could either overallocate or underallocate manufacturing overhead, depending on the

allocation base used and the actual manufacturing overhead for the year.

Note: Student answers may vary.

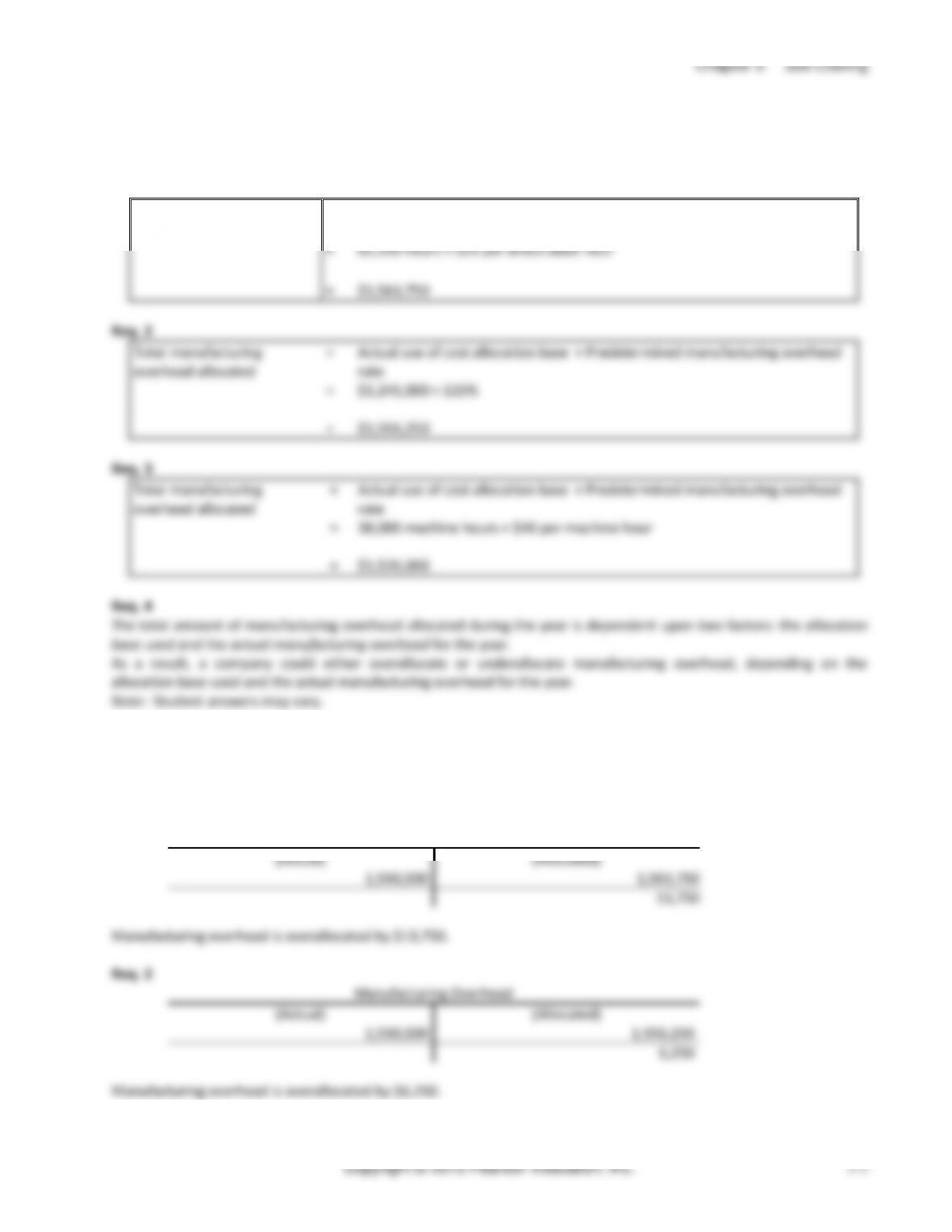

(5-10 min.) S3–7

Note: The allocated manufacturing overhead amounts shown below were from the solutions to S3-6

Req. 1

Manufacturing Overhead

(Actual)

(Allocated)

1,550,000

1,563,750

13,750

Manufacturing overhead is overallocated by $13,750.

Req. 2

Manufacturing Overhead

(Actual)

(Allocated)

1,550,000

1,556,250

6,250

Manufacturing overhead is overallocated by $6,250.

Managerial Accounting 4e Solutions Manual

Req. 3

Manufacturing Overhead

(Actual)

(Allocated)

1,550,000

1,520,000

30,000

Manufacturing overhead is underallocated by $30,000.

Req. 4

In this company’s particular case, using direct labor hours as an allocation base resulted in overcosting the jobs by

$13,750. Using direct labor cost as an allocation was the best option, causing jobs to be slightly overcosted by $6,250

during the year. Using machine hours led to the least accurate allocation: Jobs were undercosted by a total of $30,000.

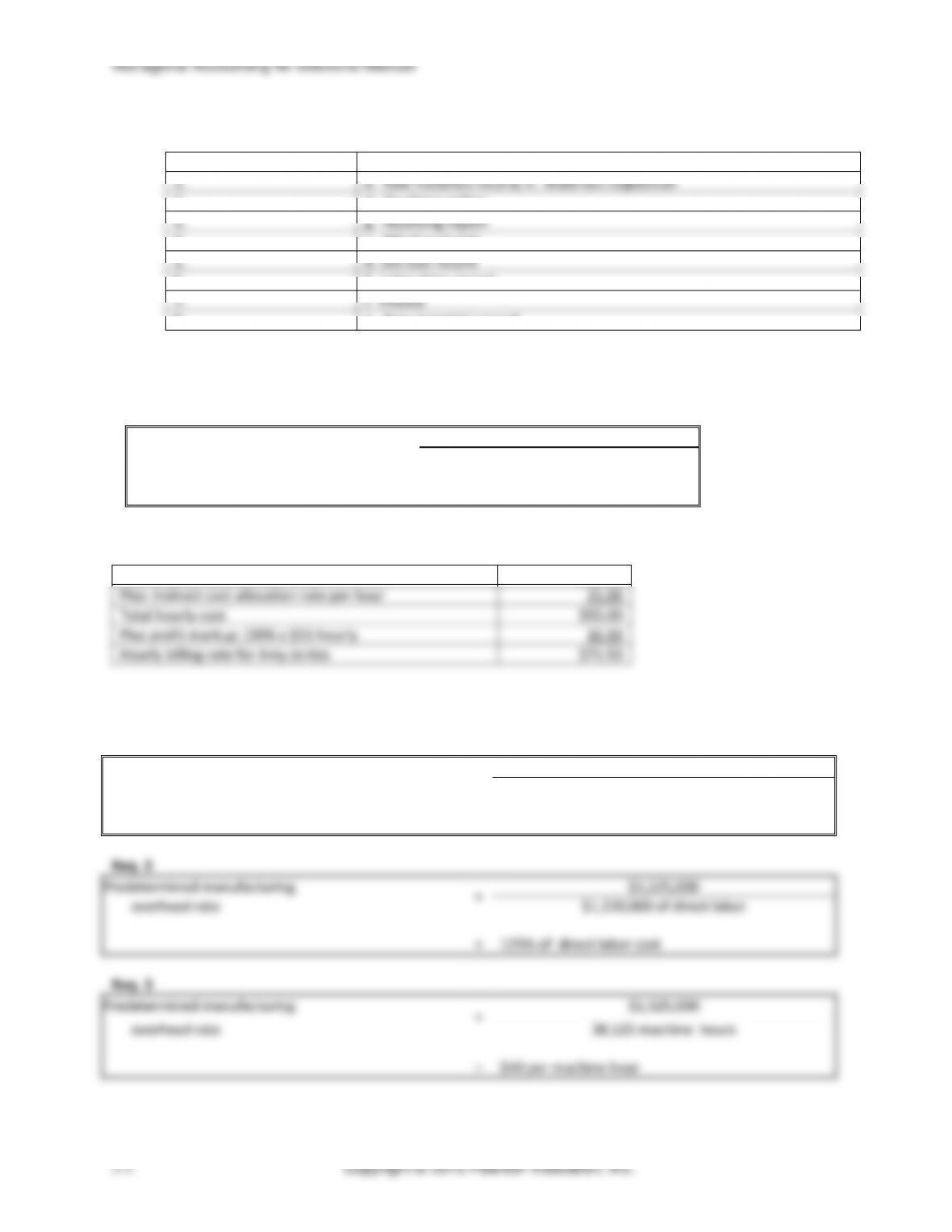

(5-10 min.) S3–8

Req. 1

Predetermined manufacturing

overhead rate

=

$1,890,000

$2,160,000 of direct labor cost

=

87.50% of direct labor cost

Req. 2

Total manufacturing overhead allocated

=

Actual use of cost allocation base × Predetermined

manufacturing overhead rate

=

$2,300,000 × 87.50%

=

$2,012,500

Req. 3

Manufacturing Overhead

(Actual)

(Allocated)

1,760,000

2,012,500

252,500

Manufacturing overhead is overallocated by $252,500.

(5 min.) S3-9

Req. 1

Direct materials

$40

Labor (2 hours × $29)

58

Shop overhead (2 hours × $22)

44

Cost to J&B Appliance

$142

Req. 2

Direct materials

$40

Labor (2 hours × $76)

152

Price to charge customer

$192

Chapter 3 Job Costing

(5-10 min.) S3–10

1. Managers use a predetermined manufacturing overhead rate so that they can get timely information on the

2. Each situation has its drawbacks. An undercosted job could lead to actual losses or lower profits than

(5-10 min.) S3-11

Journal Entry

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Raw Materials Inventory

68,100

Accounts Payable

68,100

To record purchase of materials.

Work in Process Inventorya

63,000

Manufacturing Overheadb

500

Raw Materials Inventory

63,500

To record use of materials.

Bal.

Purchased

Bal.

Managerial Accounting 4e Solutions Manual

(5 min.) S3–13

Req. 1

Hourly direct labor cost rate

=

$192,000 per year

2,400 hours per year

=

$80 per hour

Req. 2

Client 367: 15 hours × $80 / hour = $1,200

Req. 3

Indirect cost

allocation rate

=

$840,000

28,000 direct labor hours

=

$30.00 per direct labor hour

Req. 4

Chapter 3 Job Costing

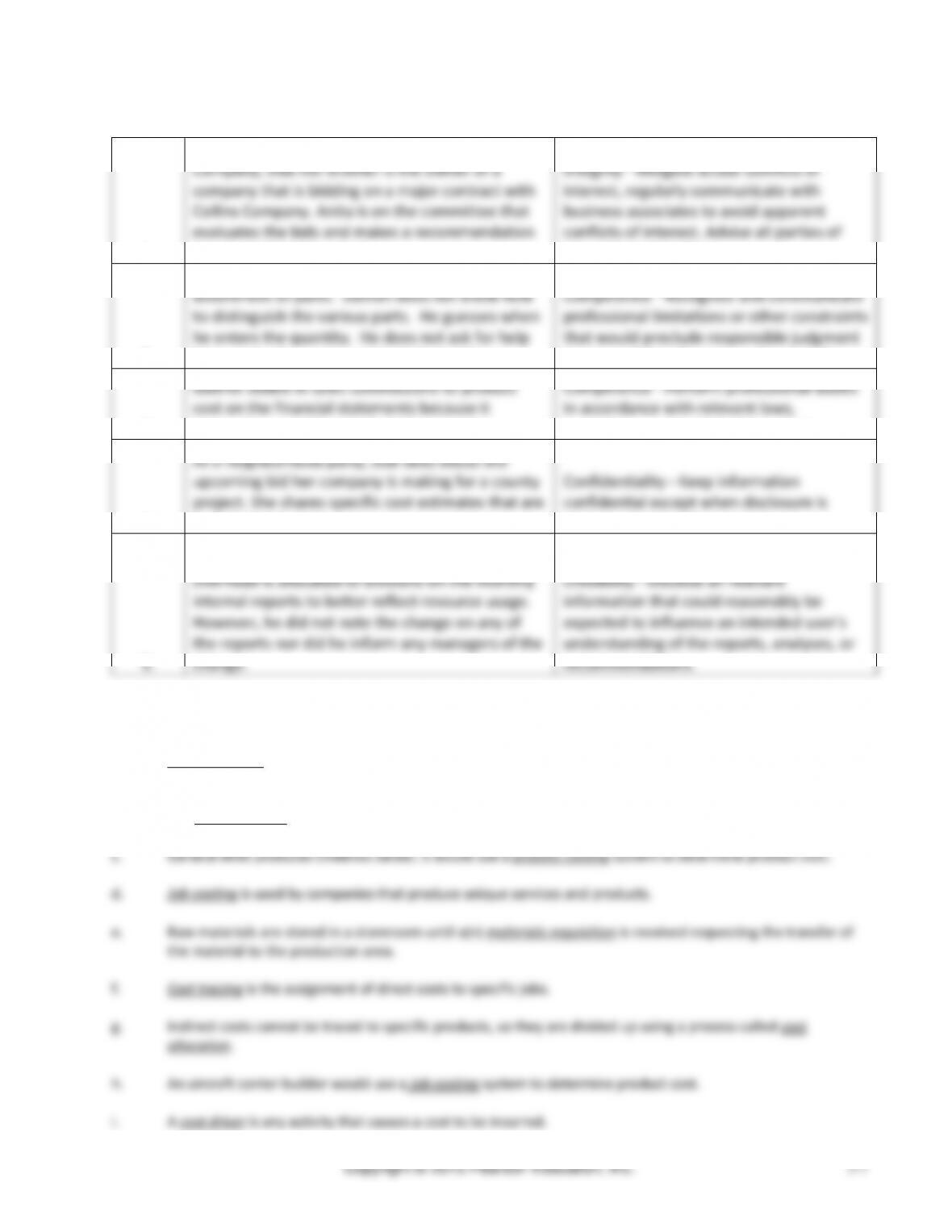

(5 min.) S3–14

1.

Anita does not disclose to her employer, Collins

Company, that her brother is the owner of a

company that is bidding on a major contract with

Collins Company. Anita is on the committee that

evaluates the bids and makes a recommendation

about which bid to select.

Integrity – Mitigate actual conflicts of

interest, regularly communicate with

business associates to avoid apparent

conflicts of interest. Advise all parties of

any potential conflicts.

2.

Damon is asked to do an inventory count of a wide

assortment of parts. Damon does not know how

to distinguish the various parts. He guesses when

he enters the quantity. He does not ask for help

because he does not want to look stupid.

Competence – Recognize and communicate

professional limitations or other constraints

that would preclude responsible judgment

or successful performance of an activity.

3.

Gabriel added in sales commissions to product

cost on the financial statements because it

seemed reasonable to include those costs.

Competence – Perform professional duties

in accordance with relevant laws,

regulations, and technical standards.

4.

At a neighborhood party, Jodi talks about the

upcoming bid her company is making for a county

project. She shares specific cost estimates that are

included in the bid.

Confidentiality – Keep information

confidential except when disclosure is

authorized or legally required.

5.

Jose changed the way that manufacturing

overhead is allocated to divisions on the monthly

internal reports to better reflect resource usage.

However, he did not note the change on any of

the reports nor did he inform any managers of the

change.

Credibility – Disclose all relevant

information that could reasonably be

expected to influence an intended user’s

understanding of the reports, analyses, or

recommendations.

(5-10 min.) S3–15

a. Process costing is used by companies that produce large numbers of identical units through a series of uniform

production steps or processes.

b. The job cost record is used to track and accumulate all of the costs for an individual job.

Managerial Accounting 4e Solutions Manual

Exercises (Group A)

(10 min.) E3-16A

a. Aircraft builder – Job costing

b. Hospital – Job costing

c. Cement plant – Process costing

d. Dentist – Job costing

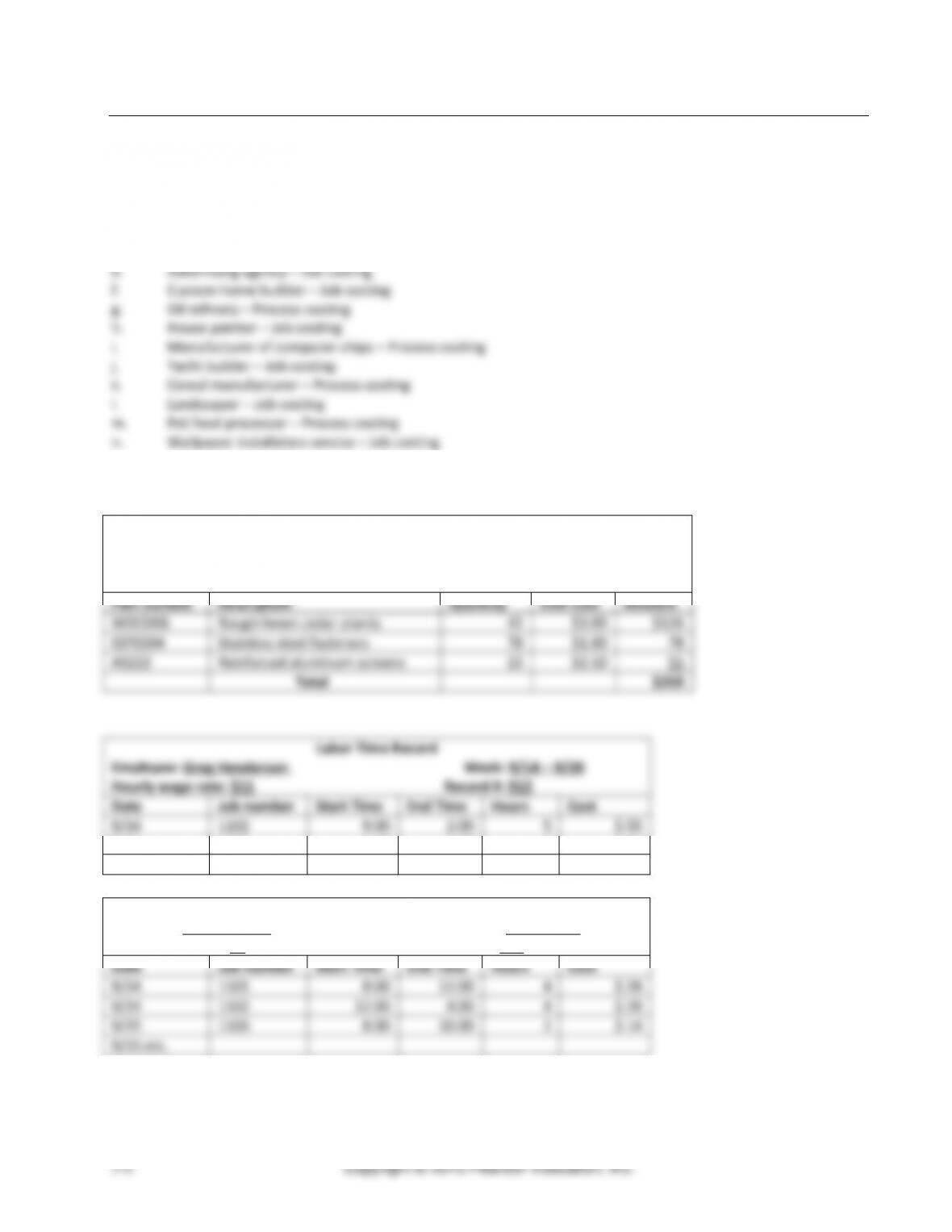

(10 min.) E3-17A

Materials Requisition

Number: #1250

Date: 9/14

Job: 1102

Part number

Description

Quantity

Unit Cost

Amount

WOCD06

Rough-hewn cedar planks

42

$3.00

$126

SSF0304

Stainless steel fasteners

78

$1.00

78

AS222

Reinforced aluminum screens

22

$2.50

55

Total

$259

Labor Time Record

Employee: Greg Henderson Week: 9/14 – 9/20

Hourly wage rate: $11 Record #: 912

Date

Job number

Start Time

End Time

Hours

Cost

9/14

1102

9:00

2:00

5

$ 55

9/14

1103

2:00

5:00

3

$ 33

9/15 etc.

Labor Time Record

Employee: Andrew Peck Week: 9/14 – 9/20

Hourly wage rate: $7 Record #: 913

Date

Job number

Start Time

End Time

Hours

Cost

9/14

1101

8:00

12:00

4

$ 28

9/14

1102

12:00

4:00

4

$ 28

9/15

1103

8:00

10:00

2

$ 14

9/15 etc.

Chapter 3 Job Costing

Job Cost Record

Job Number: 1102

Customer: Wild Birds, Inc.

Job description: 30 Model 3F (platform bird feeders)

Date Started: Sep. 14 Date Completed: ________

Manufacturing Cost Information:

Cost Summary

Direct Materials

Req. #1250:

$259

Direct Labor

No. #912 (5 hours): $ 55

No. #913 (4 hours): $ 28

$ 83

Manufacturing Overhead

9 hours x $2 per direct labor hour

$ 18

Total Job Cost

$360

Number of units

÷ 30

Cost per Unit

$ 12.00

(10 min.) E3-18A

Req. 1

Calculate the predetermined overhead rate:

Predetermined

=

$67,200

overhead rate

4,200 direct labor hours

=

$16 per direct labor hour

Req. 2

Allocate overhead using the predetermined overhead rate:

Job 101: 180 direct labor hours × $16 per direct labor hour = $2,880

Job 102: 74 direct labor hours × $16 per direct labor hour = $1,184

Req. 3

Next, calculate the total job cost for each job:

Job #101

Job #102

Direct materials

$18,000

$12,000

Direct labor

(180 direct labor hours × $24 per direct labor hour)

(74 direct labor hours × $24 per direct labor hour)

4,320

1,776

Overhead

(calculated in Req. 2)

2,880

1,184

Total job cost

$25,200

$14,960

Managerial Accounting 4e Solutions Manual

(10 min.) E3-19A

Req. 1

Calculate the predetermined overhead rate:

Predetermined

=

$356,400

overhead rate

$648,000 direct labor cost*

=

55% of direct labor cost

(5-10 min.) E3-20A

Req. 1

First, calculate the predetermined overhead rate:

Predetermined manufacturing

=

$586,600

overhead rate

41,900 direct labor hours

=

$14 per direct labor hour

Next, tabulate the total job cost:

Job #309

Direct materials

$14,200

Direct labor

(175 direct labor hours × $22 per direct labor hour)

3,850

Manufacturing overhead

(175 direct labor hours × $14 per direct labor hour)

2,450

Total job cost

$20,500

Req. 2

Job #309

Total manufacturing cost of Job #309

$20,500

22% Mark-up on manufacturing cost

× 122%

Contracted billing price

$25,010

or, alternatively:

Job #309

Total manufacturing cost of Job #309

$20,500

Add 22% Mark-up on manufacturing cost

(22% × $20,500)

+ 4,510

Contracted billing price

$25,010

(10 min.) E3-21A

Req. 1

Virgin materials

120

$ 3.70

$ 444.00

Recycled-content materials

280

$ 2.60

$ 728.00

Direct labor

16

$12.00

$ 192.00

Manufacturing overhead (based on DLH)

16

$6.00

$ 96.00

Total job cost

$1,460.00

Req. 2

Virgin materials

120

Recycled-content materials

280

70% (= 280 / 400)

Total pounds

400

Ludlow Plastics meets the 60% recycled-content requirement.

Managerial Accounting 4e Solutions Manual

(15 min.) E3-22A

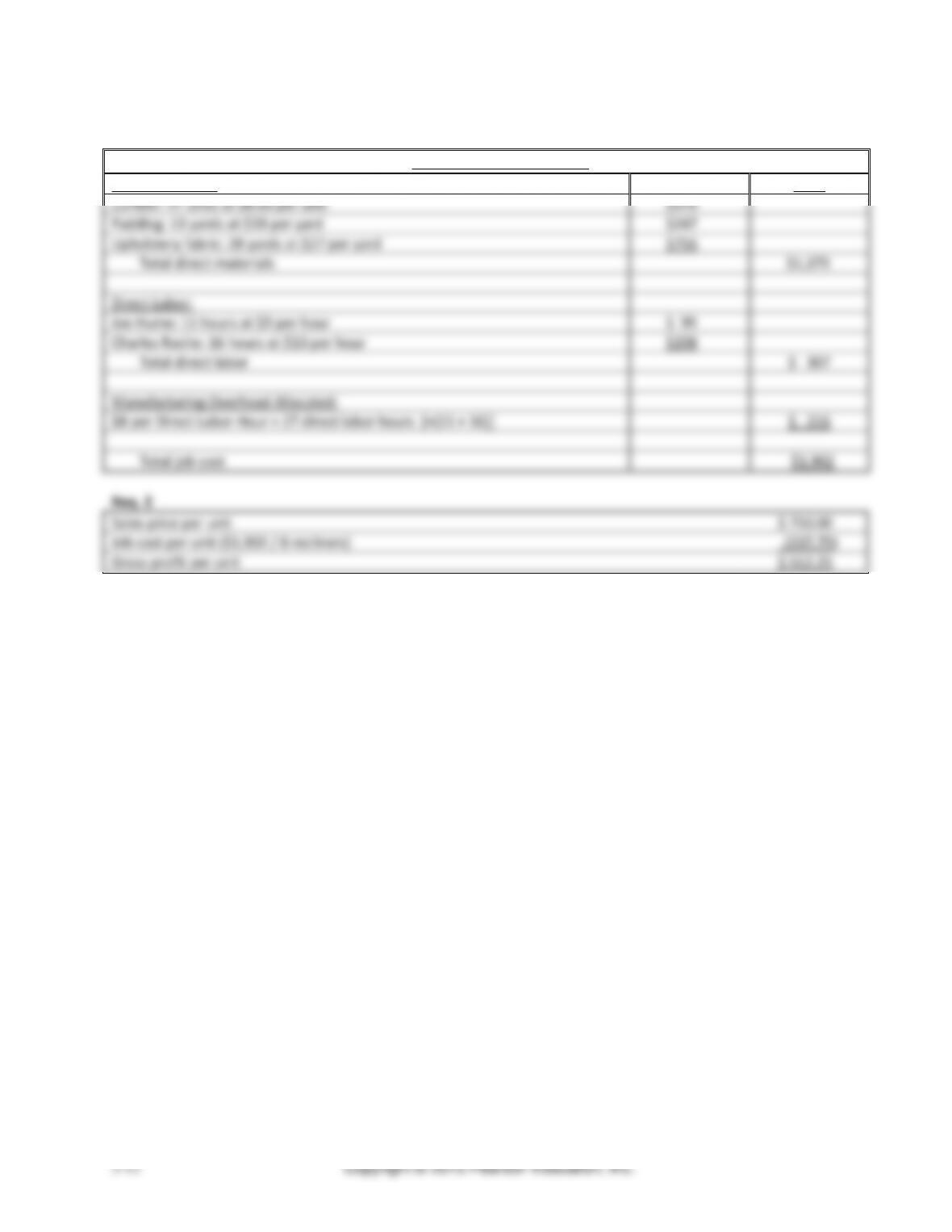

Req. 1

Job Cost Record for Job 310

Direct Materials:

Total

Lumber: 47 units at $8.00 per unit

$376

Padding: 13 yards at $19 per yard

$247

Upholstery fabric: 28 yards at $27 per yard

$756

Total direct materials

$1,379

Direct Labor:

Joe Hume: 11 hours at $9 per hour

$ 99

Charles Roche: 16 hours at $13 per hour

$208

Total direct labor

$ 307

Manufacturing Overhead Allocated:

$8 per Direct Labor Hour × 27 direct labor hours [=(11 + 16)]

$ 216

Total job cost

$1,902

Req. 2

Sales price per unit

$ 750.00

Job cost per unit ($1,902 / 8 recliners)

(237.75)

Gross profit per unit

$ 512.25

Chapter 3 Job Costing

(10 min.) E3-23A

Req. 1

First, calculate the predetermined overhead rate:

Predetermined manufacturing

=

$369,260

overhead rate

9,980 direct labor hours

=

$37 per direct labor hour

Next, tabulate the total job cost:

Direct materials

$ 25,300

Direct labor

(1,700 direct labor hours × $12 per direct labor hour)

20,400

Manufacturing overhead

(1,700 direct labor hours × $37 per direct labor hour)

62,900

Total job cost

$108,600

Then, compute bid price:

Total manufacturing cost of job

$108,600

31% Markup on manufacturing cost

× 131%

Bid price

$142,266

– or, alternatively:

–

Total manufacturing cost of job

$108,600

Add 31% mark-up on manufacturing cost

(31% × $108,600)

+ 33,666

Bid price

$142,266

Req. 2

First, calculate the predetermined overhead rate:

Predetermined manufacturing

=

$369,260

overhead rate

18,463 machine hours

=

$20 per machine hour

Managerial Accounting 4e Solutions Manual

(continued) E3-23A

Next, tabulate the total job cost:

Direct materials

$25,300

Direct labor

(1,700 direct labor hours × $12 per direct labor hour)

20,400

Manufacturing overhead

(1,980 machine hours × $20 per machine hour)

39,600

Total job cost

$85,300

Total manufacturing cost of job

$ 85,300

31% Markup on manufacturing cost

× 131%

Bid price

$111,743

– or, alternatively:

Total manufacturing cost of job

$ 85,300

Add 31% Markup on manufacturing cost

(31% × $85,300)

+ 26,443

Bid price

$111,743

Req. 3

Whether or not Rosa wins the bid will depend on the allocation base the company chose to use during the year. Rosa’s

bid price will be $142,266 if the company uses direct labor hours as the allocation base. In this case, the company will

probably lose the job to Mauzy Recycling, since their bid was only $125,000. However, Rosa will probably win the bid if

machine hours are used as the allocation base. Using machine hours as an allocation base results in a bid price of

$111,743.

Note: Student answers may vary.

(15-20 min.) E3-24A

Req. 1

Predetermined manufacturing overhead rate

=

$620,000

77,500 machine hours

=

$8 per machine hour

Req. 2

Allocated manufacturing overhead

=

54,000 actual machine hours

×

$8 per machine hour

=

$432,000

(10-15 min.) E3-25A

Req. 1

Journal Entry

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Manufacturing Overhead

$430,000

Accumulated Depreciation — plant and equipment

400,000

Property Tax Payable

20,500

Wages Payable

9,500

Req. 2

Note: Predetermined overhead rate $8

per MH

=

$620,000

77,500 machine hours

Journal Entry

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory

432,000

Manufacturing Overhead (54,000 x $8 per MH)

432,000

Allocated

Journal Entry

DATE

Managerial Accounting 4e Solutions Manual

(10 min.) E3-26A

Req. 1

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

a.

Raw Materials Inventory

195,000

Accounts Payable

195,000

b.

Work in Process Inventory

167,000

Manufacturing Overhead

27,000

Raw Materials Inventory

194,000

c.

Work in Process Inventory

215,000

Manufacturing Overhead

45,000

Wages Payable

260,000

d.

Manufacturing Overhead

26,000

Accum. Depreciation

17,000

Utilities Payable (or A/P)

9,000

e.

Work in Process Inventory

87,000

Manufacturing Overhead

87,000

f.

Website Expense

3,000

Accounts Payable

3,000

Req. 2

During January, actual manufacturing overhead costs totaled $98,000 ($27,000 + $45,000 + $26,000). By the end of

January, a total of $87,000 had been allocated to jobs. Therefore, manufacturing overhead had been underallocated by

$11,000.

Chapter 3 Job Costing

Copyright © 2015 Pearson Education, Inc.

3-17

(10 min.) E3-27A

1.

Direct materials used…………………

$ 30,000

2.

Indirect materials used………………

$ 3,500

3.

Direct labor………………………………

$ 64,500

4.

Indirect labor…………………………….

$ 13,500

5.

Cost of goods manufactured…………

$ 125,500

6.

Cost of goods sold……………………

$ 114,000

7.

Actual manufacturing overhead

$ 59,000

8.

Allocated manufacturing overhead….

$ 42,000

9.

Predetermined manufacturing

overhead rate, as a % of direct

labor cost; $42,000 /$ 64,500…………

65%

10.

Manufacturing overhead is

($59,000 actual − $42,000 allocated) = $ 17,000

Underallocated

Chapter 3 Job Costing

(10 min.) E3-29A

Req. 1

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

a.

Raw Materials Inventory

205,000

Accounts Payable

205,000

b.

Work in Process Inventory

146,000

Manufacturing Overhead

28,000

Raw Materials Inventory

174,000

c.

Work in Process Inventory

200,000

Manufacturing Overhead

10,000

Wages Payable

210,000

d.

Manufacturing Overhead

30,000

Accum. Depreciation

16,000

Utilities Payable (or A/P)

14,000

e.

Work in Process Inventory

56,000

Manufacturing Overhead

56,000

Req. 2

During January, actual manufacturing overhead costs totaled $68,000, while only $56,000 had been allocated to jobs.

Therefore, by the end of January, manufacturing overhead had been underallocated by $12,000.

Note: T-account not required.

Manufacturing Overhead

(Actual)

(Allocated)

(2) 28,000

(3) 10,000

(4) 30,000

(5) 56,000

12,000

Copyright © 2015 Pearson Education, Inc.

3-20

(10 min.) E3-30B

a. Medical practice of six doctors and four physician assistants – Job costing

b. Soft drink bottler – Process costing

c. Movie studio – Job costing

(10 min.) E3-31B

Materials Requisition

Number: 1250

Date: 9/14

Job: 1102

Part number

Description

Quantity

Unit Cost

Amount

WOCD06

Rough-hewn cedar planks

40

$2.50

$ 100

SSF0304

Stainless steel fasteners

82

$1.00

82

AS222

Reinforced aluminum screens

26

$1.50

39

Total

$221

Labor Time Record

Employee: Greg Henderson Week: 9/14 – 9/20

Hourly wage rate: $11 Record #: 912

Date

Job number

Start Time

End Time

Hours

Cost

9/14

1102

9:00

1:00

4

$ 44

9/14

1103

1:00

5:00

4

$ 44

9/15 etc.

Labor Time Record

Employee: Andrew Peck Week: 9/14 – 9/20

Hourly wage rate: $7 Record #: 913

Date

Job number

Start Time

End Time

Hours

Cost

9/14

1101

9:00

12:00

3

$ 21

9/14

1102

12:00

5:00

5

$ 35

9/15

1103

9:00

11:00

2

$ 14

9/15 etc.