Managerial Accounting 4e Solutions Manual

Problems (Group B)

(30 min.) P2–47B

Reqs. 1, 2, and 3

Jazzy Cola

Value Chain Cost Classification

(In thousands)

Production

Cost

R&D

Design

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Marketing

Distribution

Customer

Service

Truck drivers’

wages

$265

Lemon syrup

$20,000

Depreciation

on trucks

100

Lime flavoring

920

Payment for

new recipe

$1,190

Customer

hotline

190

Sales

commissions

400

Production

costs of “cents–

off” store

coupons for

customers

$ 470

Rearranging

plant layout

$1,500

Freight-in

1,700

Depreciation

on plant and

equipment

2,900

Bottles

1,210

Salt*

30

Plant utilities

$ 850

Wages of

workers who

mix syrup

$7,900

Plant janitors’

wages

1,050

Replace

products with

expired

dates

$ 60

Total costs

$1,090

$1,300

$21,070*

$8,200

$5,030

$1,070

$585

$235

*Salt’s low value makes it likely treated as indirect materials. However, some students may classify salt as direct

materials.

Req. 4

Total inventoriable product costs:

Direct materials………….………………….…..

$23,830

Direct labor………………………………………..

7,900

Manufacturing overhead……………………..

4,830

Total inventoriable product costs…….….

$36,560

Chapter 2 Building Blocks of Managerial Accounting

(continued) P2-47B

(30 min.) P2-48B

Req. 1

The ending inventory costs derived from the following schedule are: Raw materials $143,000, Work in process

$239,000, and Finished goods $150,000.

Inventory Reconstruction Schedule

Raw materials inventory

Work in Process Inventory

Finished Goods Inventory

Beginning

inventory

$113,000 (G)

Beginning

Inventory

$ 229,000 (G)

Beginning

inventory

$ 154,000 (G)

+ Purchases

476,000 (G)

+ Direct Materials

Used

446,000e

+ Cost of goods

manufactured

1,186,000c

+ Direct labor

505,000 (G)

+ Manufacturing

Overhead

245,000 (G)

= Direct

Materials

available for

use

589,000

= Total

manufacturing

costs to

account for

1,425,000 (G)

= Cost of goods

available for sale

1,340,000 (G)

− Ending

inventory

143,000f

− Ending inventory

239,000d

− Ending inventory

150,000b

= Direct

Materials

used

$446,000e

= Cost of goods

manufactured

$1,186,000c

= Cost of goods

Sold

$1,190,000a

(G) = Amount given in the case.

aCost of good sold:

Sales

×

(1 − Gross profit %)

=

Cost of goods sold

$1,700,000

×

70%

=

$1,190,000

bEnding finished goods inventory:

Cost of goods available for sale

−

Ending finished goods inventory

=

Cost of goods sold

$1,340,000

−

Ending finished goods inventory

=

$1,190,000

Ending finished goods inventory

=

$ 150,000

cCost of goods manufactured:

Beginning finished goods inventory

+

Cost of goods manufactured

=

Cost of goods

available for sale

$154,000

+

Cost of goods manufactured

=

$1,340,000

Cost of goods manufactured

=

$1,186,000

Managerial Accounting 4e Solutions Manual

(continued) P2-48B

dEnding work in process inventory:

Total manufacturing

costs to account for

−

Ending work in process inventory

=

Cost of goods

manufactured

$1,425,000

−

Ending work in process inventory

=

$1,186,000

Ending work in process inventory

=

$ 239,000

eDirect materials used:

Beginning

work in process inventory

+

Direct + Direct + Manufacturing

material labor overhead

used

=

Total manufacturing costs

to account for

$229,000

+

Direct + $505,000 + $245,000

materials

used

=

$1,425,000

Direct materials used

=

$ 446,000

fEnding direct materials inventory:

Direct materials

available for use

−

Ending direct materials inventory

=

Direct materials used

$589,000

−

Ending direct materials inventory

=

$446,000

Ending direct materials inventory

=

$143,000

(45-55 min.) P2-49B

Part One:

Cost of goods sold calculation:

Beginning inventory

$ 12,000

Plus: Purchases and freight-in*

34,000

Cost of goods available for sale

46,000

Less: Ending inventory

(9,900)

Cost of goods sold

$ 36,100

Robin’s Roses

Income Statement

Year Ended December 31, 2013

Sales revenue

$59,000

Less: Cost of goods sold

36,100

Gross profit

22,900

Less operating expenses:

Utilities expense

$ 1,200

Rent expense

3,600

Sales commission expense

4,600

9,400

Operating income

$13,500

Chapter 2 Building Blocks of Managerial Accounting

(continued) P2-49B

Part Two:

Req. 1

Calculation of Direct Materials Used

Beginning Raw Materials Inventory

14,000

Plus: Purchases of direct materials, freight-in, and import

duties

35,000

Materials available for use

49,000

Less: Ending Raw Material Inventory

(10,500)

Direct materials used

38,500

Schedule of Cost of Goods Manufactured

Beginning Work in Process Inventory

–

Plus: Manufacturing costs incurred

Direct materials used (from previous schedule)

38,500

Direct labor

21,000

Manufacturing overhead ($4,400 + $1,050 + $8,600)

14,050

Total manufacturing costs to account for

73,550

Less: Ending Work in Process Inventory

(3,500)

Cost of goods manufactured

70,050

Calculation of Cost of Goods Sold

Beginning Finished Goods Inventory

–

Plus: Cost of goods manufactured (from previous schedule)

70,050

Cost of goods available for sale

70,050

Less: Ending Finished Goods Inventory

(6,500)

Cost of goods sold

63,550

Req. 2

Floral Manufacturing

Income Statement

For Year Ended December 31, 2014

Sales revenue

102,000

Less: Cost of goods sold (from previous schedule)

63,550

Gross profit

38,450

Less operating expenses:

Delivery expense

2,000

Sales salaries expense

4,700

Customer service hotline

1,100

Total operating expenses

7,800

Operating income

30,650

Managerial Accounting 4e Solutions Manual

(continued) P2-49B

Req. 3

A manufacturer’s cost of goods sold is based on its cost of goods manufactured. In contrast, a merchandiser’s cost of

Chapter 2 Building Blocks of Managerial Accounting

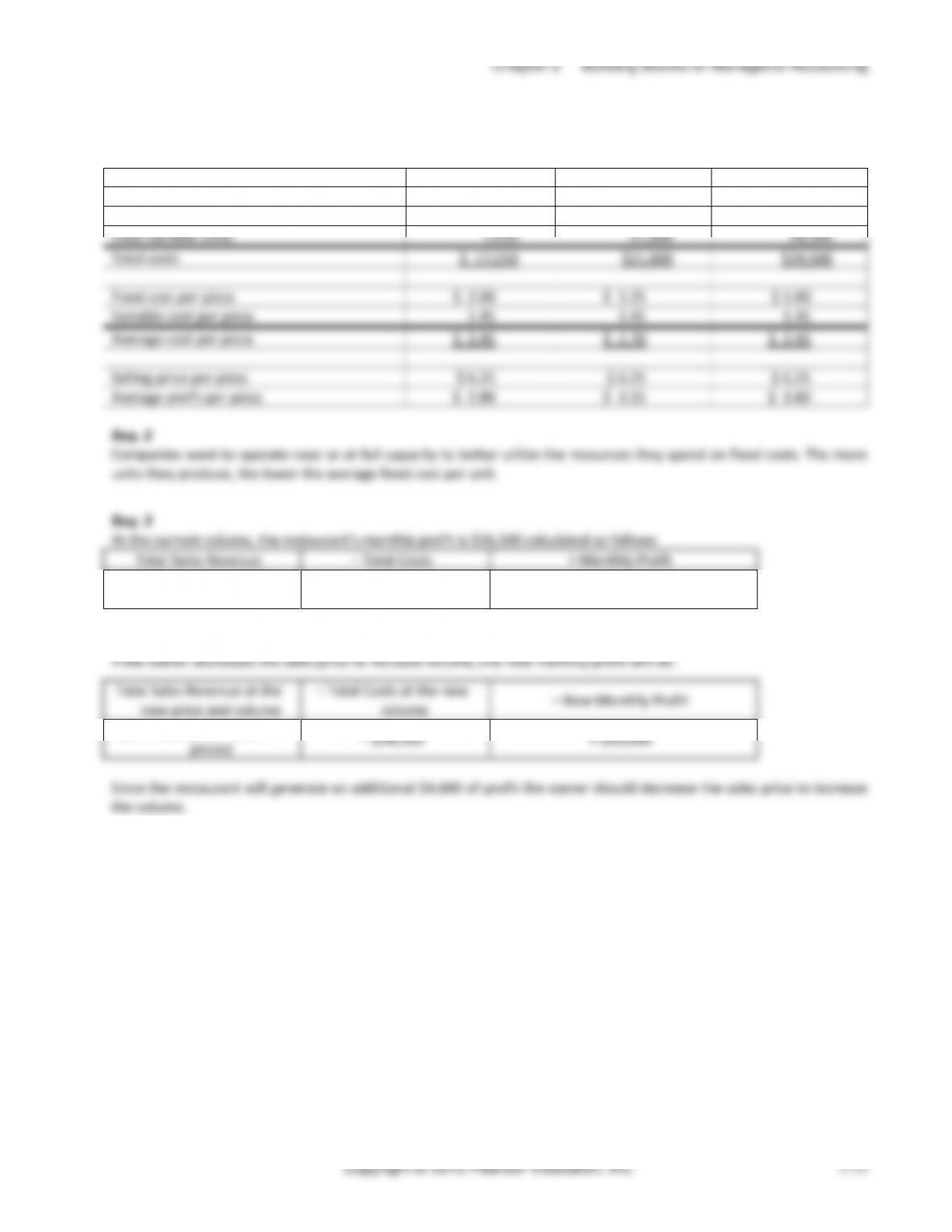

(15-20 min.) P2–51B

Req. 1

Monthly pizza volume

3,000

4,000

6,000

Total fixed costs

$ 6,000

$ 6,000

$ 6,000

Total variable costs

3,750

5,000

7,500

Total costs

$9,750

$11,000

$13,500

Fixed cost per pizza

$ 2.00

$ 1.50

$ 1.00

Variable cost per pizza

1.25

1.25

1.25

Average cost per pizza

$ 3.25

$ 2.75

$ 2.25

Sales price per pizza

$6.00

$6.00

$6.00

Average profit per pizza

$ 2.75

$ 3.25

$ 3.75

Req. 2

Companies want to operate near or at full capacity to better utilize the resources they spend on fixed costs. The more

units they produce, the lower the average fixed cost per unit.

Req. 3

At the current volume, the restaurant’s monthly profit is $20,100 calculated as follows

Total Sales Revenue

− Total Costs

= Monthly Profit

($6.00 per pizza × 4,000

pizzas)

− $11,000

= $13,000

Managerial Accounting 4e Solutions Manual

Discussion & Analysis

A2–52

1. Briefly describe a service company, a merchandising company, and a manufacturing company. Give an example

of each type of company, but do not use the same examples as given in the chapter.

2. How do service, merchandising, and manufacturing companies differ from each other? How are service,

merchandising, and manufacturing companies similar to each other? List as many similarities and differences as

you can identify.

Differ:

3. What is the value chain? What are the six types of business activities found in the value chain? Which type(s) of

business activities in the value chain generate costs that go directly to the income statement once incurred?

What type(s) of business activities in the value chain generate costs that flow into inventory on the balance

sheet?

The value chain is the activities that add value to a firm’s products and services. The six types of business activities

4. Compare direct costs to indirect costs. Give an example of a cost at a company that could be a direct cost at one

level of the organization but would be considered an indirect cost at a different level of that organization.

Explain why this same cost could be both direct and indirect (at different levels).

Chapter 2 Building Blocks of Managerial Accounting

(continued) A2-52

5. What is meant by the term “inventoriable product costs”? What is meant by the term “period costs”? Why

does it matter whether a cost is an inventoriable product cost or a period cost?

6. Compare inventoriable product costs to period costs. Using a product of your choice, give examples of

inventoriable product costs and period costs. Explain why you categorized your costs as you did.

7. Describe how the income statement of a merchandising company differs from the income statement of a

manufacturing company. Also comment on how the income statement from a merchandising company is similar

to the income statement of a manufacturing company.

8. How are the cost of goods manufactured, the cost of goods sold, the income statement, and the balance sheet

related for a manufacturing company? What specific items flow from one statement or schedule to the next?

Describe the flow of costs between the cost of goods manufactured, the cost of goods sold, the income

statement, and the balance sheet for a manufacturing company.

9. What makes a cost relevant or irrelevant when making a decision? Suppose a company is evaluating whether to

use its warehouse for storage of its own inventory or whether to rent it out to a local theater group for housing

props. Describe what information might be relevant when making that decision.

Managerial Accounting 4e Solutions Manual

(continued) A2-52

10. Explain why “differential cost” and “variable cost” do not have the same meaning. Give an example of a situation

in which there is a cost that is a differential cost but not a variable cost.

11. Greenwashing, the practice of overstating a company’s commitment to sustainability, has been in the news over

12. In the chapter, Ricoh was mentioned as a company that has designed its copiers so that at the end of the copier’s

life, Ricoh will collect and dismantle the product for usable parts, shred the metal casing, and use the parts and

Chapter 2 Building Blocks of Managerial Accounting

Application & Analysis

A2-53

Basic Discussion Questions

1. Describe the product that is being produced and the company that produces it.

2. Describe the six value chain business activities that this product would pass through from its inception to its

ultimate delivery to the customer.

3. List at least three costs that would be incurred in each of the six business activities in the value chain.

• R&D – investigating new fabrics, customer needs surveys, innovation

4. Classify each cost you identified in the value chain as either being an inventoriable product cost or a period cost.

Explain your justification.

5. A cost object can be anything for which managers want a separate measurement of cost. List three different

potential cost objects other than the product itself for the company you have selected.

6. List a direct cost and an indirect cost for each of the three different cost objects in #5. Explain why each cost

would be direct or indirect.

• Advertising

Managerial Accounting 4e Solutions Manual

A2–54

Ethics Mini-Case

1. If Joe were to increase income by adding sales commission costs and advertising costs to product costs, the

following ethical principles would be violated:

a. Competence: Perform professional duties in accordance with relevant laws, regulations, and technical

2. If Joe were to make the Company loan to Mike, it is not clear whether ethical principles would be violated. Making

3. Perhaps a third course of action would be to think of other alternatives, such as:

a. Refer Mike to a credit counseling service or to an employee assistance program

Chapter 2 Building Blocks of Managerial Accounting

A2–55

Real Life Mini-Case

1. Starbucks could be considered both a service company and a merchandiser. The café part of Starbucks would be

2. A typical value chain is composed of the following phases. Potential costs for a cup of coffee’s value chain are

included with each phase:

a. Research & Development: Performing research on the proper roasting methods for coffee beans and on the

various types of coffee beans that might be used

3. Starbucks cup of coffee served in Fairlawn, Ohio, café:

a. What costs:

i. Direct material: Coffee beans, water, cup, cup sleeve, milk, sugar

4. Starbucks café in Fairlawn, Ohio, and a pound of packaged coffee assuming coffee is ground at time of purchase

a. Costs of that pound of coffee

i. Direct material

5. Starbucks management would state that its retail stores “have more tools to absorb the increase because of other

costs included in the cost of a cup of coffee” because the coffee goes through several more steps in the store,