Chapter 2 Building Blocks of Managerial Accounting

(15 min.) E2-31B

Reqs. 1, 2, and 3

Req. 4

Total inventoriable product costs:

Direct materials……………………………………..….…

$ 69

Direct labor………………………………………

8

Manufacturing overhead……………………………

75

Total inventoriable product cost………………….

$152

Req. 5

Direct materials……………………………………………

$ 69

Direct labor………………………………………

8

$ 77

Direct labor……………………………………………

$ 8

Manufacturing overhead……………………………

75

$ 83

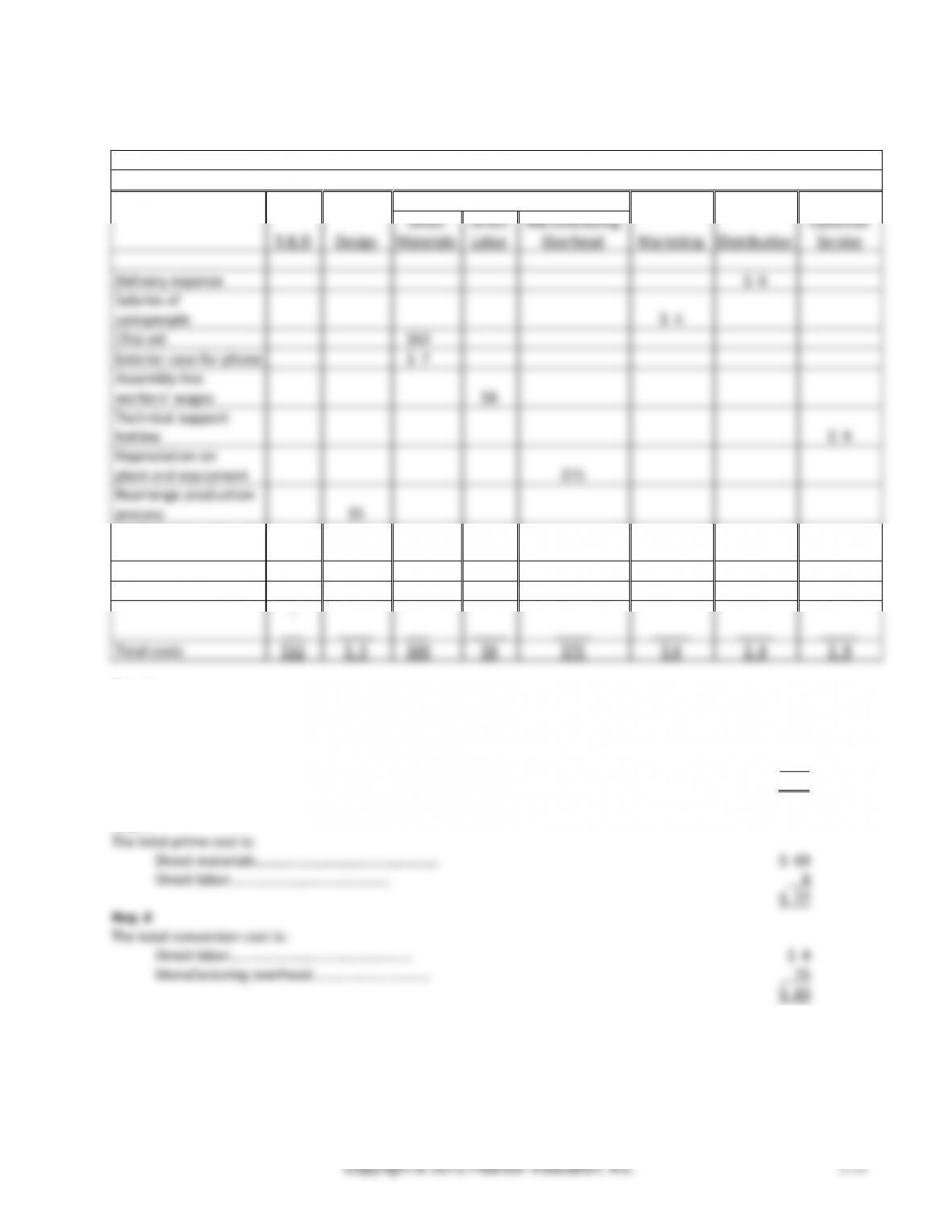

Cost Classification

Production

R & D

Design

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Marketing

Distribution

Customer

Service

Delivery expense

$ 6

Salaries of

salespeople

$ 4

Chip set

$62

Exterior case for phone

$ 7

Assembly-line

workers’ wages

$8

Technical support

hotline

$ 9

Depreciation on

plant and equipment

$75

Rearrange production

process

$5

1-800 (toll-free) line for

customer orders

$ 2

Scientists’ salaries

$12

–

Total costs

$12

$ 5

$69

$8

$75

$ 6

$ 6

$ 9

Chapter 2 Building Blocks of Managerial Accounting

(15-20 min.) E2-33B

Req. 1

DM

DL

IM

IL

Other

MOH

Period

a.

Airplane seats

$260

b.

Production supervisors’

salaries

$190

c.

Depreciation on forklifts

$90

d.

Machine lubricants

$20

e.

Factory janitors’ wages

$10

f.

Assembly workers’ wages

$610

g.

Property tax on

corporate marketing

offices

$15

h.

Plant utilities

$120

i.

Cost of warranty repairs

$215

j.

Machine operators’ health

insurance

$80

k.

Depreciation on

admin offices

$70

l.

Cost of designing new plant

layout

$170

m.

Jet engines

$1,000

TOTAL

$1,260

$690

$20

$200

$210

$470

Req. 2

Total manufacturing overhead costs

=

IM + IL + Other MOH

=

$20 + 200 + 210 = $430

Req. 3

Total inventoriable product costs

=

DM + DL + MOH

=

$1,260 + 690 + 430 = $2,380

Req. 4

Total prime costs

=

DM + DL

=

$1,260 + 690 = $1,950

Req. 5

Total conversion costs

=

DL + MOH

=

$690 + 430 = $1,120

Req. 6

Total period costs

=

$470

Managerial Accounting 4e Solutions Manual

(10 min.) E2–34B

Current Assets

Current assets:

Cash

$ 15,200

Accounts receivable

84,000

Inventories:

Raw materials inventory

$ 10,200

Work in process inventory

37,000

Finished goods inventory

66,000

Total inventories

113,200

Prepaid expenses

5,800

Total current assets

$218,200

The company must be a manufacturer, because it has three kinds of inventory: raw materials, work in process, and

finished goods.

(10-15 min.) E2–35B

Cost of goods sold calculation:

Beginning inventory

$ 18,000

Plus: Purchases and freight-in*

658,000

Cost of goods available for sale

676,000

Less: Ending inventory

(16,000)

Cost of goods sold

$ 660,000

Pretty Pets

Income Statement

For Current Year

Sales revenue

$ 1,125,000

Less: Cost of goods sold

(660,000)

Gross profit

465,000

Less operating expenses:

Web site expenses

$ 58,000

Marketing expenses

32,500

Freight-out expenses

28,500

Total operating expenses

(119,000)

Operating income

$ 346,000

*purchases of $636,000 + freight-in of $22,000 = $658,000

Managerial Accounting 4e Solutions Manual

(15-20 min.) E2-37B

Calculation of Direct Materials Used

Beginning Raw Materials Inventory

$ 21,000

Plus: Purchases of direct materials

70,000

Materials available for use

$ 91,000

Less: Ending Raw Material Inventory

(30,000)

Direct materials used

$ 61,000

Schedule of Cost of Goods Manufactured

Beginning Work in Process Inventory

$ 41,000

Plus: Manufacturing costs incurred

Direct materials used (from previous schedule)

61,000

Direct labor

87,000

Manufacturing overhead (43,000 + 8,500 +

13,300 + 3,700)

68,500

Total manufacturing costs to account for

$ 257,500

Less: Ending Work in Process Inventory

(34,000)

Cost of goods manufactured

$ 223,500

Calculation of Cost of Goods Sold

Beginning Finished Goods Inventory

$ 15,000

Plus: Cost of goods manufactured (from previous schedule)

223,500

Cost of goods available for sale

$ 238,500

Less: Ending Finished Goods Inventory

(28,000)

Cost of goods sold

$ 210,500

Managerial Accounting 4e Solutions Manual

(25 min.) E2–39B

Instructional note: This is a fairly challenging exercise that requires students to work backwards through financial

statement elements.

a.

Revenues

$27,200

Less: Cost of goods sold

14,900

Gross profit

$12,300

b. To determine beginning raw materials inventory, start with the materials used computation and work backwards:

Beginning raw materials inventory

$ 2,100

Plus: Purchases of direct materials

9,700

Available for use

11,800

Less: Ending raw materials inventory

(3,600)

Direct materials used

$ 8,200

c. To determine ending finished goods inventory, start by computing the cost of goods manufactured:

Beginning work in process inventory

$ 0

Plus: Manufacturing costs incurred:

Direct materials used

$8,200

Direct labor

3,500

Manufacturing overhead

6,300

18,000

Total manufacturing costs to account for

18,000

Less: Ending work in process inventory

(1,600)

Cost of goods manufactured

$16,400

Now use the cost of goods sold computation to determine ending finished goods inventory:

Beginning finished goods inventory

$ 4,900

Plus: Cost of goods manufactured (from above)

16,400

Cost of goods available for sale

21,300

Less: Ending finished goods inventory

(6,400)

Cost of goods sold (from part A)

$14,900

Chapter 2 Building Blocks of Managerial Accounting

(15-20 min.) E2-40B

a. The purchase price of the old computer when replacing it

with a new computer with improved features

Irrelevant

b. The cost of renovations when deciding whether to build a

new office building or to renovate the existing office building

Relevant

c. The original cost of the current stove when selecting a new,

more efficient stove for a restaurant

Irrelevant

d. Local tax incentives when selecting the location of a new

office complex for a company’s headquarters

Relevant

e. The fair market value (trade-in value) of the existing forklift

when deciding whether to replace it with a new, more efficient

model

Relevant

f. Fuel economy when purchasing new trucks for the delivery

fleet

Relevant.

g. The cost of production when determining whether to

continue to manufacture the screen for a smartphone or to

purchase it from an outside supplier

Relevant

h. The cost of land when determining where to build a new call

center

Relevant

i. The average cost of vehicle operation when purchasing a new

delivery van

Relevant

j. Real estate property tax rates when selecting the location for

a new order processing center

Relevant

1)

Variable costs

=

20,000,000 units × $1 / unit

=

$20,000,000

+ Fixed costs

=

3,000,000

= Total costs

=

$23,000,000

2)

$23,000,000

÷

20,000,000 units

=

$1.15 per unit

3)

$ 3,000,000

÷

20,000,000 units

=

$0.15 per unit

4)

Variable costs

=

30,000,000 units × $1 / unit

=

$30,000,000

+ Fixed costs

=

3,000,000

= Total costs

=

$33,000,000

5)

$33,000,000

÷

30,000,000 units

=

$1.10 per unit

6)

$ 3,000,000

÷

30,000,000 units

=

$0.10 per unit

7)

The average product cost increases as production volume

increases because the company is spreading its fixed costs over

10 million more units. The company will be operating more

efficiently, so the average cost of making each unit decreases.

Managerial Accounting 4e Solutions Manual

Problems (Group A)

(30 min.) P2-42A

Reqs. 1, 2, and 3

Rootstown Cola

Value Chain Cost Classification

(In thousands)

Production

Cost

R&D

Design

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Marketing

Distribution

Customer

Service

Plant janitors’

wages

950

Truck drivers’

wages

$285

Payment for

new recipe

$1,090

Depreciation

on delivery

trucks

300

Plant utilities

$ 850

Lime flavoring

$1,080

Rearranging

plant layout

$1,300

Bottles

$1,390

Salt*

30

Sales

commissions

400

Production

costs of

“cents–off”

store coupons

for customers

$ 670

Lemon syrup

$17,000

Replace

products with

expired

dates

$ 35

Depreciation

on plant and

equipment

3,200

Wages of

workers who

mix syrup

$8,200

Customer

hotline

200

Freight-in

1,600

Total costs

$1,090

$1,300

$21,070*

$8,200

$5,030

$1,070

$585

$235

Managerial Accounting 4e Solutions Manual

P2-43A (continued)

dEnding work in process inventory:

Total manufacturing

costs to account for

−

Ending work in process inventory

=

Cost of goods

manufactured

$1,515,000

−

Ending work in process inventory

=

$1,228,000

Ending work in process inventory

=

$ 287,000

eDirect materials used:

Beginning

work in process inventory

+

Direct + Direct + Manufacturing

material labor overhead

used

=

Total manufacturing costs

to account for

$206,000

+

Direct + $523,000 + $213,000

materials

used

=

$1,515,000

Direct materials used

=

$ 573,000

fEnding direct materials inventory:

Direct materials

available for use

−

Ending direct materials inventory

=

Direct materials used

$626,000

−

Ending direct materials inventory

=

$573,000

Ending direct materials inventory

=

$53,000

(45-55 min.) P2-44A

Part One:

Cost of goods sold calculation:

Beginning inventory

$ 12,700

Plus: Purchases and freight-in*

37,000

Cost of goods available for sale

49,700

Less: Ending inventory

(9,600)

Cost of goods sold

$ 40,100

Penny’s Posies

Income Statement

Year Ended December 31, 2013

Sales revenue

$53,000

Less: Cost of goods sold

40,100

Gross profit

12,900

Less operating expenses:

Utilities expense

$ 1,400

Rent expense

4,600

Sales commission expense

4,900

10,900

Operating income

$2,000

Managerial Accounting 4e Solutions Manual

P2-44A (continued)

Part Three: Reqs. 1 and 2

Penny’s Posies Floral

Floral Manufacturing

Partial Balance Sheet

Partial Balance Sheet

December 31, 2013

December 31, 2014

Inventory………..

$9,600

Raw materials inventory……

$ 6,500

Work in process inventory..

3,500

Finished goods inventory…

4,000

Total inventory………………..

$14,000

(10 min.) P2-45A

1) As shown below, the quantitative data suggests you would net $6,800 more by taking Job #1 and living at home.

Attributes:

Take Job #1 and live at home

Take Job #2 and rent an

apartment

Salary

$45,000

$50,000

Rent

0

(9,000)

Food

0

(2,000)

Cable and Internet

0

(800)

Salary, net of living expenses

$45,000

$38,200

Net Difference = $45,000 − $38,200 = $6,800

2) The costs of doing laundry, operating the car, and paying for cell phone service are irrelevant because they do not

differ between the two alternatives.

4) If you want Job #2 and you want to live at home, you will benefit by the higher salary and the lower living