Chapter 2 Building Blocks of Managerial Accounting

Chapter 2

Building Blocks of Managerial Accounting

Quick Check Questions

Answers:

Managerial Accounting 4e Solutions Manual

(5-10 min.) S2-3

a. Marketing

b. Design

(5-10 min.) S2-4

Cost

Direct or Indirect cost?

a. Depreciation of the building

Indirect

b. Cost of costume jewelry on the mannequins in the Juniors department

Direct

c. Cost of bags used to package customer purchases at the main registers for the

store

Indirect

d. The Medina Kohl’s store manager’s salary

Indirect

e. Cost of security staff at the Medina store

Indirect

f. Manager of Juniors department

Direct

g. Juniors department sales clerks

Direct

h. Cost of Juniors clothing

Direct

i. Cost of hangers used to display the clothing in the store

Indirect

j. Electricity for the building

Indirect

k. Cost of radio advertising for the store

Indirect

l. Juniors clothing buyers’ salaries (these buyers buy for all Juniors departments of

Kohl’s stores)

Indirect

(10 min.) S2-5

a. Indirect costs cannot be directly traced to a(n) cost object .

b. Total costs include the costs of all resources used throughout the value chain.

c. GAAP requires companies to use only inventoriable product costs for external financial reporting.

Managerial Accounting 4e Solutions Manual

(5-10 min.) S2-6

a. Period cost

b. Inventoriable product cost

(5-10 min.) S2-7

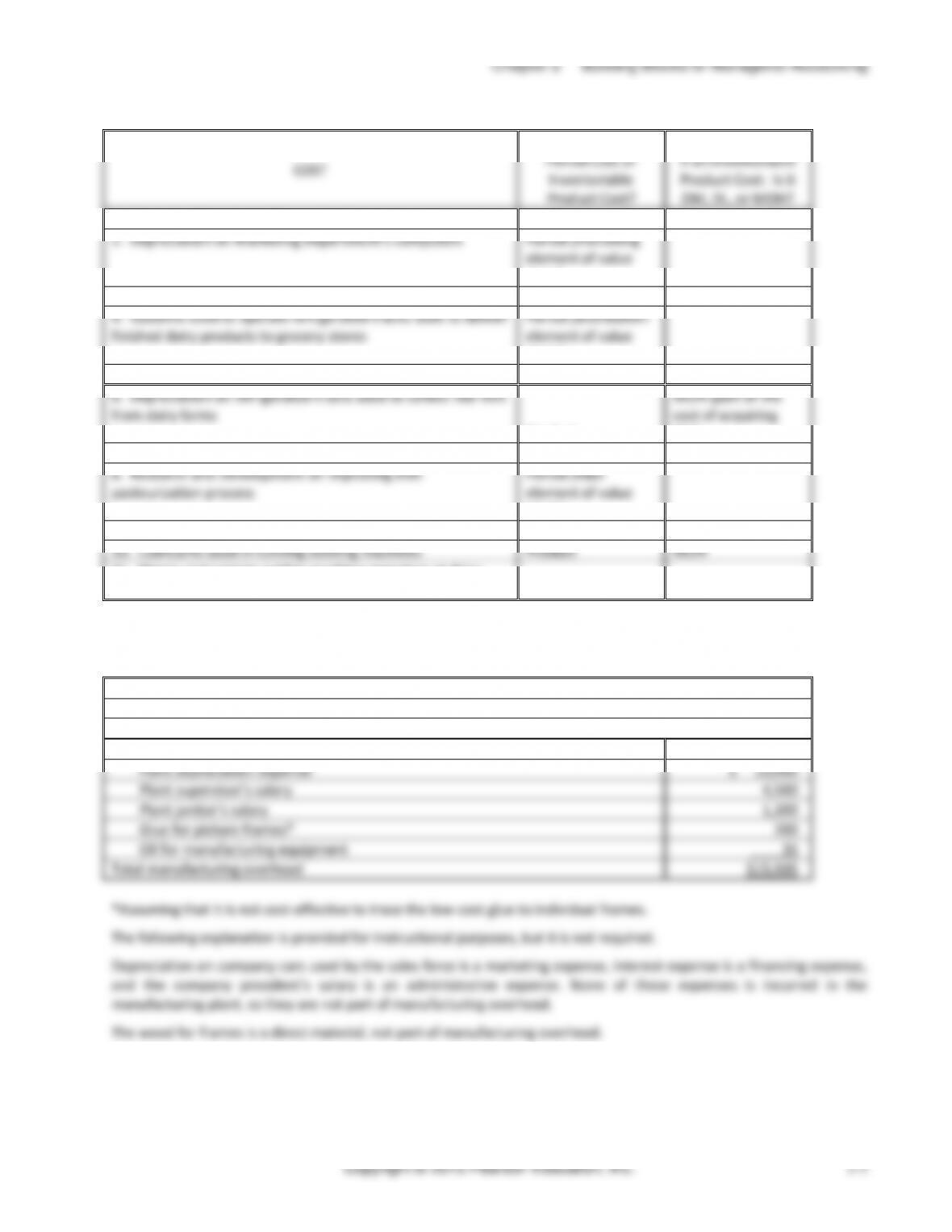

COST

Period Cost or

Inventoriable

Product Cost?

If an Inventoriable

Product Cost: Is it

DM, DL, or MOH?

a. Standard packaging materials used to package individual

units of product for sale (e.g., cereal boxes in which cereal is

packaged)

Product

DM

b. Lease payment on administrative headquarters

Period

c. Telephone bills relating to customer service call center

Period

d. Property insurance – 40% of building is used for sales and

administration; 60% of building is used for manufacturing

40% Period;

60% Product

—

MOH

e. Wages and benefits paid to assembly-line workers in the

manufacturing plant

Product

DL

f. Depreciation on automated production equipment

Product

MOH

g. Salaries paid to quality control inspectors in the plant

Product

MOH

h. Repairs and maintenance on factory equipment

Product

MOH

Managerial Accounting 4e Solutions Manual

(5 min.) S2–10

Calculation of Cost of Goods Sold

Beginning inventory

$ 3,600

Purchases

$45,000

Import duties

700

Freight-in

3,300

49,000

Cost of goods available for sale

52,600

Less: Ending inventory

(5,500)

Cost of goods sold

$47,100

(5-10 min.) S2–11

Simply Hair

Income Statement

For the Year Ended

Sales revenue

$39,225,000

Cost of goods sold:

Beginning inventory

$ 2,500,000

Purchases

21,400,000

Cost of goods available for sale

23,900,000

Less: Ending inventory

(3,245,000)

Less: Cost of goods sold

(20,655,000)

Gross profit

18,570,000

Less: Operating expenses

(6,850,000)

Operating income

$ 11,720,000

(5 min.) S2–12

Thomas Bikes

Calculation of Direct Materials Used

Beginning raw materials inventory

$ 4,100

Purchases of direct materials

$16,400

Import duties

1,300

Freight-in

200

17,900

Direct materials available for use

22,000

Less: Ending raw materials inventory

(1,900)

Direct materials used

$20,100

Chapter 2 Building Blocks of Managerial Accounting

(10 min.) S2–13

Hansen Manufacturing

Schedule of Cost of Goods Manufactured

Beginning work in process inventory

$ 79,500

Plus: manufacturing costs incurred:

Direct materials used

$515,500

Direct labor

226,700

Manufacturing overhead

774,800

1,517,000

Total manufacturing costs to account for

1,596,500

Less: Ending work in process inventory

(86,500)

Cost of goods manufactured

$1,510,000

(10 min.) S2–14

Relevant quantitative information might include:

• Difference in benefits

• Difference in costs of food

• Difference in salaries

• Difference in costs of transportation

• Difference in costs of housing

Relevant qualitative information might include:

• Difference in job description

• Difference in lifestyle

• Difference in future career development opportunities

• Proximity to family and friends

• Difference in weather

Relevant information always pertains to the future and differs between alternatives.

Student responses may vary.

(10 min.) S2–15

a. Costs that differ between alternatives are called differential costs.

b. In the long-run, most costs are controllable, meaning that management is able to influence or change the

Managerial Accounting 4e Solutions Manual

(10 min.) S2–16

COST

Variable or Fixed

a. Cost of coffee used at a Starbucks store

Variable

b. Hourly wages paid to sales clerks at Best Buy

Variable

c. Monthly flower costs for a florist

Variable

d. Cost of fuel used for a national trucking company

Variable

e. Shipping costs for Amazon.com

Variable

f. Monthly rent for a nail salon

Fixed

g. Sales commissions at a car dealership

Variable

h. Monthly insurance costs for the home office of a company

Fixed

i. Monthly depreciation of equipment for a customer service office

Fixed

j. Cost of fabric used at a clothing manufacturer

Variable

k. Cost of fruit sold at a grocery store

Variable

l. Monthly office lease costs for a CPA firm

Fixed

m. Monthly cost of French fries at a McDonald’s restaurant

Variable

n. Property taxes for a restaurant

Fixed

o. Depreciation of exercise equipment at the YMCA

Fixed

Managerial Accounting 4e Solutions Manual

Exercises (Group A)

(10-15 min.) E2-18A

Reqs. 1 and 2

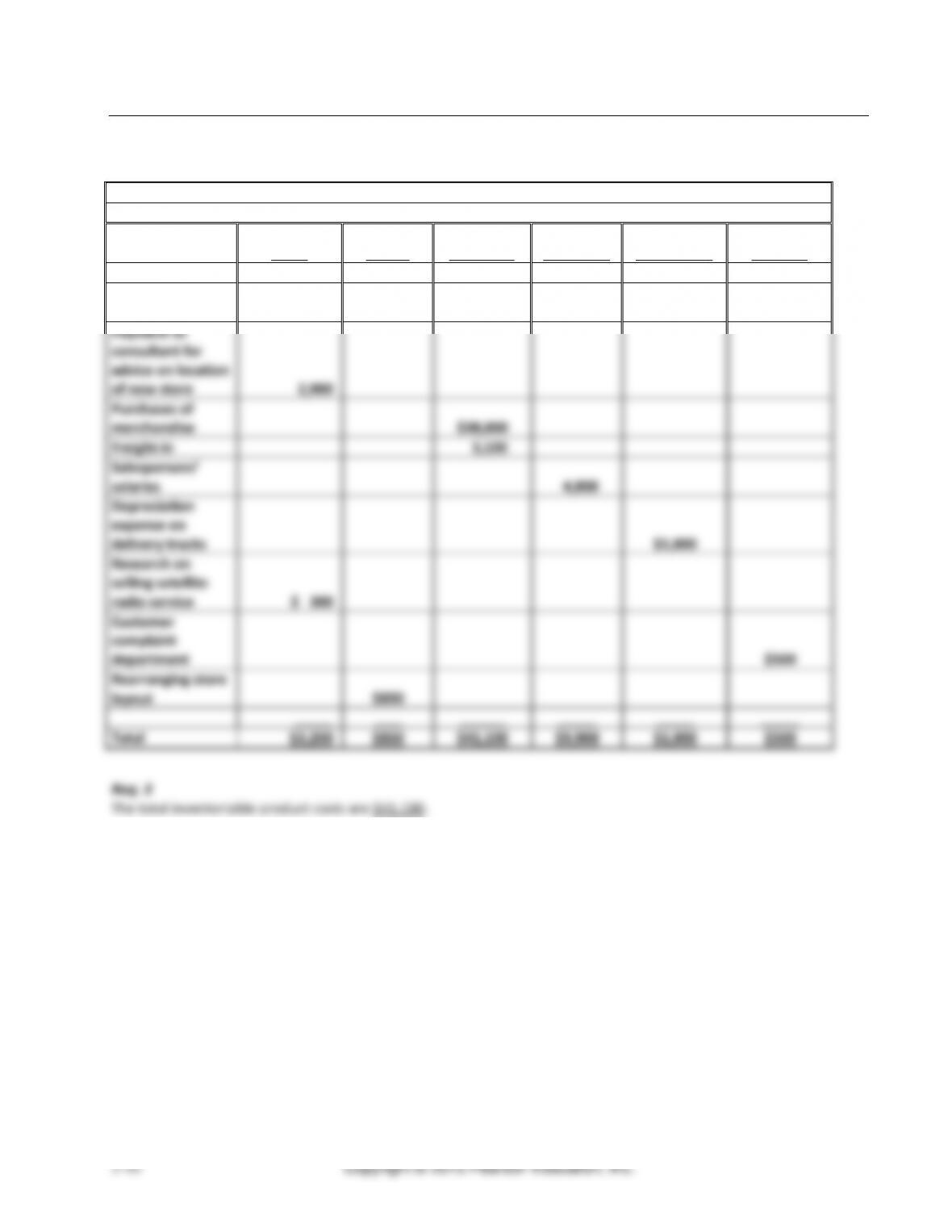

Value Chain Cost Classification

R & D

Design

Purchases

Marketing

Distribution

Customer

Service

Newspaper

advertisements

$5,100

Payment to

consultant for

advice on location

of new store

2,900

Purchases of

merchandise

$38,000

Freight-in

3,100

Salespersons’

salaries

4,800

Depreciation

expense on

delivery trucks

$1,000

Research on

selling satellite

radio service

$ 300

Customer

complaint

department

$500

Rearranging store

layout

$850

Total

$3,200

$850

$41,100

$9,900

$1,000

$500

Req. 3

The total inventoriable product costs are $41,100.

Chapter 2 Building Blocks of Managerial Accounting

(15 min.) E2-19A

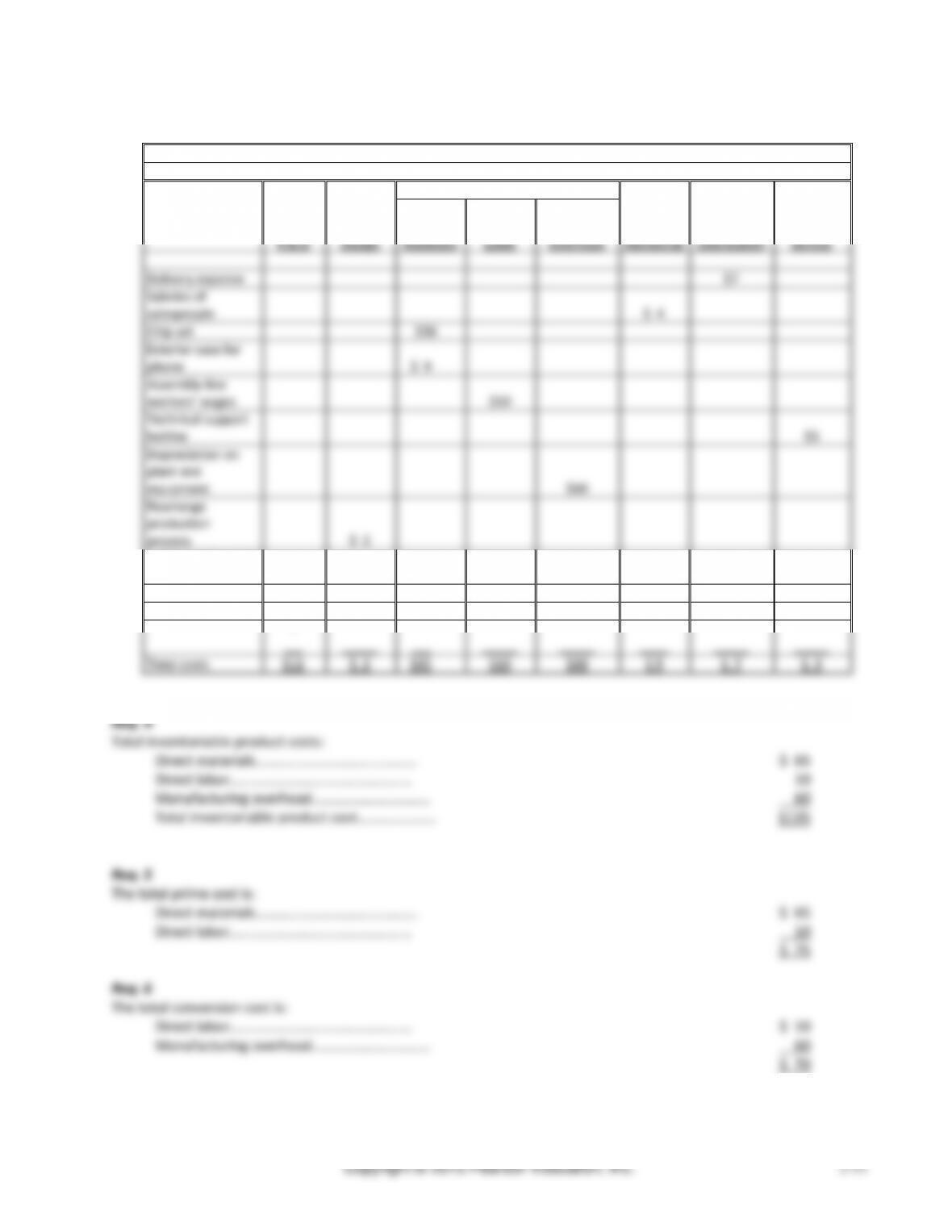

Reqs. 1, 2, and 3

Value Chain Cost Classification

Production

R & D

Design

Direct

Materials

Direct

Labor

Manufactur-

ing

Overhead

Marketing

Distribution

Customer

Service

Delivery expense

$7

Salaries of

salespeople

$ 4

Chip set

$56

Exterior case for

phone

$ 9

Assembly-line

workers’ wages

$10

Technical support

hotline

$3

Depreciation on

plant and

equipment

$60

Rearrange

production

process

$ 2

1-800 (toll-free) line

for customer orders

5

Scientists’ salaries

$11

–

Total costs

$11

$ 2

$65

$10

$60

$ 9

$ 7

$ 3

Chapter 2 Building Blocks of Managerial Accounting

Req. 2

Total manufacturing overhead costs

=

IM + IL + Other MOH

=

$45 + 160 + 210 = $415

Req. 3

Total inventoriable product costs

=

DM + DL + MOH

=

$1,660 + 700 + 415 = $2,775

Req. 4

Total prime costs

=

DM + DL

=

$1,660 + 700 = $2,360

Req. 5

Total conversion costs

=

DL + MOH

=

$700 + 415 = $1,115

Req. 6

Total period costs

=

$520

(10 min.) E2-22A

Current Assets

Current assets:

Cash

$ 15,200

Accounts receivable

75,000

Inventories:

Raw materials inventory

$9,700

Work in process inventory

35,000

Finished goods inventory

59,000

Total inventories

103,700

Prepaid expenses

5,500

Total current assets

$199,400

The company must be a manufacturer, because it has three kinds of inventory: raw materials, work in process, and

finished goods.

Managerial Accounting 4e Solutions Manual

(10-15 min.) E2-23A

Cost of goods sold calculation:

Beginning inventory

$ 18,000

Plus: Purchases and freight-in*

659,500

Cost of goods available for sale

677,500

Less: Ending inventory

(12,800)

Cost of goods sold

$ 664,700

Pampered Pets

Income Statement

For Last Year

Sales revenue

$ 986,000

Less: Cost of goods sold

(664,700)

Gross profit

321,300

Less operating expenses:

Website expenses

$ 58,500

Marketing expenses

30,700

Freight-out expenses

28,500

Total operating expenses

(117,700)

Operating income

$ 203,600

*purchases of $640,000 + freight-in of $19,500 = $659,500

(5-10 min.) E2–24A

Calculation of Direct Materials Used

Beginning Raw Materials Inventory

$ 17,000

Plus: Purchases of direct materials, freight-in, and import

duties

63,000

Materials available for use

$ 80,000

Less: Ending Raw Material Inventory

(15,000)

Direct materials used

$ 65,000

Schedule of Cost of Goods Manufactured

Beginning Work in Process Inventory

$ 26,000

Plus: Manufacturing costs incurred

Direct materials used (from previous schedule)

65,000

Direct labor

123,000

Manufacturing overhead

148,000

Total manufacturing costs to account for

$ 362,000

Less: Ending Work in Process Inventory

(19,000)

Cost of goods manufactured

$ 343,000

Managerial Accounting 4e Solutions Manual

(15-20 min.) E2-26A

Blue Sea Company

Income Statement

For Current Year

Sales revenue (39,000 units x $10)

$ 390,000

Less: Cost of goods sold (from previous exercise)

230,800

Gross profit

$ 159,200

Less operating expenses:

Marketing expenses

76,000

General and administrative expenses

27,500

Total operating expenses

$ 103,500

Operating income

$ 55,700

Students may simply use the $230,800 cost of goods sold computation from E2-25A, rather than repeating the details

of the computation of cost of goods sold here.

Chapter 2 Building Blocks of Managerial Accounting

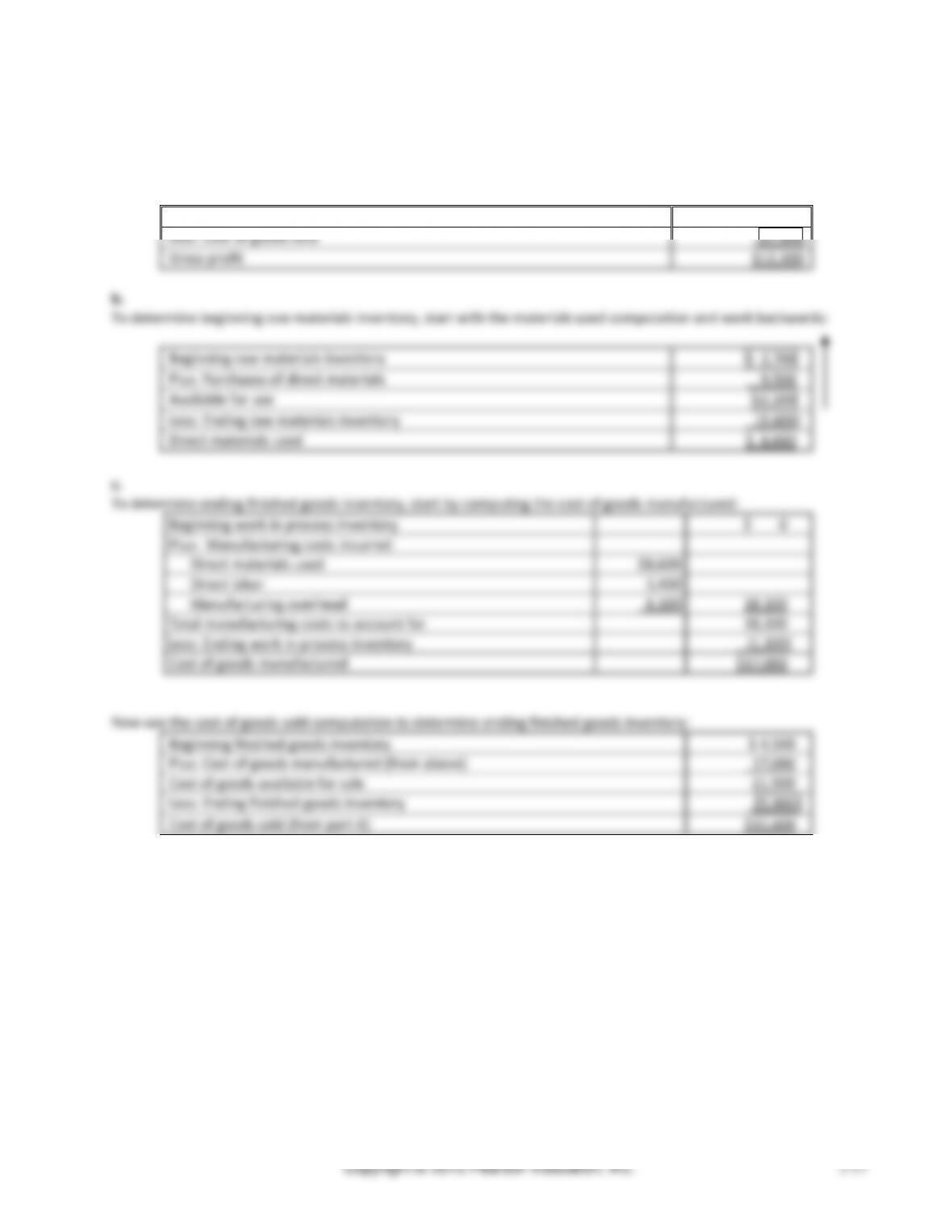

(25 min.) E2-27A

Instructional note: This is a fairly challenging exercise that requires students to work backwards through financial

statement elements.

a.

Revenues

$27,700

Less: Cost of goods sold

15,600

Gross profit

$12,100

b.

To determine beginning raw materials inventory, start with the materials used computation and work backwards:

Beginning raw materials inventory

$ 2,700

Plus: Purchases of direct materials

9,500

Available for use

12,200

Less: Ending raw materials inventory

(3,600)

Direct materials used

$ 8,600

c.

To determine ending finished goods inventory, start by computing the cost of goods manufactured:

Beginning work in process inventory

$ 0

Plus: Manufacturing costs incurred

Direct materials used

$8,600

Direct labor

3,400

Manufacturing overhead

6,100

18,100

Total manufacturing costs to account for

18,100

Less: Ending work in process inventory

(1,100)

Cost of goods manufactured

$17,000

Now use the cost of goods sold computation to determine ending finished goods inventory:

Beginning finished goods inventory

$ 4,500

Plus: Cost of goods manufactured (from above)

17,000

Cost of goods available for sale

21,500

Less: Ending finished goods inventory

(5,900)

Cost of goods sold (from part A)

$15,600

Chapter 2 Building Blocks of Managerial Accounting

Copyright © 2015 Pearson Education, Inc.

2-19

(10 min.) E2-29A

1)

Variable costs

=

($1 x 25,000,000)

=

$25,000,000

+ Fixed costs

=

6,000,000

= Total costs

=

$31,000,000

2)

$31,000,000

÷

25,000,000 units

=

$1.24 per unit

3)

$ 6,000,000

÷

25,000,000 units

=

$0.24 per unit

4)

Variable costs

=

($1 x 30,000,000)

=

$30,000,000

+ Fixed costs

=

6,000,000

= Total costs

=

$36,000,000

5)

$36,000,000

÷

30,000,000 units

=

$1.20 per unit

6)

$ 6,000,000

÷

30,000,000 units

=

$0.20 per unit

7)

The average product cost decreases as production volume

increases because the company is spreading its fixed costs over

5 million more units. The company will be operating more

efficiently, so the average cost of making each unit decreases.

Managerial Accounting 4e Solutions Manual

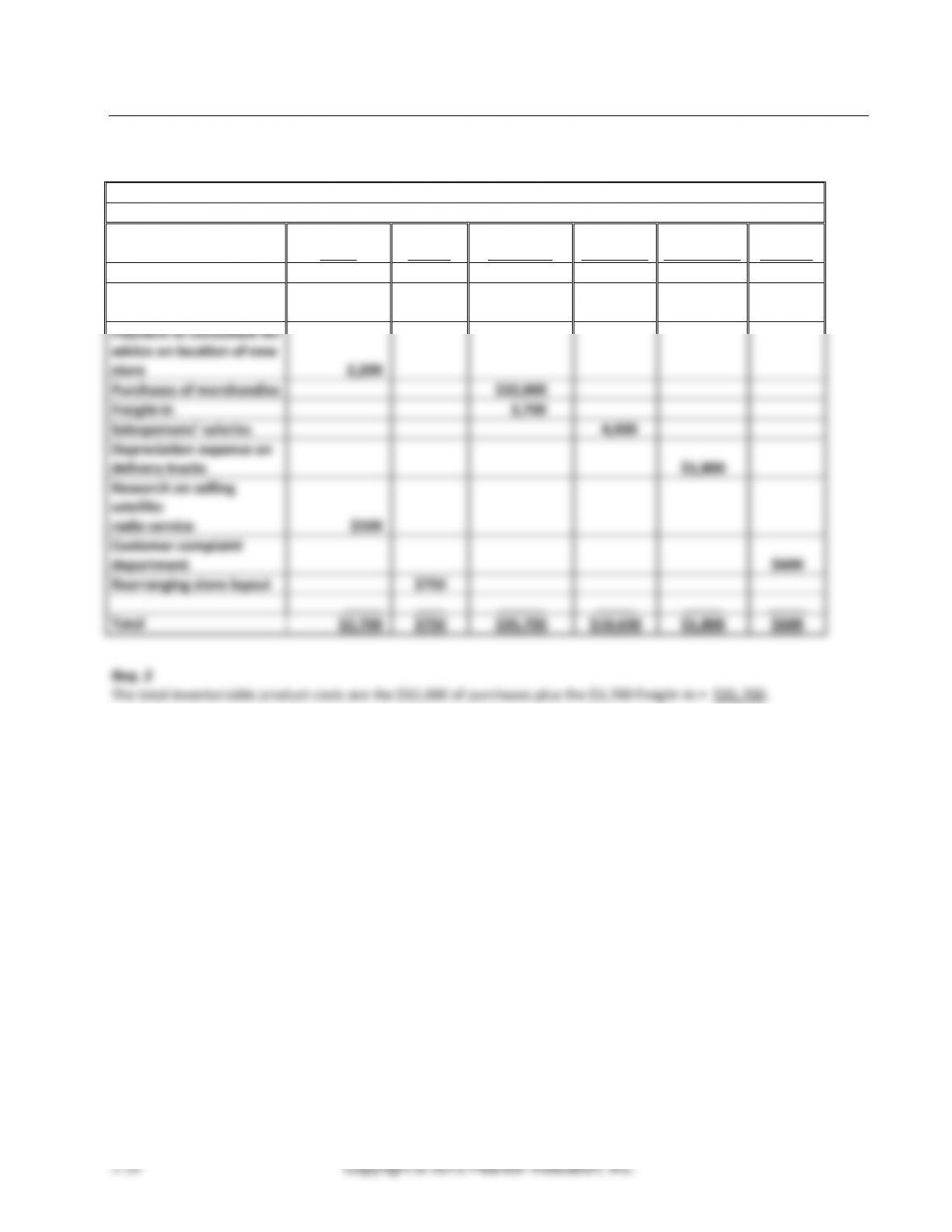

Exercises (Group B)

(10-15 min.) E2-30B

Reqs. 1 and 2

Value Chain Cost Classification

R & D

Design

Purchases

Marketing

Distribution

Customer

Service

Newspaper

advertisements

$5,700

Payment to consultant for

advice on location of new

store

2,200

Purchases of merchandise

$32,000

Freight-in

3,700

Salespersons’ salaries

4,900

Depreciation expense on

delivery trucks

$1,800

Research on selling

satellite

radio service

$500

Customer complaint

department

$600

Rearranging store layout

$750

Total

$2,700

$750

$35,700

$10,600

$1,800

$600

Req. 3

The total inventoriable product costs are the $32,000 of purchases plus the $3,700 freight-in = $35,700.