Copyright © 2015 Pearson Education, Inc.

14–19

(20-30 min.) P14-33A

Req. 1

Mirabel Optical Corporation

Trend Percentages

2014

2013

2012

2011

Net sales revenue

113%

107%

95%

100%

Net income

122%

88%

73%

100%

Common stock– holders’ equity

106.5%

93.5%

82.5%

100%

Req. 2

Dollar amounts in thousands

2012

2013

2014

Net income

$365

=

10.00%

$440

=

12.50%

$610

=

15.25%

Avg. CSE

$3,650

$3,520

$4,000

__________

Managerial Accounting 4e Solutions Manual

(20-30 min.) P14-34A

Req. 1

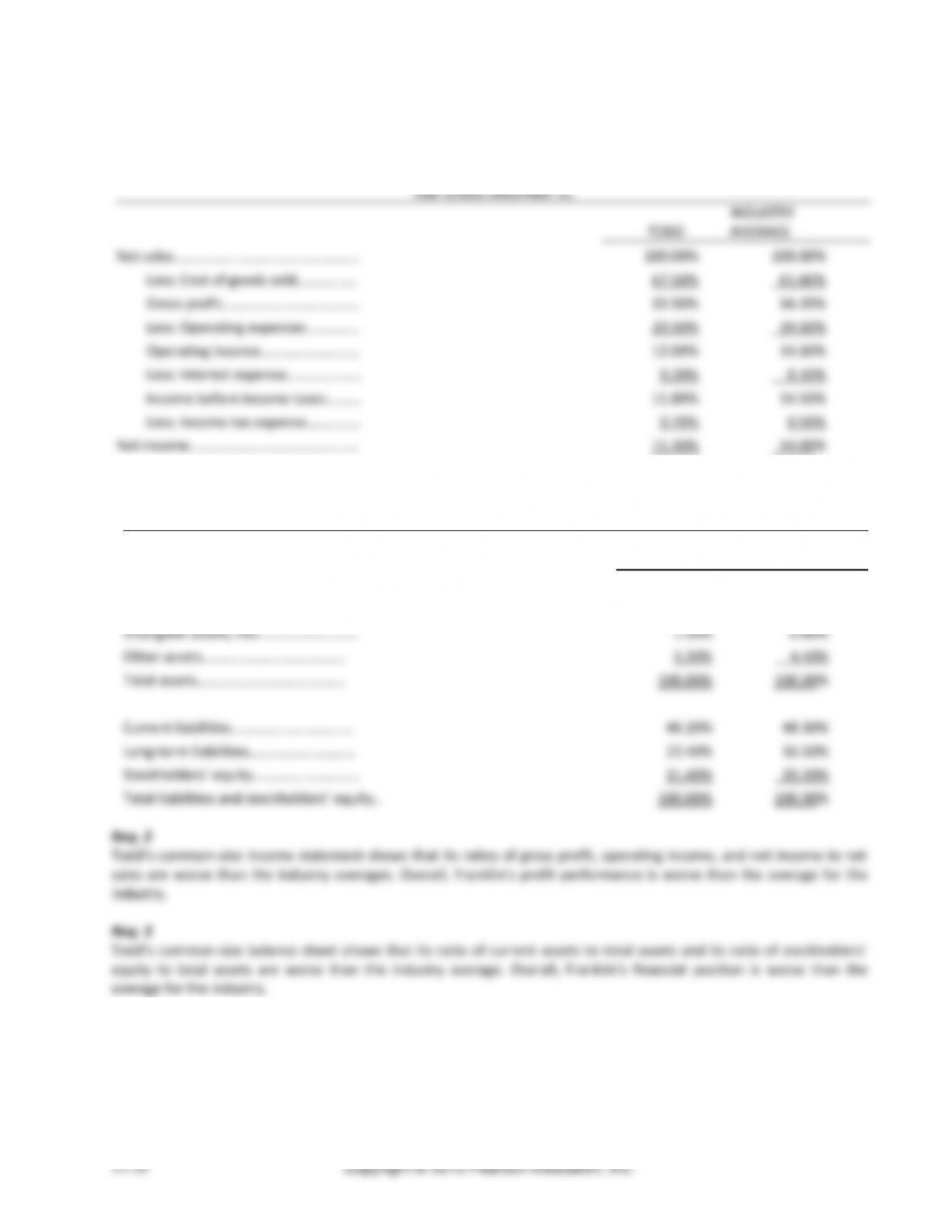

Todd Department Stores, Inc.

Common-Size Income Statement Compared

to Industry Average

Year Ended December 31

TODD

INDUSTRY

AVERAGE

Net sales…………………………………………….

100.00%

100.00%

Less: Cost of goods sold……………..

67.50%

65.80%

Gross profit…………………………………

32.50%

34.20%

Less: Operating expenses……………

20.50%

19.60%

Operating income……………………….

12.00%

14.60%

Less: Interest expense…………………

0.20%

0.10%

Income before income taxes……….

11.80%

14.50%

Less: Income tax expense……………

0.70%

0.50%

Net income………………………………………..

11.10%

14.00%

Todd Department Stores, Inc.

Common-Size Balance Sheet Compared to Industry Average

As of December 31

TODD

INDUSTRY

AVERAGE

Current assets……………………………….

67.70%

70.90%

Fixed assets, net…………………………….

25.60%

24.10%

Intangible assets, net……………………….

1.50%

0.60%

Other assets………………………………….

5.20%

4.40%

Total assets…………………………………..

100.00%

100.00%

Current liabilities…………………………….

46.20%

48.30%

Long-term liabilities…………………………

22.40%

16.50%

Stockholders’ equity…………………………

31.40%

35.20%

Total liabilities and stockholders’ equity..

100.00%

100.00%

Req. 2

Todd’s common-size income statement shows that its ratios of gross profit, operating income, and net income to net

sales are worse than the industry averages. Overall, Franklin’s profit performance is worse than the average for the

industry.

Req. 3

Todd’s common–size balance sheet shows that its ratio of current assets to total assets and its ratio of stockholders’

equity to total assets are worse than the industry average. Overall, Franklin’s financial position is worse than the

average for the industry.

Managerial Accounting 4e Solutions Manual

(40-50 min.) P14-36A

Req. 1

2014

2013

a.

Current ratio:

$352,000

=

1.6

$390,000

=

1.5

$220,000

$260,000

b.

Times-interest-

$76,650

=

7.3

$76,260

=

6.15

earned ratio:

$10,500

$12,400

c.

Inventory

$245,000

=

1.75

$216,000

=

1.2

turnover:

($135,000 + $145,000) / 2

($145,000 + $215,000) / 2

d.

Return on

$58,300 − 5,500*

=

0.33

$39,100 − 5,500*

=

0.28

common stock- holders’

equity:

($132,000 + 188,000) / 2

($188,000 + $52,000) / 2

e.

Earnings per share of

common stock:

$58,300 − 5,500*

=

$4.40

$39,100 − 5,500*

=

$2.80

12,000

12,000

f.

Price/earnings

$49.50

=

11.25

$27.02

=

9.65

ratio:

$4.40

$2.80

__________

*$110,000 × .05 = $5,500

Req. 2

Decisions:

a. Banfield’s ability to pay its debts and to sell inventory improved during 2014.

b. The investment attractiveness of Banfield’s common stock appears to have increased.

Managerial Accounting 4e Solutions Manual

Problems (Group B)

(20-30 min.) P14-38B

Req. 1

Eyesight Vision Corporation

Trend Percentages

2014

2013

2012

2011

Net sales revenue

110.8%

105.6%

95.2%

100%

Net income

124%

82%

76%

100%

Common stock– holders’ equity

154%

96%

109%

100%

Req. 2

Dollar amounts in thousands

2014

2013

2012

Net income

$682

=

17.05%

$451

=

13.75%

$418

=

12.50%

Avg. CSE

$4,000

$3,280

$3,344

__________

Managerial Accounting 4e Solutions Manual

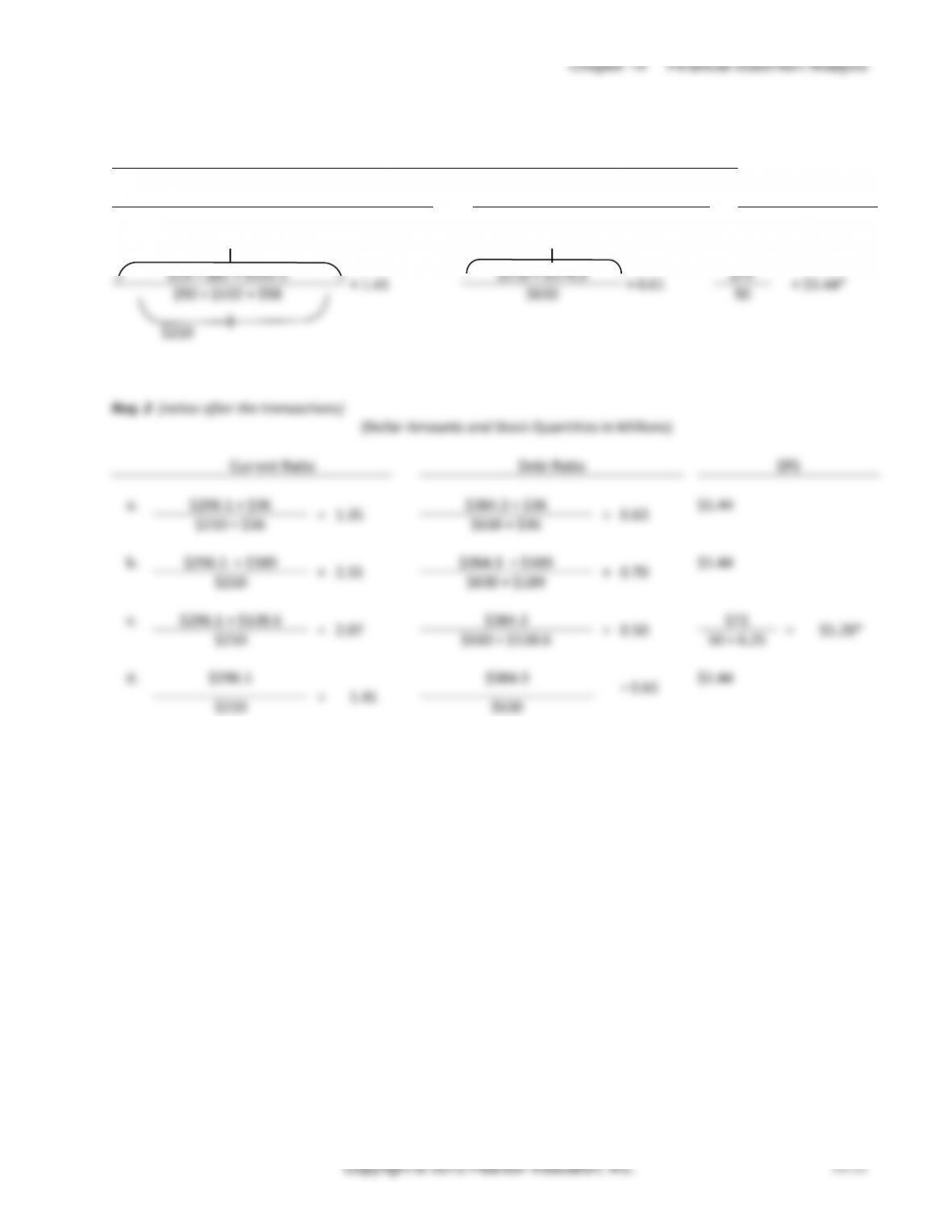

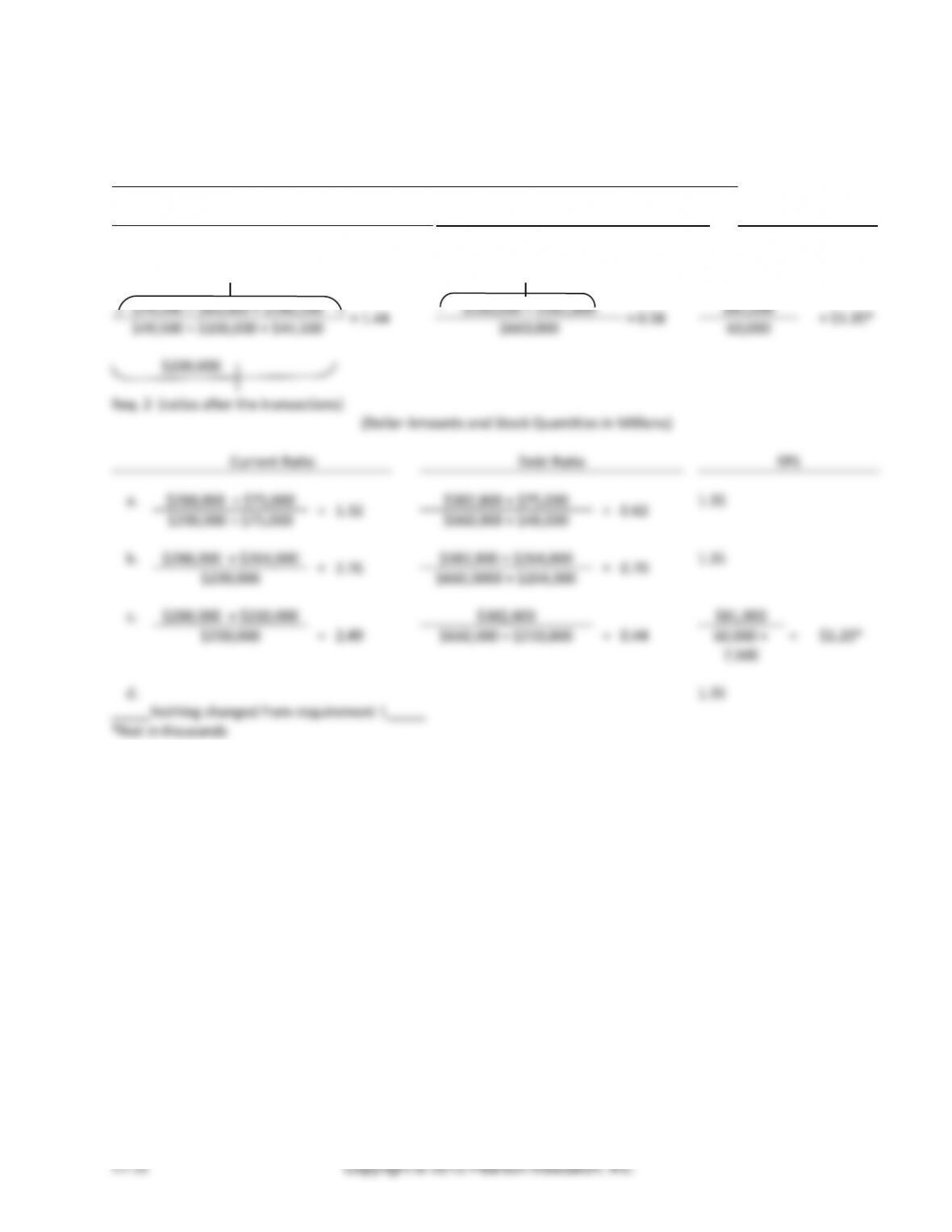

(30-40 min.) P14-40B

Req. 1 (ratios before the transactions)

(Dollar Amounts and Stock Quantities in Millions)

Current Ratio

Debt Ratio

Earnings per Share

$288,000

$382,800

$24,500 + $83,000 + $180,500

= 1.44

$200,000 + $182,800

= 0.58

$81,000

= $1.35*

$49,500 + $106,000 + $44,500

$660,000

60,000

$200,000

(Dollar Amounts and Stock Quantities in Millions)

Current Ratio

Debt Ratio

EPS

a.

$288,000 + $75,000

=

1.32

$382,800 + $75,000

=

0.62

1.35

$200,000 + $75,000

$660,000 + $48,000

b.

$288,000 + $264,000

=

2.76

$382,800 + $264,000

=

0.70

1.35

$200,000

$660,0000 + $264,000

c.

$288,000 + $210,000

=

2.49

$382,800

=

0.44

$81,000

=

$1.20*

$200,000

$660,000 + $210,000

60,000 +

7,500

d.

1.35

Managerial Accounting 4e Solutions Manual

(45-60 min.) P14-42B

LX Electronics

Rose Electronics

a.

Acid-test ratio:

$29,200 + $42,000 + $38,000

=

1.04

$20,500 + $22,200 + $44,000

=

0.85

$105,000

$102,000

b.

Inventory

$210,000

=

2.8

$255,000

=

2.72

turnover:

($83,000 + $67,000) / 2

($82,500 + $105,000) / 2

c.

Days’ sales in

receivables:

($42,000 +

$38,000) / 2

=

32

($40,700 + $44,000) / 2

=

30.25

$456,250 / 365

$511,000 / 365

d.

Debt ratio:

$105,000

=

0.35

$136,000

=

0.5

$300,000

$272,000

e.

Earnings per share

$50,000

=

$5.00

$64,400

=

$4.60

of common stock:

10,000

14,000

f.

Price/earnings

$80.00

=

16

$85.10

=

18.5

ratio:

$5.00

$4.60

Chapter 14 Financial Statement Analysis

Discussion & Analysis

A14-43

1. Describe horizontal analysis. Describe vertical analysis. What is each technique used for? How are the two

methods similar? How are they different?

2. How is the current ratio calculated? What is it used to measure? How is it interpreted?

3. Assume a company has a current ratio of 2.0. List two examples of transactions that could cause the current

4. What does the accounts receivable turnover measure? What does a relatively high accounts receivable turnover

indicate about a company?

5. Describe the set of circumstances that could result in net income increasing while ROI decreases.

6. Suppose a company has a relatively high inventory turnover. What does the high inventory turnover indicate

about the company’s short-term liquidity?

7. Describe at least four financial conditions that may signal financial trouble.

• Has net income decreased significantly for several years in a row? Has income turned into a loss? Most

Chapter 14 Financial Statement Analysis

Application & Analysis

A14-44

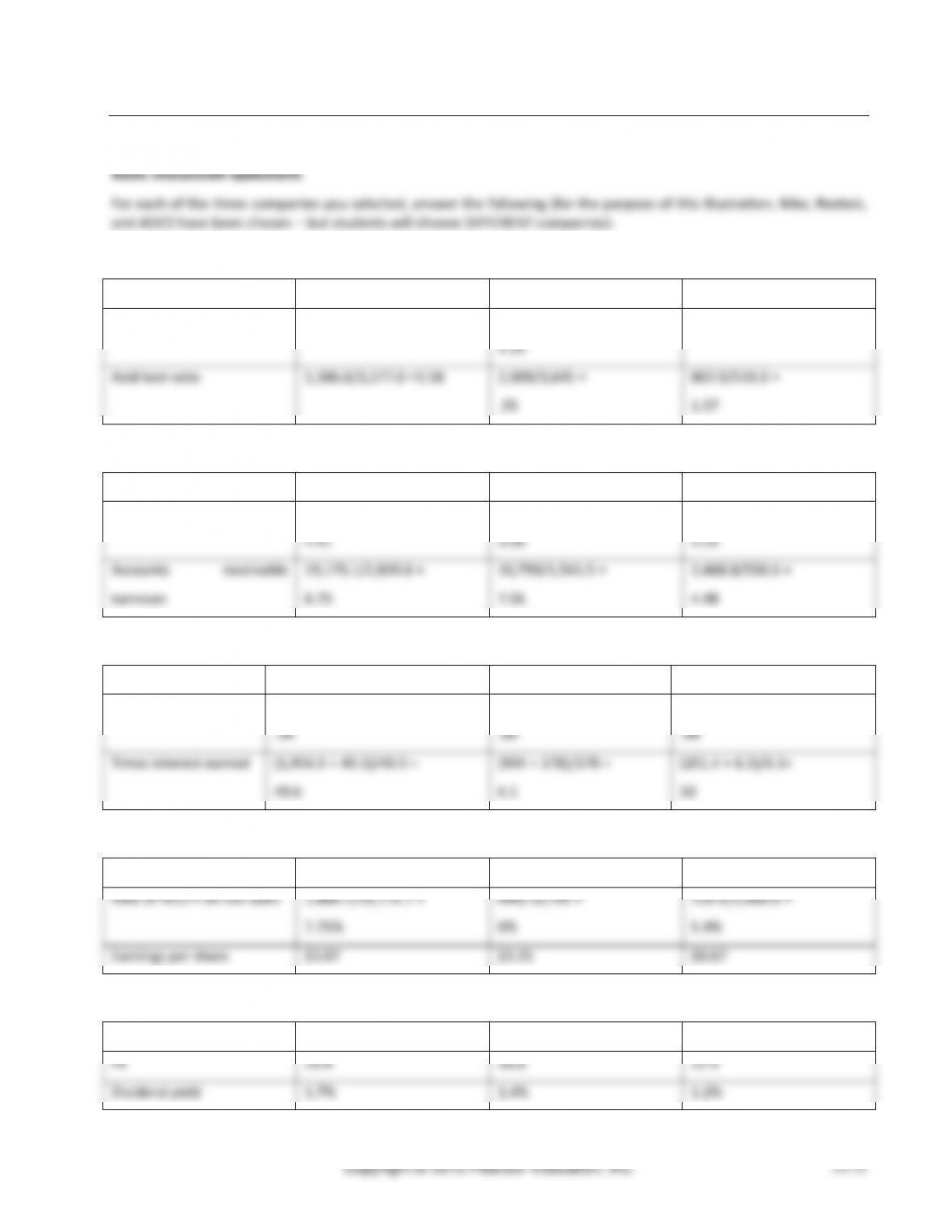

1. Calculate two ratios that measure the ability to pay current liabilities.

Nike

Reebok

ASICS

Current ratio

9,734.0/3,277.0 = 2.97

4,934/3,645 =

1.35

1,304.3/510.3 = 2.56

Acid test ratio

5,186.6/3,277.0 =1.58

2,009/3,645 =

.55

802.9/510.3 =

1.57

2. Calculate at least two ratios that measure the ability to sell inventory and collect receivables.

Nike

Reebok

ASICS

Inventory turnover

10,571.7/2,397.7 =

4.41

5,543/1812 =

3.06

1,417.4/402 =

3.53

Accounts receivable

turnover

19,176.1/2,839.6 =

6.75

10,799/1,541.5 =

7.01

2,468.8/550.6 =

4.48

3. Calculate at least two ratios that measure the ability to pay long-term debt.

Nike

Reebok

ASICS

Debt ratio

4,556.5/13,249.6 =

.34

6,133/9,533 =

.64

782.2/1,784.9 =

.44

Times interest earned

(1,956.5 + 40.3)/40.3 =

49.6

(904 + 178)/178 =

6.1

(201.4 + 6.3)/6.3=

33

4. Calculate at least two ratios that measure profitability.

Nike

Reebok

ASICS

Rate of return on net sales

1,486.7/19,176.1 =

7.75%

644/10,799 =

6%

133.5/2,468.8 =

5.4%

Earnings per share

$3.07

$3.25

$0.67

5. Calculate at least two ratios that help to analyze the stock as an investment.

Nike

Reebok

ASICS

PE

19.4

16.8

12.5

Dividend yield

1.7%

1.4%

1.2%

Managerial Accounting 4e Solutions Manual

Now that you have crunched the numbers, interpret the ratios. What can you tell about each company and its

financial position? Is one company clearly better than the others in terms of its financial position, or are all three

A14-45

a. The ethical issues in this situation are:

Competence: “Provide decision support information and recommendations that are accurate, clear, concise, and

timely.” If Tom does not disclose all of the ratios clearly, even those that are weak, the decision support

1. Ability to pay current liabilities:

a. Coca-Cola’s current ratios in 2012, 2011, and 2010 were 1.09, 1.05, and 1.17, respectively. Their acid-test

ratios in 2012, 2011, and 2010 were 0.77, 0.78, and 0.85, respectively.

b. PepsiCo’s current ratios in 2012, 2011, and 2010 were 1.10, 0.96, and 1.11, respectively. Their acid-test ratios

in 2012, 2011, and 2010 were 0.80, 0.62, and 0.80, respectively.

Chapter 14 Financial Statement Analysis

2010 was $9,019, $8,572, and $11,809, respectively. Their working capital ($ in millions) in 2012, 2011, and

2010 was $2,507, $1,214, and $3,071, respectively.

2. The Coca-Cola Company:

a. Ability to pay current liabilities: Coca–Cola’s current ratio was weak, and their acid-test ratio was lower than

average. This means that Coca-Cola may have difficulties paying off their current liabilities.

3. PepsiCo, Inc:

a. Ability to pay current liabilities: PepsiCo’s current ratio was weak, and their acid-test ratio was lower than

average. This means that PepsiCo may have difficulties paying off their current liabilities.

4. The Coca-Cola Company vs. PepsiCo, Inc:

a. Ability to pay current liabilities: Coca–Cola’s current and acid–test ratios appear to be stronger than PepsiCo’s

ratios.

b. Ability to sell inventory and collect receivables: Coca–Cola’s inventory and receivables turnover appears to be

5. Conclusions:

Team Project

A14-47

Student answers will vary.