Chapter 14 Financial Statement Analysis

Chapter 14

Financial Statement Analysis

Quick Check

Answers:

Chapter 14 Financial Statement Analysis

(5 min.) S14-7

a.

Debt ratio

=

Total liabilities

=

$8,714,000

=

0.45

Total assets

$19,345,000

b. The debt ratio is fairly low. The company’s ability to pay its liabilities appears strong.

(10 min.) S14-8

a.

Rate of return on net

sales

=

Net income

=

$6,597,100

=

18.5%

Net sales

$35,587,500

Net Interest

b.

Rate of return

=

income + expense

=

$6,597,100 + $217,500

on total assets

Average total assets

18,455,500

=

36.92%

c.

Rate of return

Net Preferred

on common

=

Income − dividends

=

$6,597,100 − $0

=

65.00%

stockholders’ equity

Average common stockholders’

equity

$10,151,500

These rates of return are strong.

(5-10 min.) S14-9

1.

EPS

=

Net income − Preferred dividends

Number of shares of common

=

$6,597,100 − $0

710,000

stock outstanding

=

$9.29

Market price per share

of common stock

2.

Price/earnings

ratio

=

=

$63.50

=

6.84 times

EPS

$9.29

Managerial Accounting 4e Solutions Manual

(10 min.) S14-10

1.

Emmett talks about the financial woes of the company he works

for when he is out with a group of friends. He shares that the

company will not be able to meet the ratios specified in the loan

covenants.

Confidentiality – Keep information

confidential except when disclosure is

authorized or legally required.

2.

Marion prepares the financial statements, but the internal control

system weaknesses are not disclosed.

Credibility – Disclose all relevant

information that could reasonably be

expected to influence an intended

user’s understanding of the reports,

analyses, or recommendations.

3.

Jeanne, an accountant working in the Accounts Payable

Department, writes a company check to herself for $1,500 to

temporarily borrow money to pay her apartment rent; she plans

on paying back the money after her next paycheck.

Integrity – Refrain from engaging in any

conduct that would prejudice carrying

out duties ethically

4.

Shirley has not participated in any continuing education activities

since she graduated five years ago because life has just been too

busy. She is unprepared for the company to issue IFRS-based

statements for the first time this year.

Competence – Maintain an appropriate

level of professional expertise by

continually developing knowledge and

skills.

5.

Floyd, the corporate controller, prepares a report for the board of

directors that summarizes the year. Floyd, wanting to look good,

only includes the favorable ratios and favorable events in this

report.

Credibility – Disclose all relevant

information that could reasonably be

expected to influence an intended

user’s understanding of the reports,

analyses, or recommendations.

Chapter 14 Financial Statement Analysis

Exercises (Group A)

(5-15 min.) E14-11A

2014

2013

2012

Total current assets

$379,780

$356,000

$309,000

Total current liabilities

188,000

184,000

149,000

Working capital

$191,780

$172,000

$160,000

11.5%

Chapter 14 Financial Statement Analysis

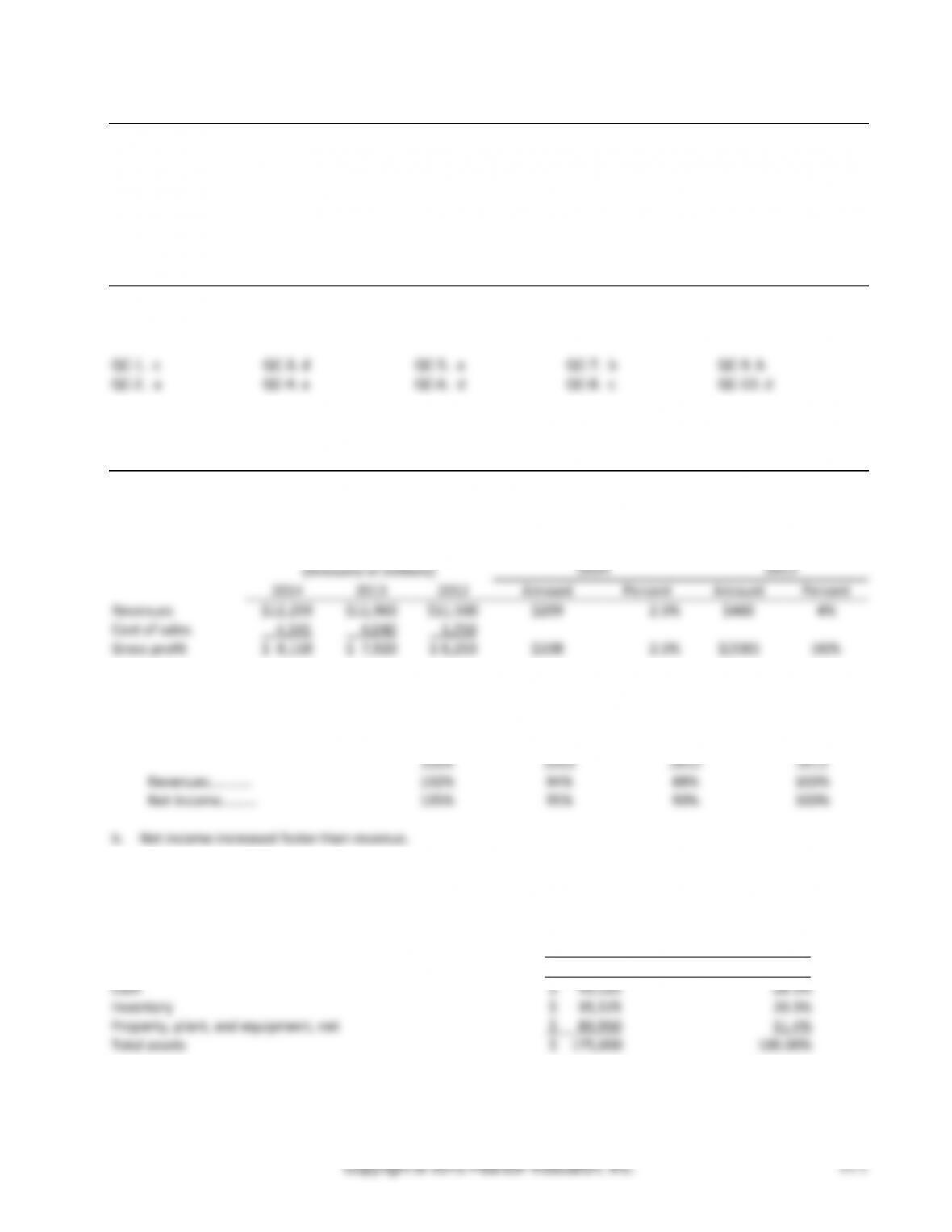

(10-15 min.) E14-15A

Mariner Designs

Income Statement

For the years ended December 31, 2014 and 2013

2014

2013

Net sales revenue…………………………….

100.00%

100.00%

Less: Cost of goods sold……………………

47.03%

50.3%

Gross Profit………….…………………………..

52.97%

49.70%

Less: Operating expenses…………………

26.22%

28.46%

Operating income……………………………

26.75%

21.24%

Less: Interest expense……………………..

1.75%

0.83%

Income before income taxes……………

25.00%

20.41%

Less: Income tax expense…………………

3.74%

3.75%

Net income……………………………………….

21.26%

16.67%

An investor would be pleased with 2014 in comparison with 2013. Net sales and net income are both up significantly

from 2013. Cost of goods sold and selling and general expenses — the two largest expenses — consumed smaller

percentages of total revenues in 2014, and net income represents a higher percentage of revenues. Overall, profits are

rising.

(10-15 min.) E14-16A

a.

Current ratio

=

$178,750

=

1.43

$125,000

b.

Acid-test (quick)

=

$16,500 + 10,750 + 49,000

=

0.61

ratio

$125,000

c.

Inventory turnover

=

$319,000

=

4.00 times

79,750

d.

Days’ sales in

=

$63,180

=

54 days

average receivables

$1,170

Chapter 14 Financial Statement Analysis

(10-15 min.) E14-19A

2014

2013

a.

Price/earnings ratio:

$17.50

=

20.0

$14.00

=

17.5

($83,375 − $12,500) / 81,000

($77,300 − $12,500) / 81,000

b.

Dividend yield:

$19,845 / 81,000

=

1.40%

$19,845 / 81,000

=

1.75%

$17.50

$14.00

c.

Book value per share of common stock:

$772,000 − $205,000

=

$7.00

$605,950 − $205,000

=

$4.95

81,000

81,000

The stock’s attractiveness increased during 2013, as shown by the increases in the price/earnings ratio and in book

value per share. The dividend yield decreased, but that would be important only to investors who want dividends.

Overall, the common stock looks more attractive than it did a year ago.

Chapter 14 Financial Statement Analysis

(5 min.) E14-21A

a. People

b. Profit

Copyright © 2015 Pearson Education, Inc.

14–12

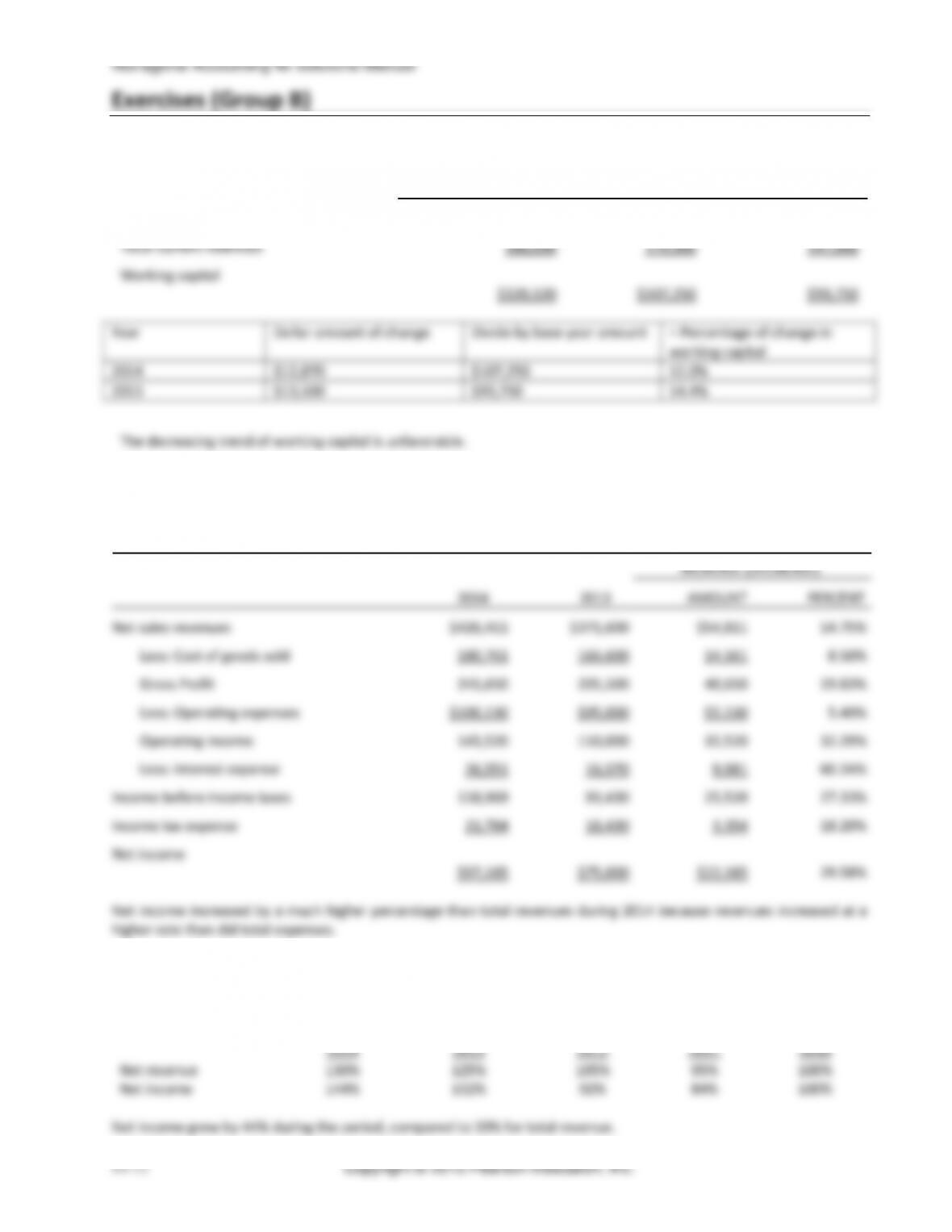

(5-15 min.) E14-22B

2014

2013

2012

Total current assets

$306,120

$286,250

$240,750

Total current liabilities

186,000

179,000

147,000

Working capital

$120,120

$107,250

$93,750

Year

Dollar amount of change

Divide by base year amount

= Percentage of change in

working capital

2014

$12,870

$107,250

12.0%

2013

$13,500

$93,750

14.4%

The decreasing trend of working capital is unfavorable.

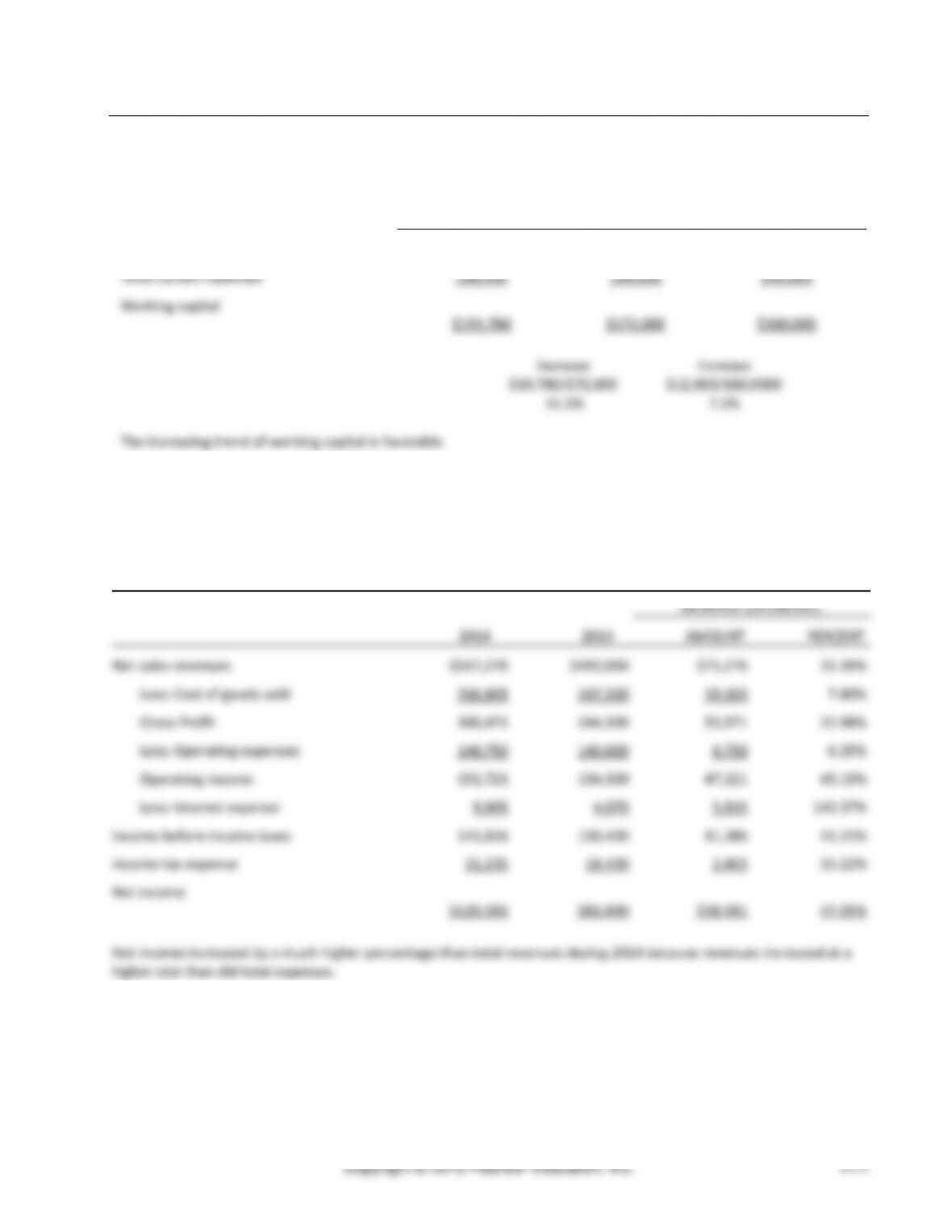

(10-15 min.) E14-23B

Enchanted Designs

Horizontal Analysis of Comparative Income Statement

Years Ended December 31, 2014 and 2013

INCREASE (DECREASE)

2014

2013

AMOUNT

PERCENT

Net sales revenues

$426,411

$371,600

$54,811

14.75%

Less: Cost of goods sold

180,761

166,600

14,161

8.50%

Gross Profit

245,650

205,500

40,650

19.83%

Less: Operating expenses

$100,130

$95,000

$5,130

5.40%

Operating income

145,520

110,000

35,520

32.29%

Less: Interest expense

26,551

16,570

9,981

60.24%

Income before income taxes

118,969

93,430

25,539

27.33%

Income tax expense

21,784

18,430

3,354

18.20%

Net income

$97,185

$75,000

$22,185

29.58%

Net income increased by a much higher percentage than total revenues during 2014 because revenues increased at a

higher rate than did total expenses.

(5-10 min.) E14-24B

Trend percentages:

2014

2013

2012

2011

2010

Net revenue

130%

125%

105%

95%

100%

Net income

144%

132%

92%

84%

100%

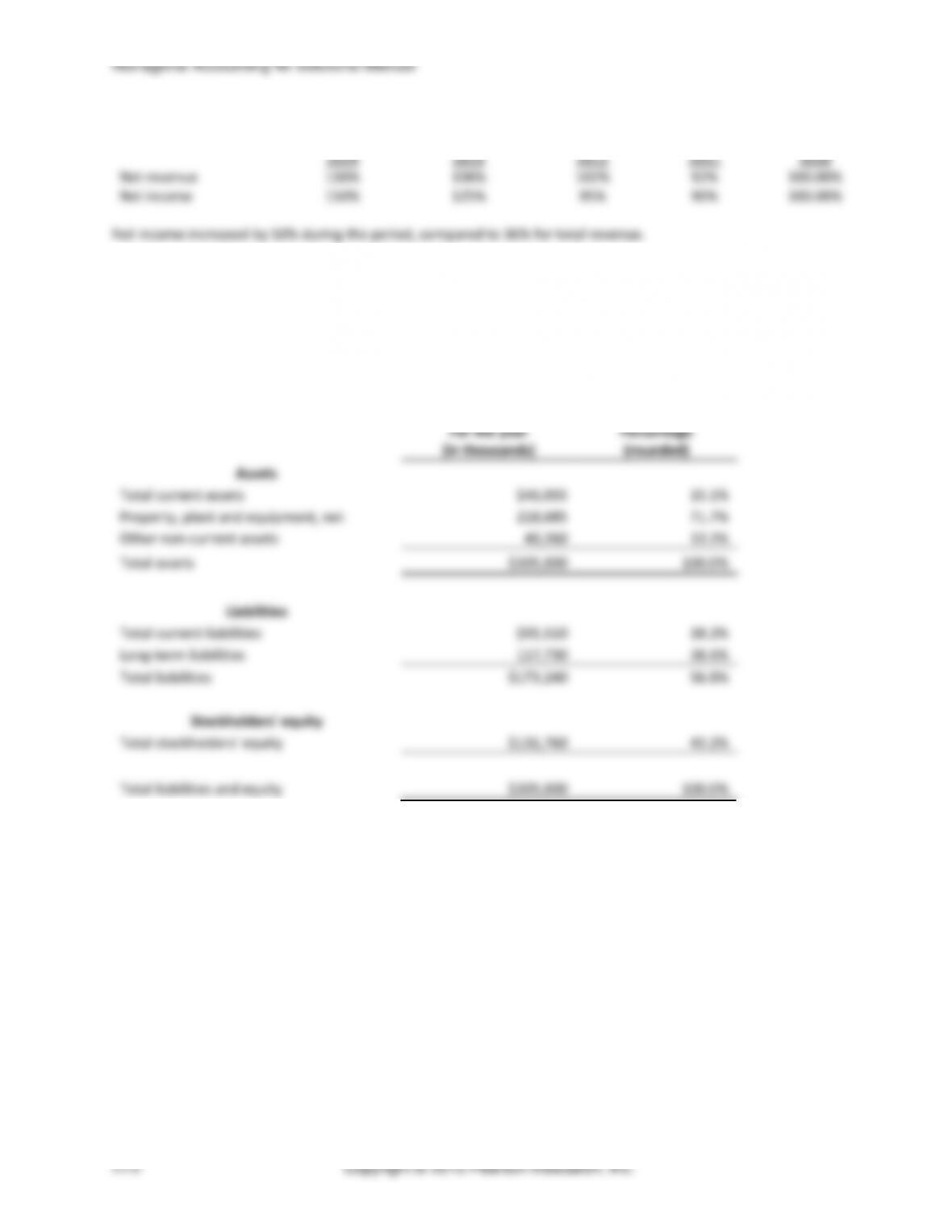

Net income grew by 44% during the period, compared to 30% for total revenue.

Chapter 14 Financial Statement Analysis

(10-15 min.) E14-25B

Eta Designs, Inc.

Vertical Analysis of Balance Sheet

As of December 31

AMOUNT

PERCENT

ASSETS

Total current assets………………………..

$44,250

14.75%

Property, plant, and equipment, net

$216,000

72%

Other assets…………………………………..

$39,750

13.25%

Total assets……………………………………

$300,000

100%

LIABILITIES

Total current liabilities…………………….

$55,500

18.5%

Long-term debt……………………………….

$115,500

38.5%

Total liabilities…………………………………

$171,000

57.0%

STOCKHOLDERS’ EQUITY

Total stockholders’ equity………………..

$129,000

43.0%

Total liabilities and stockholders’ equity

$300,000

100%

Chapter 14 Financial Statement Analysis

(15-20 min.) E14-28B

a. Current ratio:

2014:

$429,300 (60,500 + 26,500 + 115,500 + 226,800)

=

1.59

$270,000

2013:

$439,790 (45,000 + 0 + 108,230 + 286,560)

=

2.21

$199,000

b. Acid-test ratio:

2014:

$60,500 + $26,500 + $115,500

=

0.75

$270,000

2013:

$45,000 + $0 + $108,230

=

0.77

$199,000

c. Debt ratio:

2014:

$301,320*

=

0.54

2013:

$229,360**

=

0.47

$558,000

$488,000

2014:

$168,295

=

3.47 times

2013:

$159,580

=

4.04 times

2014:

$25,368

=

2013:

$18,291

=

2014:

2013:

2014:

2013:

2014:

2013:

Chapter 14 Financial Statement Analysis

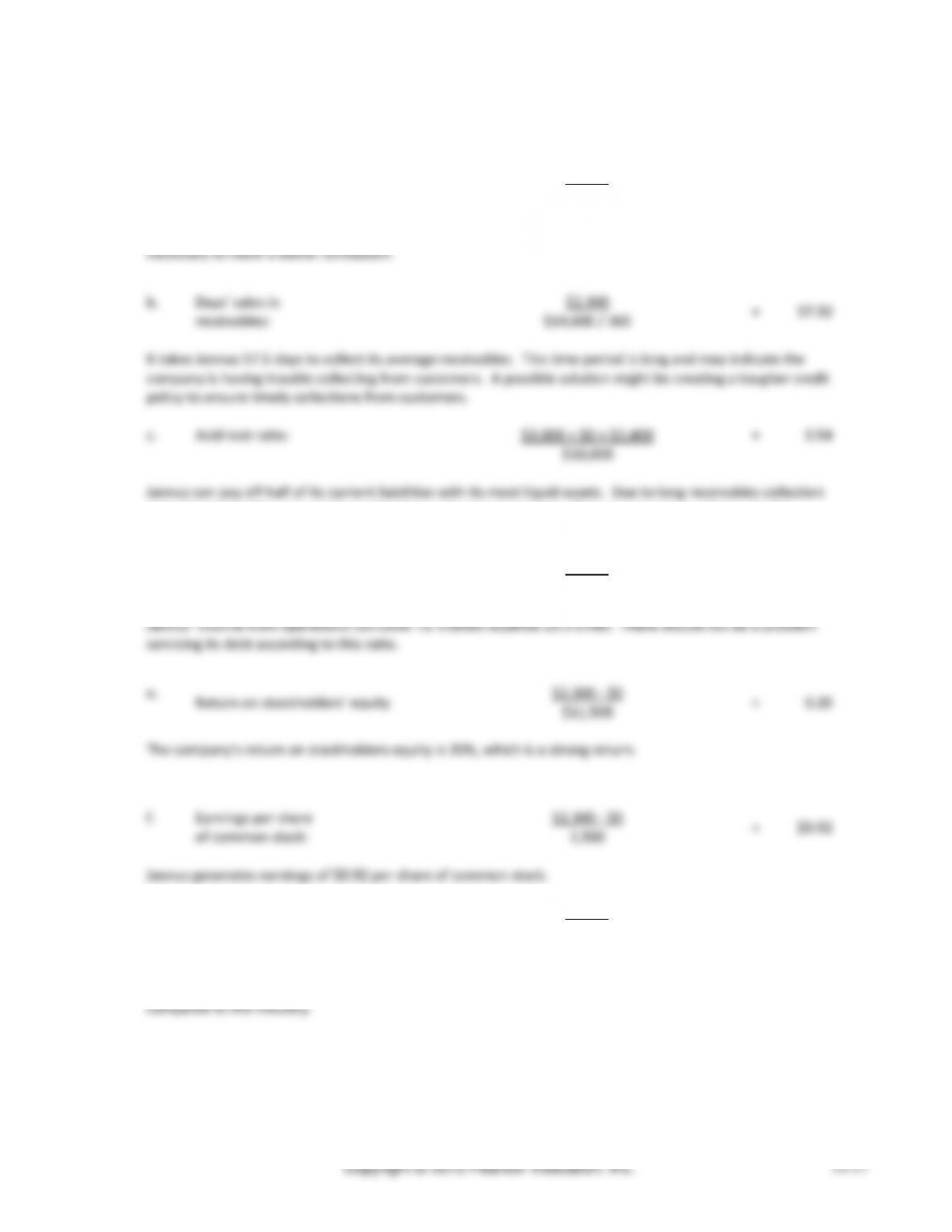

(20-30 min.) E14-31B

a.

Inventory turnover:

$5,400

=

3.0

$1,800

Jannus sells its inventory 3 times per year. This seems low. A comparison to industry standards would be

necessary to reach a better conclusion.

b.

Days’ sales in

receivables:

$2,300

=

57.50

$14,600 / 365

It takes Jannus 57.5 days to collect its average receivables. This time period is long and may indicate the

company is having trouble collecting from customers. A possible solution might be creating a tougher credit

policy to ensure timely collections from customers.

c.

Acid-test ratio:

$3,000 + $0 + $2,400

=

0.54

$10,000

Jannus can pay off half of its current liabilities with its most liquid assets. Due to long receivables collection

time, the receivables may not be as liquid as cash and equivalents. This may be a cause of concern for

management.

d.

Times-interest-earned

$4,700

=

23.5

$200

Jannus’ income from operations can cover its interest expense 23.5 times. There should not be a problem

servicing its debt according to this ratio.

e.

Return on stockholders’ equity

$2,300 – $0

$11,500

=

0.20

The company’s return on stockholders equity is 20%, which is a strong return.

f.

Earnings per share

of common stock:

$2,300 – $0

=

$0.92

2,500

Jannus generates earnings of $0.92 per share of common stock.

g.

Price/earnings ratio:

$34.50

=

37.5

$0.92

According to this ratio, the market price of one share of stock is 37.5 times the earnings per one share of

stock. A comparison to industry standards is needed to determine if this stock is overpriced or underpriced

compared to the industry.