Chapter 13 Statement of Cash Flows

Chapter 13

Statement of Cash Flows

Quick Check

Answers:

QC-1. c

QC-3. c

QC-5. a

QC-7. d

QC-9. a

QC-2. c

QC-4. b

QC-6. b

QC-8. c

QC-10. b

Short Exercises

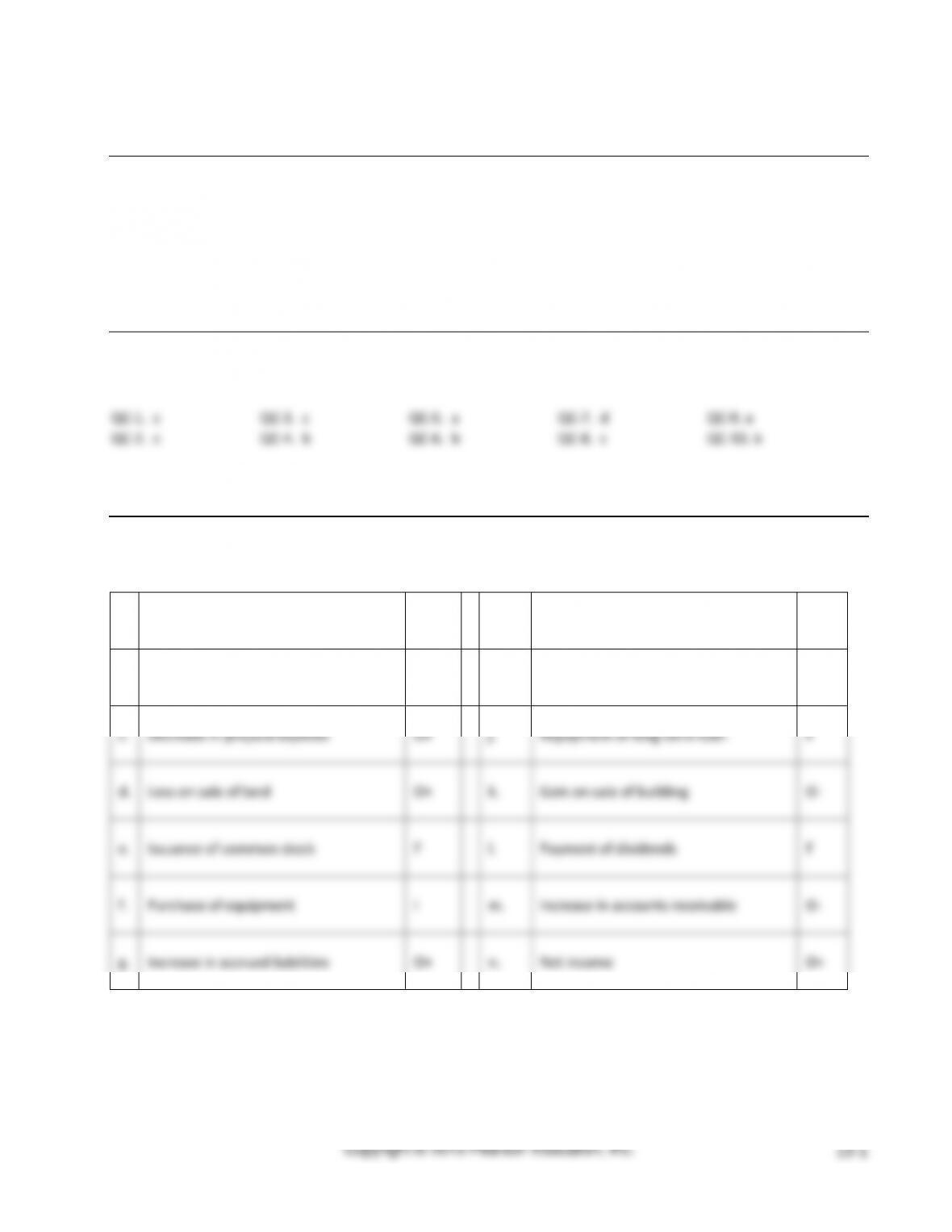

(5-10 min.) S13-1

a.

Amortization expense

O+

h.

Increase in inventory

O-

b.

Retained earnings

NA

i.

Increase in accounts payable

O+

c.

Decrease in prepaid expense

O+

j.

Repayment of long-term loan

F

d.

Loss on sale of land

O+

k.

Gain on sale of building

O-

e.

Issuance of common stock

F

l.

Payment of dividends

F

f.

Purchase of equipment

I

m.

Increase in accounts receivable

O-

g.

Increase in accrued liabilities

O+

n.

Net income

O+

Copyright © 2015 Pearson Education, Inc.

13-6

Beginning cash balance

158,000

Net increase (decrease) in cash for the year (Req. 4)

243,100

Ending cash balance

$401,100

(5-10 min.) S13-9

Account Title

Behavior during year

Accounts receivable

Decreased

Inventory

Increased

Other current assets

Decreased

Accounts payable

Decreased

Other current liabilities

Increased

(10-15 min.) S13-10

Req. 1

Cash flows from operating activities:

Received from customers

$ 50,000

Paid for interest

(4,300)

Paid for utilities

(17,000)

Paid for taxes

(5,500)

Paid to employees

(13,000)

Paid to suppliers

(39,000)

Paid for insurance

(9,200)

Paid for advertising

(7,400)

Net cash provided (used)by operating activities

$ (45,400)

Req. 2

Cash flows from investing activities:

Paid for equipment

$(14,000)

Received from sale of land

15,000

Received from sale of plant assets

6,900

Net cash provided (used) by investing activities

$ 7,900

Req. 3

Cash flow from financing activities:

Paid dividends

$(7,400)

Received from issuing long-term note payable

29,000

Net cash provided (used) byfinancing activities

$21,600

Net cash provided (used) by operating activities (Req. 1)

(45,400)

Net cash provided (used) by investing activities (Req. 2)

7,900

Net cash provided (used) by financing activities (Req. 3)

21,600

Net increase (decrease) in cash for the year

$(15,900)

Req. 5

Beginning cash balance

349,000

Net increase (decrease) in cash for the year (Req. 4)

(15,900)

Ending cash balance

$333,100

(5 – 10 min.) S13-11

1.

Patsy is an accountant at Highland Restaurant Group,

Inc. She has helped to prepare the financial statements.

She knows that the internal controls over cash are

weak, but she does not speak up because she feels that

it is not her job.

Credibility – Disclose delays or deficiencies in

information, timeliness, processing, or internal

controls in conformance with organization

policy and/or applicable law.

2.

Teri uses the indirect method to prepare the statement

of cash flows even though her company has adopted

International Financial Reporting Standards. She is

unfamilar with the steps required to produce a

statement using the direct method.

Competence – Perform professional duties in

accordance with relevant laws, regulations, and

technical standards.

3.

Lamar is an accountant at Boise & Hall, Inc. Lamar

confides to a close friend that he is concerned about

the future of Boise & Hall. Lamar explains that

operating cash flows are negative; this information is

on the not-yet-released financial statements.

Confidentiality – Keep information confidential

except when disclosure is authorized or legally

required.

4.

The statement of cash flows has never been Julius’

strength; he struggled with it in school. This year, Julius

cannot get the statement of cash flows to balance so he

decides to hide the amount that the statement is off by

adding that difference to one of the items in the

operating section.

Competence – Perform professional duties in

accordance with relevant laws, regulations, and

technical standards.

5.

Darryl does not disclose to upper management that his

sister is a partner in the accounting firm that the

company is hiring for the audit.

Integrity – Mitigate actual conflicts of interest,

regularly communicate with business associates

to avoid apparent conflicts of interest. Advise all

parties of any potential conflicts.

Managerial Accounting 4e Solutions Manual

Exercises (Group A)

(5-10 min.) E13-12A

Mosaic Travel Services, Inc.

Statement of Cash Flows – Indirect Method (Operating Activities)

For year ended December 31, 2014

Cash flows from operating activities:

Net Income

$33,000

Adjustments to reconcile net income to cash basis:

Loss on sale of land

$ 3,400

Depreciation expense

7,000

Decrease in accounts receivable

1,000

Increase in inventory

(40,000)

Decrease in prepaid insurance

3,000

Decrease in accounts payable

(9,000)

Increase in wages payable

2,000

Increase in interest payable

1,000

Increase in income tax payable

3,000

Total reconciling adjustments

(28,600)

Net cashprovided (used) by operating activities

$4,400

Copyright © 2015 Pearson Education, Inc.

13–16

(15-20 min.) E13-22B

Dream Big Travel Services, Inc.

Statement of Cash Flows – Indirect Method

For year ended December 31, 2014

Cash flows from operating activities:

Net Income

$37,000

Adjustments to reconcile net income to cash basis:

Loss on sale of land

$ 3,900

Depreciation expense

5,000

Decrease in accounts receivable

5,000

Increase in inventory

(35,000)

Decrease in prepaid insurance

2,000

Decrease in accounts payable

(3,000)

Increase in wages payable

11,000

Increase in interest payable

2,000

Increase in income taxes payable

3,000

Total reconciling adjustments

(6,100)

Net cash provided (used) by operating activities

$30,900

(10-15 min.) E13-23B

Dream Big Travel Services, Inc.

Statement of Cash Flows – Indirect Method

For year ended December 31, 2014

Cash flows from operating activities:

Net Income

$37,000

Adjustments to reconcile net income to cash basis:

Loss on sale of land

$ 3,900

Depreciation expense

5,000

Decrease in accounts receivable

5,000

Increase in inventory

(35,000)

Decrease in prepaid insurance

2,000

Decrease in accounts payable

(3,000)

Increase in wages payable

11,000

Increase in interest payable

2,000

Increase in income taxes payable

3,000

Total reconciling adjustments

(6,100)

Net cash provided (used) by operating activities

30,900

Cash flows from investing activities:

Proceeds from sale of land

8,100

Purchase of equipment

(20,000)

Net cash flows provided (used) by investing activities

(11,900)

Copyright © 2015 Pearson Education, Inc.

13–17

Cash flows from financing activities:

Long term notes issued

5,000

Dividends paid

(7,000)

Issuance of stock for cash

7,000

Net cash provided (used) by financing activities

5,000

Net increase (decrease) in cash

24,000

Cash, beginning of year

18,000

Cash, end of year

$42,000

(10-15 min.) E13-24B

Req. 1

Cash dividends paid during the year total $22,000.

(5-10 min.) E13-25B

Eduardo Corporation

Statement of Cash Flows – Indirect Method (Operating Activities)

For year ended December 31

Cash flows from operating activities:

Net Income

$42,000

Adjustments to reconcile net income to cash basis:

Depreciation expense

$ 18,000

Increase in current assets other than cash

(5,000)

Decrease in current liabilities

(7,000)

Total reconciling adjustments

6,000

Net cash provided (used) by operating activities

$48,000