Chapter 12 Capital Investment Decisions and the Time Value of Money

(continued) P12-56A

(Req. 1 continued)

Managerial Accounting 4e Solutions Manual

(continued) P12-57A

Accounting

rate of return

=

Average annual operating income from asset

Initial investment

Average annual net

cash inflow from asset − Annual depreciation expense on asset

Initial investment

Plan A

=

$1,600,000 − $937,778a

$8,440,000

=

$662,222

$8,440,000

=

7.8%

Plan B

=

$1,250,000 − $793,333b

$8,240,000

=

$456,667

$8,240,000

=

5.5%

__________

a Annual depreciation = $8,440,000 / 9 = $937,778

b Annual depreciation = ($8,240,000 − $1,100,000) / 9 = $793,333

PV factor at

i = 10%, n = 9

Net Cash Inflow

Total Present Value

Plan A:

Present value of annuity of

equal annual net cash

inflows for 9 years at 10%

5.759 c × $1,600,000 per year

$ 9,214,400

Less: Initial Investment

(8,440,000)

Net present value of Plan A

$ 774,400

Plan B:

Present value of annuity of

equal annual net cash

inflows for 9 years at 10%

5.759c × $1,250,000 per year

$ 7,198,750

Present value of residual value (lump sum, not

annuity)

0.424 d × $1,100,000

466,400

Less: Initial investment

(8,240,000)

Net present value of Plan B

$ (574,850)

c Present Value of Annuity of $1 (n = 9, i = 10%)

d Present Value of $1 (n = 9, i = 10%)

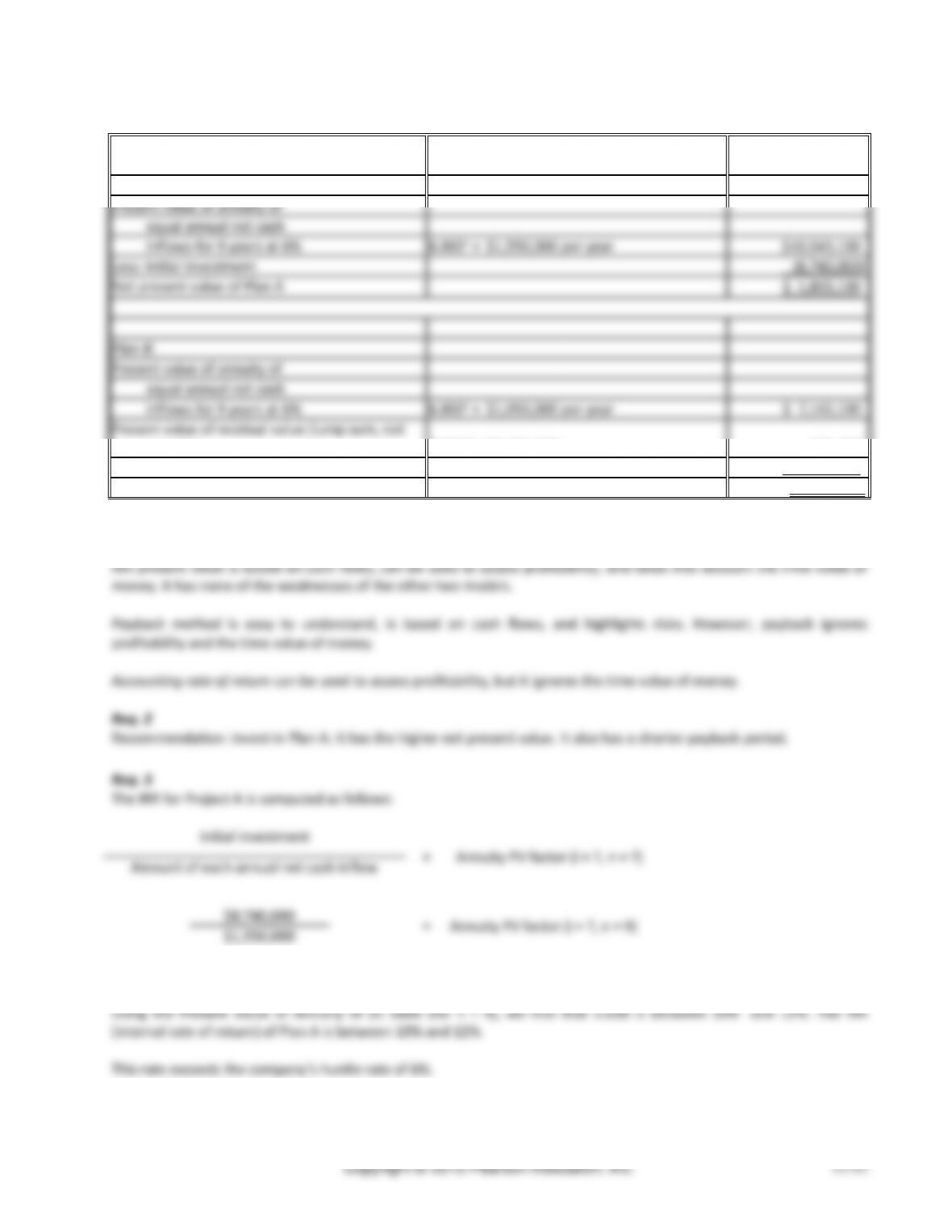

Net present value is based on cash flows, can be used to assess profitability, and takes into account the time value of

money. It has none of the weaknesses of the other two models.

Chapter 12 Capital Investment Decisions and the Time Value of Money

(continued) P12-57A

Payback method is easy to understand, is based on cash flows, and highlights risks. However, payback ignores

profitability and the time value of money.

Managerial Accounting 4e Solutions Manual

Problems (Group B)

(30-45 min.) P12-58B

Scenario #1:

Future value

=

$ 55,000 × (FV factor, i = 12%, n = 15)

=

$ 55,000 × 5.474

=

$301,070

Scenario #2:

Present value

=

$4,000,000 × (PV factor, i = 14%, n = 40)

=

$4,000,000 × 0.005

=

$ 20,000

Scenario #3:

Present value

=

Annuity × (Annuity PV factor, i = 8%, n = 20)

$2,000,000

=

Annuity × 9.818

$203,707

=

Annuity (rounded)

Chapter 12 Capital Investment Decisions and the Time Value of Money

(continued) P12-58B

Scenario #4:

Future value

=

$ 4,500 × (Annuity FV factor, i = 10%, n = 7)

=

$ 4,500 × 9.487

=

$42,692 (rounded)

Scenario #5:

Present value

=

$9,000 × (Annuity PV factor, i = 10%, n = 9)

=

$9,000 × 5.759

=

$51,831

=

$302,000 × 0.926 =

=

$208,000 × 0.857 =

=

$98,000 × 0.794 =

Total Present value

Less: Initial Investment

Net Present Value (NPV)

=

$302,000 × 0.909 =

$ 274,518

=

$208,000 × 0.826 =

=

$98,000 × 0.751 =

Total Present value

Less: Initial investment

Net Present Value (NPV)

Managerial Accounting 4e Solutions Manual

(15-20 min.) P12-59B

Retirement planning involves two separate annuities:

1) the annual cash savings (from age 20 to age 40) and

2) the annual withdrawals (from age 40 to age 85).

To find the amount of annual savings needed, we perform a two– step process:

First, we discount the retirement withdrawals back to their present value (at age 40).

Second, we set that amount equal to the future value of the savings annuity.

Req. 1

Present Value

=

Annual cash withdrawals × (Annuity PV factor, i = 10=4%, n = 45)

=

$ 220,000 × (7.123)

=

$1,567,060

By age 40, you need to have accumulated a sum of $1,567,060.

Amount of annual cash savings × (91.023)

Amount of annual cash savings

AT AGE 40:

PV of future

retirement

withdrawals =

FV of the

annual savings

installments

Annual savings installments

Annual retirement

withdrawals

45 years

20 years

(20-30 min.) P12-60B

Req. 1

Payback

=

Initial Investment

period

Expected annual net cash inflow

=

$1,850,000

$495,000

=

3.7 years

Accounting

=

Average annual operating income from asset

rate of return

Initial investment

Average annual net

cash inflow from asset

−

Annual depreciation

expense on asset

Initial investment

=

$495,000 − $205,556a

$1,850,000

=

$289,444

$1,850,000

=

15.6% (rounded)

__________

aAnnual depreciation

=

$1,850,000

=

$205,556

9

Annuity PV factor at i

= 10%, n= 9

Net Cash Inflow

Total Present Value

Net present value:

Present value of annuity of

equal annual net cash

inflows for 9 years at 10%

5.759 $495,000 per year =

$ 2,850,705

Less: Initial Investment

(1,850,000)

Net present value

$ 1,000,705

Managerial Accounting 4e Solutions Manual

(30-45 min.) P12-61B

Req. 1

Payback period

=

Initial investment

Expected annual net cash inflow

Plan A

=

$8,740,000

$1,550,000

=

5.6 years

Plan B

=

$8,140,000

$1,050,000

=

7.8 years

Accounting

rate of return

=

Average annual operating income from asset

Initial investment

Average annual net

cash inflow from asset − Annual depreciation expense on asset

Initial investment

Plan A

=

$1,550,000 − $971,111

$8,740,000

=

$578,889

$8,740,000

=

6.6 %

Plan B

=

$1,050,000 − $785,000

$8,140,000

=

$265,000

$8,140,000

=

3.3%

Chapter 12 Capital Investment Decisions and the Time Value of Money

(continued) P12-61B

PV factor at

i = 6%, n = 9

Net Cash Inflow

Total Present Value

Plan A:

Present value of annuity of

equal annual net cash

inflows for 9 years at 6%

6.802c × $1,550,000 per year

$10,543,100

Less: Initial investment

(8,740,000)

Net present value of Plan A

$ 1,803,100

Plan B:

Present value of annuity of

equal annual net cash

inflows for 9 years at 6%

6.802c × $1,050,000 per year

$ 7,142,100

Present value of residual value (lump sum, not

annuity)

0.592 d × $1,075,000

636,400

Less: Initial investment

(8,140,000)

Net present value of Plan B

$ (361,500)

c Present Value of Annuity of $1 (n = 9, i = 6%)

d Present Value of $1 (n = 9, i = 6%)

Annuity PV factor (i = ?, n = 9)

Managerial Accounting 4e Solutions Manual

Discussion & Analysis

A12-62

1. Describe the capital budgeting process in your own words.

2. Define capital investment. List at least three examples of capital investments other than the examples provided

3. “As the required rate of return increases, the net present value of a project also increases.” Explain why you

agree or disagree with this statement.

4. Summarize the net present value method for evaluating a capital investment opportunity. Describe the

circumstances that create a positive net present value. Describe the circumstances that may cause the net

present value of a project to be negative. Describe the advantages and disadvantages of the net present value

method.

5. Net cash inflows and net cash outflows are used in the net present value method and in the internal rate of

return method. Explain why accounting net income is not used instead of cash flows.

6. Suppose you are a manager and you have three potential capital investment projects from which to choose.

Funds are limited, so you can only choose one of the three projects. Describe at least three methods you can

7. The net present value method assumes that future cash inflows are immediately reinvested at the required rate

of return, while the internal rate of return method assumes that future cash inflows are immediately invested at

8. The decision rule for NPV analysis states that the project with the highest NPV should be selected. Describe at

least two situations when the project with the highest NPV may not necessarily be the best project to select.

9. List and describe the advantages and disadvantages of the internal rate of return method.

10. List and describe the advantages and disadvantages of the payback method.

11. Oftentimes, investments in sustainability projects do not meet traditional investment selection criteria. Suppose

you are a manager and have prepared a proposal to install solar panels to provide lighting for the office. The

12. Think of a company with which you are familiar. What are some examples of possible sustainable investments

Managerial Accounting 4e Solutions Manual

Application & Analysis

1. Research the cost of each model (includes taxes and title costs). Also, obtain an estimate of the miles per gallon

fuel efficiency of each model.

7. What qualitative factors might affect your decision about which model to purchase?

record.

A12-64

1.

a. The ethical issues in this situation are:

Competence: “Provide decision support information and recommendations that are accurate, clear, concise,

2. Instead of simply accepting or rejecting the proposal, Peter could consult upper management to discuss the

A12-65

1. Apple made its announcement in 2012 to beat these other large technology companies to the punch. Apple

2. Americans like things that are made in America. There is also a possibility that the products will be of better quality

than if they were made in China.

4. The stakeholders that are impacted are: the former (Chinese) employees who would have been manufacturing the

5. Potentially, if the company is not producing at its greatest margin, it could become the victim of a takeover

attempt. It also hurts the employees who work for lower wages so that they could keep their jobs.