(5-10 min.) E12-36B

Payback period

=

Initial Investment

Expected annual net cash inflow

=

$1,600,000

$320,000

=

5 years

The payback occurs well before the plant must be replaced, so the payback method supports purchasing the plant.

(5-10 min.) E12-37B

Full years

+

Amount to complete

recovery in next year

/

Projected net cash

inflow in next

year

=

Payback

5

+

( $135,000

/

$230,000 )

=

5.59 years

(10-15 min.) E12-38B

Accounting rate of return

=

Average annual operating

income from asset

Initial Investment

ARR

=

$101,500

$1,450,000

ARR

=

7.00%

Managerial Accounting 4e Solutions Manual

(10-15 min.) E12-39B

Accounting rate of return

=

Average annual operating

income from asset

Initial Investment

Accounting rate of return on Atlas

=

$170,500

$1,100,000

=

15.5%

Accounting rate of return on Kyler

=

$247,500

$1,375,000

=

18.0%

(15-20 min.) E12-40B

Req. 1

Your “out–of–pocket” cost is $127,500 either way: ($5,100 × 25 years) vs. ($10,625 × 12 years).

Req. 2

Future Value

=

Annuity × (Annuity FV factor, i = 12%, n = 25)

=

$5,100 × (133.334)

=

$680,003 (rounded)

Future Value

=

Annuity × (Annuity FV factor, i = 12%, n = 12)

=

$10,625 × (24.133)

=

$256,413 (rounded)

=

$680,003 × (2.476)

=

$1,683,687

Future Value

=

$256,413 × (FV factor, i = 12%, n = 8)

=

$256,413 × (2.476)

=

$634,879

(15-20 min.) E12-41B

Req. 1

Payback = 15 years ($600,000/40,000)

(5-10 min.) E12-42B

Req. 1

With the 8% interest rate, Laurel needs:

Present Value

=

Annuity × (Annuity PV factor, n = 4, i = 8%)

=

$27,000 × (3.312)

=

$89,424

=

$27,000 × (3.465)

=

$93,555

Present Value

$15,000,000 × (PV factor, i = 10%, n = 4)

$15,000,000 × 0.683

$10,245,000

Present Value

$2,200,000 × (Annuity PV factor, i = 10%, n = 5)

$2,200,000 × 3.791

$8,340,200

Present Value

$11,000,000 × (PV factor, i = 10%, n = 3)

$11,000,000 × 0.751

$8,261,000

Managerial Accounting 4e Solutions Manual

(10-15 min.) E12-44B

Scenario #1:

Future value

=

$3,500 × (FV factor, i = 10%, n = 6)

=

$3,500 × 1.772

=

$6,202

Scenario #2:

Present value

=

$ 4,000 × (Annuity PV factor, i = 8%, n = 20)

=

$ 4,000 × 9.818

=

$39,272

Scenario #3:

Present value

=

$145,000 × (PV factor, i = 6%, n = 7)

=

$145,000 × 0.665

=

$ 96,425

Scenario #4:

Future value

=

$4,000 × (Annuity FV factor, i = 14%, n = 10)

=

$4,000 × 19.337

=

$77,348

Scenario #5:

Future value

=

$ annuity × (Annuity FV factor, i = 6%, n = 4)

$51,000

=

$ annuity × 4.375

$11,657

=

$ annuity

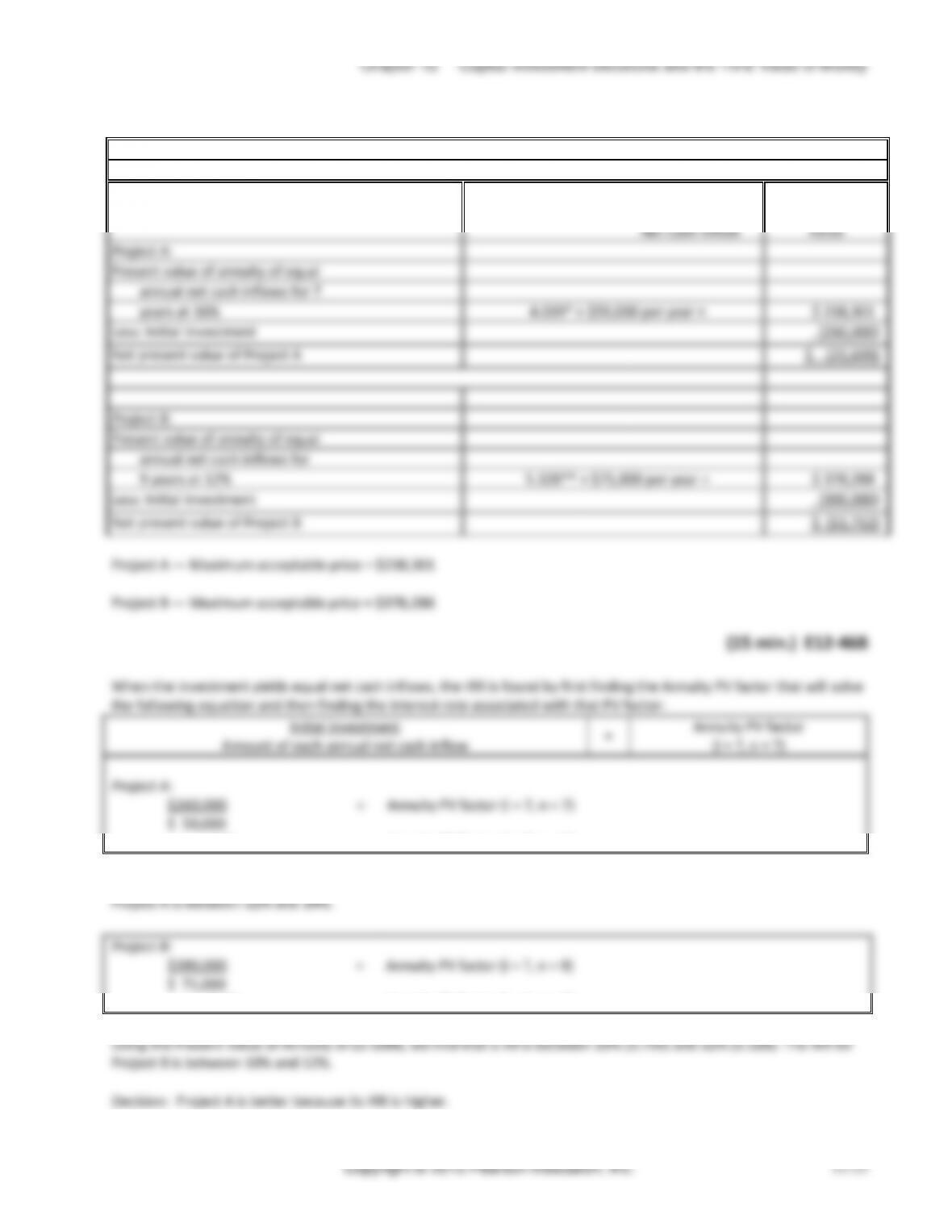

(15-20 min.) E12-45B

Smith Products

Net Present Value Analysis

Annuity PV Factors

at I = 16%; 12%

Net Cash Inflow

Total Present

Value

Project A:

Present value of annuity of equal

annual net cash inflows for 7

years at 16%

4.039* × $59,000 per year =

$ 238,301

Less: Initial Investment

(260,000)

Net present value of Project A

$ (21,699)

Project B:

Present value of annuity of equal

annual net cash inflows for

9 years at 12%

5.328** × $71,000 per year =

$ 378,288

Less: Initial investment

(390,000)

Net present value of Project B

$ (11,712)

Managerial Accounting 4e Solutions Manual

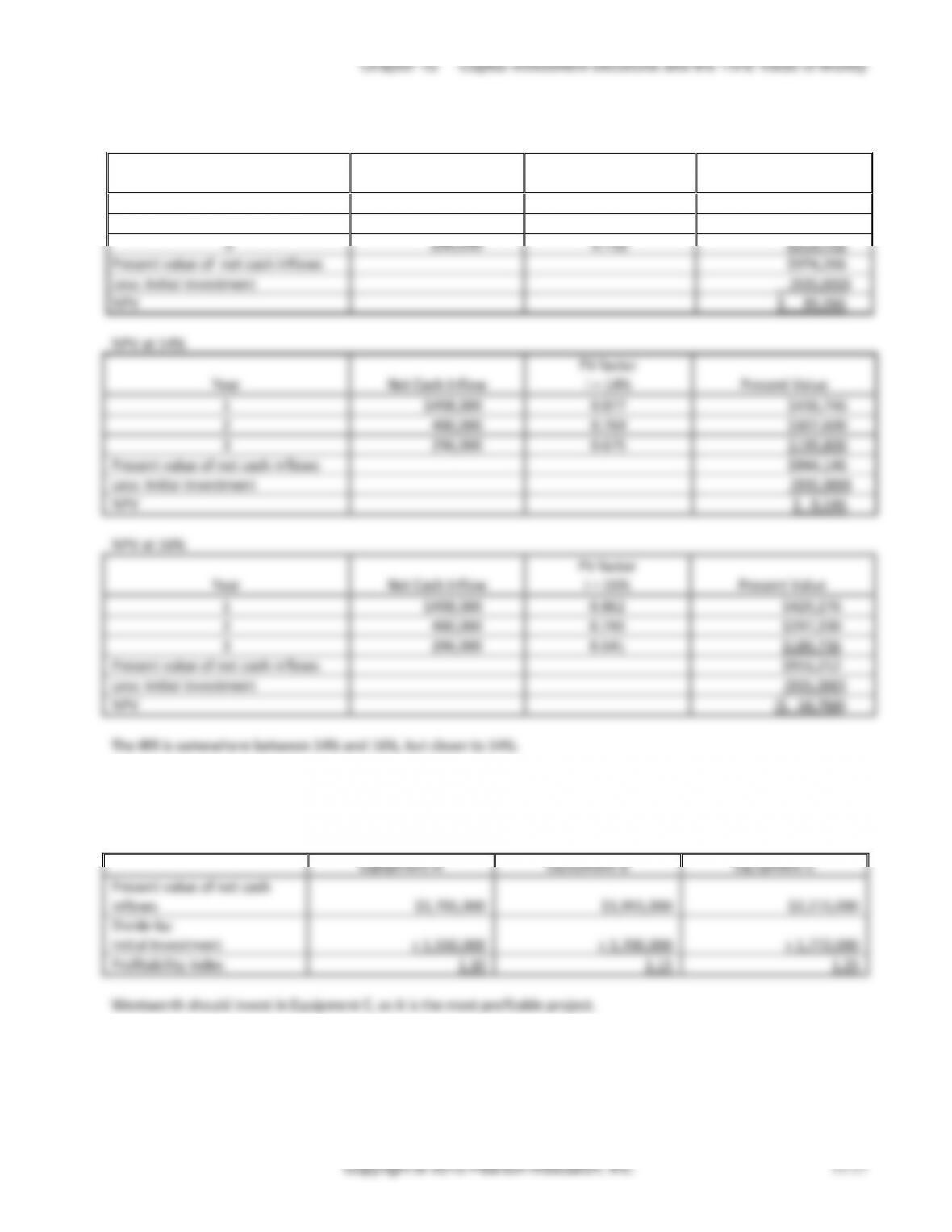

(15-20 min.) E12-47B

Req. 1

The equipment’s net present value (NPV) is calculated as follows. Since each annual cash inflow is unique, we cannot

use the annuity table. We must discount each annual cash inflow using the PV Factors found in the Present Value of $1

table:

Year

Net cash inflow

PV of $1 factor

(i =16%)

Present Value of Net

Cash inflow

Year 1 (n = 1)

$264,000

0.862

$227,568

Year 2 (n = 2)

$253,000

0.743

$187,979

Year 3 (n = 3)

$224,000

0.641

$143,584

Year 4 (n = 4)

$213,000

0.552

$117,576

Year 5 (n = 5)

$204,000

0.476

$97,104

Year 6 (n = 6)

$177,000

0.410

$72,570

Present value of net cash inflows

$846,381

Less: Initial Investment

($915,000)

Net present value

($68,619)

Alderman Industries should not invest in the equipment because its NPV is negative.

Req. 2

Alderman must determine whether the equipment investment becomes favorable (positive NPV) if the equipment is

refurbished, used for one more year, and then sold. The following analysis needs to be added to the NPV computations

above:

Year

Cash (outflow) /

inflow

PV of $1 factor

(i = 16%)

Present Value

Refurbishment at the end of Year 6 (n = 6)

($104,000)

0.410

($42,640)

Cash inflows in Year 7 (n = 7)

$ 76,000

0.354

26,904

Residual value (n=7)

$ 55,000

0.354

19,470

Additional NPV provided from

refurbishment

$ 3,734

NPV from part 1

($68,619)

New NPV

($64,885)

The refurbishment provides a positive NPV. The refurbishment NPV is not large enough to overcome the original NPV

of the equipment ($68,619). Therefore, the refurbishment should not alter Alderman Industries’ original decision to

turn down the equipment investment.

(15-20 min.) E12-48B

NPV at 12%

Year

Net Cash Inflow

PV factor

i = 12%

Present Value

1

$498,000

0.893

$444,714

2

400,000

0.797

$318,800

3

296,000

0.712

$210,752

Present value of net cash inflows

$974,266

Less: Initial investment

(935,000)

NPV

$ 39,266

Net Cash Inflow

400,000

296,000

Net Cash Inflow

$429,276

400,000

$297,200

296,000

$189,736

$916,212

(935,000)

$1,705,000

$1,955,000

$2,215,000

Managerial Accounting 4e Solutions Manual

(10-15 min.) E12-50B

Req. 1

Avg. net cash inflow per

day

x

Number of ski days per year

=

Avg. annual net cash

inflow

$12,120

x

163

=

$1,975,560

Req. 2

Avg. annual net cash inflow

–

Annual depreciation expense

=

Avg. annual operating income

from asset

$1,975,560

–

$810,000

=

$1,165,560

Req. 3

Initial Investment

/

Expected annual net cash inflow

=

Payback period

$9,000,000

/

$1,975,560

=

4.56 years

Req. 4

Avg. annual operating income

from asset

/

Initial investment

=

Accounting

rate of return

$1,165,560

/

$9,000,000

=

12.95%

(5-10 min.) E12-51B

Req. 1

The payback period of 4.56 years will not change since the method does not consider any cash flows that occur after

=

Payback period

=

Chapter 12 Capital Investment Decisions and the Time Value of Money

(continued) E12-51B

Req. 2

The ARR will change if the asset has no residual value. The average annual operating income will be lower since there

$9,000,000

(10-15 min.) E12-52B

Req. 1

PV factor at

12%

Net Cash Inflow

Total Present Value

Present value of annuity of equal

annual net cash inflows for 10

years at 12%

5.650 × $1,975,560a

$11,161,914

Present value of residual value*

0.322 b × $900,000

289,800

Total present value

$11,451,714

Less: Initial investment

(9,000,000)

Net present value of expansion

$ 2,451,714

a From E12-51B

b The residual value is a single lump sum (not an annuity) that will occur at the end of the investment’s useful life. The

Present Value of $1 table is used to find the correct PV factor for i = 12%, n = 10.

The expansion is an attractive project because its NPV is positive.

Req. 2

Annuity PV

factor at i =

12%, n = 10

Net Cash Inflow

Total Present Value

Present value of annuity of equal

annual net cash inflows for 10

years at 12%

5.650 × $1,975,560a

$11,161,914

Less: Initial investment

(9,000,000)

Net present value of expansion

$ 2,161,914

__________

a From E12-51B

Without a residual value, the expansion is still attractive because of the project’s positive NPV.

Managerial Accounting 4e Solutions Manual

(20 min.) E12-53B

Req. 1

(a)

Net Present

Value

(b)

Profitability Index

(c)

Internal Rate of

Return

(d)

Payback

Period

(e)

Accounting

Rate of Return

1st preferred

C

A

B

C

D

2nd preferred

D

C

A

A

A

3rd preferred

A

B

C

D

B

4th preferred

B

D

D

B

C

Req. 2

Net Present Value (NPV) – This method indicates profitability by comparing the present value of the investment’s net

cash inflows with the cost of the investment (already stated at its present value). This method is superior because it

incorporates the time value of money.

Profitability index – This method helps to compare the NPV across alternative investments of varying sizes.

Internal rate of return (IRR) – This method also indicates profitability and incorporates the time value of money. This

method will show us the actual rate of return being earned on the investment by equating the present value of the net

cash inflows to the investment’s cost. In other words, it is the interest rate, which brings the investment’s NPV to zero.

Payback Period – This method will show the company how quickly it recoups its initial investment. This method will be

good for screening out those potential investments that are too risky because the payback period is too long. However,

the payback period will not be the sole criterion for accepting capital investments since it does not give the company

any insight about the investment’s profitability. Additionally, it does not incorporate the time value of money.

Accounting rate of return (ARR) – This method will give the company an indication of how profitable the investment

will be. However, since it does not consider the time value of money, it is not the best indicator of profitability. This

method is the only method that uses accrual accounting figures. Therefore it will help the company assess the impact

of investments on the financial statements. The other methods use net cash flows.

Present value

=

Annuity × (Annuity PV factor, i = 10%, n = 20)

$2,000,000

=

Annuity × 8.514

$234,907

=

Annuity

Future value

=

$ 3,000 × (Annuity FV factor, i = 14%, n = 8)

=

$ 3,000 × 13.233

=

$39,699

Scenario #5:

Present value

=

$15,000 × (Annuity PV factor, i = 12%, n = 10)

=

$15,000 × 5.650

=

$84,750

=

$300,000 × 0.926 =

=

$206,000 × 0.857 =

=

$100,000 × 0.794 =

Total Present value

Less: Initial Investment

Net Present Value (NPV)

(30-45 min.) P12-54A

Scenario #1:

Future value

=

$ 35,000 × (FV factor, i = 10%, n = 15)

=

$ 35,000 × 4.177

=

$146,195

Scenario #2:

Present value

=

$3,500,000 × (PV factor, i = 12%, n = 30)

=

$3,500,000 × 0.033

=

$ 115,500

Managerial Accounting 4e Solutions Manual

(continued) P12-54A

Scenario #7:

The IRR is the interest rate at which the investment’s NPV = 0. Since the NPV was positive at 8% (in Scenario 6), we’ll

Chapter 12 Capital Investment Decisions and the Time Value of Money

(continued) P12-55A

Req. 1

Present Value

=

Annual cash withdrawals × (Annuity PV factor, i = 12%, n = 40)

=

$ 250,000 × (8.244)

=

$2,061,000

Amount of annual cash savings × (Annuity FV factor, i =12%, n = 15)

Amount of annual cash savings × (37.280)

$55,284

Amount of annual cash savings

Managerial Accounting 4e Solutions Manual

(20-30 min.) P12-56A

Req. 1

Payback

=

Initial investment

period

Expected annual net cash inflow

=

$2,000,000

$520,000

=

3.8 years

Accounting

=

Average annual operating income from asset

rate of return

Initial investment

Average annual net

cash inflow from asset

−

Annual depreciation

expense on asset

Initial investment

=

$520,000 − $200,000

$2,000,000

=

$320,000

$2,000,000

=

16%