Chapter 11 Standard Costs and Variances

Problems (Group B)

DM

2.0 yards

X

$8.5 per yard

$17

Req. 2

$35,802 / 4,590 = $7.80 per yard

Req. 3

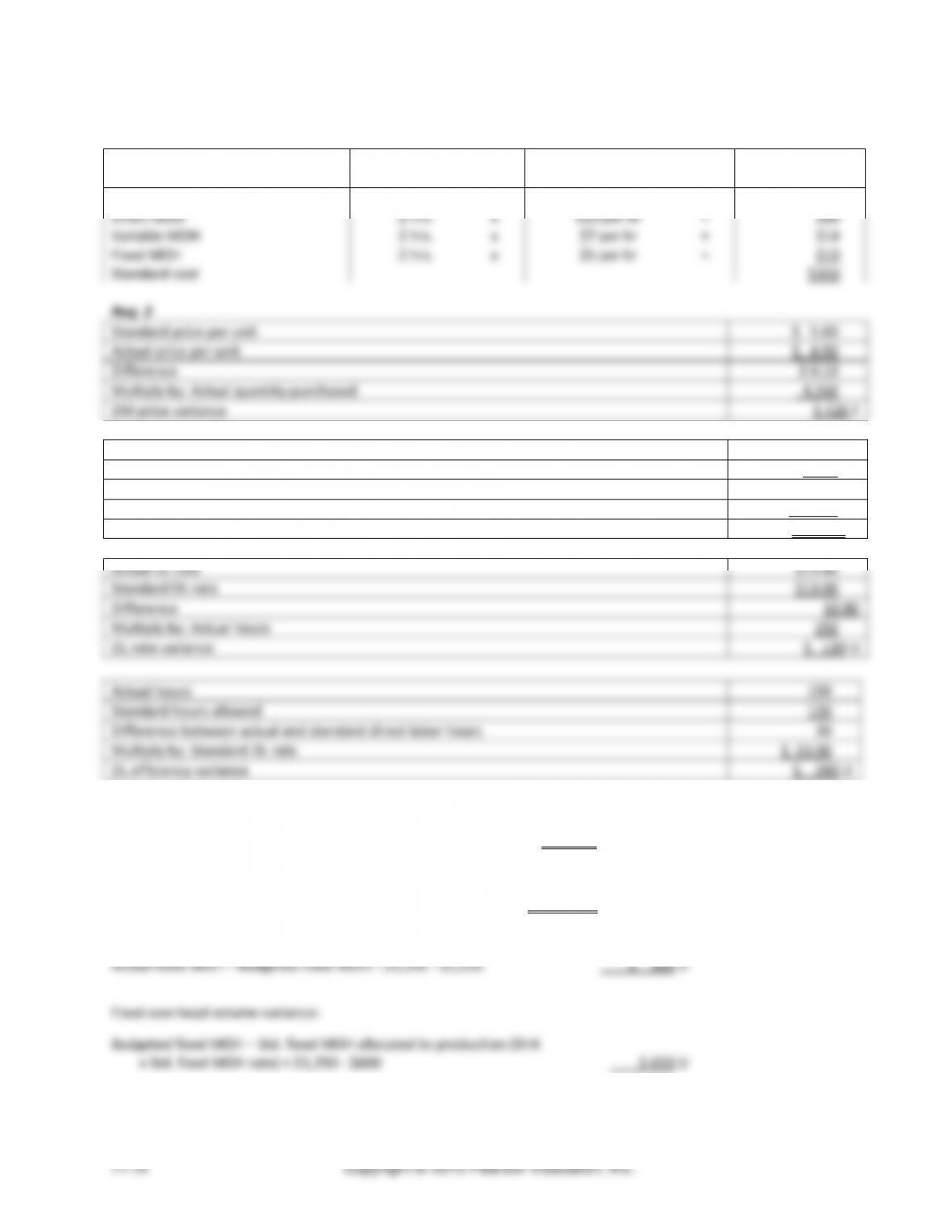

Standard price per unit

$ 8.50

Actual price per unit

$ 7.80

Difference

$ 0.70

Multiply by: Actual quantity purchased

4,590

Direct Material price variance

$ 3,213 F

Actual quantity used

3,990

Standard quantity allowed

3,400

Difference

590

Multiply by: Standard price

$ 8.50

Direct Materials quantity variance

$ 5,015 U

Req. 4

DL

1.5 yards

X

$12 per yard

$18

Req. 5

$29,904 / 2,670 = $11.20 per yard

Req. 6

Actual rate

$11.20

Standard rate

$12.00

Difference

$0.80

Multiply by: Actual direct labor hours

2,670

DL rate variance

$ 2,136 F

Actual hours

2,670

Standard hours allowed

2,550

Difference

120

Multiply by: Standard rate

$12.00

DL efficiency variance

$ 1,440 U

Managerial Accounting 4e Solutions Manual

(continued) P11-53B

Req. 7

The favorable DM price variance and unfavorable DM quantity variance may have been caused by purchasing inferior

(15-30 min.) P11-54B

Req. 1

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Direct materials

19 yards

x

$13 per yard

=

$247

Direct labor

4 hrs.

x

$11 per hr

=

$44

Variable MOH

4 hrs.

x

$5 per hr

=

$20

Fixed MOH

4 hrs.

x

$10 per hr

=

$40

Standard cost

$351

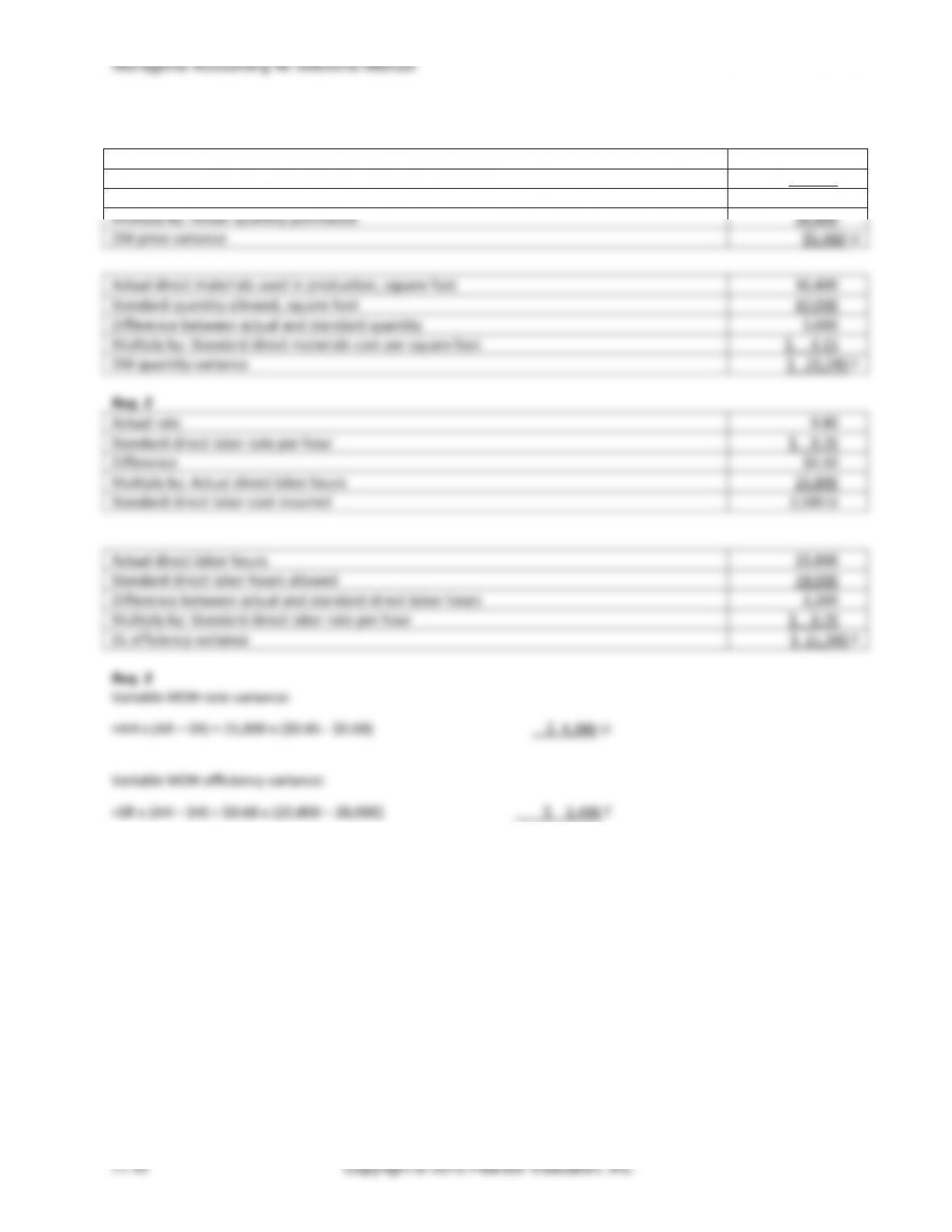

Standard price per unit

$ 13.00

Actual price per unit

$ 12.60

Difference

$ 0.40

Multiply by: Actual quantity purchased

43,470

DM price variance

$ 17,388 F

Actual quantity used

38,800

Standard quantity allowed

39,900

Difference

1,100

Multiply by: Standard direct materials cost per yard

$ 13.00

DM quantity variance

$ 14,300 F

Chapter 11 Standard Costs and Variances

(continued) P11-54B

Actual DL rate per hour

$11.20

Standard DL rate per hour

$11.00

Difference

$0.20

Multiply by: Actual DL hours

8,270

DL rate variance

$ 1,654 F

Actual DL hours

8,270

Standard DL hours allowed

8,400

Difference

130

Multiply by: Standard DL rate per hour

$11.00

DL efficiency variance

$ 1,430 F

Variable MOH rate variance:

=AH x (AR – SR) = 8,270 x ($5.40 – $5.00)

$ 3,308 U

Variable MOH efficiency variance:

=SR x (AH – SH) = $5.00 x (8,270 – 8,400)

$ 650 F

Fixed overhead budget variance:

Actual fixed MOH – Budgeted fixed MOH = $86,800 – $81,800

$ 5,000 U

Fixed overhead volume variance:

Budgeted fixed MOH – Std. fixed MOH allocated to production (SHA

x Std. fixed MOH rate) = $81,800 – $84,000

$ 2,200 F

Req. 3

The favorable DM price variance shows that less was paid for the raw material than was budgeted. The favorable DM

quantity variance shows that less of the raw material was used in production than was budgeted.

A favorable DL rate variance shows that the wage paid was less than the wage budgeted. The favorable DL efficiency

variance shows that less labor was used than was budgeted.

The Unfavorable variable MOH rate variance tells managers that the actual amount of MOH was greater than the

expected amount given the direct labor hours used. The favorable variable MOH efficiency variance tells managers that

the actual hours used were less than the standard hours allowed.

The unfavorable fixed MOH budget variance tells managers that more fixed overhead costs were incurred than were

budgeted for. The favorable fixed MOH volume variance tells managers that production volume was greater than

anticipated.

Student answers may vary.

Managerial Accounting 4e Solutions Manual

(15-30 min.) P11-55B

Req. 1

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Direct materials

60 lbs

x

$5 per lb

=

$300

Direct labor

2 hrs.

x

$13 per hr

=

$26

Variable MOH

2 hrs.

x

$7 per hr

=

$14

Fixed MOH

2 hrs.

x

$5 per hr

=

$10

Standard cost

$350

Standard price per unit

$ 5.00

Actual price per unit

$ 4.90

Difference

$ 0.10

Multiply by: Actual quantity purchased

4,260

DM price variance

$ 426 F

Actual quantity used

4,200

Standard quantity allowed

3,600

Difference between actual and standard quantity

600

Multiply by: Standard price

$ 5.00

DM quantity variance

$ 3,000 U

Actual DL rate

$13.80

Standard DL rate

$13.00

Difference

$0.80

Multiply by: Actual hours

150

DL rate variance

$ 120 U

Actual hours

150

Standard hours allowed

120

Difference between actual and standard direct labor hours

30

Multiply by: Standard DL rate

$ 13.00

DL efficiency variance

$ 390 U

Variable MOH rate variance:

=AH x (AR – SR) = 150 x ($7.50 – $7.00)

$ 75 U

Variable MOH efficiency variance:

=SR x (AH – SH) = $7.00 x (150 – 120)

$ 210 U

Fixed overhead budget variance:

Actual fixed MOH – Budgeted fixed MOH = $1,550 – $1,250

$ 300 U

Fixed overhead volume variance:

Budgeted fixed MOH – Std. fixed MOH allocated to production (SHA

x Std. fixed MOH rate) = $1,250 – $600

$ 650 U

Chapter 11 Standard Costs and Variances

(continued) P11-55B

Req. 3

(15-30 min.) P11-56B

Req. 1

Standard direct labor rate per hour

–

Favorable labor rate

variance

=

Actual direct labor rate per

hour

$8.00

–

0.30

=

$7.70

Coral’s Music

Schedule to Compute Actual Direct Labor Hours

Actual

Flexible Budget for

Actual Output

Flexible

Budget

Variance

Direct labor hours

5,500

5,340

Cost per hour

$ 7.70

$ 8.00

Total direct labor cost

$42,350

$42,720

Flexible budget variance

$ 370 F

Req. 2

Price variance

=

Actual price

−

Standard price

×

Actual quantity

per input unit

per input unit

of input

Direct labor

=

($7.70 per hour − $8.00 per hour)

×

5,500 hours

price variance

=

$1,650 F

Efficiency

=

Actual quantity

−

Standard quantity

×

Standard price

variance

of input

of input

per input unit

Direct labor

=

(5,500 hours − 5,340 hours)

×

$8.00 per hour

efficiency variance

=

$1,280 U

The favorable direct labor rate variance combined with the unfavorable direct labor efficiency variance suggests that

the manager may have used lower paid, less efficient workers. However, due to the overall net effect, it appears this

was a reasonable tradeoff.

Chapter 11 Standard Costs and Variances

(continued) P11-57B

Req. 4

Fixed overhead budget variance:

Actual fixed MOH – Budgeted fixed MOH = $57,508 – $63,000

$ 5,492 F

Fixed overhead volume variance:

Budgeted fixed MOH – Std. fixed MOH allocated to production (SHA

x Std. fixed MOH rate) = $63,000 – $61,600

$ 1,400 U

Req. 5

The favorable quantity, efficiency, and budget variances more than offset the unfavorable price, rate, and fixed volume

variances. If the superior materials purchased for the November production decreased materials and labor usage, then

management’s decision was wise.

Req. 6

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Raw Materials Inventory (36,400 x $4.15)

151,060

Direct Materials Price Variance

5,460

Accounts Payable (36,400 x $4.30)

156,520

To record the purchase of raw materials.

Work in Process Inventory (42,000 x $4.15)

174,300

Direct Materials Efficiency Variance

23,240

Raw Materials Inventory (36,400 x $4.15)

151,060

To record the use of raw materials.

Work in Process Inventory (28,000 x $9.70)

271,600

Direct Labor Efficiency Variance

2,580

Direct Labor Rate Variance

21,340

Wages Payable (25,800 x $9.80)

252,840

To record incurrence of direct labor.

Managerial Accounting 4e Solutions Manual

Discussion & Analysis

1. Suppose a company is implementing lean accounting throughout the organization. Why might standard costing

NOT be beneficial for that company?

company.

2. What advantages might be experienced by a company if it adopts ideal standards for its direct material

standards and direct labor standards? What advantages are there to using practical standards? As an employee,

which would you prefer and why? Does your answer change if you are the manager in charge of production?

3. Select a product with which you are familiar. Describe what type of standards (direct material and direct labor)

might be in effect for that product wherever it is produced. For each of these standards, discuss how those

4. Service organizations also use standards. Describe what types of standards might be in effect at each of the

following types of organizations:

5. What does the direct materials price variance measure? Who is generally responsible for the direct materials

price variance? Describe two situations that could result in a favorable materials price variance. Describe two

Chapter 11 Standard Costs and Variances

6. What does the direct materials efficiency variance measure? Who is generally responsible for the direct

materials efficiency variance? Describe two situations that could result in a favorable direct materials efficiency

variance. Describe two situations that could result in an unfavorable direct materials efficiency variance.

7. What does the direct labor rate variance measure? Who is generally responsible for the direct labor rate

variance? Describe two situations that could result in a favorable direct labor rate variance. Describe two

8. What does the direct labor efficiency variance measure? Who is generally responsible for the direct labor

efficiency variance? Describe two situations that could result in a favorable labor efficiency variance. Describe

two situations that could result in an unfavorable labor efficiency variance.

9. Describe at least four ways a company could use standard costing and variance analysis.

• Standard costing saves on bookkeeping costs.

10. What are the two manufacturing overhead variances? What does each measure? Who within the organization

would be responsible for each of these variances?

11. Suppose a company that makes and sells spaghetti sauce in plastic jars makes a change to its bottle that allows it

to use significantly less plastic in each bottle. Describe at least four ways this change could help the company

Chapter 11 Standard Costs and Variances

Team Project

(30-60 min.) A11-60

1. Pella will need standards that will enable them to compute:

• Direct materials price and efficiency variances for individual direct materials, including:

– glass

– wood

– different types of hardware, such as door handles, and window cranks

– and so on.

not very helpful for controlling business operations, so Pella may decide not to compute this variance.

• Pella should develop non-financial standards for key factors such as quality (number of defects) and on-time

delivery.

2a. Three alternative approaches to setting standards include:

• Engineering analysis/time-and-motion studies

This approach reveals the minimum amount of direct materials, direct labor, and manufacturing overhead

practice within the company. If the Carroll, Iowa, plant is not the most efficient in the company, then

benchmarks could be adopted from the most efficient of the company’s other plants. External benchmarks

require standards based on the “best practice” of other companies. Pella might be able to obtain benchmark

data from industry trade publications or from consultants. Or Pella might enter into a partnering relationship

with another company such as Anderson Windows or Peachtree Windows, where the partner companies

Managerial Accounting 4e Solutions Manual

these costs be reduced by a specified percentage each quarter (or year). A problem with this approach is that

after some point, further reductions may not be possible. Management must be careful not to make demands

that employees believe are unattainable.

2) Continuous improvement standards, and/or

3) Benchmarking.

Any of these three approaches will provide incentives to reduce costs and increase operating efficiency. Without

more information on the costs of each approach, we cannot definitively recommend a single method.