Chapter 11 Standard Costs and Variances

(10-15 min.) E11-39B

Journal Entry

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

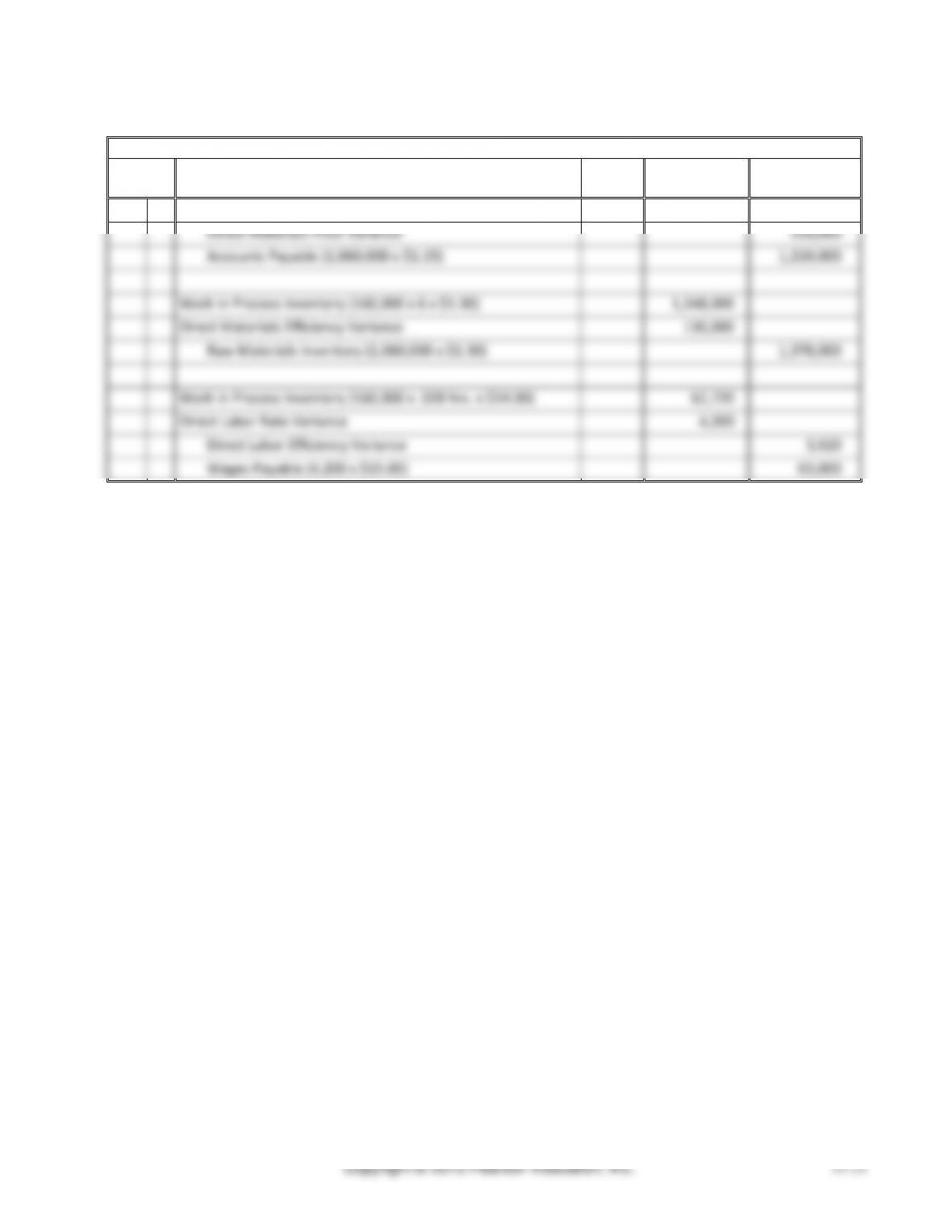

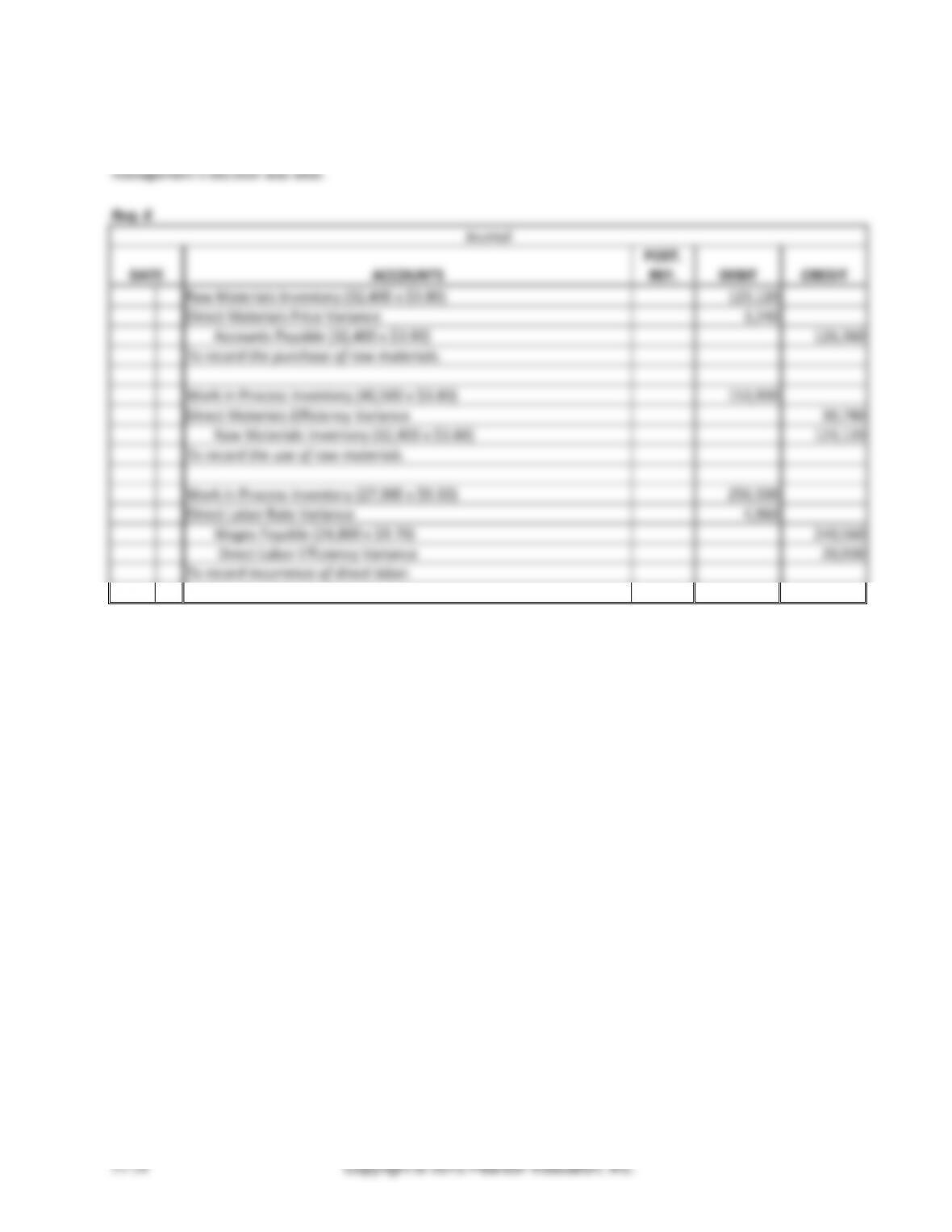

Raw Materials Inventory (1,060,000 x $1.30)

1,378,000

Direct Materials Price Variance

159,000

Accounts Payable (1,060,000 x $1.15)

1,219,000

Work in Process Inventory (160,000 x 6 x $1.30)

1,248,000

Direct Materials Efficiency Variance

130,000

Raw Materials Inventory (1,060,000 x $1.30)

1,378,000

Work in Process Inventory (160,000 x .028 hrs. x $14.00)

62,720

Direct Labor Rate Variance

4,200

Direct Labor Efficiency Variance

3,920

Wages Payable (4,200 x $15.00)

63,000

Chapter 11 Standard Costs and Variances

(10-15 min.) E11-42B

Req. 1

Variable overhead allocated (162,000 x .25 x $0.55)

$22,275

Fixed overhead allocated (162,000 x .25 x $16.60)

$675,300

Req. 2

Standard hours allowed (SHA)

= 162,0000 cases x .25 DLH = 40,500 DLH

Variable MOH rate variance (a)

= AH x (AR – SR) = 42,000 x (1.05 – $0.55) = $21,000 U

Variable MOH efficiency variance (b)

= SR x (AH – SH) = $0.55 x (42,000 – 40,500) = $825 U

Fixed overhead budget variance (a)

= Actual FOH – Budgeted FOH = $644,000 – $634,000 = $10,000 U

Fixed overhead volume variance (b)

= Budgeted FOH – Standard FOH Allocated

= $634,000 – 672,300

= $38,300 F

(10-15 min.) E11-43B

Req. 1

Standard price per unit

$ 5.00

Actual price per unit

$ 5.20

Difference

$0.20

Multiply by: Actual quantity purchased

30,230

DM price variance

$6,046 U

Actual direct materials used in production (pounds)

29,830

Standard direct materials allowed, in pounds

28,500

Difference between actual and standard quantity

1,330

Multiply by: Standard direct materials cost per pound

$ 5.00

DM quantity variance

$ 6,650 U

Req. 2

The total variance cannot be calculated due to the purchased quantity being different from the used quantity.

Req. 3

The direct materials price variance is the responsibility of the purchasing manager. The materials quantity variance is

the responsibility of the production manager.

Req. 4

The unfavorable price variance shows that more was paid for the raw material than was budgeted. The unfavorable

quantity variance shows that more of the raw material was used in production than was budgeted.

Chapter 11 Standard Costs and Variances

(10-15 min.) E11-46B

Req. 1

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

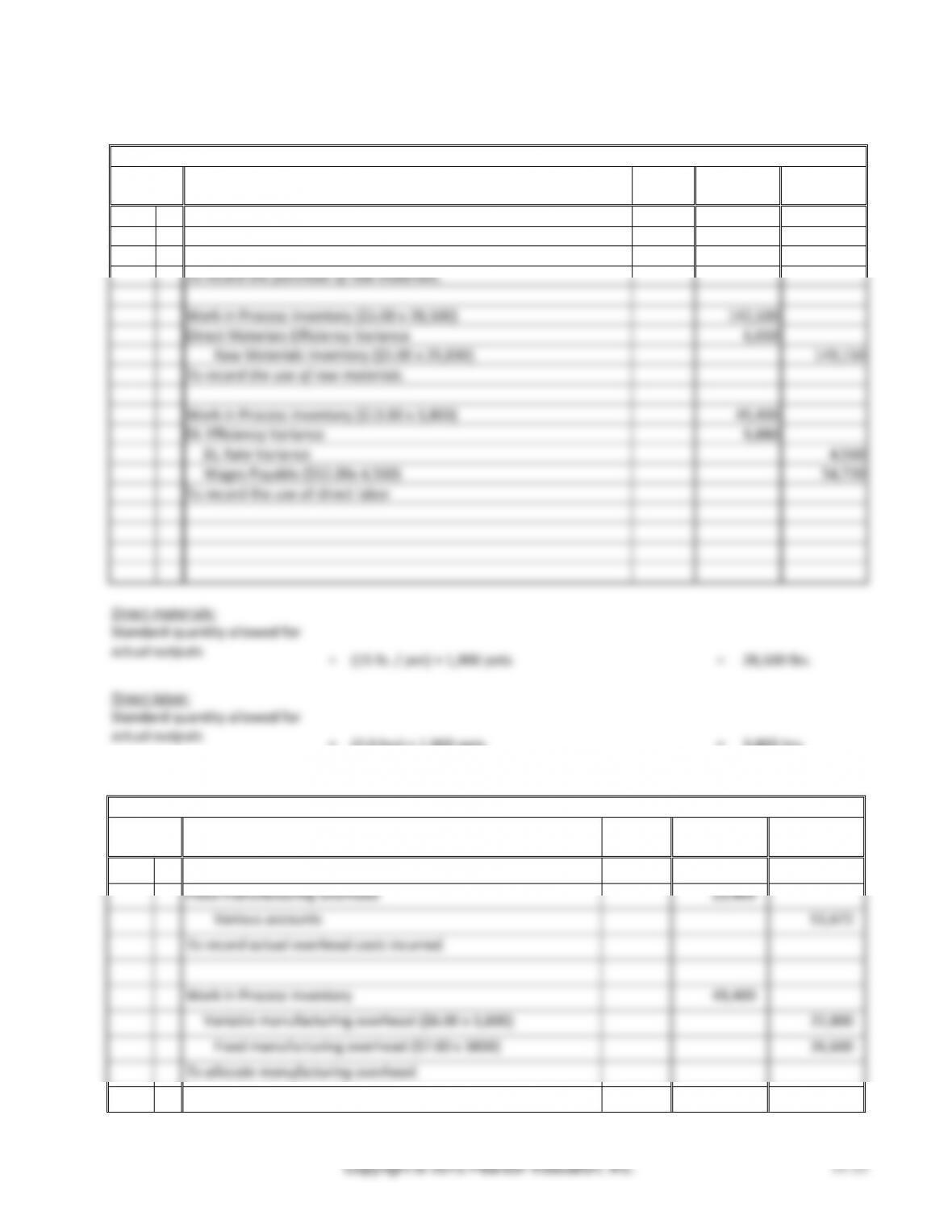

Raw Materials Inventory (30,230 x $5.00)

151,150

Direct Materials Price Variance

6,046

Accounts Payable (30,230 x $5.20)

157,196

To record the purchase of raw materials.

Work in Process Inventory ($5.00 x 28,500)

142,500

Direct Materials Efficiency Variance

6,650

Raw Materials Inventory ($5.00 x 29,830)

149,150

To record the use of raw materials.

Work in Process Inventory ($13.00 x 3,800)

49,400

DL Efficiency Variance

9,880

DL Rate Variance

4,560

Wages Payable ($12.00x 4,560)

54,720

To record the use of direct labor

Direct materials:

Standard quantity allowed for

actual outputs

=

(15 lb. / pot) × 1,900 pots

=

28,500 lbs.

Direct labor:

Standard quantity allowed for

actual outputs

=

(2.0 hrs) × 1,900 pots

=

3,800 hrs.

Req. 2

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Variable manufacturing overhead

28,272

Fixed manufacturing overhead

23,400

Various accounts

51,672

To record actual overhead costs incurred.

Work in Process Inventory

49,400

Variable manufacturing overhead ($6.00 x 3,800)

22,800

Fixed manufacturing overhead ($7.00 x 3800)

26,600

To allocate manufacturing overhead.

Managerial Accounting 4e Solutions Manual

(continued) E11-46B

Req. 3

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

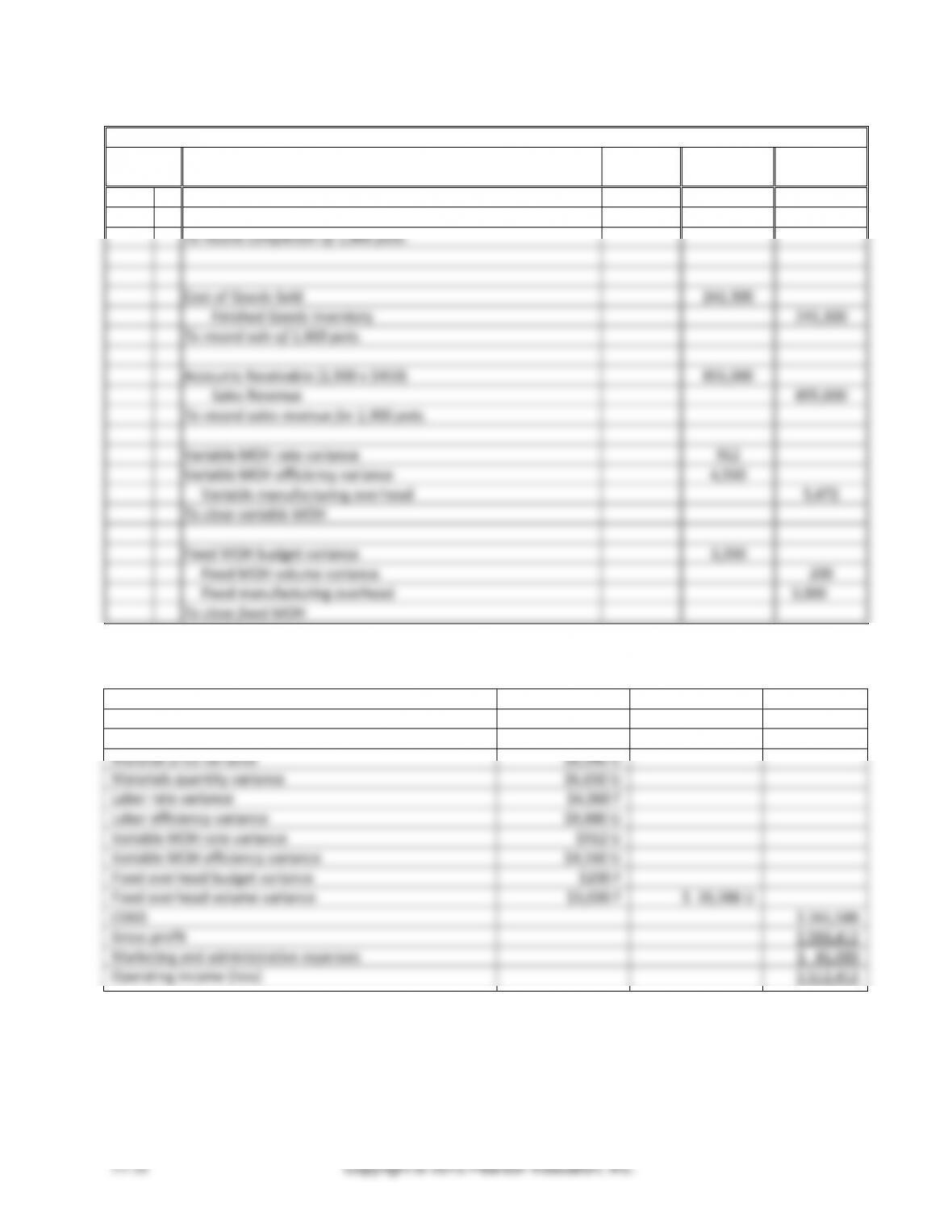

Finished Goods Inventory

241,300

Work in Process Inventory (142,500 + 49,400 + 49,400)

241,300

To record completion of 1,900 pots:

Cost of Goods Sold

241,300

Finished Goods Inventory

241,300

To record sale of 1,900 pots.

Accounts Receivable (1,900 x $450)

855,000

Sales Revenue

855,000

To record sales revenue for 1,900 pots.

Variable MOH rate variance

912

Variable MOH efficiency variance

4,560

Variable manufacturing overhead

5,472

To close variable MOH

Fixed MOH budget variance

3,200

Fixed MOH volume variance

200

Fixed manufacturing overhead

3,000

To close fixed MOH

(10-15 min.) E11-47B

Sales revenue

$ 855,000

Cost of goods sold at standard cost

$241,300

Manufacturing cost variances:

Material price variance

$6,046 U

Materials quantity variance

$6,650 U

Labor rate variance

$4,560 F

Labor efficiency variance

$9,880 U

Variable MOH rate variance

$912 U

Variable MOH efficiency variance

$4,560 U

Fixed overhead budget variance

$200 F

Fixed overhead volume variance

$3,000 F

$ 20,288 U

COGS

$ 261,588

Gross profit

$ 593,412

Marketing and administrative expenses

$ 81,000

Operating income (loss)

$ 512,412

Chapter 11 Standard Costs and Variances

Problems (Group A)

(15 min.) P11-48A

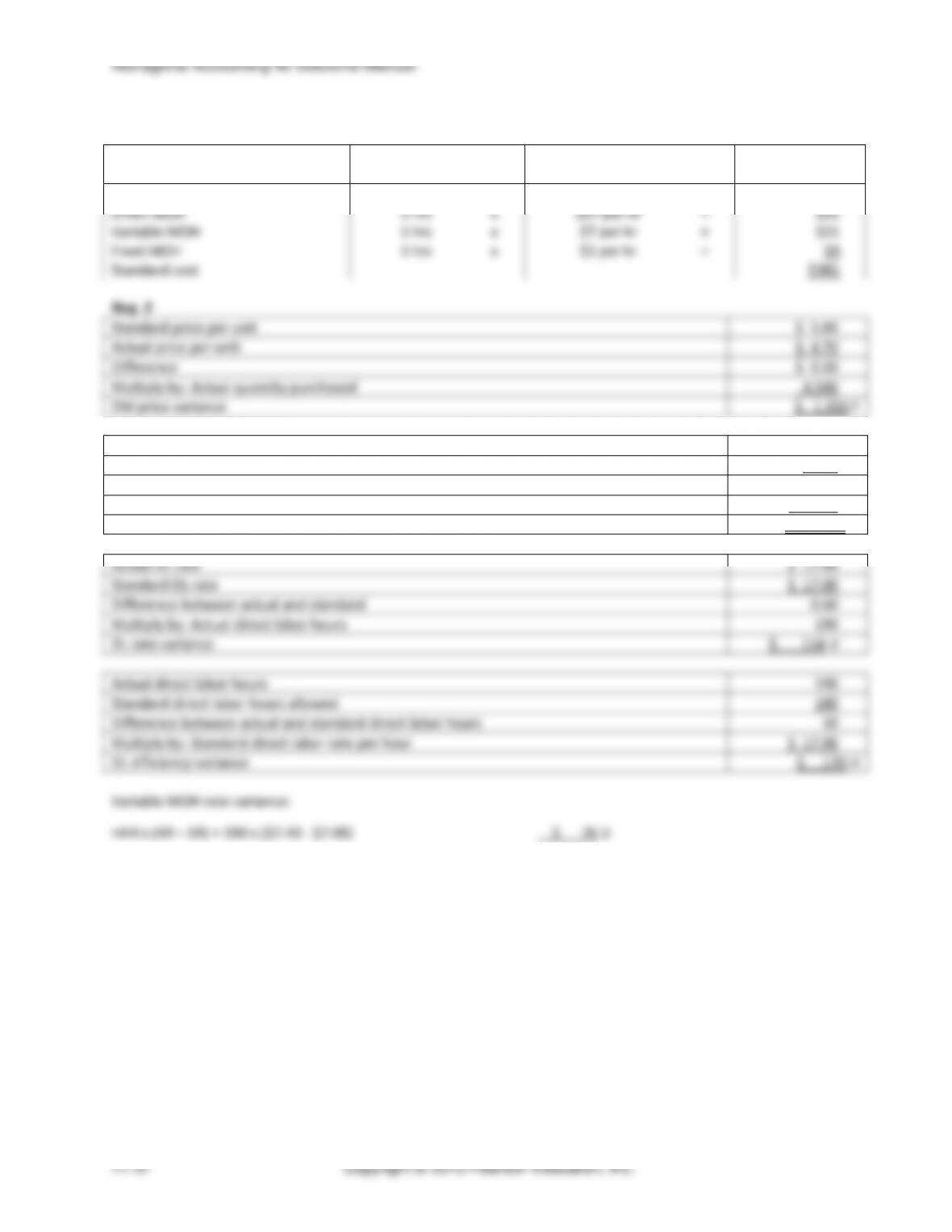

Req. 1

DM

6 yards

X

$9.00 per yard

$54

Standard price per unit

$ 9.00

Actual price per unit

$ 8.10

Difference

$ 0.90

Multiply by: Actual quantity purchased

15,750

Direct Material price variance

$ 14,175 F

Actual rate

$ 18.30

Standard rate

$ 19.00

Difference:

$0.70

Multiply by: Actual direct labor hours

1,370

DL rate variance

$959 F

Actual hours

1,370

Standard hours allowed

1,250

Difference

120

Multiply by: Standard rate

$ 19.00

DL efficiency variance

$ 2,280 U

Req. 7

The favorable DM price variance and unfavorable DM quantity variance may have been caused by purchasing inferior

Actual direct materials used in production (yards)

15,250

Standard quantity allowed, in yards

15,000

Difference

250

Multiply by: Standard cost per yard

$ 9.00

Direct Material quantity variance

$ 2,250 U

Managerial Accounting 4e Solutions Manual

(continued) P11-48A

(15-20 min.) P11-49A

Req. 1

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Direct materials

22 yard

x

$13 per yard

=

$286

Direct labor

5 hrs.

x

$15 per hr

=

$75

Variable MOH

5 hrs.

x

$8 per hour

=

$40

Fixed MOH

5 hrs.

x

$6 per hour

=

$30

Standard cost

$431

Standard price per unit

$ 13.00

Actual price per unit

$ 12.90

Difference

$ 0.10

Multiply by: Actual quantity purchased

51,260

DM price variance

$ 5,126 F

Actual direct materials used

47,500

Standard quantity allowed

48,400

Difference

900

Multiply by: Standard direct materials cost per yard

$ 13.00

DM quantity variance

$ 11,700 F

Standard DL rate per hour

$ 15.00

Actual DL rate per hour

$ 15.50

Difference

$0.50

Multiply by: Actual direct labor hours

10,850

DL rate variance

$5,425 U

Actual direct labor hours

10,850

Standard direct labor hours allowed

11,000

Difference

150

Multiply by: Standard direct labor rate per hour

$ 15.00

DL efficiency variance

$ 2,250 F

Chapter 11 Standard Costs and Variances

(continued) P11-49A

Variable MOH rate variance:

=AH x (AR – SR) = 10,850 x ($8.60 – $8.00)

$ 6,510 U

Variable MOH efficiency variance:

=SR x (AH – SH) = $8 x (10,850 – 11,000)

$ 1,200 F

Fixed overhead budget variance:

Actual fixed MOH – Budgeted fixed MOH ($67,500 – $63,500)

$ 4,000 U

Fixed overhead volume variance:

Budgeted fixed MOH – Std. fixed MOH allocated to production (SHA

x Std. fixed MOH rate) ($63,500 – $66,000)

$ 2,500 F

Req. 3

The favorable DM price variance shows that less was paid for the raw material than was budgeted. The favorable DM

quantity variance shows that less of the raw material was used in production than was budgeted.

An unfavorable DL rate variance shows that the wage paid was higher than the wage budgeted. The favorable DL

efficiency variance shows that less labor was used than was budgeted.

The Unfavorable variable MOH rate variance tells managers that the actual amount of MOH was greater than the

expected amount given the direct labor hours used. The favorable variable MOH efficiency variance tells managers that

the actual hours used were less than the standard hours allowed.

The unfavorable fixed MOH budget variance tells managers that more fixed overhead costs were incurred than were

budgeted for. The favorable fixed MOH volume variance tells managers that production volume was greater than

anticipated.

Student answers may vary.

Chapter 11 Standard Costs and Variances

(continued) P11-50A

Variable MOH efficiency variance:

=SR x (AH – SH) = $7.00 x (190 – 180)

$ 70 U

Fixed overhead budget variance:

Actual fixed MOH – Budgeted fixed MOH = $1,490 – $1,090

$ 400 U

Fixed overhead volume variance:

Budgeted fixed MOH – Std. fixed MOH allocated to production (SHA

x Std. fixed MOH rate) = $1,090 – $540

$ 550 U

Req. 3

Management has not done a good job controlling material, labor, and overhead costs. Each of these areas incurred an

unfavorable variance during the period.

Req. 4

The following are benefits of a standard costing system:

Standards are often used as the basis for many components in the master budget.

Standard costing systems simplify bookkeeping.

Standards create a benchmark by which to judge actual costs.

The use of practical, or attainable, standards should increase employee motivation.

The company should continue the standard cost system if the benefits outweigh the costs.

Managerial Accounting 4e Solutions Manual

(15-20 min.) P11-51A

Req. 1

Standard direct labor rate per hour

–

Favorable labor rate

variance

=

Actual direct labor rate per

hour

$10.00

–

0.50

=

$9.50

Petra’s Music

Schedule to Compute Actual Direct Labor Hours

Actual

Flexible Budget for

Actual Output

Flexible

Budget

Variance

Direct labor hours

5,860

5,600

Cost per hour

$ 9.50

$ 10.00

Total direct labor cost

$55,670

$56,000

Flexible budget variance

$ 330 F

Req. 2

Price variance

=

Actual price

−

Standard price

×

Actual quantity

per input unit

per input unit

of input

Direct labor

=

($9.50 per hour − $10.00 per hour)

×

5,860 hours

price variance

=

$2,930 F

Efficiency

=

Actual quantity

−

Standard quantity

×

Standard price

variance

of input

of input

per input unit

Direct labor

=

(5,860 hours − 5,600 hours)

×

$10.00 per hour

efficiency variance

=

$2,600 U

The favorable direct labor rate variance combined with the unfavorable direct labor efficiency variance suggests that

the manager may have used lower paid, less efficient workers. However, due to the overall net effect, it appears there

was a reasonable tradeoff.

(15-20 min.) P11-52A

Req. 1

Standard price per unit

$ 3.80

Actual price per unit

$ 3.90

Difference

$ 0.10

Multiply by: Actual quantity purchased

32,400

DM price variance

$ 3,240 U

Chapter 11 Standard Costs and Variances

(continued) P11-52A

Actual direct materials used in production, square foot

32,400

Standard quantity allowed, square foot

40,500

Difference between actual and standard quantity

8,100

Multiply by: Standard direct materials cost per square foot

$ 3.80

DM quantity variance

$ 30,780 F

Req. 2

Actual rate

$9.70

Standard direct labor rate per hour

$9.50

Difference

$0.20

Multiply by: Actual direct labor hours

24,800

DL rate variance

$ 4,960 U

Actual hours

24,800

Standard hours allowed

27,000

Difference between actual and standard direct labor rate

2,200

Multiply by: standard DL rate

$9.50

DL efficiency variance

$ 20,900 F

Req. 3

Variable MOH rate variance:

=AH x (AR – SR) = 24,800 x ($0.70 – $0.58) =

$ 2,976 U

Variable MOH efficiency variance:

=SR x (AH – SH) = $0.58 x (24,800 – 27,000) =

$1,276 F

Req. 4

Fixed overhead budget variance:

Actual fixed MOH – Budgeted fixed MOH = $56,565 – $64,200

$ 7,635 F

Fixed overhead volume variance:

Budgeted fixed MOH – Std. fixed MOH allocated to production (SHA

x Std. fixed MOH rate) = $64,200 – $60,750

$ 3,450 U

Managerial Accounting 4e Solutions Manual

(continued) P11-52A

Req. 5

The favorable quantity, efficiency, and budget variances more than offset the unfavorable price, rate and fixed volume

variances. If the superior materials purchased for the November production decreased materials and labor usage, then