Chapter 11 Standard Costs and Variances

Copyright © 2015 Pearson Education, Inc.

11-1

Chapter 11

Standard Costs and Variances

Quick Check

Answers:

QC-1. a

QC-3. a

QC-5. c

QC-7. d

QC-9. a

QC-2. b

QC-4. d

QC-6. b

QC-8. c

QC-10. d

(5 min.) S11-1

Quantity

Price

Cost

Sugar per cup

7

$ 0.17

$ 1.19

Chocolate chips per ounce

23

$ 0.18

$ 4.14

Butter per ounce

16

$ 0.11

$ 1.76

Evaporated milk per ounce

18

$ 0.14

$ 2.52

Std DM cost per batch

$ 9.61

(5 min.) S11-2

0.26 hours x $17.50 = $4.55 standard direct labor cost per batch

(5 min.) S11-3

Actual direct material cost per unit

$ 1.92

Standard direct material cost per unit

$ 2.00

Difference between actual and standard cost per unit

$ 0.08

Multiply by: Actual direct material purchased and used

78,125

Direct material price variance

$ 6,250 F

Actual direct material purchased and used

78,125

Standard direct material usage

75,000

Difference between actual and standard material usage

3,125

Multiply by: Standard direct material cost per unit

$ 2.00

Direct material quantity variance

$ 6,250 U

Chapter 11 Standard Costs and Variances

(5-10 min.) S11-7

Req. 1

Actual machine hours used

1,550 hrs.

Standard total hours (3,000 x 0.25)

1,500 hrs

Difference

50 hrs.

Multiply by: Standard rate per hour

Variable MOH efficiency variance

$900 U

(5-10 min.) S11-9

Req. 1

Total overhead variance:

Actual fixed overhead cost

$1,270,000

Standard fixed overhead allocated to production

$1,220,000

Total fixed overhead variance

$50,000 U

The variance tells managers that Harris underallocated fixed manufacturing overhead by this amount.

Req. 2

Overhead flexible budget variance:

Actual fixed overhead cost

$1,270,000

Budgeted fixed overhead for actual outputs

$1,285,000

Fixed overhead budget variance

$ 15,000 F

The variance tells managers that the company actually incurred less for fixed manufacturing overhead than it would

have expected for the actual volume produced during the year.

Req. 3

Fixed overhead volume variance:

Budgeted fixed overhead for actual outputs

$1,285,000

Standard fixed overhead allocation to production

$1,220,000

Fixed overhead volume variance

$65,000 U

Managers can tell from the variance amount that the total fixed overhead variance arose because the company

produced less flutes than originally expected. It is unfavorable because the company used its plant capacity less

efficiently than originally anticipated.

Actual rate per hour

$17.00

Standard rate per hour

$18.00

Difference

$1.00

Multiply by: Actual machine hours used

1,550 hrs.

Variable MOH rate variance

$1,550 F

Chapter 11 Standard Costs and Variances

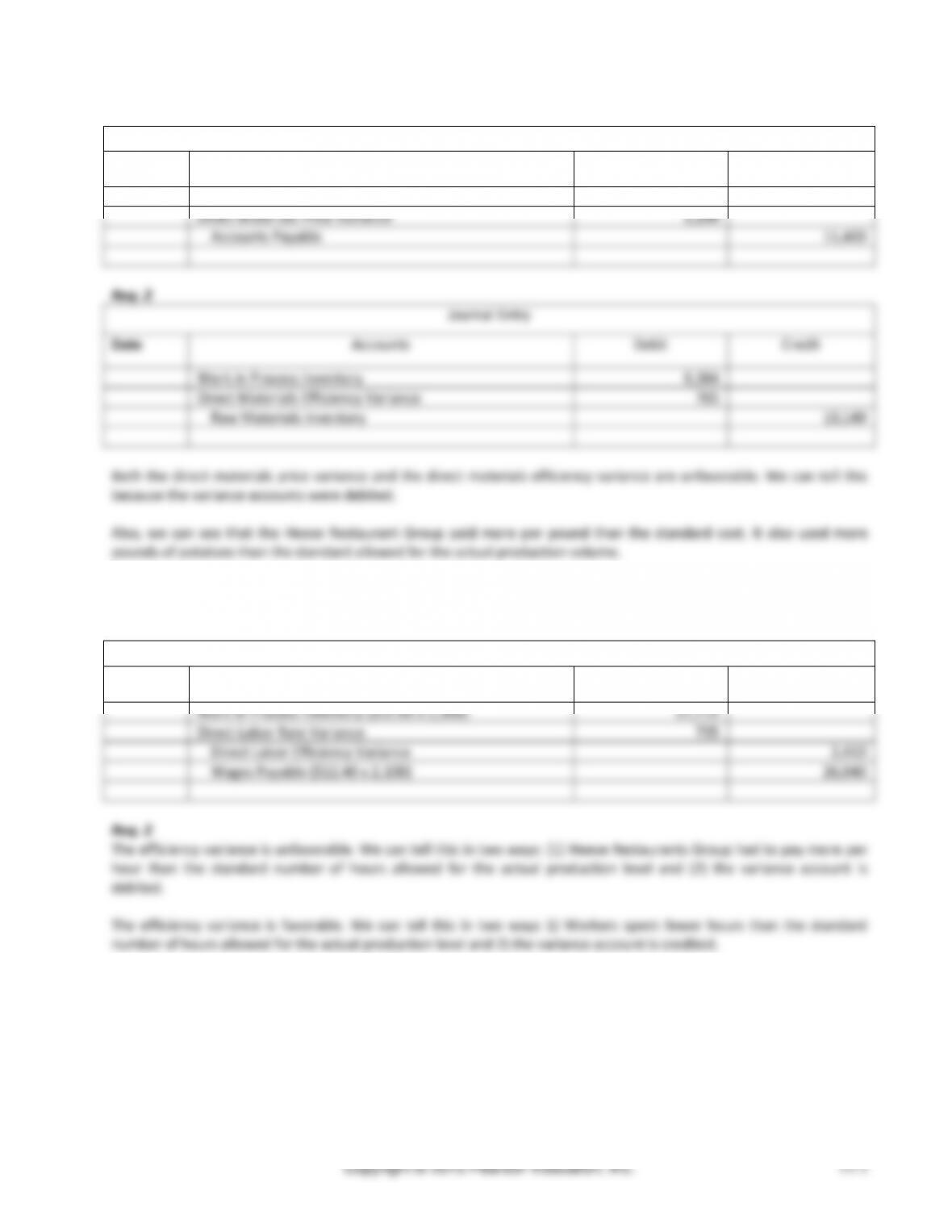

(10 min.) S11-12

Req. 1

Journal Entry

Date

Accounts

Debit

Credit

Raw Material Inventory

10,200

Direct Materials Price Variance

1,200

Accounts Payable

11,400

Work in Process Inventory

9,384

Direct Materials Efficiency Variance

Raw Materials Inventory

10,149

Journal Entry

Accounts

Debit

Credit

Work in Process Inventory ($12.05 x 2,300)

27,715

Direct Labor Rate Variance

Direct Labor Efficiency Variance

Wages Payable ($12.40 x 2,100)

26,040

Managerial Accounting 4e Solutions Manual

(5 – 10 min.) S11-14

1.

Sarabeth, an accountant at Warren Industries, and Jay,

an accountant at Sorenia Manufacturing, exchanged

cost and other production data so that they would have

benchmarks to use for their company reports.

Confidentiality – Keep information confidential

except when disclosure is authorized or legally

required.

2.

When Sandra prepares variance reports, only favorable

variances are listed. Unfavorable variances are only

provided if someone specifically asks.

Credibility – Disclose all relevant information

that could reasonably be expected to influence

an intended user’s understanding of the

reports, analyses, or recommendations.

3.

Preston is the chief accountant at Long Industries. Each

month, he prepares variance reports that are given to

all department managers. The variance reports are

frequently late and usually contain a few errors.

Competence – Provide decision support

information and recommendations that are

accurate, clear, concise, and timely.

4.

Devin accepts an all-expenses paid trip to Las Vegas

from a major supplier.

Integrity – Mitigate actual conflicts of interest,

regularly communicate with business associates

to avoid apparent conflicts of interest. Advise all

parties of any potential conflicts.

5.

Milton has just started to work at Brady Lake Supply. In

his first week, he is asked to fill in for a senior

accountant who is out of the office for six weeks on

maternity leave. He is asked to prepare the standard

costing journal entries. Milton does not know how to

do this work, but he decides to guess because he does

not want to appear stupid by asking for help.

Competence – Recognize and communicate

professional limitations or other constraints

that would preclude responsible judgment or

successful performance of an activity.

Chapter 11 Standard Costs and Variances

(10-15 min.) S11-15

Term

Definition

1. Fixed overhead volume

variance

e. Measures the difference between the budgeted fixed MOH costs and the

standard allocated MOH costs

2. Direct labor efficiency variance

b. Tells managers how much of the total variance is due to using a greater or

lesser amount of time than anticipated

3. Practical standards

i. Also known as attainable standards

4. Standard cost

g. The budget for a single unit of product

5. Direct materials quantity

variance

c. Tells managers how much of the total variance is due to using a difference

quantity of direct materials than expected

6. Direct labor rate variance

a. Tells managers how much of the total variance is due to paying a different

hourly wage rate than anticipated

7. Variable overhead rate

variance

h. Also called the variable overhead spending variance

8. Fixed overhead budget

variance

k. Measures the difference between the actual fixed MOH costs incurred and

the budgeted fixed MOH costs

9. Ideal standards

j. Standards based on conditions that do not allow for any waste in the

production process

10. Direct materials price

variance

f. Tells managers how much of the total variance is due to paying a different

price than expected for direct materials

11. Variable overhead efficiency

variance

d. Tells managers how much of the total variable MOH variance is due to using

more or less hours of the allocation base than anticipated for the actual volume

of output

Copyright © 2015 Pearson Education, Inc.

11-8

(10-15 min.) E11-16A

Req. 1

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Flour

3 cups

x

$0.12 per cup

=

$ 0.36

Pecans

½ cup

x

2.00 per cup

=

$ 1.00

Cocoa

¼ cup

x

1.24 per cup

=

$ 0.31

Sugar

2 cups

x

0.10 per cup

=

$ 0.20

Chocolate chips

½ cup

x

0.80 per cup

=

$ 0.40

Eggs

2

x

0.10 per egg

=

$ 0.20

Oil

1/3 cup

x

0.24 per cup

=

$ 0.08

Packaging

1 pkg.

x

0.60 per package

=

$ 0.60

Total direct materials

$ 3.15

Direct labor

1/4 hour

x

9.00 per hour

=

$ 2.25

Bakery overhead

½ hour

x

5.00 per hour

=

$ 2.50

Total

$ 7.90

Req. 2

The gross profit per pan of gourmet brownies is $6.10.

Req. 3

Jessica should reassess standard prices quite often, since the price of ingredients changes quite frequently. She should

also reassess her price standards if she finds cheaper suppliers for her ingredients.

However, they really won’t need to reassess her quantity standards for the direct materials unless she changes the

recipe. On the other hand, she should reassess her quantity standard for overhead if she decides to bake more than

one batch at a time in the oven.

(10-15 min.) E11-17A

Req. 1

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Direct materials

8 lbs.

x

$6 per lbs.

=

$48

Direct labor

2 hrs.

x

$15 per hr.

=

$30

Variable MOH

2 hrs.

x

$4 per hr.

=

$8

Fixed MOH

2 hrs.

x

$8 per hr.

=

$16

Req. 2

Total

$ 102

Managerial Accounting 4e Solutions Manual

(10 min.) E11-20A

Req. 1

Actual wage rate paid = $34,580 / 2,470 = $14.00 per hour

Req. 2

Actual rate per hour

$ 14.00

Standard rate per hour

$ 13.50

Difference between actual and standard rate per hour

$ 0.50

Multiply by: Actual direct labor hours used

2,470

Direct labor rate variance

$ 1,235 U

Req. 3

Actual direct labor hours used

2,470

Standard total hours allowed

2,500

Difference

30

Multiply by: Standard rate per hour

$13.50

Direct labor efficiency variance

$ 405 F

Req. 4

The unfavorable direct labor rate variance might mean that Altieri Tax Services hired more qualified return preparers at

a higher pay rate. As a result, the return preparers were able to use fewer hours than the standard allows. This

accounts for the favorable efficiency variance.

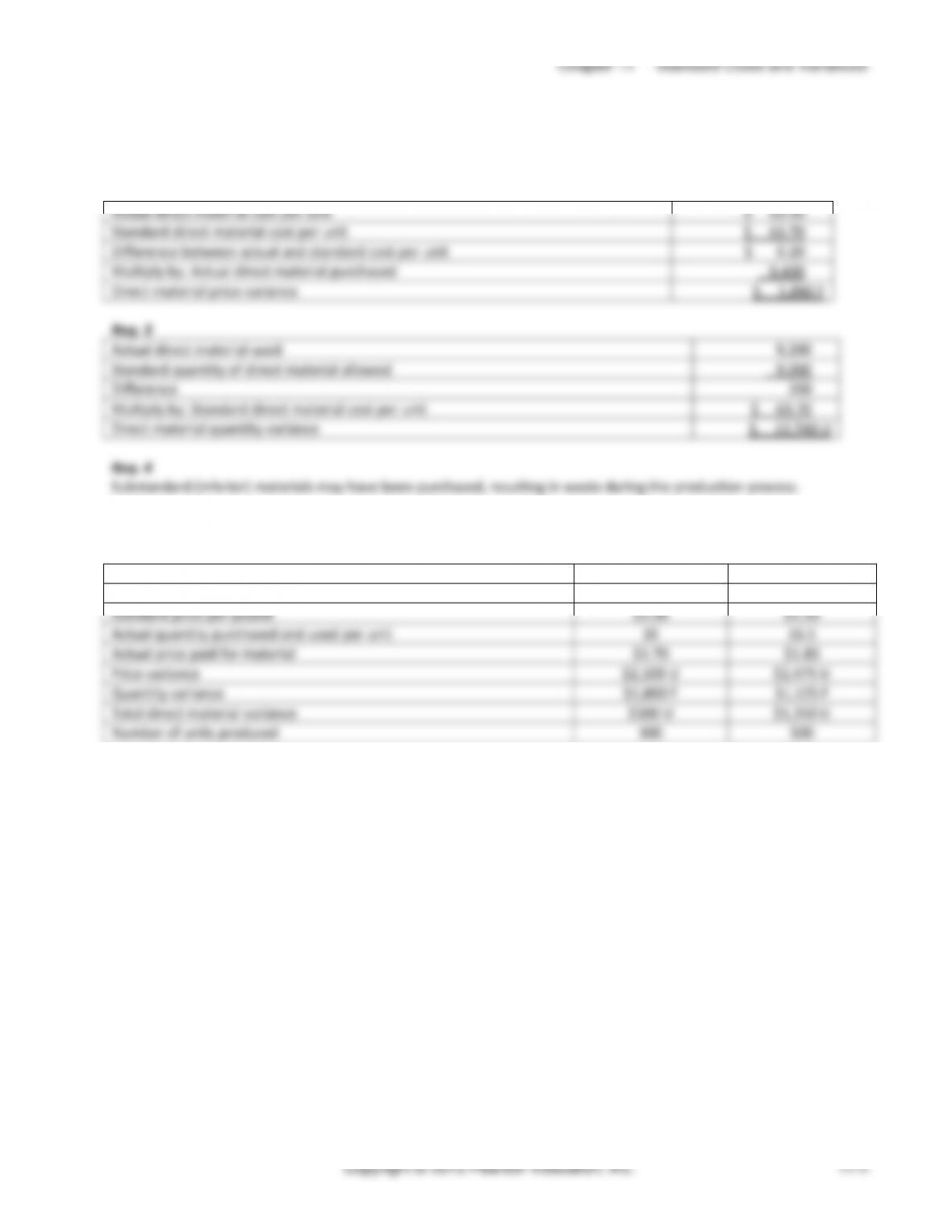

(10-15 min.) E11-21A

Req. 1

(

Actual price per unit

– Stand. price per unit

)

x

Actual quantity of input

=

Price variance

( $0.70 – 0.80 )

x

101,000

=

$10,100 F

(

Actual quantity of input

– Stand. quantity of input

)

x

Standard price per input

unit

=

Efficiency value

( 101,000 – 98,000 )

x

$0.80

=

$2,400 U

Req. 2

One plausible explanation is that Heese Restaurant Group bought lower grade potatoes at a cheaper price, which

resulted in the favorable price variance. However, because the potatoes were lower grade, some of the potatoes were

bad, and could not be used in production. As a result, the manufacturing facility had to use more potatoes than

standards allow. This accounts for the unfavorable efficiency variance.

Req. 3

Price variance (2,500 x ($12.25 – $12.10) =

$375 U

Efficiency variance ($12.10 x (2,500 – 2,400) =

$1,210 U

Req. 4

The unfavorable labor rate and efficiency variances could be tied to the material variances. For example, if the material

variances were the result of purchasing lower grade potatoes, then the factory would use more labor in sorting the

potatoes. As a result, they would have had to pay workers an overtime premium.

Managerial Accounting 4e Solutions Manual

(10-15 min.) E11-24A

Req. 1

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Direct materials

220 kg

x

$6 per kg

=

$1,320

Direct labor

4 hrs.

x

$20 per hr

=

$80

Variable MOH

4 hrs.

x

$40 per hr.

($400,000 / 10,000)

=

$160

Standard cost

$1,560

Input

Quantity Standard

Price Standard

Standard Cost of

Input

Direct materials

165 kg

(220 x .75)

x

$6 per kg

=

$990

Direct labor

3.2 hrs.

(4 x .8)

x

$20 per hr

=

64

Variable MOH

3.2 hrs.

(4 x .8)

x

$47.50 per hr.

(($400,000 x .95)/

8,000*)

=

152

Standard cost

$1,206

(5-10 min.) E11-25B

a. STANDARD COSTING would probably be beneficial

Managerial Accounting 4e Solutions Manual

(10-15 min.) E11-27A

Req. 1

Standard price per unit

$ 6.00

Actual price per unit

$ 6.30

Difference

$ 0.30

Multiply by: Actual quantity purchased

9,950

DM price variance

$2,985 U

Standard direct materials quantity per unit (pounds)

8.00

Actual units produced

1,100

Standard direct materials quantity, in pounds

8,800

Actual direct materials used in production (pounds)

9,350

Standard direct materials allowed, in pounds

8,800

Difference between actual and standard quantity

550

Multiply by: Standard direct materials cost per pound

$ 6.00

DM quantity variance

$ 3,300 U

Req. 2

The total variance cannot be calculated due to the purchased quantity being different from the used quantity.

Req. 3

The direct materials price variance is the responsibility of the purchasing manager. The materials quantity variance is

the responsibility of the production manager.

Req. 4

The unfavorable price variance shows that more was paid for the raw material than was budgeted. The unfavorable

quantity variance shows that more of the raw material was used in production than was budgeted.

Managerial Accounting 4e Solutions Manual

(10-15 min.) E11-30A

Req. 1

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Raw Materials Inventory (9,950 lbs. × $6.00)

59,700

Direct Materials Price Variance

2,985

Accounts Payable (9,950 lbs. × $6.30)

62,685

To record the purchase of raw materials.

Work in Process Inventory ($6.00 x 8,800)

52,800

Direct Materials Efficiency Variance

3,300

Raw Materials Inventory ($6.00 x 9,350)

56,100

To record the use of raw materials.

Work in Process Inventory ($15.00 x 2,200)

33,000

DL Efficiency Variance

3,300

DL Rate Variance

2,420

Wages Payable ($14.00 x 2,240)

33,880

To record the use of direct labor

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Variable manufacturing overhead

10,406

Fixed manufacturing overhead

16,400

Various accounts

26,806

To record actual overhead costs incurred.

Work in Process Inventory

26,400

Variable manufacturing overhead ($4.00 x 2,200)

8,800

Fixed manufacturing overhead ($8.00 x 2,200)

17,600

To allocate manufacturing overhead.

Chapter 11 Standard Costs and Variances

(continued) E11-30A

Req. 3

Journal

DATE

ACCOUNTS

POST.

REF.

DEBIT

CREDIT

Finished Goods Inventory

112,200

Work in Process Inventory (52,800 + 33,000 + 26,400)

112,200

To record completion of 1,100 pots:

Cost of Goods Sold

112,200

Finished Goods Inventory

112,200

To record sale of 1,100 pots.

Accounts Receivable (1,100 × $450)

495,000

Sales Revenue

495,000

To record sales revenue for 1,100 pots.

Variable MOH rate variance

726

Variable MOH efficiency variance

880

Variable manufacturing overhead

1,606

To close variable MOH

Fixed manufacturing overhead

1,200

Fixed MOH budget variance

200

Fixed MOH volume variance

1,000

To close fixed MOH

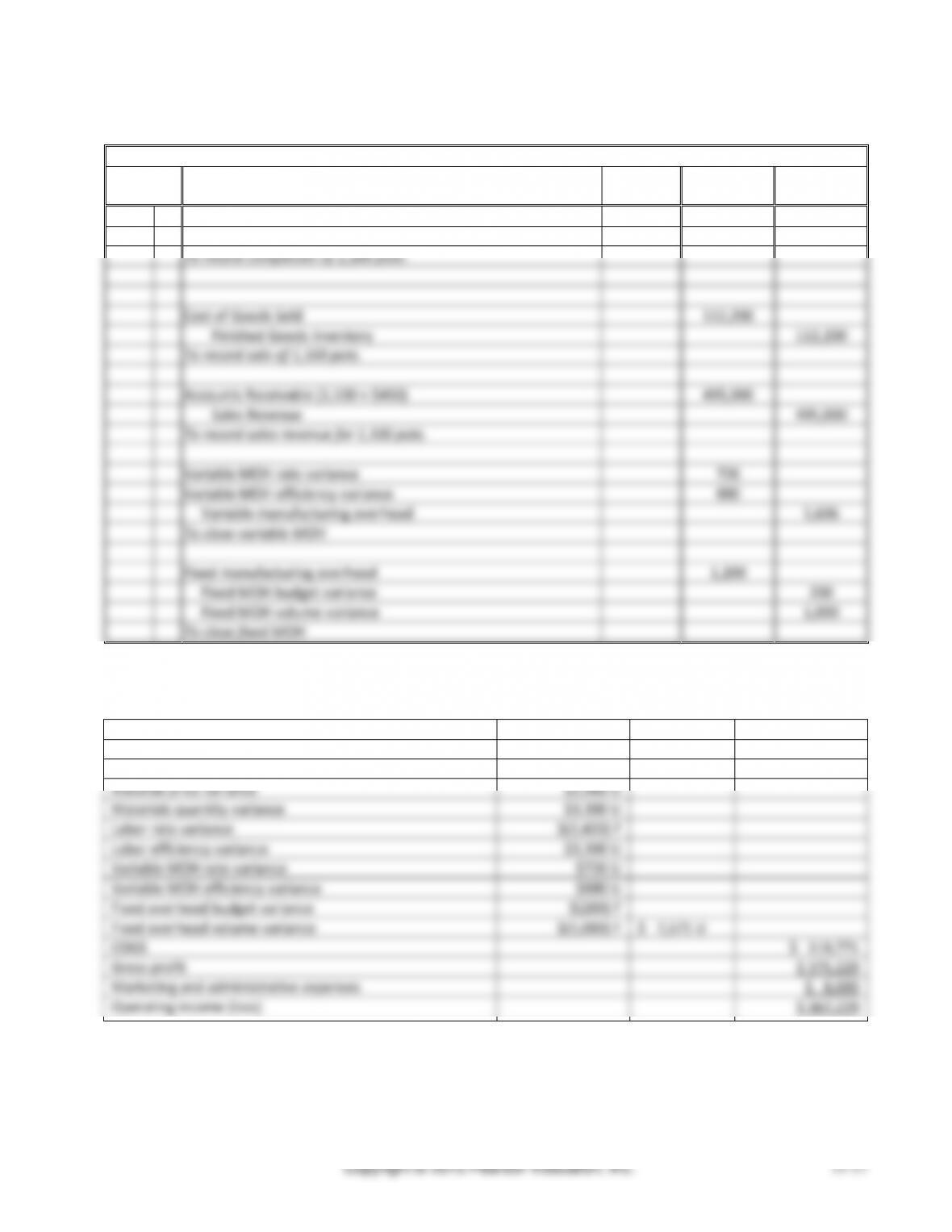

(15-20 min.) E11-31A

Sales revenue

$ 495,000

Cost of goods sold at standard cost

$112,200

Manufacturing cost variances:

Material price variance

$2,985 U

Materials quantity variance

$3,300 U

Labor rate variance

$(2,420) F

Labor efficiency variance

$3,300 U

Variable MOH rate variance

$726 U

Variable MOH efficiency variance

$880 U

Fixed overhead budget variance

$(200) F

Fixed overhead volume variance

$(1,000) F

$ 7,571 U

COGS

$ 119,771

Gross profit

$ 375,229

Marketing and administrative expenses

$ 8,000

Operating income (loss)

$ 367,229

Copyright © 2015 Pearson Education, Inc.

11–18

(10-15 min.) E11-32B

Req. 1

Input

Quality Standard

Price Standard

Standard Cost of

Input

Flour

2 cups

x

$0.14 per cup

=

$ 0.28

Pecans

½ cup

x

1.00 per cup

=

$ 0.50

Cocoa

¼ cup

x

1.60 per cup

=

$ 0.40

Sugar

1 cup

x

0.20 per cup

=

$ 0.20

Chocolate chips

½ cup

x

0.70 per cup

=

$ 0.35

Eggs

2

x

0.14 per egg

=

$ 0.28

Oil

1/3 cup

x

0.21 per cup

=

$ 0.07

Packaging

1 pkg.

x

0.60 per pkg.

=

$ 0.60

Total direct materials

$ 2.68

Direct labor

1/6 hour

x

9.00 per hour

=

$ 1.50

Bakery overhead

½ hour

x

5.00 per hour

=

$ 2.50

Total

$ 6.68

Req. 2

The gross profit per pan of gourmet bars is $6.32.

Req. 3

Rachel should reassess standard prices quite often, since the price of ingredients changes quite frequently. She should

also reassess her price standards if she finds cheaper suppliers for her ingredients.

However, she really won’t need to reassess her quantity standards for the direct materials unless she changes the

recipe. On the other hand, she should reassess her quantity standard for overhead if she decides to bake more than

one batch at a time in the oven.

(10-15 min.) E11-33B

Standard cost of one pot:

DM (15 lbs x $5.00)

$75.00

DL (2 hr x $13.00)

$26.00

Var MOH (2 hr x $6)

$12.00

Fix MOH (2 hr x $7)

$ 14.00

Standard cost

$127.00

Managerial Accounting 4e Solutions Manual

(10-15 min.) E11-37B

Req. 1

(

Actual price per unit

– Stand. price per unit

)

x

Actual quantity of input

=

Price variance

( $0.75 – 0.85 )

x

98,000

=

$9,800 F

(

Actual quantity of input

– Stand. quantity of input

)

x

Standard price per input

unit

=

Quantity

variance

( 98,000 – 94,000 )

x

$0.85

=

$3,400 U

Req. 2

One plausible explanation is that Roger bought lower grade potatoes at a cheaper price, which resulted in the

favorable price variance. However, because the potatoes were lower grade, some of the potatoes were bad, and could

not be used in production. As a result, the manufacturing facility had to use more potatoes than standards allow. This

accounts for the unfavorable efficiency variance.

Req. 3

Price variance (2,100 x ($12.35 – $12.15)) =

$420 U

Quantity variance ($12.15 x (2,100 – 2,000)) =

$1,215 U

Req. 4

The unfavorable labor rate and efficiency variances could be tied to the material variances. For example, if the material

variances were the result of purchasing lower grade potatoes, then the factory would use more labor in sorting the

potatoes. As a result, they would have had to pay workers an overtime premium.

(15-20 min.) E11-38B

(

Actual price per unit

– Stand. price per unit

)

x

Actual quantity of input

=

Price variance

DM

( $1.15 – 1.30 )

x

1,060,000

=

$159,000 F

DL

( $15.00 – 14.00 )

x

4,200

=

$4,200 U

(

Actual quantity of input

– Stand. quantity of input

)

x

Standard price per input

unit

=

Efficiency variance

DM

( 1,060,000 – 960,000 )

x

1.30

=

$130,000 U

DL

( 4,200 – 4,480 )

x

14.00

=

$3,920 F

The favorable direct materials price variance combined with the unfavorable direct labor efficiency variance suggests

that managers may have used lower quality materials. The net effect is favorable.

The unfavorable direct labor rate variance combined with the favorable direct labor efficiency variance suggests that

managers may have used higher paid workers who performed more efficiently. The net effect is unfavorable.