Chapter 10 Performance Evaluation

(15-20 min.) E10-37B

Sweet Street Muffins

Flexible Budget Performance Report – Sales and Operating Expenses

For Year Ended December 31

Actual

Flexible

Budget

Variance

Flexible Budget

Volume

Variance

Master Budget

8,400 cases

8,400 cases

7,900 cases

Sales Revenue ($33 per case)

$ 284,800

$ 7,600F

$ 277,200

$ 16,500F

$ 260,700

Variable Operating Expenses:

Packaging Expense ($3 per case sold)

$ 26,100

$ 900U

$ 25,200

$ 1,500U

$ 23,700

Shipping Expense ($1.00 per case sold)

$ 8,900

$ 500U

$ 8,400

$ 500U

$ 7,900

Sales Commissions (2% of sales price)

$ 5,696

$ 152U

$ 5,544

$ 330U

$ 5,214

Fixed Operating Expenses:

Salaries

$ 7,700

$ 800U

$ 6,900

$ –

$ 6,900

Office Rent

$ 3,300

$ –

$ 3,300

$ –

$ 3,300

Depreciation

$ 3,000

$ –

$ 3,000

$ –

$ 3,000

Insurance Expense

$ 2,000

$ 300F

$ 2,300

$ –

$ 2,300

Office Supplies Expense

$ 1,300

$ 200U

$ 1,100

$ –

$ 1,100

Total Operating Expenses

$ 57,996

$ 2,252U

$ 55,744

$ 2,330U

$ 53,414

Operating Income

$ 226,804

$ 5,348F

$ 221,456

$ 14,170F

$ 207,286

Chapter 10 Performance Evaluation

(15-20 min.) E10-39B

a. Flexible budget variance

(15-20 min.) E10-40B

Jubilee Corporation

Balanced Scorecard Report

For Quarter Ended December 31

Perspective

Objective

KPI

Goal

Actual

Goal Achieved?

Financial

Gross margin growth percentage

Gross margin growth

percentage

27%

28%

Yes

Sales revenue Growth –Core

product line

Core product line

$2,300,000

$2,000,000

No

Customer

Number of repeat customers

Number of customers

100,000

103,000

Yes

Market share percentage

Percentage repeat

customers

18%

13%

No

Internal business process

Average repair time (number of

days)

Average repair time in

days

1.1 days

1.3 days

No

Number of new core products

Core products

15

19

Yes

Learning and growth

Employee training

Hours of employee

training

2,400

2,275

NO

Employee turnover rate

Employee turnover rate

5%

7%

No

Chapter 10 Performance Evaluation

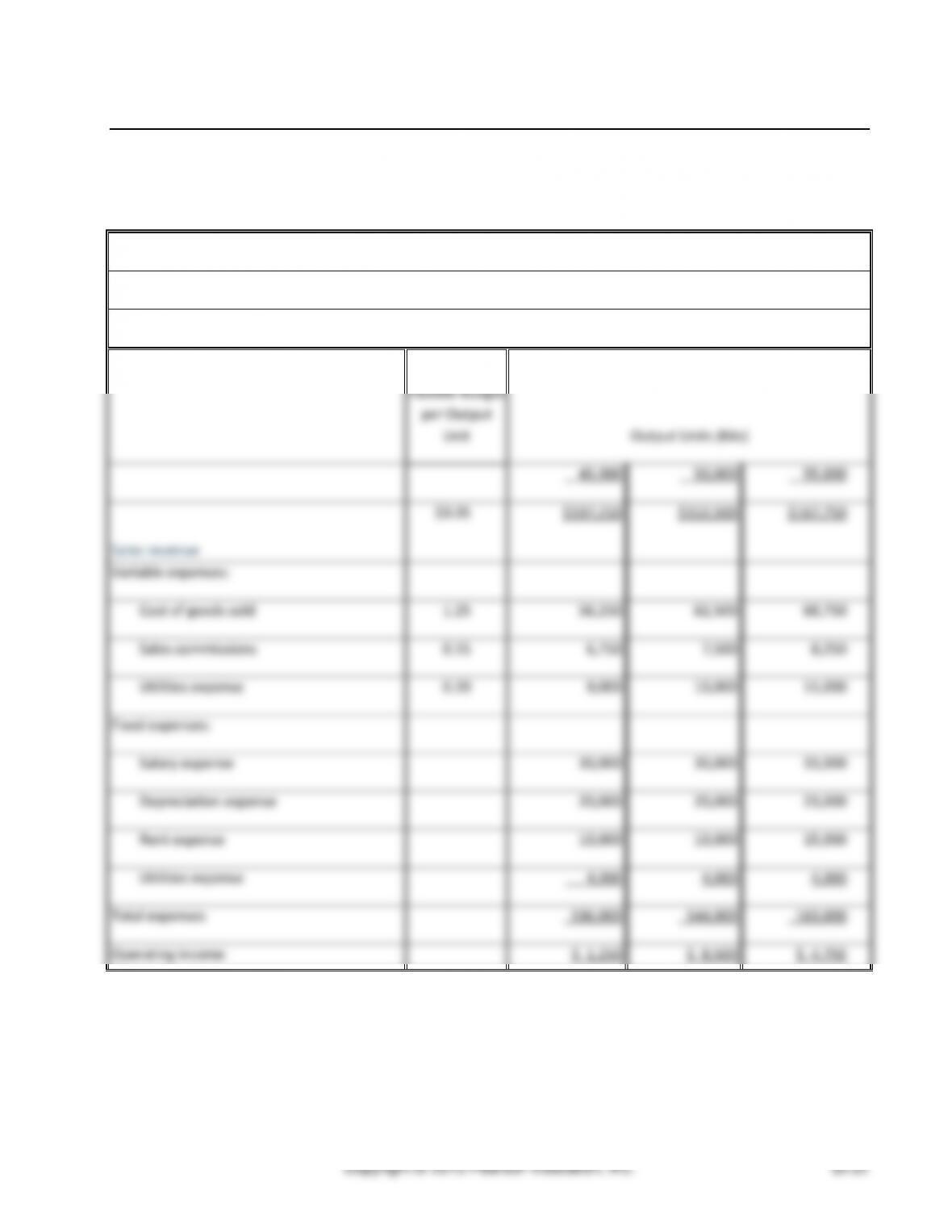

Problems (Group A)

(20-25 min.) P10-42A

Req. 1

Lively Bubbles, Inc.

Flexible Budget Income Statement

Month Ended July 31

Flexible Budget

per Output

Unit

Output Units (Kits)

45,000

50,000

55,000

Sales revenue

$3.05

$137,250

$152,500

$167,750

Variable expenses:

Cost of goods sold

1.25

56,250

62,500

68,750

Sales commissions

0.15

6,750

7,500

8,250

Utilities expense

0.20

9,000

10,000

11,000

Fixed expenses:

Salary expense

30,000

30,000

33,000

Depreciation expense

20,000

20,000

23,000

Rent expense

10,000

10,000

15,000

Utilities expense

4,000

4,000

4,000

Total expenses

136,000

144,000

163,000

Operating income

$ 1,250

$ 8,500

$ 4,750

Managerial Accounting 4e Solutions Manual

(continued) P10-42A

cost.

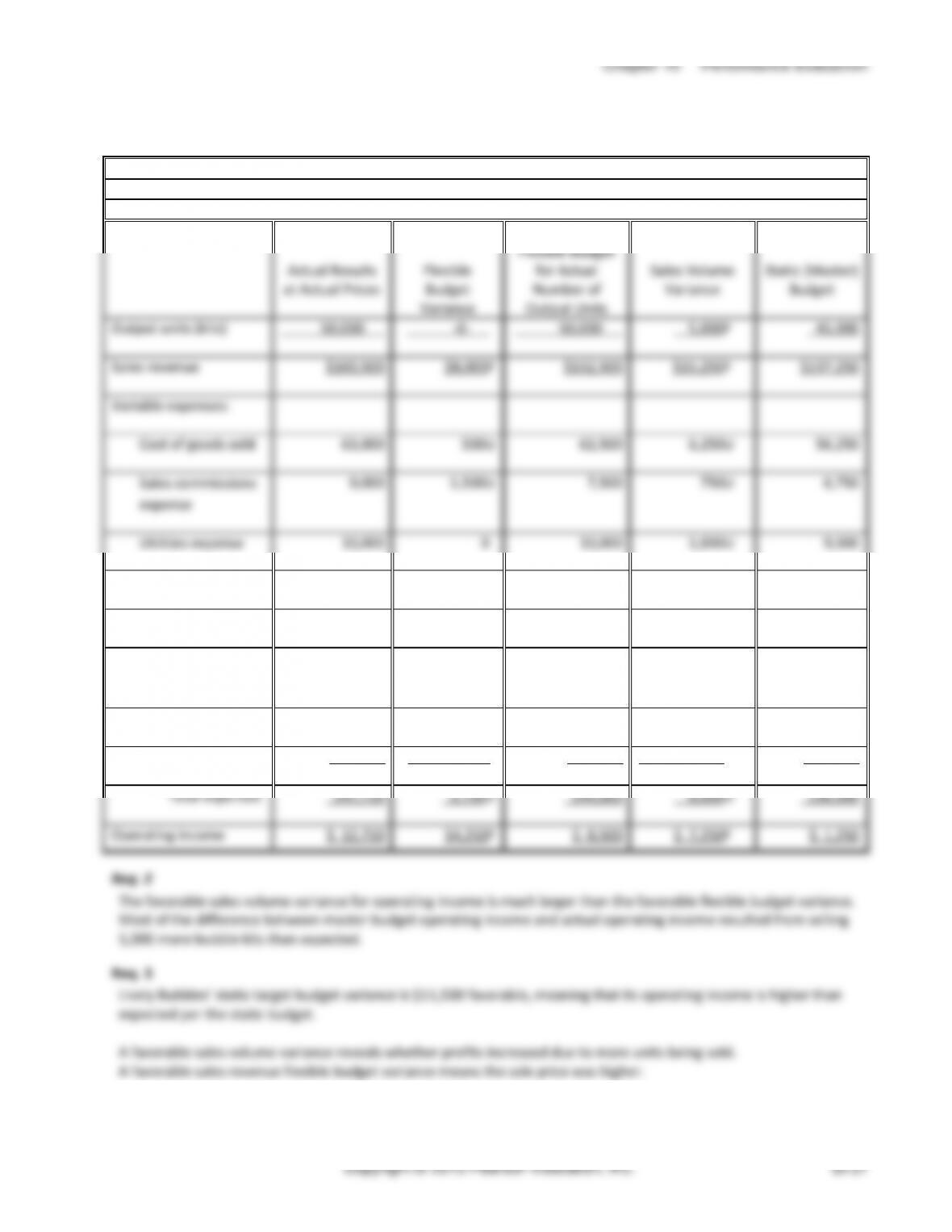

(15-20 min.) P10-43A

Req. 1

Lively Bubbles, Inc.

Income Statement Performance Report

Month Ended July 31

Actual Results

at Actual Prices

Flexible

Budget

Variance

Flexible Budget

for Actual

Number of

Output Units

Sales Volume

Variance

Static (Master)

Budget

Output units (kits)

50,000

-0-

50,000

5,000F

45,000

Sales revenue

$160,500

$8,000F

$152,500

$15,250F

$137,250

Variable expenses:

Cost of goods sold

63,000

500U

62,500

6,250U

56,250

Sales commissions

expense

9,000

1,500U

7,500

750U

6,750

Utilities expense

10,000

0

10,000

1,000U

9,000

Fixed expenses:

Salary expense

32,200

2,200U

30,000

0

30,000

Depreciation

expense

20,000

0

20,000

0

20,000

Rent expense

9,550

450F

10,000

0

10,000

Utilities expense

4,000

0

4,000

0

4,000

Total expenses

147,750

3,750U

144,000

8,000U

136,000

Operating income

$ 12,750

$4,250F

$ 8,500

$ 7,250F

$ 1,250

Req. 2

The favorable sales volume variance for operating income is much larger than the favorable flexible budget variance.

Most of the difference between master budget operating income and actual operating income resulted from selling

5,000 more bubble kits than expected.

Req. 3

Lively Bubbles’ static target budget variance is $11,500 favorable, meaning that its operating income is higher than

expected per the static budget.

A favorable sales volume variance reveals whether profits increased due to more units being sold.

A favorable sales revenue flexible budget variance means the sale price was higher.

Managerial Accounting 4e Solutions Manual

(15-20 min.) P10-44A

Req. 1

Paint Stores

Consumer

Operating income

$ 440,000

$ 148,200

÷ Total assets

÷$1,250,000

÷$1,425,000

Return on investment

35.2%

10.4%

Req. 2

Paint Stores

Consumer

Operating income

$ 440,000

$ 148,200

÷ Sales

÷$4,000,000

÷$1,140,000

Sales margin

11%

13%

The Consumer Division is more profitable on each dollar of sales.

Req. 3

Paint Stores

Consumer

Sales

$4,000,000

$1,140,000

÷ Total assets

÷$1,250,000

÷$1,425,000

Capital turnover

3.2 times

0.8 times

The Paint Stores Division is more efficient in generating sales with its assets.

Req. 4

Paint Stores

Consumer

Sales margin

11%

13%

× Capital turnover

×3.2

×0.8

ROI

35.2%

10.4%

The Consumer Division’s profitability on each dollar of sales is higher than the Paint Stores Divisions’ profitability.

However, the Paint Stores Division’s efficiency is significantly higher than the Consumer Division’s efficiency. These

results cause the Paint Stores Division’s ROI to be higher than the Consumer Division’s ROI.

Req. 5

RI = Operating income − Minimum acceptable income

= Operating income − (Target rate of return × Total assets)

Paint Stores RI = $440,000 − ($1,250,000 × 21%) = $177,500

Consumer RI = $148,200 − ($1,425,000 × 21%) = $(151,050)

Only the Paint Stores Division is meeting management’s target rate of return. The Consumer Division should work on

improving its capital turnover rate. Improving the capital turnover rate may help the division achieve positive residual

income.

Req. 6

Most companies use the average asset balance since the income used in the ROI calculation is earned over the course

Chapter 10 Performance Evaluation

(continued) P10-44A

Req. 7

Risk level of the division’s business

assets.

Chapter 10 Performance Evaluation

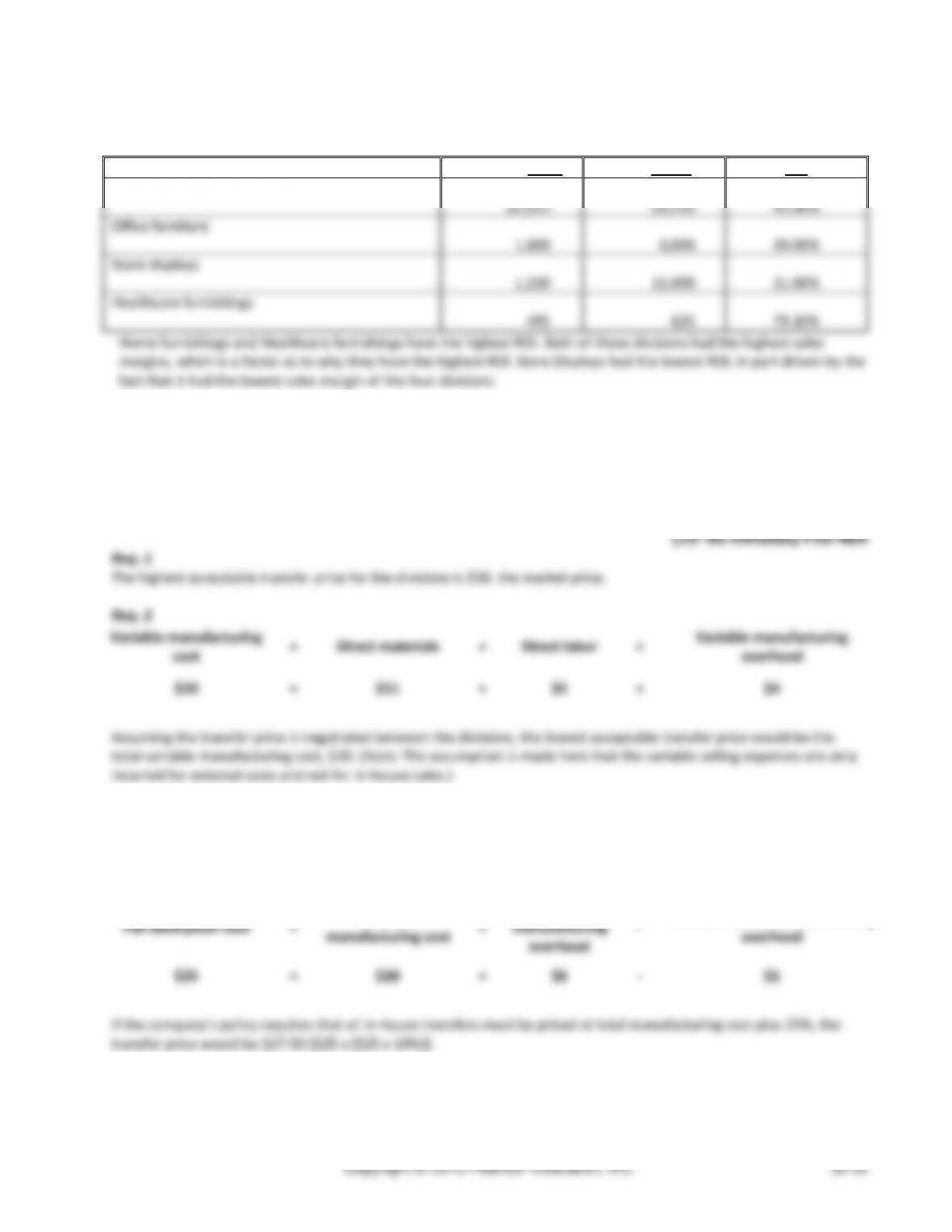

(continued) P10-45A

Req. 4

(Millions of dollars)

Operating Profit

Total Assets

ROI

Home furnishings

$2,625

$6,250

42.00%

Office furniture

1,800

6,000

30.00%

Store displays

1,210

11,000

11.00%

Healthcare furnishings

495

625

79.20%

Home furnishings and Healthcare furnishings have the highest ROI. Both of these divisions had the highest sales

margins, which is a factor as to why they have the highest ROI. Store Displays had the lowest ROI, in part driven by the

fact that it had the lowest sales margin of the four divisions.

Req. 5

Financial reporting is for the benefit of external users, not internal management. Therefore, not all company

information is disclosed in the financial statements. Residual income (RI) calculations involve management’s target rate

of return. Since this information is not presented, residual income cannot be calculated by an external user without

making an assumption about the rate.

$20

=

$11

+

$5

$4

Req. 3

The manager of the Small Components Division would prefer the $30 transfer price. The manager of the Computer

Division would prefer the $20 transfer price.

Req. 4

Full absorption cost

=

Variable

manufacturing cost

+

Fixed

manufacturing

overhead

–

Decrease in fixed manufacturing

overhead

$25

=

$20

+

$6

–

$1

If the company’s policy requires that all in-house transfers must be priced at total manufacturing cost plus 25%, the

transfer price would be $27.50 [$25 x ($25 x 10%)].

Managerial Accounting 4e Solutions Manual

(continued) P10-46A

Req. 5

Chapter 10 Performance Evaluation

(15-20 min.) P10-47A

Req. 1

Sports–Subunit X

Actual

Flexible Budget

Flexible Budget

Percent

Variance

Variance*

(U or F)

Sales

$545,500

$500,000

$45,500

F

9.10%

F

Cost of goods sold

387,000

375,000

12,000

U

3.20%

U

Gross margin

158,500

125,000

33,500

F

26.80%

F

Operating expenses

10,380

10,000

380

U

3.80%

U

Operating income before

Common fixed expenses

148,120

115,000

33,120

F

28.80%

F

Common fixed expenses

(allocated)

52,000

40,000

12,000

U

30.00%

U

Operating income

$96,120

$75,000

$21,120

F

28.16%

F

Req. 3

Service department charges

Req. 4

Managers should investigate favorable as well as unfavorable variances. Favorable variances may be due to

bookkeeping or budgeting errors. Management needs to evaluate large favorable as well as unfavorable variances to

Managerial Accounting 4e Solutions Manual

(continued) P10-47A

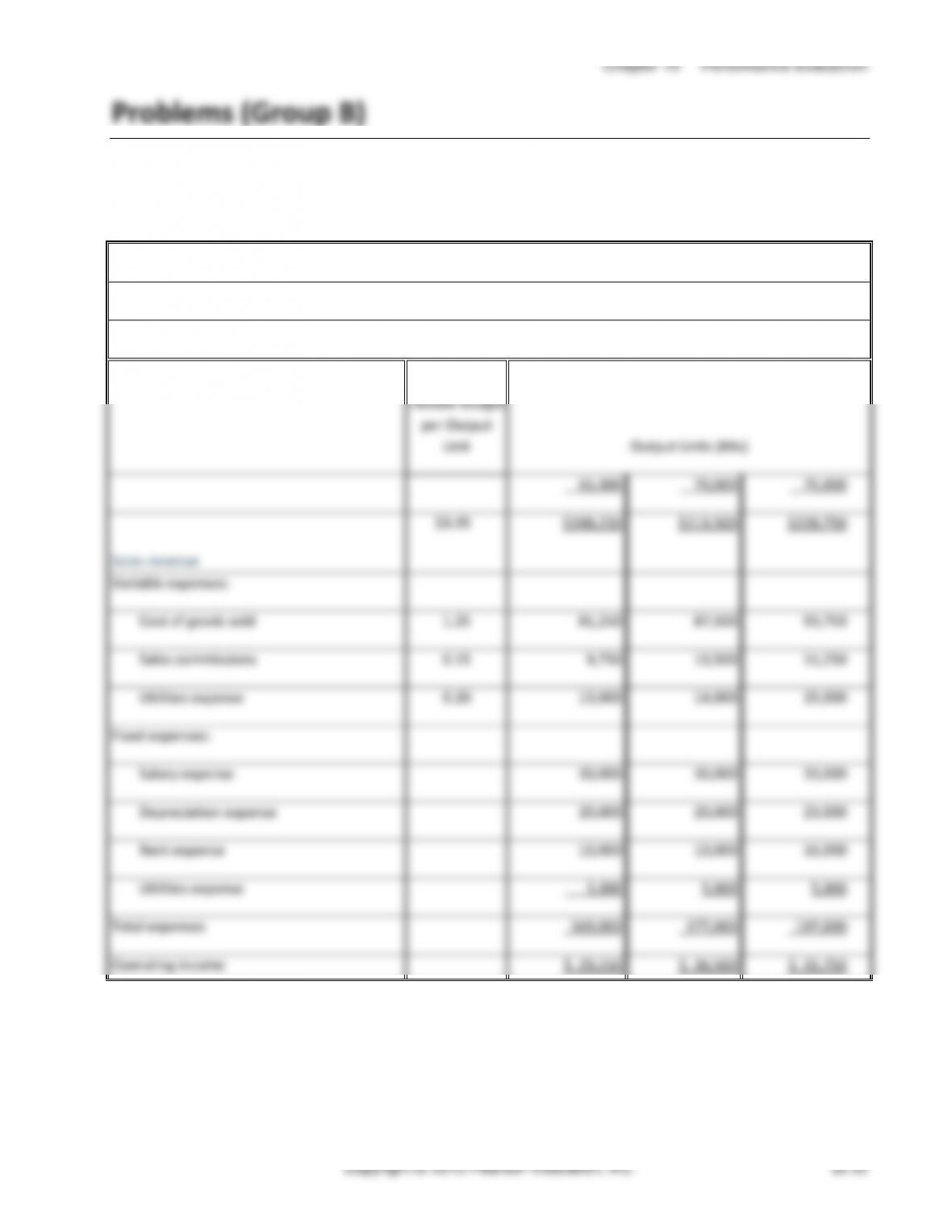

(20-25 min.) P10-48B

Req. 1

Precious Bubbles, Inc.

Flexible Budget Income Statement

Month Ended March 31

Flexible Budget

per Output

Unit

Output Units (Kits)

65,000

70,000

75,000

Sales revenue

$3.05

$198,250

$213,500

$228,750

Variable expenses:

Cost of goods sold

1.25

81,250

87,500

93,750

Sales commissions

0.15

9,750

10,500

11,250

Utilities expense

0.20

13,000

14,000

15,000

Fixed expenses:

Salary expense

30,000

30,000

33,000

Depreciation expense

20,000

20,000

23,000

Rent expense

10,000

10,000

16,000

Utilities expense

5,000

5,000

5,000

Total expenses

169,000

177,000

197,000

Operating income

$ 29,250

$ 36,500

$ 31,750

Managerial Accounting 4e Solutions Manual

(continued) P10-48B

cost.