Chapter 10 Performance Evaluation

Copyright © 2015 Pearson Education, Inc.

10-1

Chapter 10

Performance Evaluation

Quick Check

Answers:

QC-1. d

QC-3. c

QC-5. b

QC-7. a

QC-9. c

QC-2. b

QC-4. c

QC-6. d

QC-8. b

QC-10. d

Short Exercises

(5 min.) S10-1

a. An investment center

b. A cost center

Managerial Accounting 4e Solutions Manual

(5 – 10 min.) S10-4

Cost center 1. Manager of the Housekeeping Department at the Holiday Inn

Investment center 2. Manager of the Holiday Inn Express corporate division

(10 min.) S10-6

Sales

margin

Capital

turnover

ROI

Functional Ingredients

26.0%

2.20

57.20%

Consumer Markets

12.5%

2.00

25.00%

Performance Materials

26.0%

1.00

26.00%

ROI 26.0% x 2.2 = 57.20%

ROI 12.5% x 2.0 = 25.0%

ROI 26.0% x 1.0 = 26.0%

(10 min.) S10-7

1. Enter the formula, then calculate each division’s ROI.

Operating Income

÷

Total Assets

=

ROI

Snow Sports

$ 950,000

÷

$ 4,900,000

=

19.4 %

Non-Snow Sports

$ 1,482,000

÷

$ 7,100,000

=

20.9 %

3. Can you explain why one division’s ROI is higher?

Managerial Accounting 4e Solutions Manual

(10 – 15 min.) S10-8

Req. 1

Snow Sports

Non-snow Sports

Operating income

$950,000

$1,482,000

÷ Sales

÷$5,000,000

÷$7,800,000

Sales margin

19%

19%

Based on the divisions’ sales margins, we know that the sales margin was not the reason the divisions had different

ROIs.

Req. 2

Snow Sports

Non-snow Sports

Sales

$5,000,000

$7,800,000

÷ Total assets

÷$4,900,000

÷$7,100,000

Capital turnover

1.02

1.10

Based on the divisions’ capital turnover rates, we know that the capital turnover rate was the reason that the divisions

had different ROIs.

Req. 3

Snow Sports

Non-snow Sports

Sales margin (from S10-7)

19%

19%

× Capital turnover (from part 1)

×1.02

×1.10

ROI

19.4%

20.9%

Chapter 10 Performance Evaluation

(10 – 15 min.) S10-11

2. The actual results indicate that the company sold 5 pools in April.

3. The flexible budget for performance reports is always based on the actual output for the month. This is done so

pools.

5. The budgeted variable cost is $11,600 per pool.

6. As the name suggests, the flexible budget variance is the difference between the flexible budget and the actual

7. The volume variance is the difference between the static (master) budget and the flexible budget. As the name

8. See completed Performance Report below.

Golden Pools

Income Statement Performance Report

Year Ended April 30

Actual results at

actual prices

Flexible

budget

variance

Flexible budget

for actual

number of

output units

Volume

variance

Master

budget

Output units

5

0

6

1

5

Sales revenue

$ 115,000

$ 6,000

U

$ 121,000

$ 24,200

F

$ 96,800

Variable expenses

55,000

3,000

F

58,000

11,600

U

46,400

Fixed expenses

25,000

4,000

F

29,000

0

29,000

Total expenses

$ 80,000

$ 7,000

F

$ 87,000

$ 11,600

U

$ 75,400

Managerial Accounting 4e Solutions Manual

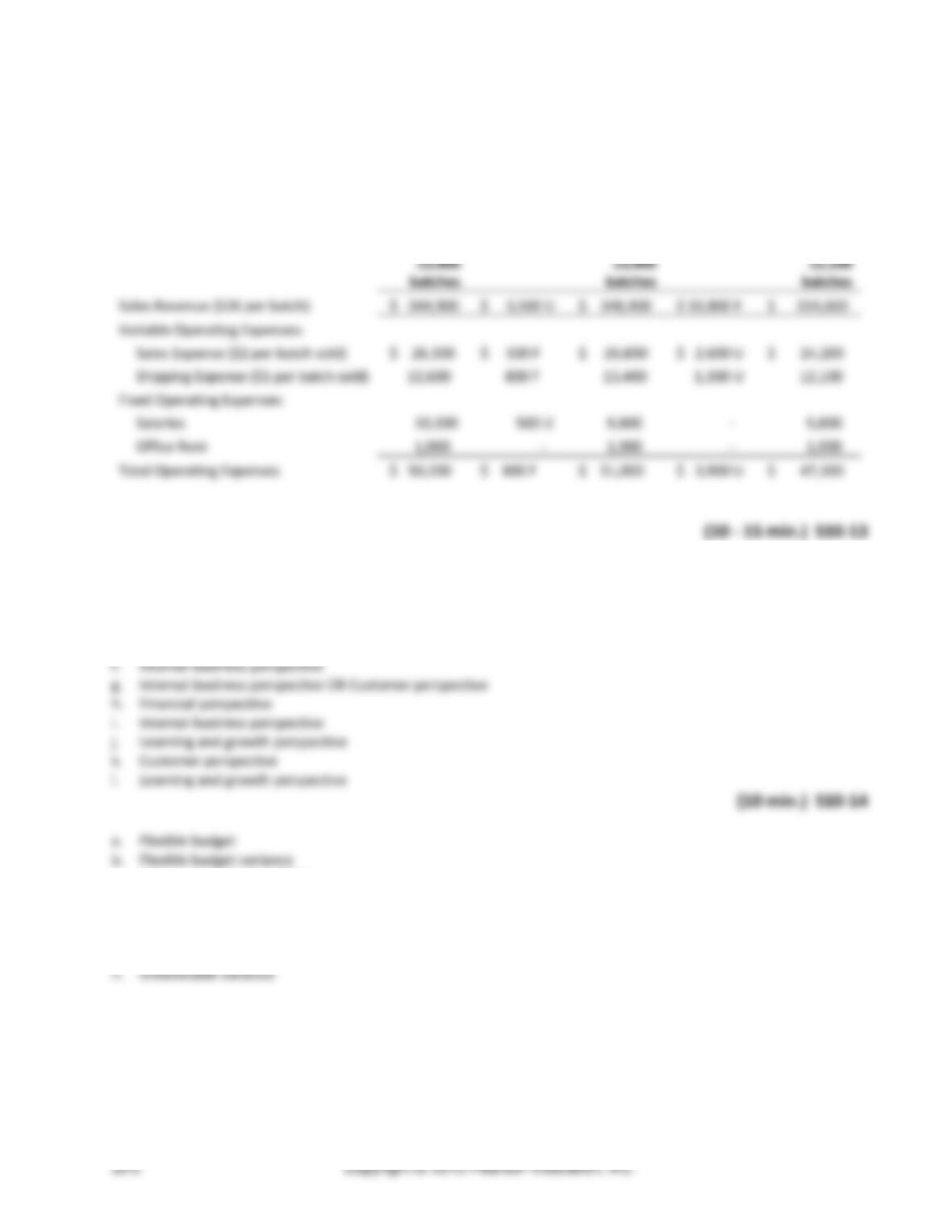

(10 -15 min.) S10-12

Sweet Earth Organic Chocolates

Master Budget Performance Report – Sales and Operating Expenses

For Year Ended December 31

Actual

Flexible

Budget

Variance

Flexible

Budget

Volume

Variance

Master

Budget

13,400

batches

13,400

batches

12,100

batches

Sales Revenue ($26 per batch)

$ 344,900

$ 3,500 U

$ 348,400

$ 33,800 F

$ 314,600

Variable Operating Expenses:

Sales Expense ($2 per batch sold)

$ 26,300

$ 500 F

$ 26,800

$ 2,600 U

$ 24,200

Shipping Expense ($1 per batch sold)

12,600

800 F

13,400

1,300 U

12,100

Fixed Operating Expenses:

Salaries

10,300

500 U

9,800

–

9,800

Office Rent

1,000

–

1,000

–

1,000

Total Operating Expenses

$ 50,200

$ 800 F

$ 51,000

$ 3,900 U

$ 47,100

(10 – 15 min.) S10-13

a. Financial perspective

b. Internal business perspective

c. Learning and growth perspective

d. Internal business perspective (post-sales service)

e. Customer perspective

c. Return on Investment (ROI)

d. Favorable variance

e. Revenue center

f. Volume variance

g. Capital turnover

Chapter 10 Performance Evaluation

(continued) S10-14

i. Management by exception

(10 min.) S10-15

1.

Benjamin, the controller at Bristal Industries, does not

inform management that his sister is the principal

partner in a consulting firm that is bidding on work at

Bristal Industries.

Integrity – Mitigate actual conflicts of interest,

regularly communicate with business associates

to avoid apparent conflicts of interest. Advise all

parties of any potential conflicts.

2.

Each month Jenna, a corporate controller, prepares

segment reports for all of the divisions of her company.

In these reports, she includes every general ledger

account. As a result, the report for each division is

several pages long and no one except Jenna and her

staff can interpret the reports.

Competence – Provide decision support

information and recommendations that are

accurate, clear, concise, and timely.

3.

In the past six years since he graduated with an

accounting degree, Joe has not attended any

continuing education seminars. He has figured that he

knows enough to do his job since he has not forgotten

any relevant information from his college degree

program.

Competence – Maintain an appropriate level of

professional expertise by continually developing

knowledge and skills.

4.

In casual conversation with friends on a Friday night,

Loren talks about how transfer prices are set at the

company where he is an accountant. As part of that

conversation, he shares the variable costs of the

company’s main product.

Confidentiality – Keep information confidential

except when disclosure is authorized or legally

required.

5.

In the year end report to the Board of Directors,

Samuel, the controller, prepares the performance

report for the board of directors. The board will base

the annual bonuses on this report. Samuel designs the

report so that the favorable KPIs are displayed

prominently, while the KPIs that are unfavorable are

either not included or are buried deep in the later

pages of the report so that they are unlikely to be seen.

Credibility – Communicate information fairly

and objectively.

Managerial Accounting 4e Solutions Manual

Exercises (Group A)

(5 – 10 min.) E10-16A

a. Investment

b. Profit

Chapter 10 Performance Evaluation

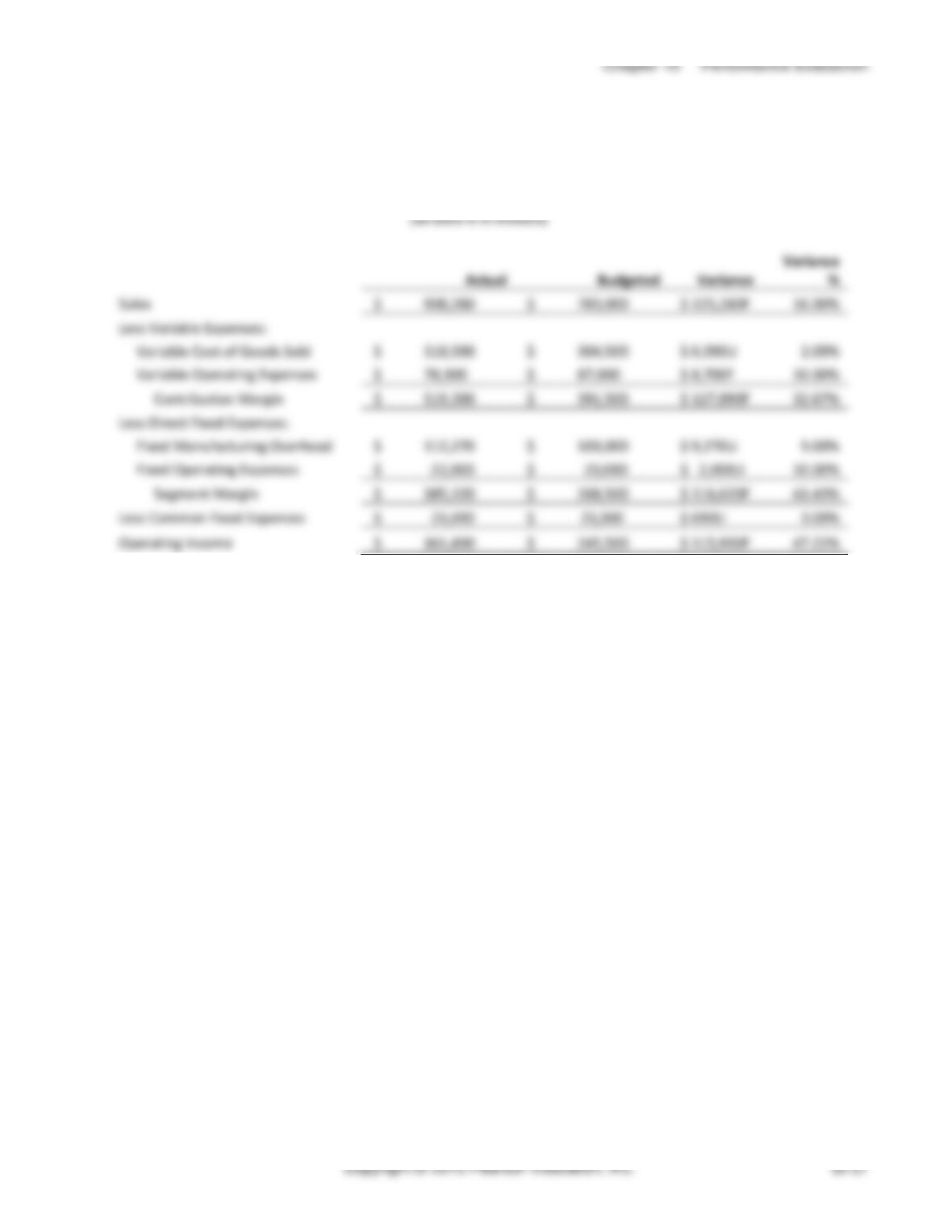

(15 min.) E10-18A

Performance Report

Crandell Industries – Pharmaceutical Segment

For Fiscal Year Ending December 31

(all data is in millions)

Actual

Budgeted

Variance

Variance %

Sales

$1,436,400

$ 1,260,000

$ 176,400F

14.00%

Less Variable Expenses:

Variable Cost of Goods Sold

$192,600

$ 180,000

$ 12,600U

7.00%

Variable Operating Expenses

121,500

$ 135,000

$ 13,500F

10.00%

Contribution Margin

$1,122,300

$ 945,000

$ 177,300F

18.76%

Less Direct Fixed Expenses:

Fixed Manufacturing

Overhead

$117,700

$ 107,000

$ 10,700U

10.00%

Fixed Operating Expenses

16,160

$ 16,000

$ 160U

1.00%

Segment Margin

988,440

$ 822,000

$ 166,440F

20.25%

Less Common Fixed Expenses

17,170

$ 17,000

$ 170U

1.00%

Operating Income

$971,270

$ 805,000

$ 166,270F

20.65%

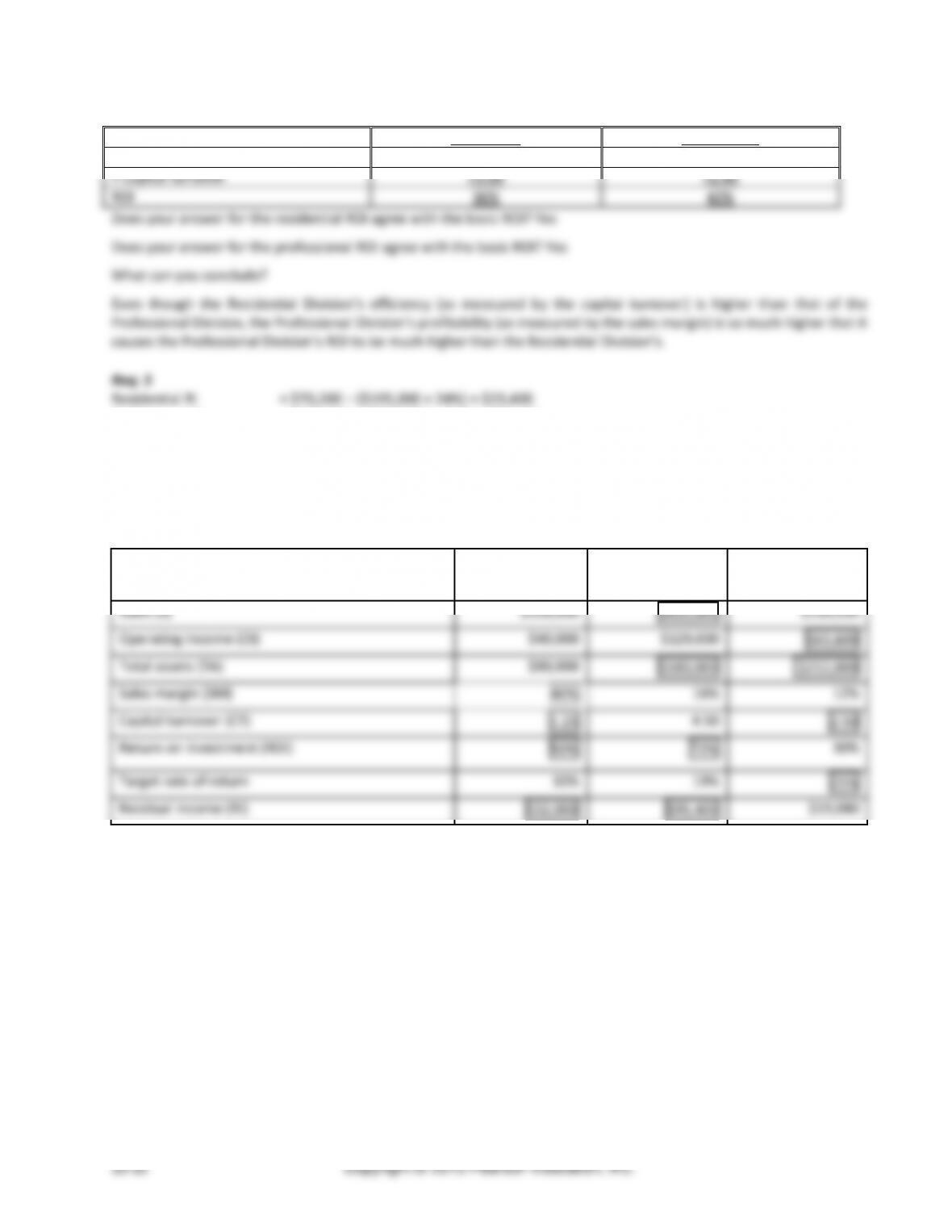

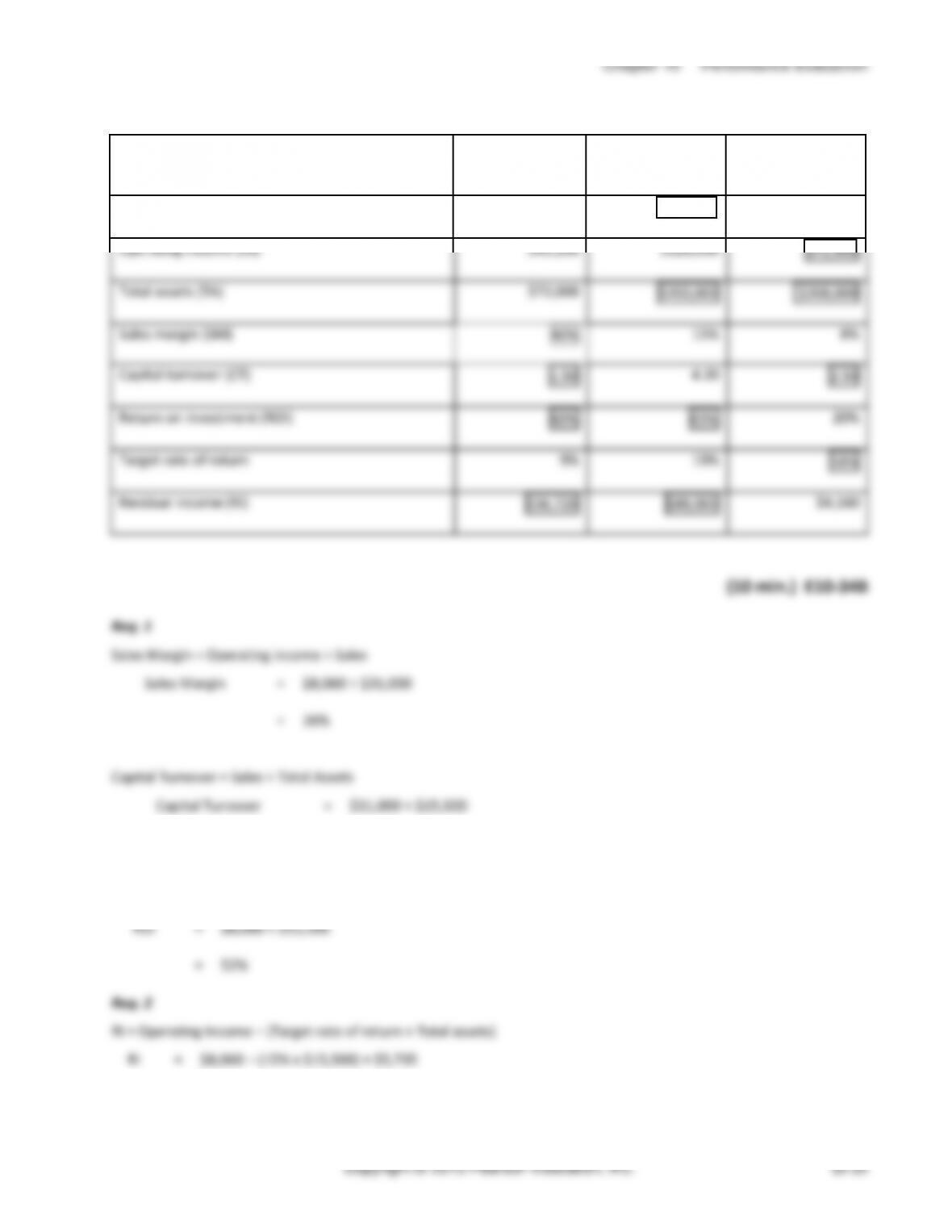

Residential

Professional

Operating income

$ 70,200

$152,040

÷ Total assets

÷$195,000

÷$362,000

Return on investment

36%

42%

Each division’s ROI is very high; however, the Professional Division has an even higher ROI than the Residential Division.

Req. 2

Residential

Professional

Operating income

$ 70,200

$152,040

÷ Sales

÷$585,000

÷$1,013,600

Sales margin

12%

15%

The Professional Division is earning about $0.15 on each dollar of sales whereas the Residential Division is only earning

about $0.12 on each dollar of sales. The Professional Division’s higher sales margin helps to account for its higher ROI.

Req. 3

Residential

Professional

Sales

$585,000

$1,013,600

÷ Total assets

÷$195,000

÷$ 362,000

Capital turnover

3.00

2.80

The Professional Division is generating $2.80 of sales for every dollar of assets invested in the division. The Residential

Division is generating $3.00 of sales for every dollar of assets invested. The Residential Division is even more efficient.

Managerial Accounting 4e Solutions Manual

(continued) E10-19A

Req. 4

Residential

Professional

Sales margin

12%

15%

× Capital turnover

×3.00

×2.80

ROI

36%

42%

Professional RI = $152,040 − ($362,000 × 24%) = $65,160

Both divisions are exceeding management’s expectations.

(10 – 15 min.) E10-20A

Kyler Company

Fielding Industries

Johnson, Inc.

Sales (S)

$100,000

$810,000

$530,000

Operating income (OI)

$40,000

$129,600

$63,600

Total assets (TA)

$80,000

$180,000

$212,000

Sales margin (SM)

40%

16%

12%

Capital turnover (CT)

1.25

4.50

2.50

Return on investment (ROI)

50%

72%

30%

Target rate of return

10%

19%

21%

Residual income (RI)

$32,000

$95,400

$19,080

(10 min.) E10-21A

Req. 1

Sales Margin

=

$7,560 ÷ $27,000

=

28%

=

$27,000 ÷ $12,000

=

2.25 times

=

$7,560 ÷ $12,000

=

63%

Managerial Accounting 4e Solutions Manual

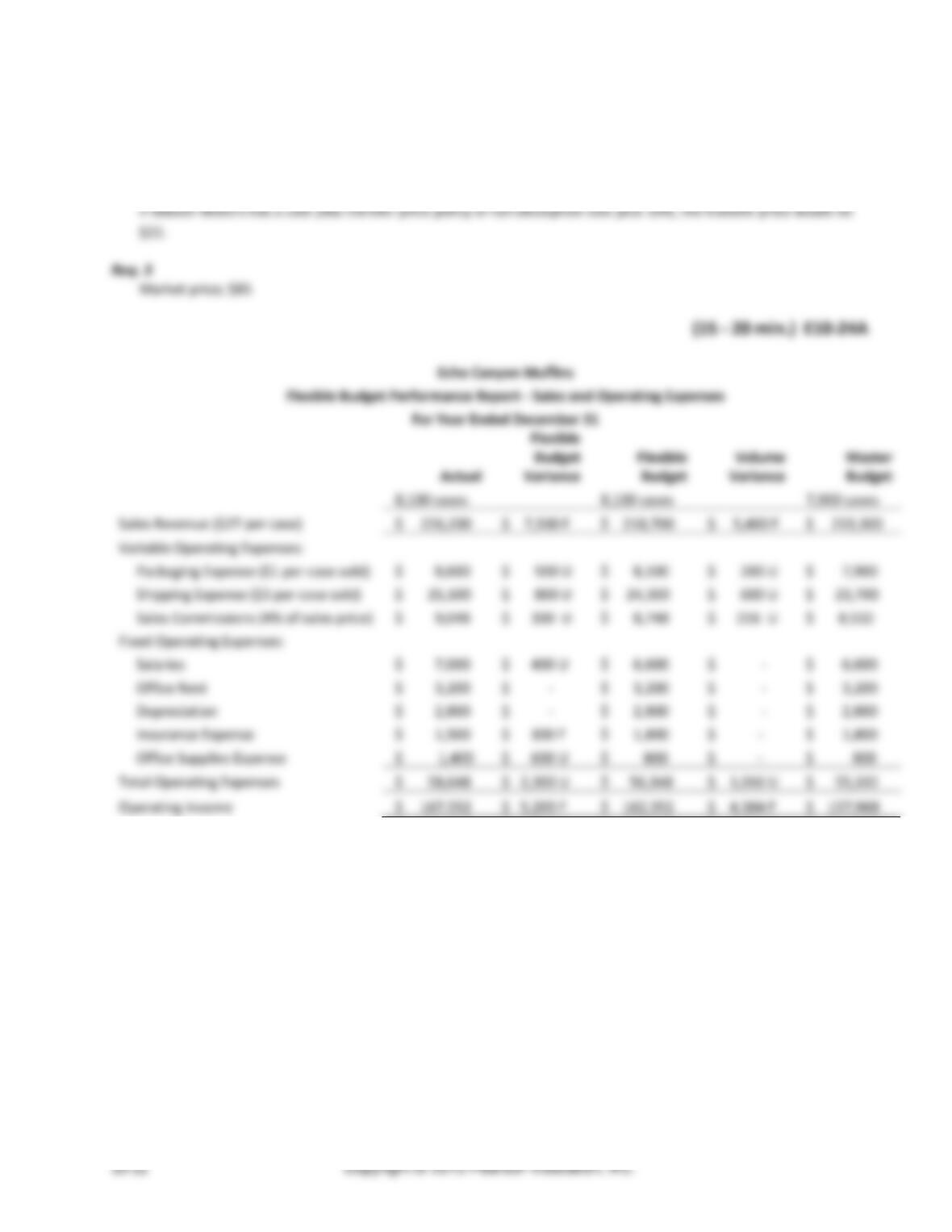

(10 min.) E10-23A

Req. 1

Lowest – Variable cost of $18 ($17 + $1.) Highest – Market price of $85

Req. 2

Chapter 10 Performance Evaluation

(15-20 min.) E10-25A

Req. 1

Ski Products-Subunit X

Revenue by Product

Actual

Flexible

Budget

Variance

Flexible Budget

Sales Volume

Variance

Static

(Master)

Budget

Downhill—

Model RI

$ 320,000

$ 8,000 (F)

$ 312,000

$18,000 (F)

$ 294,000

Downhill—

Model RII

152,000

11,000 (U)

163,000

20,000 (F)

143,000

Cross-Country—

Model EXI

290,000

1,000 (U)

291,000

19,000 (U)

310,000

Cross-Country—

Model EXII

253,000

6,000 (F)

247,000

18,500 (U)

265,500

Snowboard—

Model LXI

430,000

4,000 (F)

426,000

18,000 (F)

408,000

Total

$1,445,000

$ 6,000 (F)

$1,439,000

$18,500 (F)

$1,420,500

Req. 2

This subunit is a revenue center.

Req. 3

The sales volume variance is always due strictly to volume — therefore, the number of units sold was different than

budgeted for every model. The company sales mix appears to be shifting in the direction of downhill ski and snowboard

Managerial Accounting 4e Solutions Manual

(15 – 20 min.) E10-27A

Mancato Corporation

Balanced Scorecard Report

For Quarter Ended December 31

Perspective

Objective

KPI

Goal

Actual

Goal Achieved?

Financial

Increase profitability of core

product line

Core product line profit as %

of core product line sales

22%

25%

√

Increase sales of core product line

Sales revenue growth

2,000,000

2,250,000

√

Customer

Increase market share

Market Share %

13%

20%

√

Number of Customers

130,000

125,000

Internal business process

Improve post-sales service

Average repair time (# of

days)

1.7

1.1

√

Safety

Number of Plant Accidents

4.0

3.0

√

Learning and growth

Improve employee job satisfaction

Employee Turnover rate

7%

9%

Improve employee product

knowledge

Employee training hours

2,425

2,250

Chapter 10 Performance Evaluation

(15 – 20 min.) E10-28A

a. Financial

b. Internal business

c. Learning and growth

Managerial Accounting 4e Solutions Manual

Exercises (Group B)

(5 – 10 min.) E10-29B

a. Profit

b. Cost

c. Revenue

d. Cost

(15 min.) E10-31B

Performance Report

Clayton Industries – Pharmaceutical Segment

For Fiscal Year Ending December 31

(all data is in millions)

Actual

Budgeted

Variance

Variance

%

Sales

$ 908,280

$ 783,000

$ 125,280F

16.00%

Less Variable Expenses:

Variable Cost of Goods Sold

$ 310,590

$ 304,500

$ 6,090U

2.00%

Variable Operating Expenses

$ 78,300

$ 87,000

$ 8,700F

10.00%

Contribution Margin

$ 519,390

$ 391,500

$ 127,890F

32.67%

Less Direct Fixed Expenses:

Fixed Manufacturing Overhead

$ 112,270

$ 103,000

$ 9,270U

9.00%

Fixed Operating Expenses

$ 22,000

$ 20,000

$ 2,000U

10.00%

Segment Margin

$ 385,120

$ 268,500

$ 116,620F

43.43%

Less Common Fixed Expenses

$ 23,690

$ 23,000

$ 690U

3.00%

Operating Income

$ 361,430

$ 245,500

$ 115,930F

47.22%

Managerial Accounting 4e Solutions Manual

(10-15 min.) E10-32B

Req. 1

Residential

Professional

Operating income

$ 70,200

$152,040

÷ Total assets

÷$195,000

÷$362,000

Return on investment

36%

42%

Each division’s ROI is very high; however, the Professional Division has an even higher ROI (46%) than the Residential

Division.

Req. 2

Residential

Professional

Operating income

$ 70,200

$152,040

÷ Sales

÷$585,000

÷$1,013,600

Sales margin

12%

15%

The Professional Division is earning about $0.15 on each dollar of sales whereas the Residential Division is only earning

about $0.15 on each dollar of sales. The Professional Division’s higher sales margin helps to account for its higher ROI.

Req. 3

Residential

Professional

Sales

$585,000

$1,013,600

÷ Total assets

÷$195,000

÷$ 362,000

Capital turnover

3.00 times

2.80 times

Sales margin

× Capital turnover

ROI

(10 min.) E10-33B

Osborne

Company

Plumb Industries

Calloway Inc.

Sales (S)

$108,000

$840,000

$520,000

Operating income (OI)

$43,200

$126,000

$41,600

Total assets (TA)

$72,000

$200,000

$208,000

Sales margin (SM)

40%

15%

8%

Capital turnover (CT)

1.50

4.20

2.50

Return on investment (ROI)

60%

63%

20%

Target rate of return

9%

19%

18%

Residual income (RI)

$36,720

$88,000

$4,160

(10 min.) E10-34B

Req. 1

Sales Margin = Operating income ÷ Sales

Sales Margin

=

$8,060 ÷ $31,000

=

26%

Capital Turnover = Sales ÷ Total Assets

Capital Turnover

=

$31,000 ÷ $15,500

=

2.00 times

ROI = Operating income ÷ Total Assets

ROI

=

$8,060 ÷ $15,500

=

52%

Req. 2

RI = Operating Income − (Target rate of return × Total assets)

RI

=

$8,060 − (15% x $15,500) = $5,735

Managerial Accounting 4e Solutions Manual

(10-15 min.) E10-35B

Req. 1

The original return on investment (ROI) for the Cleary Ceramics division before the additional investment is 17.5%.

Req. 2

If this investment opportunity were undertaken the ROI would be 16.4%.

(10 min.) E10-36B

Req. 1