Chapter 1 Introduction to Managerial Accounting

Chapter 1

Introduction to Managerial Accounting

Quick Check

Answers:

Chapter 1 Introduction to Managerial Accounting

(5 min.) S1-6

a. The Institute of Management Accountants says that more accountants work in organizations rather than at

CPA firms.

(10 min.) S1-7

Each of the four ethical standards contributes to maintaining the IMA’s (and society’s) expectation that management

accountants will uphold the highest standards of ethical behavior.

COMPETENCE: Without the necessary competence, management accountants will be unable to perform their

responsibilities. Even if they do recognize an ethical dilemma, they could lack the competence required to determine all

the alternative courses of action and the implications of each alternative.

(5 min.) S1-8

a. Providing earnings information to your brother before it is publicly announced violates the confidentiality

standard.

Chapter 1 Introduction to Managerial Accounting

Exercises (Group A)

(10 min.) E1-12A

a. Managerial accounting systems report on various segments or business units of the company.

b. When managers evaluate the company’s performance compared to the plan, they are performing the

(10 min.) E1-13A

1. Financial accounting information

3. Both

5. Financial accounting information

7. Both

9. Financial accounting information

11. Financial accounting information

13. Financial accounting information

(10 min.) E1-14A

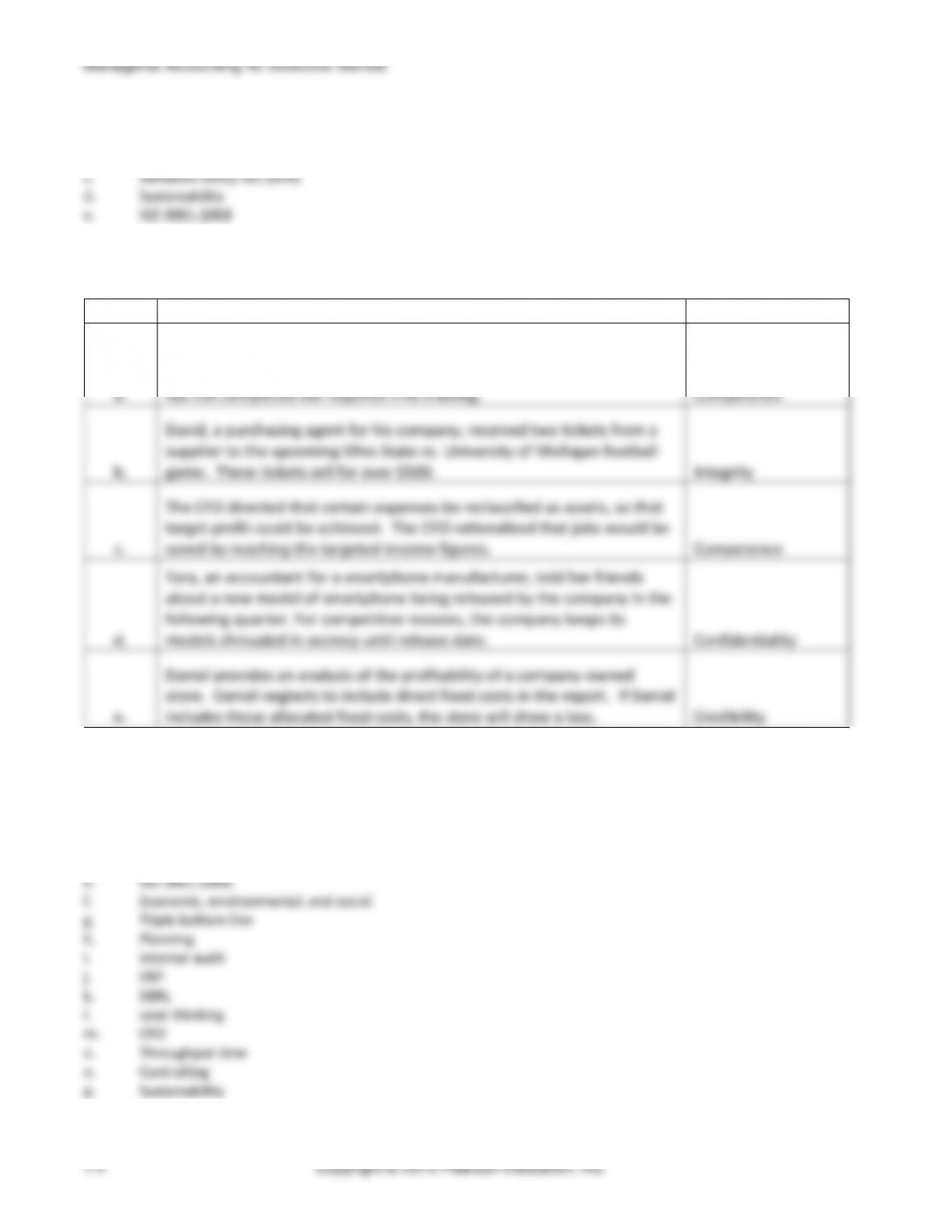

2. competence

4. credibility

6. integrity

8. competence

10. credibility

12. confidentiality

Managerial Accounting 4e Solutions Manual

(10 min.) E1-15A

Req. 1

Total costs of adopting lean production model:

Employee training…………..…………………..……………………..

$26,000

Streamline plant’s production process……………………….

68,000

Supplier identification………………………….………….…………

7,500

Total costs…………………………….…………………………………..

$101,500

Req. 2

Benefits of adopting lean production:

Savings in warehouse expenses……………………………..

$67,000

Lower spoilage costs……..…….…………..………….…………….

38,200

Total benefits…………..………………….…………………………

$105,200

Req. 3

Expected total benefits…………………….…………………….

$105,200

Expected total costs…………………..…….…………………….

(101,500)

Excess of benefits over costs…………………………..………….

$ 3,700

The company should adopt the lean production model because the expected benefits exceed the costs.

(10 min.) E1-16A

a. Social

b. Environmental

c. Economic

d. Social

e. Social

f. Environmental

g. Environmental

h. Social

i. Social

j. Economic

k. Environmental

l. Social

m. Environmental

Chapter 1 Introduction to Managerial Accounting

Exercises (Group B)

(5 min.) E1-17B

a. U.S. companies must follow GAAP or IFRS in their financial accounting systems.

(5-10 min.) E1–18B

1. Both

3. Financial accounting information

5. Financial accounting information

7. Financial accounting information

9. Financial accounting information

11. Both

13. Financial accounting information

(10 min.) E1-19B

2. competence

4. competence

6. credibility

8. competence

10. confidentiality

12. confidentiality

Managerial Accounting 4e Solutions Manual

(10 min.) E1-20B

Req. 1

Total costs of adopting lean production model:

Employee training………………………………………………………

$45,100

Streamline plant’s production process……………………….

35,000

Supplier identification………………………….…………………….

7,750

Total costs……….………………………………………………………..

$87,850

Savings in warehouse expenses……………………………..

$87,000

Lower spoilage costs………………………..………………….…....

35,200

Total benefits…………..………………….…………………………

$122,200

Req. 3

Expected total benefits…………………….……………………..

$122,200

Expected total costs……………………………………………….

(87,850)

Excess of benefits over costs………………..……………………

$ 34,350

The company should adopt the lean production model because the expected benefits are greater than the costs.

(10 min.) E1-21B

a. Environmental

b. Social

c. Environmental

d. Environmental

e. Economic

f. Social

g. Environmental

h. Environmental

i. Social

j. Environmental

k. Economic

l. Environmental

m. Environmental

Chapter 1 Introduction to Managerial Accounting

Problems (Group A)

(45-60 min.) P1-22A

Req. 1

Planning

Directing

Controlling

Sales

Increase Sales

Setting competitive prices

Examine sales reports

Monitor sales numbers and

prices from different products

and locations over time.

Investigate variances.

Repairs

Increase volume

of repairs

Streamline process to save time.

Set competitive prices; generate

reports showing time used for

each type of repair.

Track total number of repairs

and see if more repairs are

being made and if time is

utilized efficiently.

Customization

Increase number

of custom systems

built

Find out what customers want

and need. Observe competitors

for prices and options offered.

Improve employee certification

and offer higher-quality parts.

Examine number of computer

systems built per type

(multimedia, gaming, etc.).

Web

Development

Increase web

traffic

Improve design of web site.

Offer more products online.

Make shopping easier and more

intuitive. Increase marketing

efforts.

Monitor web traffic by having an

online counting device. Look at

sales numbers to see if people

are just surfing or actually

buying merchandise.

Accounting

Implement ERP

system to monitor

department

activities and

record finances

Train employees on new system.

Find potential flaws in the

system and fix before

implementation.

Track employee work schedules

to stay on time. Double check

entries to ensure system is

working properly.

Human

Resources

Decrease

employee

turnover

Hire employees that are “a good

fit” for the company.

Raise employee morale; set

clear job descriptions. Give

feedback to employees.

Monitor both involuntary and

voluntary turnover. Interview

employees to determine

potential problems with the

workplace.

Managerial Accounting 4e Solutions Manual

(continued) P1-22A

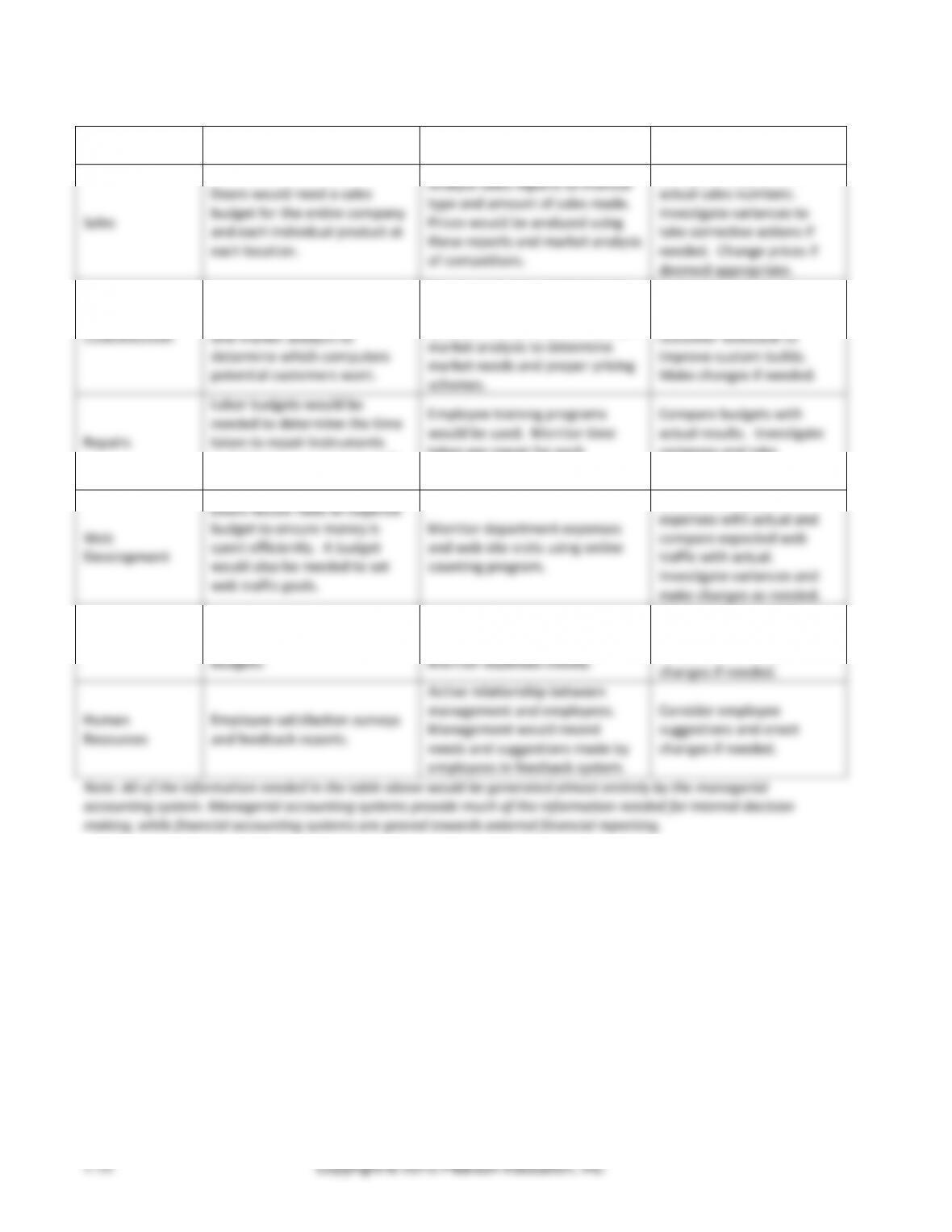

Req. 2

Planning

Directing

Controlling

Sales

Doors would need a sales

budget for the entire company

and each individual product at

each location.

Analyze sales reports to monitor

type and amount of sales made.

Prices would be analyzed using

these reports and market analysis

of competitors.

Compare budgets with

actual sales numbers.

Investigate variances to

take corrective actions if

needed. Change prices if

deemed appropriate.

Customization

Budgets for types of computers

offered, time needed per job,

and market analysis to

determine which computers

potential customers want.

Ensure customer satisfaction by

hiring qualified staff. Research

quality of available parts. Analyze

market analysis to determine

market needs and proper pricing

schemes.

Compare budgets with

actual results. Use

customer feedback to

improve custom builds.

Make changes if needed.

Repairs

Labor budgets would be

needed to determine the time

taken to repair instruments

and if hiring more repair staff

would be feasible.

Employee training programs

would be used. Monitor time

taken per repair for each

member of repair staff.

Compare budgets with

actual results. Investigate

variances and take

corrective action if needed.

Web

Development

Doors would need an expense

budget to ensure money is

spent efficiently. A budget

would also be needed to set

web traffic goals.

Monitor department expenses

and web site visits using online

counting program.

Compare budgeted

expenses with actual and

compare expected web

traffic with actual.

Investigate variances and

make changes as needed.

Accounting

Doors would need time

budgets as well as expense

budgets.

Train employees on new system

to keep within time budget.

Monitor expenses closely.

Compare budget with

actual numbers. Investigate

variances and make

changes if needed.

Human

Resources

Employee satisfaction surveys

and feedback reports.

Active relationship between

management and employees.

Management would record

needs and suggestions made by

employees in feedback system.

Consider employee

suggestions and enact

changes if needed.

Note: All of the information needed in the table above would be generated almost entirely by the managerial

accounting system. Managerial accounting systems provide much of the information needed for internal decision

making, while financial accounting systems are geared towards external financial reporting.

Chapter 1 Introduction to Managerial Accounting

(15-20 min.) P1-23A

a. If advertising is postponed, there is no transaction to record. This strategy is beyond the responsibility of the

controller, so it does not violate IMA standards.

b. The value of each individual sales return may not be material. However, even if each is small on an individual

Chapter 1 Introduction to Managerial Accounting

(10-15 min.) P1–25A

Costs:

Financial assistance to dealers………………………..

$ 740,000

Computer hardware upgrade………………………….

145,000

Software and consulting fees………………………..

215,000

Total costs…………………………………………………………

$1,100,000

Value of benefits (lower labor costs)………….………..

$1,430,000

Total costs………………………….………………………….…

(1,100,000)

Excess of benefits over costs……………………………

$ 330,000

Because the benefits exceed the costs, a cost-benefit analysis suggests that the company should proceed with the

Internet-based ordering system.

(20-25 min.) P1-26A

Req. 1

The expected value of the benefits is the labor cost savings of $928,000. This is a downward revision from what was

originally estimated in P1-25A.

Expected value of benefits……….………………………

Total costs (from P1–25A)……………………………….

Net cost………………….….…………………………………