Chapter 24

Hedging with Financial Derivatives

Hedging

Forward Markets

Interest-Rate Forward Contracts

The Practicing Manager: Hedging Interest-Rate Risk with Forward Contracts

Pros and Cons of Forward Contracts

Financial Futures Markets

Financial Futures Contracts

Following the Financial News: Financial Futures

The Practicing Manager: Hedging with Financial Futures

Organization of Trading in Financial Futures Markets

Globalization of Financial Futures Markets

Explaining the Success of Futures Markets

Mini-Case Box: The Hunt Brothers and the Silver Crash

The Practicing Manager: Hedging Foreign Exchange Risk with Forward and Futures Contracts

Hedging Foreign Exchange Risk with Forward Contracts

Hedging Foreign Exchange Risk with Futures Contracts

Stock Index Futures

Stock Index Futures Contracts

Mini-Case Box: Program Trading and Portfolio Insurance: Were They to Blame for the Stock

Market Crash of 1987?

Following the Financial News: Stock Index Futures

The Practicing Manager: Hedging with Stock Index Futures

Options

Option Contracts

Profits and Losses on Options and Futures Contracts

Factors Affecting the Prices of Option Premiums

Summary

The Practicing Manager: Hedging with Futures Options

Interest-Rate Swaps

Interest-Rate Swap Contracts

144 Mishkin/Eakins • Financial Markets and Institutions, Eighth Edition

The Practicing Manager: Hedging with Interest-Rate Swaps

Advantages of Interest-Rate Swaps

Disadvantages of Interest-Rate Swaps

Financial Intermediaries in Interest-Rate Swaps

Credit Derivatives

Credit Options

Credit Swaps

Credit-Linked Notes

Case: Lessons from the Subprime Financial Crisis: When Are Financial Derivatives Likely to

be a Worldwide Time Bomb?

◼ Overview and Teaching Tips

The treatment of financial derivatives markets (forwards, futures, options, and swaps) in this book differs

markedly from that in other financial markets and institutions books. Financial derivatives are approached

from the perspective of managers of financial institutions, and this is why this material is placed in the

management of financial institutions part of the book. Rather than go into a lot of facts about these different

markets, this chapter, which covers financial derivatives, focuses on how these markets work and how

they can be used to hedge the risk faced by financial institutions. This approach makes more sense to

students who now clearly see why studying these markets and their operation is relevant.

One problem that I have encountered in teaching students about financial derivatives is that many do not

find the financial derivative contracts to be particularly intuitive. In order to get them to understand how

these contracts work, I find that it helps to outline the basic principle of hedging: Hedging risk involves

engaging in a financial transaction that offsets a long position with a short position, or offsets a short

position with a long position. The chapter then uses this principle over and over again to demonstrate how

different types of contracts can be used to hedge risk. In addition, to hammer home how these contracts

work, this chapter contains several Practicing Manager applications which provide specific numerical

examples of how hedges are conducted with financial futures and forward contracts. I know of no other

financial markets and institutions textbook that takes as applied an approach to teaching students about

financial futures and forward contracts as I do in this book. My experience is that only with applications of

the type found in this chapter can students have any real understanding of what financial derivatives are all

about.

The Practicing Manager applications in this chapter are all self-contained and can be skipped without loss

of continuity. For example, if an instructor only wants to focus on hedging interest rate risk, then he or she

can easily skip the applications dealing with hedging stock market risk or foreign exchange rate risk.

Other financial markets and institutions textbooks tend to give only a cursory treatment of what profits arise

for a holder of an option contract given different market outcomes. They may have a figure illustrating

the profits, but do not give a detailed explanation of how profits are generated. I think that this is a terrible

mistake because students often do not find financial derivatives contracts to be particularly intuitive, and

this is particularly true for the options contract. This chapter takes a different approach by containing an

extensive explanation and discussion of Figure 1, which outlines the profits and losses that occur on financial

options and futures contracts depending on what happens to the price of bonds. To get the students to

understand these contracts and what their differences are, the instructor needs to carefully walk the students

through the numerical example of Figure 1. My experience in class suggests that unless this is done, many

students will just not understand what these financial derivatives and, particularly options, are all about.

Chapter 24: Hedging with Financial Derivatives 145

◼ Answers to End-of-Chapter Questions

1. Because for any given price at expiration, a lower strike price means a higher profit for a call option

◼ Quantitative Problems

1. You would like to enter into a contract which specifies that you will purchase $120 million of bonds

with an interest rate equal to the current interest rate six months from now.

3. The futures price must fall to $101. Otherwise, arbitrageurs would buy the bond for $101, sell the

4. You have a loss of 6 points, or $6000, per contract.

5. You would buy a $100 million worth, i.e. 1000 contracts of long-term bond futures contracts with an

6. You would buy $100 million worth (1000 contracts) of the call long-term bond option with a delivery

date of one year in the future and with a strike price that corresponds to a yield of 8%. This means that

7. The put option is out of the money because you would not want to take the option to sell the futures

9. Because an option has the feature that you win big if the price has a large change in one direction but

Chapter 24: Hedging with Financial Derivatives 147

Compute PV. PV = $98,312.41, or $889.97 of the payments went toward principal.

16. Laura, a bond portfolio manager, administers a $10 million portfolio. The portfolio currently has

a duration of 8.5 years. Laura wants to shorten the duration to 6 years using T-bill futures. T-bill

futures have a duration of 0.25 years and are trading at $975 (face value = $1,000). How is this

accomplished?

Solution: The average portfolio duration needs to be 6 years.

17. Futures are available on 3-month T-bills with a contract size of $1 million. If you take a long position

at 96.22 and later sell the contracts at 96.87, how much would the total net gain or loss be on this

transaction?

18. Chicago Bank and Trust has $100 million in assets and $83 million in liabilities. The duration of the

assets is 5.9 years, and the duration of the liabilities is 1.8 years. How many futures contracts does

this bank need to fully hedge itself against interest rate risk? The available Treasury bond futures

contracts have a duration of 10 years, a face value of $1,000,000, and are selling for $979,000.

19. A bank issues a $3 million commercial mortgage with a nominal APR of 8%. The loan is fully

amortized over 10 years requiring monthly payments. The bank plans on selling the loan after

2 months. If the required nominal APR increases by 45 basis points when the loan is sold, what

loss does the bank incur?

148 Mishkin/Eakins • Financial Markets and Institutions, Eighth Edition

Solution: The mortgage requires monthly payments as follows:

PV = 3000000, I = 8/12, N = 120, FV = 0

20. Assume the bank in the previous question partially hedges the mortgage by selling three 10-year

T-note futures contracts at a price of

20 32

100 / .

Each contract is for $1,000,000. After 2 months, the

futures contract has fallen in price to

24 32

98 / .

What was the gain or loss on the futures transaction?

Solution: On each contract, the gain is

20 24

32 32

(100 / 98 / ) 10,000 18,750− =

Total gain = $18,750 3 = $56,250

21. Springer Country Bank has assets totaling $180 million with a duration of 5 years, and liabilities

totaling $160 million with a duration of 2 years. Bank management expects interest rates to fall from

9% to 8.25% shortly. A T-bond futures contract is available for hedging. Its duration is 6.5 years and

is currently priced at

532

99 /

How many contracts does Springer need to hedge against the expected

rate change? Assume each contract is has a face value of $1,000,000.

Solution:

22. From the previous question, rates do indeed fall as expected, and the T-bond contract is priced at

532

103 / .

If Springer closes its futures position, what is the gain or loss? How well does this offset the

approximate change in equity value.

Solution:

gap 5 (160/180) 2 3.22

al

L

DUR DUR DUR

A

= − = − =

Change in equity = –3.22 (−0.0075/1.09) 180,000,000 = $3,990,826

Each T-bill contract is worth $1,031,562.50, or $92,840,625 for the 90 contracts. This

represents a loss of $3,609,856, which roughly offsets the gain in equity value.

Although it appears that the bank would have been better off doing nothing, there was no

guarantee that rates would not rise!

150 Mishkin/Eakins • Financial Markets and Institutions, Eighth Edition

Solution:

27. A banker commits to a two-year $5,000,000 commercial loan and expects to fulfill the agreement in

30 days. The interest rate will be determined at that time. Currently, rates are 7.5% for such loans. To

hedge against rates falling, the banker buys a 30-days interest rate floor with floor rate of 7.5% on a

notional amount of $10,000,000. After 30 days, actual rates fall to 7.2%. What is the expected interest

income from the loan each year? How much did the option pay?

Solution: Assuming a simple interest commercial loan, the interest received each year will be

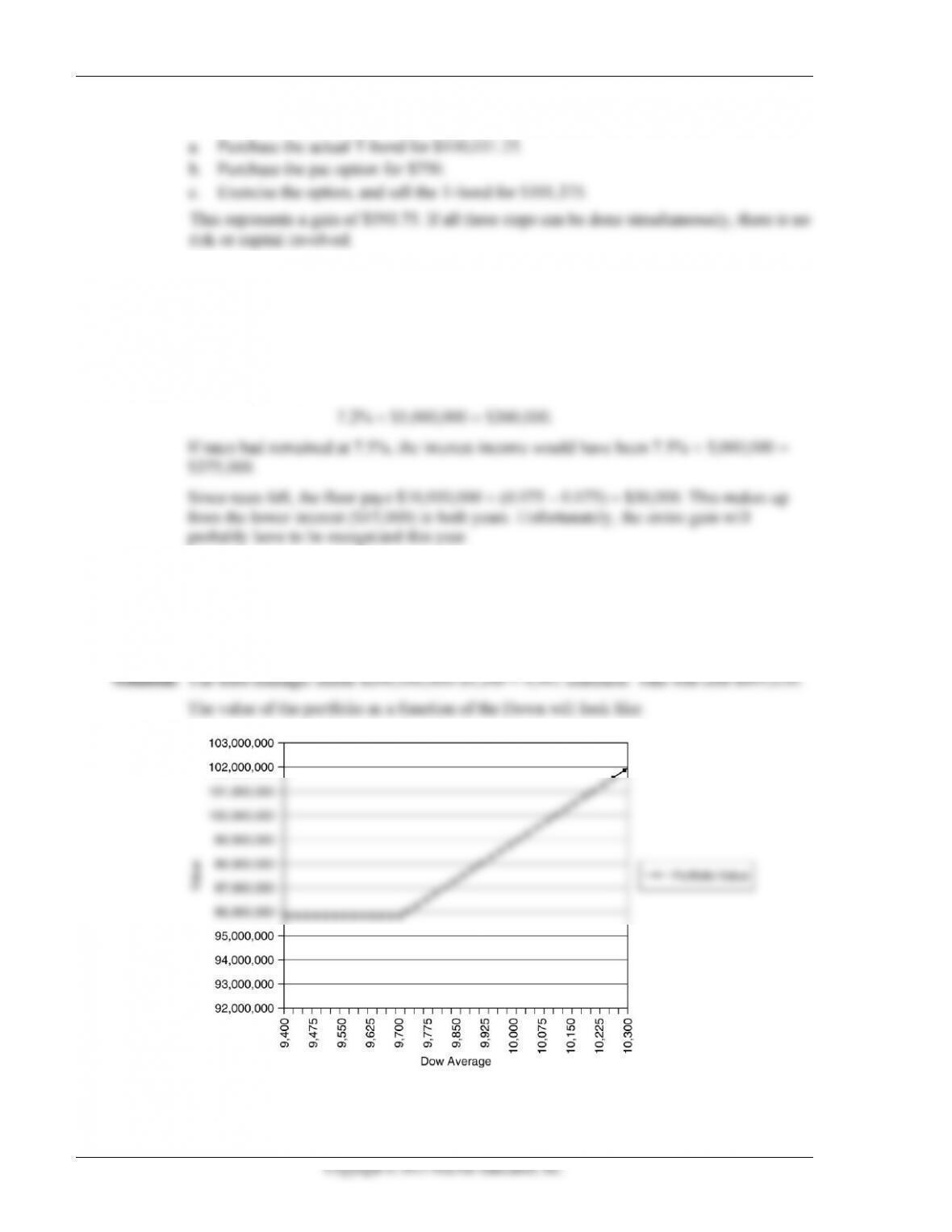

28. A trust manger for a $100,000,000 stock portfolio wants to minimize short-term downside risk using

Dow put options. The options expire in 60 days, have a strike price of 9,700, and a premium of $50.

The Dow is currently at 10,100. How many options should she use? Long or short? How much will

this cost? If the portfolio is perfectly correlated with the Dow, what is the portfolio value when the

option expires, including the premium paid?