180 Mishkin/Eakins • Financial Markets and Institutions, Seventh Edition

Chapter 23 Mini-Case

1. (Using assumptions in the chapter example):

a. 29 = 4 + 9 + (20% of 15) +13)

3. a. The income on assets declines by 0.03 × $29 million = $0.87 million. The payments on the

4. a. 0.31%

5. a. –26.4

b. –12.2

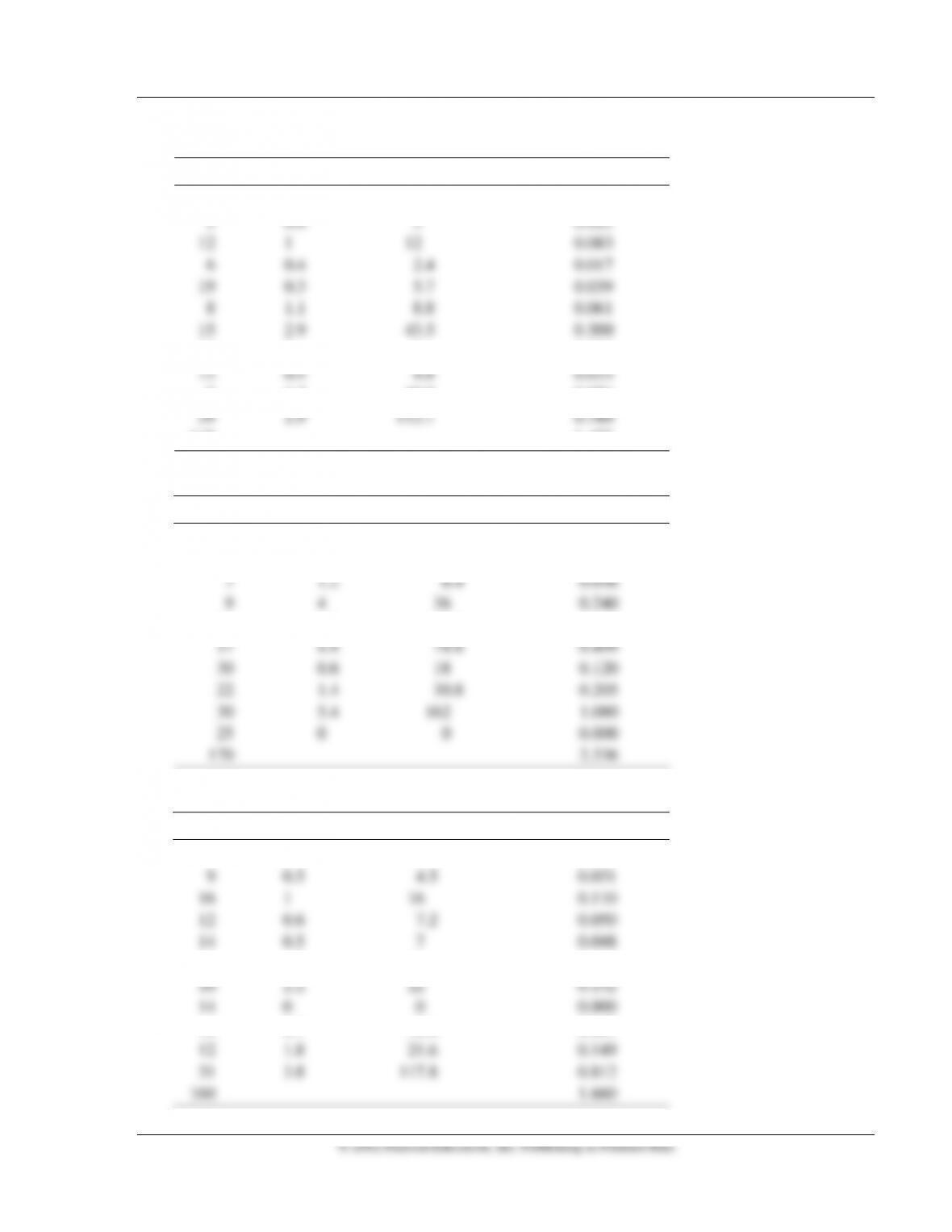

6. Calculate the weighted duration of each asset and liability.

Assets (Your Firm)

Asset Amount Duration Amount × Duration Weighted Duration

3 0 0 0.000

3 1.6 4.8 0.032

7 5 35 0.233

15 5.5 82.5 0.550

Solutions to Online Mini-Cases 181

Liabilities (Your Firm)

Amount Duration Amount

× Duration Weighted Duration

10 1 10 0.069

10 0 0 0.000

9 1.2 10.8 0.074

145 1.477

Assets (Your Competition)

Asset Amount Duration Amount × DurationWeighted Duration

4 0 0 0.000

5 0.3 1.5 0.010

21 0.9 18.9 0.126

Liabilities (Your Competition)

Amount Duration Amount

× Duration Weighted Duration

14 1 14 0.097

10 1.8 18 0.124

18 0.7 12.6 0.087

Solutions to Online Mini-Cases 183

Chapter 24 Mini-Case A

1. Short

af = 1.3 × 0.90 = 1.17]

4. a. $560,000 [= 7,000,000 × 0.08]

5. a. –$3

Because: %ΔNW = –DURgap × Δi/(1 + i) = –2.2 × 0.01/(1 + 0.06) = –0.0207 = –2.07%. Hence,

6. a. 75

Because: Vf = –DURgap × Va/DURf = –150 million × 2.2/4.4 = –75 million

8. Bank is required to show profits or losses from hedges without recognizing offsetting events.

10. [=

β

× (value of portfolio)/(value of contract) = 0.90 × (12 million)/(200,000)]

11. Bank would set up the hedge to offset adverse changes in foreign exchange rates relative to the U.S.

12. (Same general answer as found in question 11 above.) Bank would set up the hedge to offset adverse

changes in foreign exchange rates relative to the U.S. dollar. Gains in futures market would offset losses

184 Mishkin/Eakins • Financial Markets and Institutions, Seventh Edition

Chapter 24 Mini-Case B

1. $7 million/$100,000 = 70

3. a. HR = (7%/6%) × 1.1 = 1.28

b. Contracts = 1.28 × 70 = 89.6

4. The accounting problems created from hedging with financial futures are avoided by removing the

6. a. There is insufficient information to solve for the swap’s duration. However, if we assume the

swap’s duration is –3.3, the rest, b through d, can be solved as follows:

is 3.11%.

e. Approximately zero for a perfect hedge

7. Foreign exchange rate risk may be hedged using currency options, currency swaps, futures contracts

Chapter 26 Mini-Case-Web

2. 50% or $140

4. 3% of assets or $8

6. Company has high real estate loans, bank loans, and commercial paper with low other assets, debt not

elsewhere, and other liabilities.

8. Concentration of services for one-stop centers and increased flexibility in support of customer needs