5-53 (20 min.)

Basic Marginal Total

Number of flights per month 3,000 120 3,120

Available seats 300,000 12,000 312,000

Seats filled 156,000 2,400 158,400

Whelan, only after the line’s basic schedule has been set.

“Then you go a step farther,” he says, and see if adding more flights will

contribute to profits. Similarly, if he’s thinking of dropping a flight with a

disappointing record, he puts it under the marginal microscope: “If your revenues are

going to be more than your out-of-pocket costs, you should keep the flight on.”

all. A pair of night coach flights on the Houston-San Antonio-El Paso-Phoenix-Los

Angeles leg, added on a marginal basis, have turned out to be so successful that they

are now more than covering fully allocated costs.

Alternative. Whelan uses an alternative cost analysis closely allied with the

marginal concept in drawing up schedules. For instance, on his 11:11 p.m. flight

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

215

And there are other absolute-loss flight scheduled solely to bring passengers to a

connecting Continental long-haul flight; even when the loss on the feeder service is

considered a cost on the long-haul service, the line makes a net profit on the trip.

Continental’s data handling system produces weekly reports on each flight, with

revenues measured against both out-of-pocket and fully allocated costs. Whelan uses

these to give each flight a careful analysis at least once a quarter. But those added on

a marginal basis get the fine-tooth-comb treatment monthly.

The business on these flights tends to be useful as a leading indicator, Whelan

finds, since the off-peak traffic is more than normally sensitive to economic trends

and will fall off sooner than that on the popular-hour flights. When he sees the night

coach flights turning in consistently poor showings, it’s a clue to lower his projections

5-54 (15-20 min.)

1. Total variable costs are $.85 + $.65 = $1.50 per boomerang.

Total fixed costs are $109,000 + $23,000 = $132,000

Volume in units 170,000 220,000 260,000

2. Note the significant difference in predictions. For example, the correct analysis

indicates $157,000 operating income at a 170,000 volume level; the incorrect

5-55 (15-20 min.)

1. Compare option a to option b:

Extra revenue from option a: ($32 – $15) × 30 passengers = $510

Extra costs for option a: ($2.20 – $.20) × 65 mi + $400 = $530

2. This depends on the total additional revenues and costs for option b, the best of

the two options:

Revenue: $15 × 30 $450.00

$197. The cost of the tour guide and the cost of moving the car to the main track

5-56 (15-20 min.)

1. Net income will be increased by 300 × (€40 – €25 – €10) = €1,500.

3. €180,000, €70,000, €30,000, €10; i.e., all numbers are irrelevant except €25.

4. Selling price: €180,000 ÷ 2,000 units = €90

Total sales: 2,400 × 2 × €90 = €432,000

5-57 (15-25 min.)

1. Budgeted fixed manufacturing overhead per unit:

$72,000,000 ÷ 9,000,000 = $8

2. Relevant items:

Additional sales $3,450,000

3. Students may raise many points, including:

a. Whether the president is willing to “invest” $740,000 in forgone operating

4. Budgeted fixed manufacturing overhead rate would be $72,000,000 ÷ 4,500,000

= $16. However, the additional operating income in requirement 2 would be

5-58 (20-30 min.) When this problem was used in an exam, it was well done by

students who used contribution margin analysis in total dollars. A number of students

attempted to force a decision by means of analysis of unit costs or by break-even

analysis, failing to consider the effect of sales volume on profits. A number of good

solutions were marred by failure to draw specific conclusions.

However, this is in excess of present capacity.

Maximum at present capacity: 75,000 units output at $26

= Contribution margin of $900,000

This is $900,000 – $845,000 = $55,000 more contribution than is generated by

the current price of $27. Even with no capacity expansion, the price should be

5-59 (10-15 min.)

1. Manufacturing cost $27.00

$32.40, assuming that market research is right about the market price of $26.00.

Even with no profit margin, the cost of $27 exceeds the price of $26.

2. Using target costing, Memphis would begin with the market price of $26.00.

From this, managers would compute the largest acceptable manufacturing cost,

$21.67:

3. Memphis managers would have to determine if they could design the garage-

door-opener motor and its production process in a way that manufacturing costs

were below $21.67. Both the design specifications for the motor and the

5-60 (35-45 min.)

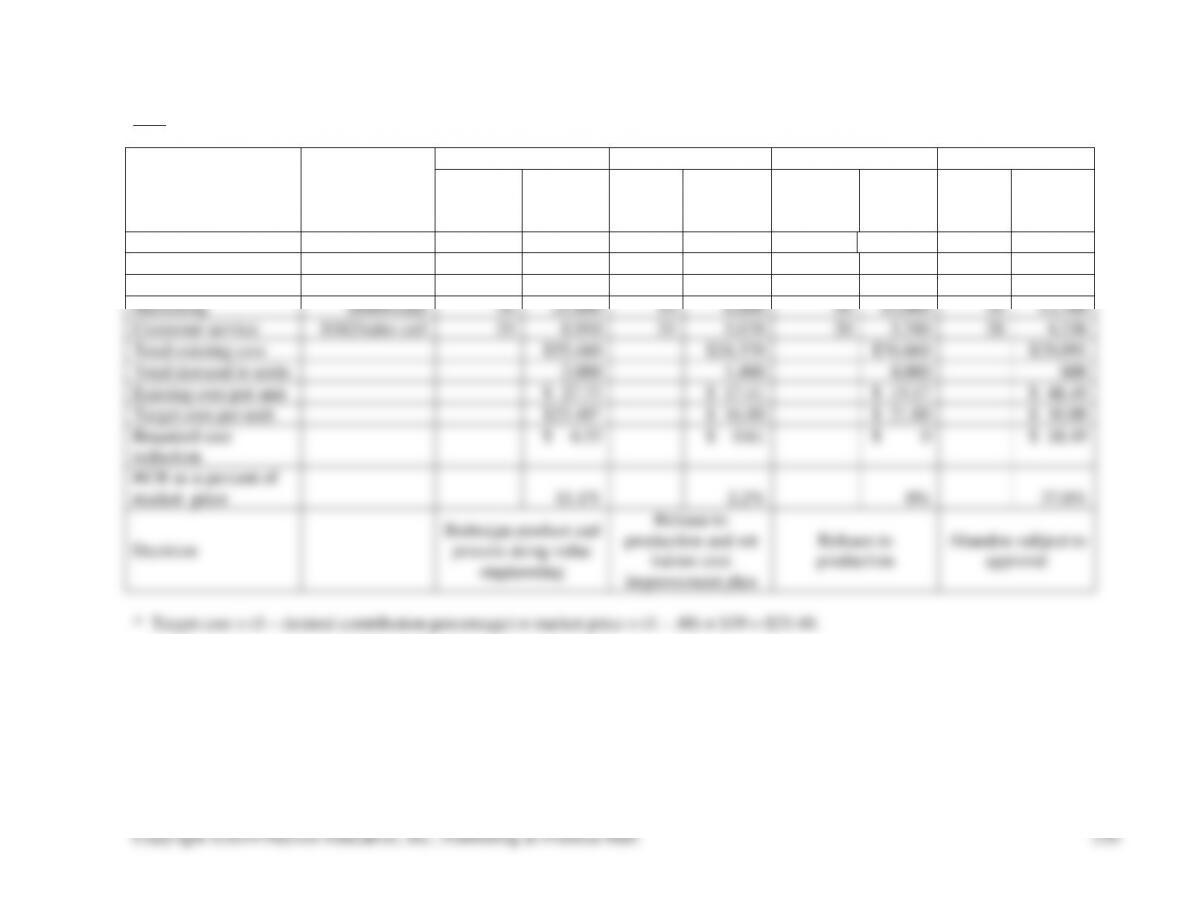

Cost per driver

unit

C-200472

C-200473

C-200474

C-200475

Number

of units

Cost

Numbe

r of

units

Cost

Number

of units

Cost

Numbe

r of

units

Cost

Direct material

$1.60/ pound

2,000

$3,200

1,000

$ 1,600

4,000

$ 6,400

800

$1,280

Setup/maintenance

$1,015/ setup

10

10,150

4

4,060

12

12,180

5

5,075

Processing

$370/ mach. hr.

20

7,400

12

4,440

32

11,840

12

4,440

Marketing

$860/order

30

25,800

10

8,600

50

43,000

16

13,760

Customer service

$162/sales call

55

8,910

35

5,670

20

3,240

28

4,536

Total existing cost

$55,460

$24,370

$76,660

$29,091

Total demand in units

2,000

1,400

4,000

600

Existing cost per unit

$ 27.73

$ 17.41

$ 19.17

$ 48.49

Target cost per unit

$23.40*

$ 16.80

$ 21.00

$ 30.00

Required cost

reduction

$ 4.33

$ 0.61

$ 0

$ 18.49

RCR as a percent of

market price

11.1%

2.2%

0%

37.0%

Decision

Redesign product and

process using value

engineering

Release to

production and set

kaizen cost

improvement plan

Release to

production

Abandon subject to

approval

* Target cost = (1 – desired contribution percentage) × market price = (1 – .40) × $39 = $23.40.

5-61 (20 min.)

1. Contribution margin = $795 – ($460 + $40) = $295

Total contribution = $295 × 47,700 mowers = $14,071,500

2. Desired profit = .10 × ($795 × 47,700) = $3,792,150

3. A target costing company does not quit when the first cost estimate comes in too

high. Managers establish a target cost and try to adjust design, production and

marketing processes to meet the target cost. In this case, the target cost is:

Revenue $37,921,500

5-62 (30 – 40 min.)

Fixed overhead allocation rate per machine hour = €2,160,000 90,000 = €24

Variable overhead allocation rate = €40–€24 = €16 per machine hour

St. Tropez should not accept either order. The company does not have adequate

plant capacity to manufacture the order of 20,000 jewelry cases from Lyon Inc. without

Machine hours required to produce 20,000 jewelry cases

= Number of cases × machine hours per case = 20,000 × .25 = 5,000 hours.

The Lyon Inc. order for 20,000 jewelry cases would require 5,000 machine

hours, but only 4,500 machine hours are available in the second quarter.

Computations related to the order from Avignon Co. are as follows:

5-63 (10 – 15 min.)

1. Capacity is not sufficient to accept both orders, but there is enough capacity to

accept either the Nordstrom or the Macy’s order. There is excess capacity for 150,000

shoes, but the two orders together would require production of 90,000 + 75,000 =

165,000 shoes.

2. Some considerations would involve cannibalization of existing sales by lower prices,

5-64 (20 – 30 min.) For the solution to this Excel Application Exercise, follow the

step-by-step instructions provided in the textbook chapter. The answers to the

3. The relevant costs are the variable costs, so we can focus on the contribution

5-65 (60 min. or more)

Pricing tends to be more of an “art” than a “science” in small firms. In large firms,

students will find a wide variety of tools and techniques but will most likely get

interesting answers to all the recommended questions.

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

224

example, one restaurant establishes prices using a formula of three times the cost of food

used in each menu item. This markup is designed (hoped) to cover all the operating costs

in the restaurant’s value chain beyond food cost (direct material). Other important factors

commonly mentioned include market conditions and the experience level of

management.

Small companies tend not to use target costing. Some form of cost plus pricing is

most often used. When target costing is used and managers are asked to explain the

target-costing process, it is often discovered that only some elements of a fully developed

target costing process are used.

Students may discover that different pricing policies are used for different product

or service families in the same firm. This is particularly true for large companies that

compete in many different markets.

5-66 (50 – 60 min.)

1. In its 2011 Annual Report, the major component of Colgate’s strategy is investing in

innovative new products with growth potential. The company supports this strategy

by focusing on the value chain functions R & D and marketing. The company that

places an emphasis on rapid product development needs relevant information

2. The importance of Colgate’s code of conduct can be measured several ways. Not only

does the company provide a link to the actual code of conduct for public viewing, the

following excerpt from the section “Living our Values” gives a good feel for the code

of conduct priority at Colgate.

Since 1987, our Code of Conduct has served as a guide for our daily

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

225

people, including Directors, Officers, and all employees of the Company

and its subsidiaries around the globe. Vendors and Suppliers are also

subject to these requirements as adherence to the Code is a condition for

conducting business with Colgate.

The Code of Conduct is regularly updated and reissued to ensure its

comprehensiveness. On June 7, 2012, Colgate’s Board of Directors

approved certain amendments to the Code of Conduct, including (i)

enhancements to existing provisions regarding conflicts of interest (to

address potential conflicts from internal interactions), protection of

Colgate’s confidential information and use of information technology

resources and (ii) additional provisions regarding data privacy and social

media. The updated Code of Conduct also highlights Colgate’s values

and leading with respect principles.

Yet another excerpt from that section speaks to Colgate’s commitment to ethical

values:

Most importantly, each employee is responsible for demonstrating

integrity and leadership by complying with the provisions of the Code of

Conduct, Global Business Practices Guidelines, Company policies and

all applicable laws. By fully including ethics and integrity in our

ongoing business relationships and decision-making, we demonstrate a

commitment to a culture that promotes the highest ethical standards.

3. As of late 2012, one of the new products is a Hill’s® Prescription Diet® y/d™ cat

4. The company displays its major product groups and major market regions using a

heading page. In late 2012, eight laundry conditioners were listed. The information

5. The company’s financial strategy is to continuously improve gross margin

percentage, reduce overhead (sales, general, and administrative expenses), and

59.1% in 2010 to 57.3% in 2011 (from the comparative consolidated statements of

income). Selling, general, and administrative expenses (a good surrogate for

of $1.734 billion in 2011.

These results are the primary source supporting increased R & D and advertising for