CHAPTER 2

COVERAGE OF LEARNING OBJECTIVES

LEARNING OBJECTIVE

FUNDA–

MENTAL

ASSIGN–

MENT

MATERIAL

CRITICAL

THINKING

EXERCISES

AND

EXERCISES

PROBLEMS

CASES, NIKE

10K, EXCEL,

COLLAB., &

INTERNET

EXERCISES

LO1: Explain how cost

drivers affect cost behavior.

A1, B1

25, 26, 28, 30,

31

47,49, 51, 53,

56

68

LO2: Show how changes in

activity cost–driver levels

affect variable and fixed costs.

A1, B1, A2,

A3, B2, B3

25, 26, 29, 30,

31, 32, 41, 48

47,49, 52, 53,

54, 56, 59, 60,

63

68, 69, 73

LO3: Explain step- and

mixed-cost behavior.

A4,B4

24,36,37,38,

39

75

LO4: Create a cost–volume–

profit graph and understand

the assumptions behind it.

33, 34, 35,40,

49

LO5: Calculate break–even

sales volume in total dollars

and total units.

A2, A3, B2,

B3

40, 41,42, 43

47,50, 52, 54,

55, 57, 59, 61

68, 69, 73, 74

LO6: Calculate sales volume

in total dollars and total units

to reach a target profit.

A2 , B3

33, 34, 43, 62

47,50, 52, 54,

55, 57, 59,

69

LO7: Differentiate between

contribution margin and gross

margin.

61

LO8: Explain the effects of

sales mix on profits

(Appendix 2A).

44

64, 65

70

LO9: Compute cost–volume–

profit relationships on an after–

tax basis (Appendix 2B).

45, 46

66, 67

71

CHAPTER 2

Introduction to Cost Behavior and Cost-Volume Relationships

2-A1 (20-25 Min.)

1. The cost driver for both resources is number of times the plant is cleaned. Labor cost

is a fixed-cost resource, and cleaning supplies is a variable cost. Costs for cleaning

between 4 and 8 times a month are:

Number of

2. If Napco hires the outside cleaning company, all its cleaning costs will be variable at a

rate of $5,700 per cleaning. The cost driver will be “number of times cleaned.” The

predicted cost to clean a total of 5 + 6 + 8 = 19 times is 19 × $5,700 = $108,300. Thus,

Napco will save by not hiring the outside cleaning company.

2–A2 (20–25 min.)

1. Let N = number of units

Sales = Fixed expenses + Variable expenses + Net income

$1.00 N = $4,000 + $.68 N + 0

$.32 N = $4,000

N = 12,500 units

Contribution margin percentage

.32

2. The quick way: (45,000 – 12,500) × $.32 = $10,400

Compare income statements:

Break-even

3. Total fixed expenses would be $4,000 + $1,600 = $5,600

$5,600

$.32/unit

$5,600

.32

or 17,500 units × $1.00 / unit = $17,500 sales

4. New contribution margin is $1.00 – $.68 – $.07 = $.25 per unit

2–A3 (20–30 min.)

The following format is only one of many ways to present a solution. This

situation is really a demonstration of “sensitivity analysis,” whereby a basic solution is

2. (a) 500,000 1.00 500,000 50,000 450,000

(b) 650,000 .40 260,000 50,000 210,000

2-A4 (20-25 min.) Some of these answers are controversial, and reasonable cases can

drivers.

1. (b) Fixed cost.

2. (d) Step cost.

3. (a) Variable cost with respect to revenue.

5. (c) Mixed cost with respect to miles driven.

7. (b) Fixed cost.

9. (a) Variable cost with respect to cases of 7-Up.

11. (b) Fixed cost.

2-B1 (20-25 Min.)

1. The cost driver for both resources is number of times the restaurant is cleaned. Labor

cost is a fixed-cost resource, and cleaning supplies is a variable cost. Costs for

cleaning between 35 and 50 times are:

Square Cleaning

2. If Applejack hires the outside cleaning company, all its cleaning costs will be variable

at a rate of $0.25 per square foot cleaned. The predicted cost to clean a total of 45 +

50 = 95 times is 95 × 6,000 × $0.25 = $142,500. Thus, Applejack will not save by

hiring the outside cleaning company.

(1) Times

Cleaned

(2) Square Feet

Cleaned

(3) Applejack

Total Cleaning Cost*

Outside Cleaning Cost

$.25 × (2)

35

210,000

$37,800

$52,500

40

240,000

40,200

60,000

45

270,000

42,600

67,500

50

300,000

45,000

75,000

* From requirement 1, total cost is $21,000 + $.08 x square feet cleaned

2-B2 (15-25 min.)

1. $2,340 ÷ ($30 – $12) = 130 child-days

3. a. 198 × ($30 – $12) – $2,340 = $3,564 – $2,340 = $1,224

or (22 × $18) + $828 = $396 + $828 = $1,224

2-B3 (15-20 min.)

$9,100

=

$9,100

= 1,300 units

2. Contribution margin ratio:

($43,000 $30,100)

$43,000

−

= 30%

3.

($29 –$13)

$16

5. New contribution margin: $48 – ($36 – 25% of $36)

= $48 – ($36 – $9) = $21;

$21

$21

2-B4 (20-25 min.)

The following classifications are open to debate. With appropriate assumptions,

other answers could be equally supportable. For example, in #2, the health insurance

would be a fixed cost if the number of employees will not change. This problem provides

1. X–ray operating cost Mixed Number of x–rays

3. Cancer research Fixed

5. Training cost Fixed

7. Consulting Fixed

2-1 This is a good characterization of cost behavior. Identifying cost drivers will

2-2 Two rules of thumb to use are:

a. Total fixed costs remain unchanged regardless of changes in cost-driver

2-3 Examples of variable costs are the costs of merchandise, materials, parts, supplies,

2-4 Fixed costs, by definition, do not vary in total as volume changes within the

relevant range and during the time period specified (a month, year, etc.). However, when

the cost-driver level is outside the relevant range (either less than or greater than the

2-5 Yes. Fixed costs per unit change as the volume of activity changes. Therefore,

2-6 No. Cost behavior is much more complex than a simple dichotomy into fixed or

2-7 No. The relevant range pertains to both variable and fixed costs. Outside a

2-8 The major simplifying assumption is that we can classify costs as either variable

or fixed with respect to a single measure of the volume of output activity.

2-9 The same cost may be regarded as variable in one decision situation and fixed in a

second decision situation. For example, fuel costs are fixed with respect to the addition

2-10 No. Contribution margin is the excess of sales over all variable costs, not fixed

costs. It may be expressed as a total, as a ratio, as a percentage, or per unit.

2-11 A “break-even analysis” does not describe the real value of a CVP analysis, which

shows profit at any volume of activity within the relevant range. The break-even point is

2-12 No. break-even points can vary greatly within an industry. For example, Rolls

2-13 No. The CVP technique you choose is a matter of personal preference or

2-14 Three ways of lowering a break-even point, holding other factors constant, are:

decrease total fixed costs, increase selling prices, and decrease unit variable costs.

2-15 No. In addition to being quicker, incremental analysis is simpler. This is

2-16 Operating leverage is a firm’s ratio of fixed to variable costs. A highly leveraged

2-17 An increase in demand for a company’s products will drive almost all other cost–

driver levels higher. This will cause cost drivers to exceed capacity or the upper end of

2-19 No. In retailing, the contribution margin is likely to be smaller than the gross

margin.

2-20 No. CVP relationships pertain to both profit-seeking and nonprofit organizations.

2-21 Contribution margin could be lower because the proportion of sales of the product

bearing the higher unit contribution margin is lower than the proportion budgeted.

2-22

before incomeTarget

incomenet

in Change

unitsin

in volume Change

Contribution margin

per unit

2-24 The fixed salary portion of the compensation is a fixed cost. It is independent of

2-25 The key to determining cost behavior is to ask, “If there is a change in the level of

the cost driver, will the total cost of the resource change immediately?” If the answer is

yes, the resource cost is variable. If the answer is no, the resource cost is fixed. Using

2-26 The key to determining cost behavior is to ask, “If there is a change in the level of

the cost driver, will the total cost of the resource change immediately?” If the answer is

2-27 Suggested value chain functions are listed below.

New Products

New Technology

New Positioning

Strategies

New Pricing

❑ Marketing

❑ R & D

❑ Design

❑ R & D

❑ Design

❑ Marketing

❑ Support

functions

❑ Marketing

2–28 (10-15 min.)

Situation

Best Cost Driver

Justification

1.

Number of Setups

Because each setup takes the same amount of time,

the best cost driver is number of setups. Data is both

plausible, reliable, and easy to maintain.

2.

Setup Time

Longer setup times result in more consumption of

mechanics’ time. Simply using number of setups as

in situation 1 will not capture the diversity

associated with this activity.

3.

Cubic Feet

Assuming that all products are stored in the

warehouse for about the same time (that is

inventory turnover is about the same for all

products), and that products are stacked, the volume

occupied by products is the best cost driver.

4.

Cubic Feet Weeks

If some types of product are stored for more time

than others, the volume occupied must be multiplied

by a time dimension. For example, if product A

occupies 100 cubic feet for an average of 2 weeks

and product B occupies only 40 cubic feet but for an

average of 10 weeks, product B should receive

twice as much allocation of warehouse occupancy

costs.

5.

Number of Orders

Because each order takes the same amount of time,

the best cost driver is number of orders. Data is both

plausible, reliable, and easy to maintain.

6.

Number of Orders

Each order is for different types of products but

there is not diversity between them in terms of the

time it takes to process the order. (If there was

variability in the number of product types ordered,

the best driver would be number of order line

items.)

2–29 (5-10 min.)

1. Contribution margin = $960,000 – $533,000 = $427,000

Net income = $427,000 – $310,000 = $117,000

3. Sales = $500,000 + $520,000 = $1,020,000

Net income = $520,000 – $200,000 = $320,000

2-30 (5-10 min.)

The $278,000 annual advertising fee is a fixed cost. The $6,100 cost for each

advertisement is a variable cost.

2-31 (5-10 min.)

With respect to the cost driver sales dollars, the $3,200,000 annual salaries of sales

personnel is a fixed cost. The sales commissions, travel costs, and entertainment costs are

2-32 (10-20 min.)

1. d = c × (a – b)

$750,000 = 125,000 × ($26 – b)

2. d = c × (a – b)

3. c = d ÷ (a – b)

4. d = c × (a – b)

= 60,000 × ($30 – $20)

5. d = c × (a – b)

$172,000 = 86,000 × (a – $12)

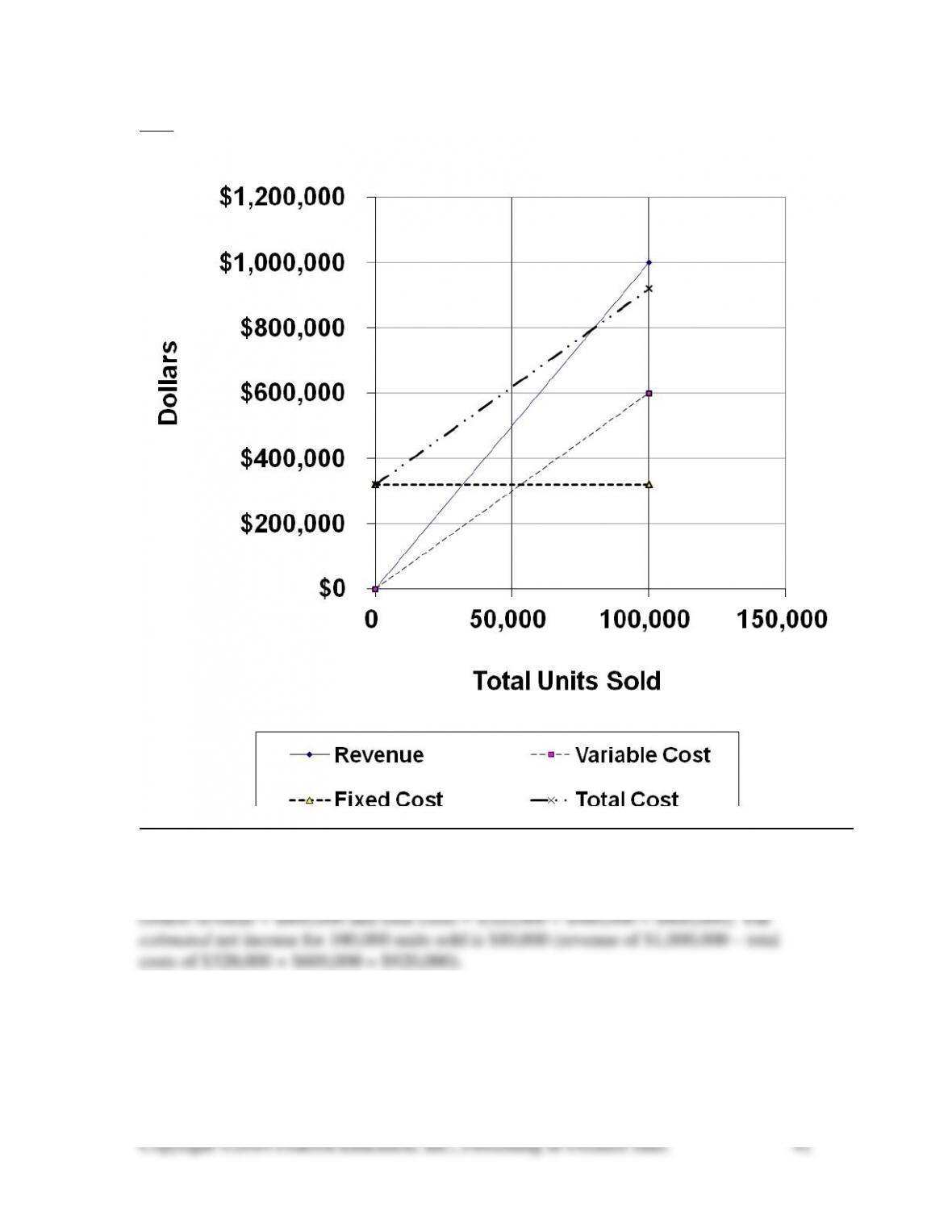

2-33 (10 min.)

Using the graph above, the estimated breakeven point in total units sold is about 80,000

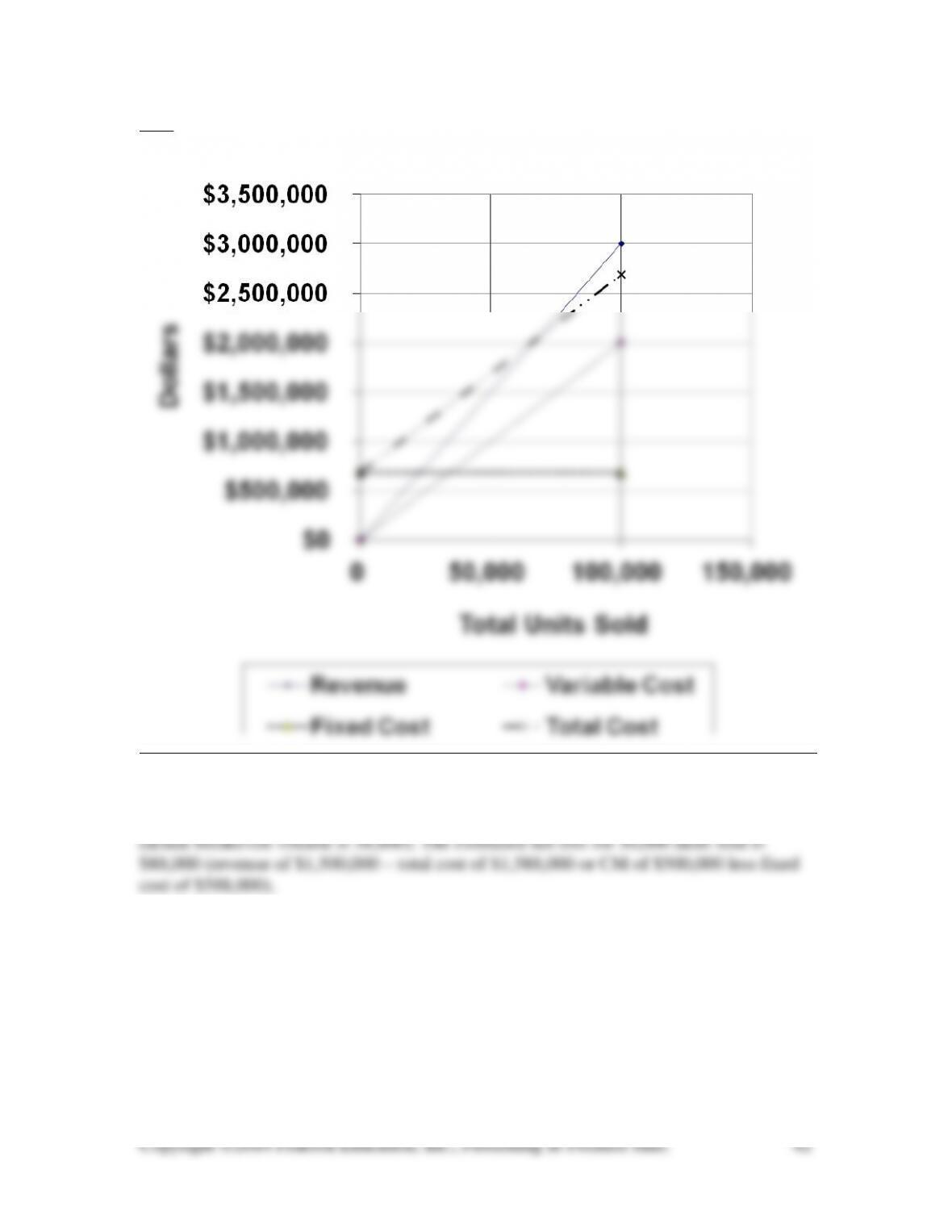

2-34 (10 min.)

Using the graph above, the estimated breakeven point in total units sold is about 60,000

$-

$0.05

$0.10

100,000 125,000 150,000 175,000 200,000

Square Feet

Labor Cost per Square Foot

Supplies Cost per Square Foot

Square Feet

2-35 (20–25 min.)

Square

Feet

Labor Cost

Labor Cost per

Square Foot

Supplies Cost

Supplies Cost per

Square Foot

100,000

$24,000

$ 0.240

$ 5,000

$0.050

125,000

24,000

$ 0.192

6,250

0.050

150,000

24,000

$ 0.160

7,500

0.050

175,000

24,000

$ 0.137

8,750

0.050

200,000

24,000

$ 0.120

10,000

0.050

Fixed-Cost

per Unit

Behavior

2-36 (20-25 min.)

Supplies

Labor Cost Per Cost per

Square Square Foot Total Labor Square Supplies

Feet (Estimated) Cost Foot Cost

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

100,000

125,000

150,000

Labor Costs

Square Feet

Total Labor Cost

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

100,000

125,000

150,000

Supplies Cost

Square Feet

Total Supplies Cost

Labor cost shows a fixed-cost behavior, while supplies cost shows a variable-cost

behavior.

2-37 (5 min.) Only (b) is a step cost.

(a) This is a fixed cost. The same cost applies to all volumes in the relevant

range.

2-38 (5 min.) The $8,000 is a fixed cost and the $52 per unit is a variable cost. By

definition, adding a fixed cost and a variable cost together produces a mixed cost.

2-39 (10-15 min.)

1. Machining labor: G, number of units completed or labor hours

3. Annual wage: C or E (depending on work levels), labor hours

5. Quantity discounts: A, amount purchased

7. Sheet steel: D, number of farm implements of various types

9. Natural gas bill: C, cubic feet of usage

2-40 (10 min.)

1. Let TR = total revenue

2. Daily revenue per patient = $60,000,000 ÷ 37,500 = $1,600. This may appear

2-41 (10 min.)

1. The break-even point in total revenue is fixed cost divided by the contribution-

margin ratio (CMR). CMR equals 1 – Variable-Cost Ratio.

2.

a. Total revenue $150,000,000

Variable cost (.7 × 150,000,000) 105,000,000

Contribution margin 45,000,000

Fixed costs 42,000,000

Net profit $ 3,000,000

b. Total revenue $150,000,000

Variable cost (1.1 × .7 × 150,000,000) 115,500,000

Contribution margin 34,500,000

Fixed costs 42,000,000

Net loss $ (7,500,000)