15-38 (20-30 min.)

Case

1 2 3 4 5 6 7

X $11,000 $3,000 $9,000 $14,000 $7,500 $ 8,000 $ 4,200

Y 6,000 7,000 2,000 3,900

: Z = $7,000 – $4,000 = $3,000

4: X = $8,000 + $12,000 – $6,000 = $14,000

5: X = $3,000 + $4,500 = $7,500

6: X = $14,000 – $6,000 = $8,000

: Y = $6,000 – $4,000 = $2,000

The following framework may help on cases 6 and 7:

Stockholders’ equity: Case 6 Case 7

Beginning ? = 4,500 $8,200 – 4,000 = 4,200

Additional investments +5,000 0

Net profit Y = 6,000 – 4,000 = +2,000 ? = 100

15-39 (45-75 min.)

2. CONNECTIVITY PLUS

Statement of Income

For the Month Ended April 30, 20X1

Sales $62,000

Cost of goods sold 31,000

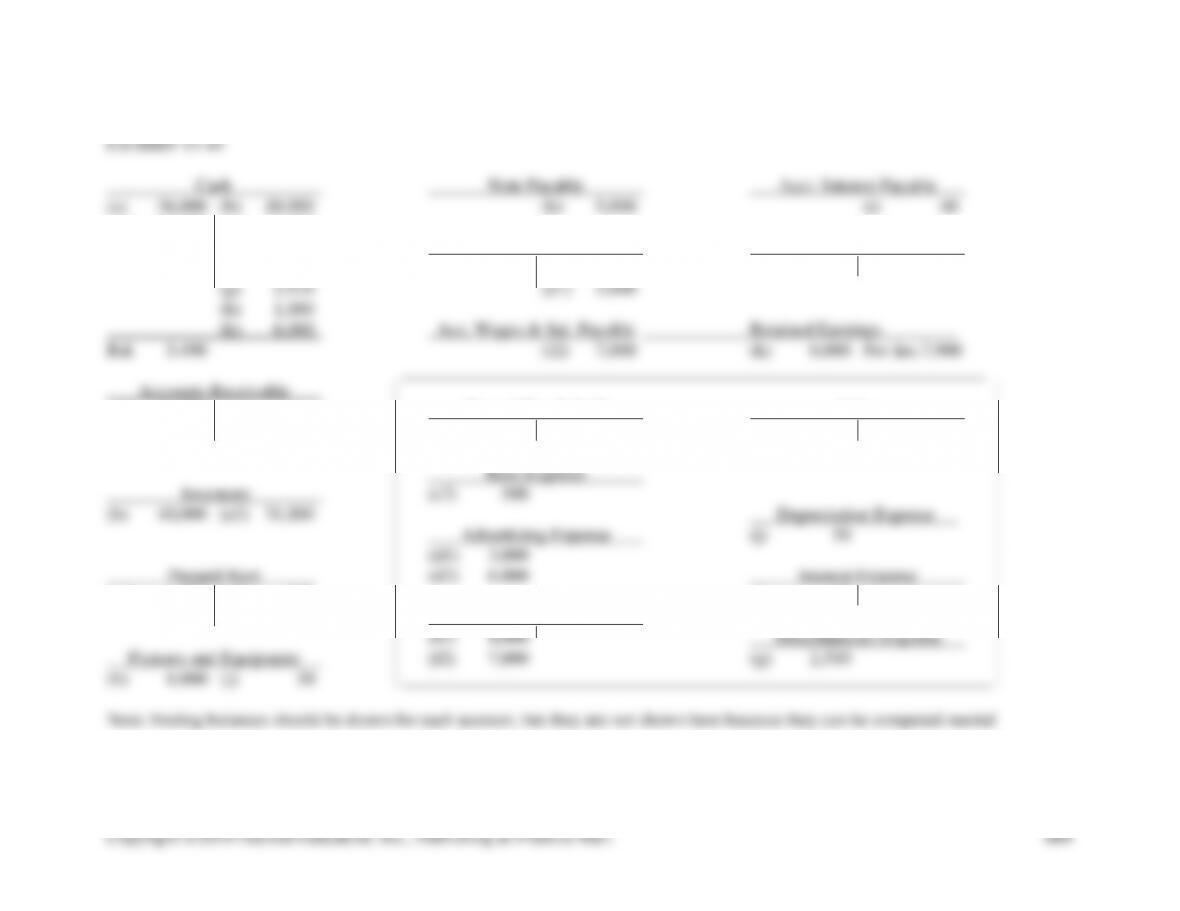

EXHIBIT 15-39

Assets = Liabilities + Stockholders’ Equity

Pre- Fixtures Liabilities Stockholders’ Equity

Accounts paid & Equip- Accounts Notes Accr. Accr. Paid-in Retained

Trans. Cash + Receivable +Inventory +Rent + ment = Payable +Payable + Wages + Int. + Capital + Earnings

g. – 2,510 = – 2,510 (E)

h. – 1,000 +6,000 = +5,000

i. = +40** – 40 (E)

j. – 50 = – 50 (E)

k. – 6,000 = – 6,000 (D)

Balance

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

660

CONNECTIVITY PLUS

Balance Sheet

April 30, 20X1

Assets Equities

Liabilities:

Cash $ 5,490 Accounts payable $23,000

Accounts receivable 52,000 Notes payable 5,000

Inventory 9,000 Accrued wages and

Prepaid rent 500 salaries payable 7,000

Fixtures and equipment, net 5,950 Accrued interest payable 40

Total Liabilities $35,040

Stockholders’ equity:

3. The picture in this set of financial statements is not unusual for new businesses.

Some of the liabilities are very current: accounts payable, $23,000, and accrued

wages, $7,000. These are much larger than the $5,490 of cash. Unless much of

promptly.

15-40 (30 min.)

1. DR. F. RIVERA, DENTIST

Income Statement

For the Year Ended December 31, 20X1

Cash Basis Accrual Basis

Fee revenue $79,000 $97,000 1

Expenses:

2. The accrual basis provides a better measure of economic performance because it

encompasses all assets and liabilities arising from operations rather than their

immediate cash effects alone. For example, the $2,000 advance payment has not

yet been earned and therefore represents an obligation of Dr. Rivera. However,

1. Dr. 2. Cr. 3. Cr. 4. Cr. 5. Dr. 6. Cr. 7. Cr. 8. Cr.

1. F. Purchases of inventory should be debited to Inventory and credited to

Accounts Payable.

3. T

5. F. The first sentence is correct. However, credit entries always must be on the

right.

7. F. Decreases in assets are shown on the credit side, but decreases in liabilities and

stockholders’ equity are shown on the debit side.

9. F. All credits are on the right.

15-43 (10-15 min.)

1 and 2. These accounts will generally have a beginning balance. The balances are

omitted in the following T-accounts.

Cash

Dues Receivable

Accounts Receivable

a. 600

a. 600

b. 200

d. 200

b. 150

d. 200

c. 210

b. 350

c. 210

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

663

EXHIBIT 15-44 Amounts are in thousands of dollars.

Cash Note Payable Paid-in Capital

(a) 150 (b) 35 (g) 24 (a) 150

(d1) 35 (f) 18

(e) 20 (g) 12

(d1) 75 (e) 20 Cost of Goods Sold Sales

(d2) 40 (d1) 110

Merchandise Inventory

(b) 35 (d2) 40 Rent Expense Wages, Sal., & Comm.

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

664

EXHIBIT 15-45

Cash Note Payable Accr. Interest Payable

(a) 36,000 (b) 20,000 (h) 5,000 (i) 40

(e1) 10,000 (c1) 1,000

(d2) 6,000 Accounts Payable Paid-in Capital

(f1) 4,000 (b) 20,000 (a) 36,000

(e1) 52,000 Cost of Goods Sold Sales

(e2) 31,000 (e1) 62,000

(c1) 1,000 (c2) 500 (i) 40

Wages & Sal. Expense

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

665

15-46 (10-15 min.)

1. The bank’s assets (cash) and liabilities (deposits) would each increase by $5,000.

Your mix of personal assets would change, but your total assets and your

2. The bank’s total assets and liabilities would be unaffected. The only change

3. Personal cash (asset) would increase by $20,000, and personal liabilities (note

payable) would increase by the same amount.

15-47 (20 min.)

COSTCO WHOLESALE CORPORATION

Balance Sheet

August 28, 2011

(in millions of dollars)

15-48 (20-25 min.)

1. GOOGLE INC.

Income Statement

For the Year Ended December 31, 2011

2. GOOGLE INC.

Changes in Retained Earnings

For the Year Ended December 31, 2011

3. Google did not pay any cash dividends. Apparently management decided that

15-49 (15-25 min.)

The following is Dell’s income statement. Students may use other acceptable

formats. Accounts payable and cash are irrelevant.

DELL INC.

Income Statement

15-50 (10 min.)

The sale of the new shares will bring in cash of $50,000 and add $50,000 to the existing

$150,000 of capital, but instead of the capital being identified with a particular owner it

1. Percentage increase in total assets:

($14,998 ÷ $14,419) – 1 = 4.0%

2. Assets = Liabilities + Shareholders’ Equity

$14,998 = $5,155 + $9,843

3. Beginning retained earnings $6,095

Net income 2,133

4. Percentage growth in net income, fiscal 2011:

($2,133 ÷ $1,907) – 1 = 11.9%

15-52 (45-60 min.) For the solution to this Excel Application Exercise, follow the

month.

3. Cash decreased by $76,000. This is not unusual for a young company. Many of

expenses.

15-53 (20 – 30 min.)

The purpose of this game is to help students identify different types of implicit

transactions. Usually implicit transactions are harder for students to understand than

15-54 (15-25 min.) NOTE TO INSTRUCTOR: This solution is based on the web site

changed.

1. McDonalds’ largest asset is property and equipment, comprising about 69% of

2. One measure of the size of a company is its total assets. McDonalds’ total assets

increased 3%, from $32.0 billion to $33.0 billion. This is shown on the balance

sheet.

3. McDonalds’ total revenues grew about 12.2%, from $24,075 million to $27,006

4. Each of the basic financial statements includes clues that McDonalds is a

corporation. Most obvious is that each statement is labeled “consolidated.” The

5. The “Report of Independent Auditors” indicates that McDonalds’ financial

statements comply with GAAP. The quote from the auditor’s report is: “[T]he