Exhibit 12-47, Part 2

Model 1 Model 2 Model 3

Direct materials:

Model 1: ¥4,000 × 80 boards ¥320,000

Model 2: ¥6,000 × 160 boards ¥960,000

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

543

12-49 (20 min.)

1. Allocations are in millions:

Actual Allocated

2. Northeast’s manager would probably be indifferent, Mid-Atlantic’s would be

pleased, and Southeast’s would be displeased.

The major weakness of using revenue as a basis for cost allocation is that it often

fails to portray underlying cause-and-effect relationships. The major point of

this problem is to show how strange results occur when the costs being allocated

result.

3. Allocations are in millions:

Budgeted Allocated

Revenue Costs

Divisions:

Northeast $120 [(120 ÷ 640) × $30] = $ 5.625

4.7%. The resultant deviation of the actual percentage (5.1%) from the budgeted

percentage (4.7%) would highlight the effects of Mid-Atlantic’s troubles.

4. Many accountants and managers oppose allocating any central costs when no

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

545

12-50 (20-40 min.)

1. (a) The allocation of joint costs would be in a 1:5 ratio:

Product Product

A B Total

Sales value $2,000 $2,000 $4,000

2. (a) The relative sales value method deducts separable costs to arrive at an

imputed sales value at split-off point:

A B Total

Sales value $2,000 $2,000 $4,000

Separable costs 700 400 1,100

12-51 (100 – 200 min.)

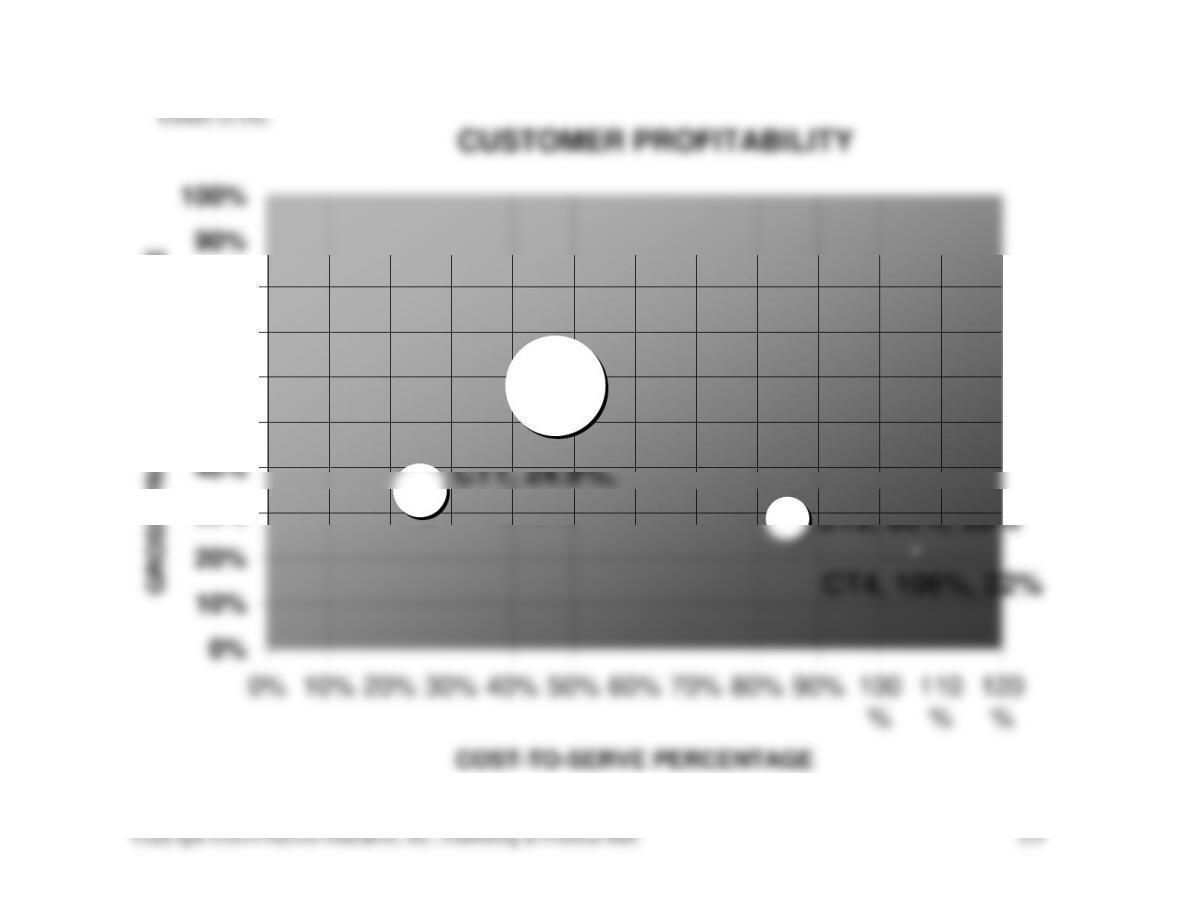

1. Exhibits 12-51A and 12-51B show the calculation of customer gross margin

2. Suggested strategies for profit improvement for the 4 customer types follow.

• Customer type 1 – Mega stores. These stores have the lowest cost-to-serve.

Profitability can be improved by focusing on a better product mix. A quarter of

the sales (cases) to these stores are from bulk and singles products – both of

which have a negative gross margin. A shift in mix towards more regular and

serve.

For example, suppose that the average order size could be increased from 75,000

to 150,000 cases. If the total annual cases sold is unchanged (6,000,000), a total of

40 orders, a 50% reduction, would be made. An estimate of the cost savings and

the impact on the cost-to-serve percentage can be made as follows:

Cost per Driver Unit Reduction in Driver Cost Savings

on increasing order size can only be estimated, it is reasonable to expect dramatic

cost savings from the current 85% of revenue.

Other factors that should be investigated include the high level of corporate

support and customer service.

• Customer type 3 – Local large stores. Local large stores generate $68,400 ÷

should rationalize their business. Several actions could be suggested. One is to

charge a premium for all high-security products. The vast majority of these

products are sold to specialty stores with only marginal sales to mega and local

small stores. Another action is to adopt a customer loyalty program based on

volume of sales. The list price of $7.25 per case would apply to customers with

CUSTOMER PROFITABILITY

CT3, 47%, 58%

CT2, 85%, 29%

CT1, 24.9%,

34.9%

CT4, 106%, 22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100

%

110

%

120

%

COST-TO-SERVE PERCENTAGE

Exhibit 12-51C

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

552

12-52 (50-60 min.)

1. Systems Claims

Department Claims Department

First Department First

2. Solution is in Exhibit 12-52.

3. a. The new charging system should improve cost control in the Systems

Department (if the rates are valid) because inefficiencies can no longer be

passed on to the user departments. Thus, the Systems Department would be

forced to watch its costs closely.

b. The recommended system for charging costs to user departments should

Copyright ©2014 Pearson Education, Inc., Publishing as Prentice Hall.

553

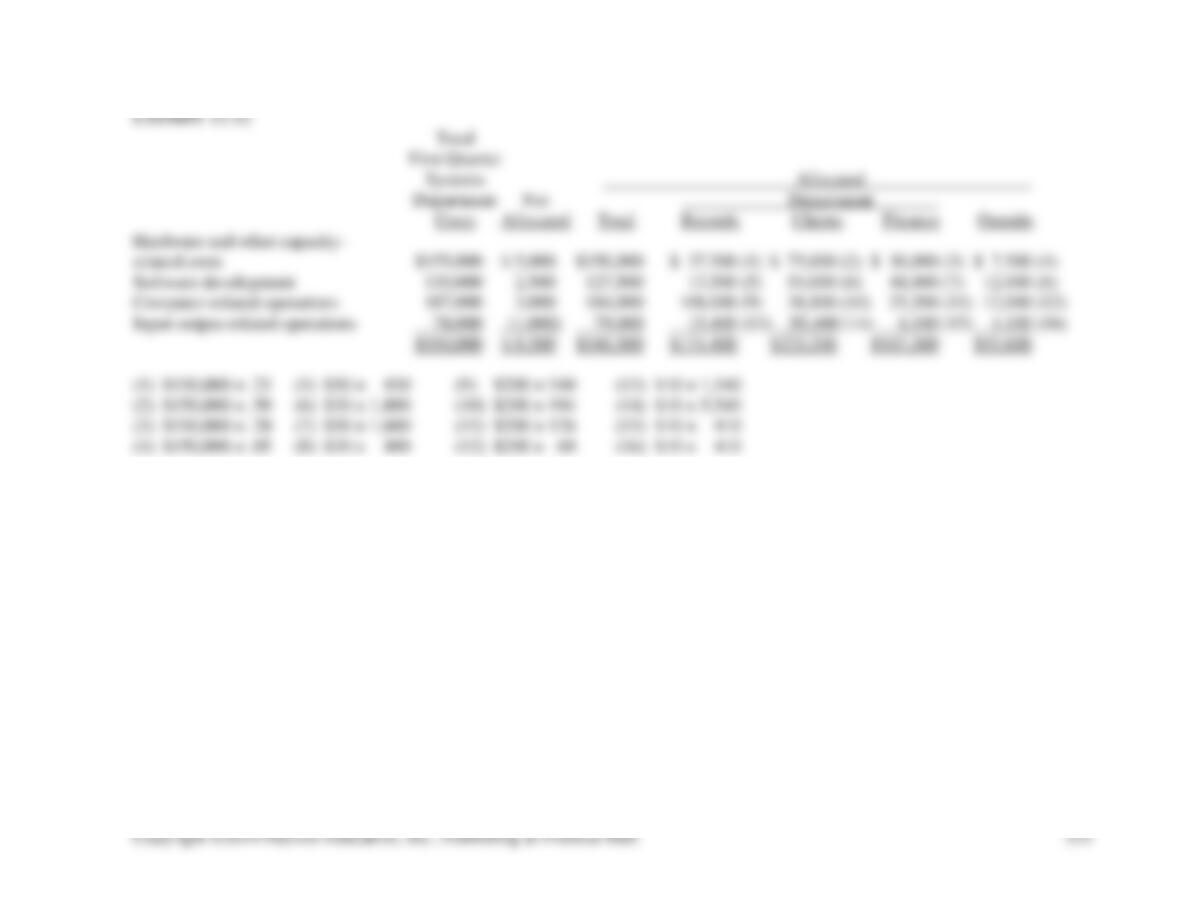

EXHIBIT 12-52

Total

First Quarter

Systems Allocated

Department Not Department

Costs Allocated Total Records Claims Finance Outside

Hardware and other capacity-

related costs $155,000 $ 5,000 $150,000 $ 37,500 (1) $ 75,000 (2) $ 30,000 (3) $ 7,500 (4)

Software development 130,000 2,500 127,500 13,500 (5) 54,000 (6) 48,000 (7) 12,000 (8)

Computer-related operations 187,000 3,000 184,000 108,000 (9) 38,800 (10) 25,200 (11) 12,000 (12)

Input-output-related operations 78,000 (1,000) 79,000 15,400 (13) 55,400 (14) 4,100 (15) 4,100 (16)

$550,000 $ 9,500 $540,500 $174,400 $223,200 $107,300 $35,600

(1) $150,000 × .25 (5) $30 × 450 (9) $200 × 540 (13) $10 × 1,540

(2) $150,000 × .50 (6) $30 × 1,800 (10) $200 × 194 (14) $10 × 5,540

(3) $150,000 × .20 (7) $30 × 1,600 (11) $200 × 126 (15) $10 × 410

(4) $150,000 × .05 (8) $30 × 400 (12) $200 × 60 (16) $10 × 410

12-53 (15-20 min.) Amounts are in millions.

Earnings

Earnings Allocation After

Before of Allocation of

1. Residential = $305,500

Commercial = $504,500

3. Commercial = $504,750

4. In this case there is little difference between the two methods, so the less costly

12-55 (100 min. or more)

The purposes of this exercise are to conduct library research in the current

management accounting literature and to gain a better understanding of activity-based

costing and activity-based management. Students must find their own article on ABC or

12-56 (30-40 min.) NOTE TO INSTRUCTOR: This solution is based on the web site as

1. Sears Holdings consists of Kmart and Sears stores. Sears and Kmart operate over

2. In footnote 17 to the financial statement in the 10K report for 2011, the company

reports revenue, operating costs and expenses, operating profits (loss), total assets, and

3. The percent of selling and administrative costs allocated to segments with different

cost-allocation bases is:

Cost-Allocation Base Kmart Sears Domestic Sears Canada

Actual “bases” used 3,371 ÷ 10,664 = 32% 6,042 ÷ 10,664 = 57% 1,251 ÷ 10,664 = 12%