CHAPTER 3

SUPPLY AND DEMAND

QUESTIONS

1. Demand: Quantities of a good or service that people are ready to buy within a given time period

“Demand” encompasses all possible quantities demanded at different prices, while “quantity

2. Demand: 1) income; 2) tastes and preferences; 3) prices of related products; 4) future expectations;

3. An important part of the functioning of the market process is the determination of the price of a

4. Comparative statics analysis is an approach to studying a problem that is frequently used in

5. The rationing function involves the increase or decrease in price to clear the market of any shortage

or surplus. It is a function that takes effect in the short run in response to supply or demand

6. The guiding function takes effect in the long run. Resources are guided into or out of markets as a

Supply and Demand 9

7. Short Run, Producers’ Perspective: Time enough only to react to changes in demand (and price) by

changing their variable factors of production.

Short Run, Consumers’ Perspective: Time enough to react to changes in supply (and price) by

Long Run, Consumers’ Perspective: Time enough to react to changes in supply (and price) by

changing demand. (For example, if the price of gasoline rises, people will react in the long run by

8. From an economic standpoint, a shortage exists when the quantity demanded exceeds the quantity

Scarcity is a relative situation reflected in the market equilibrium price. For example, if the price of

We can use the contrast between the short run and long run market time periods (along with

* A late frost destroys a sizable proportion of the Florida orange crop. Supply for oranges shifts to

the left.

* As a result in the decrease in supply, a shortage is created at the existing market price for oranges.

* Because of the shortage, the price of oranges rises.

* This rise in the equilibrium price of oranges indicates to market participants that oranges are

scarcer.

9. It is important because it will help them to analyze what might be currently happening as well as

For example, suppose the managers of a firm that produces bottled water experience an unexpected

Copyright © 2014 Pearson Education, Inc.

Supply and Demand 10

10. We can use the actual example of the additional tax of 10 percent levied on luxury cars sold for

over $30,000. This tax certainly increases the actual price of the car to the consumer. Assuming a

It is also not certain whether the price will actually fall in the long run. Over time, the demand for

luxury cars might shift to the left but then again it might not. This is because in reality, all “other

11. Economists make the distinction between “demand” and “quantity demanded” in order to facilitate

the use of the supply and demand diagrams in explaining the rationing and guiding functions of

As instructors, we have noticed that economics texts books (particularly principles texts) greatly

12. (Other answers are possible for all of the following, given correct reasoning.)

a. Busier life styles, two-income families, single-parent households will continue to cause demand

b. Demand is already increasing drastically for goods purchased on the Internet and is posed to

e. Pay-per-view and satellite TV programs will continue to erode video rental demand.

f. Pay-per-view should increase as broader band connections to the home make this form of

g. Longer term trends point in an upward direction.

Copyright © 2014 Pearson Education, Inc.

Supply and Demand 11

h. It is difficult to tell, but if demand for SUV’s and trucks continues to rise, there will also be a

13. a. (1) Discovery of new sources of oil: supply increases. (2) Invention of new long-lasting battery

b. (1) Cattle ranching declines as it becomes harder to earn a good return in the market for beef (in

c. Increase in the building of new manufacturing facilities in Asian countries such as Taiwan—

d. Mergers and acquisitions in the hotel industry (could increase or decrease number of rooms—

e. U.S. or European based multinationals such as McDonald’s and Burger King build new

f. New co-branded cards are offered by financial institutions—supply increases.

g. More manufacturing, assembly and distribution capacity by key companies such as Dell,

h. More PC companies such as Dell and Compaq 2000 enter the server market or increase their

PROBLEMS

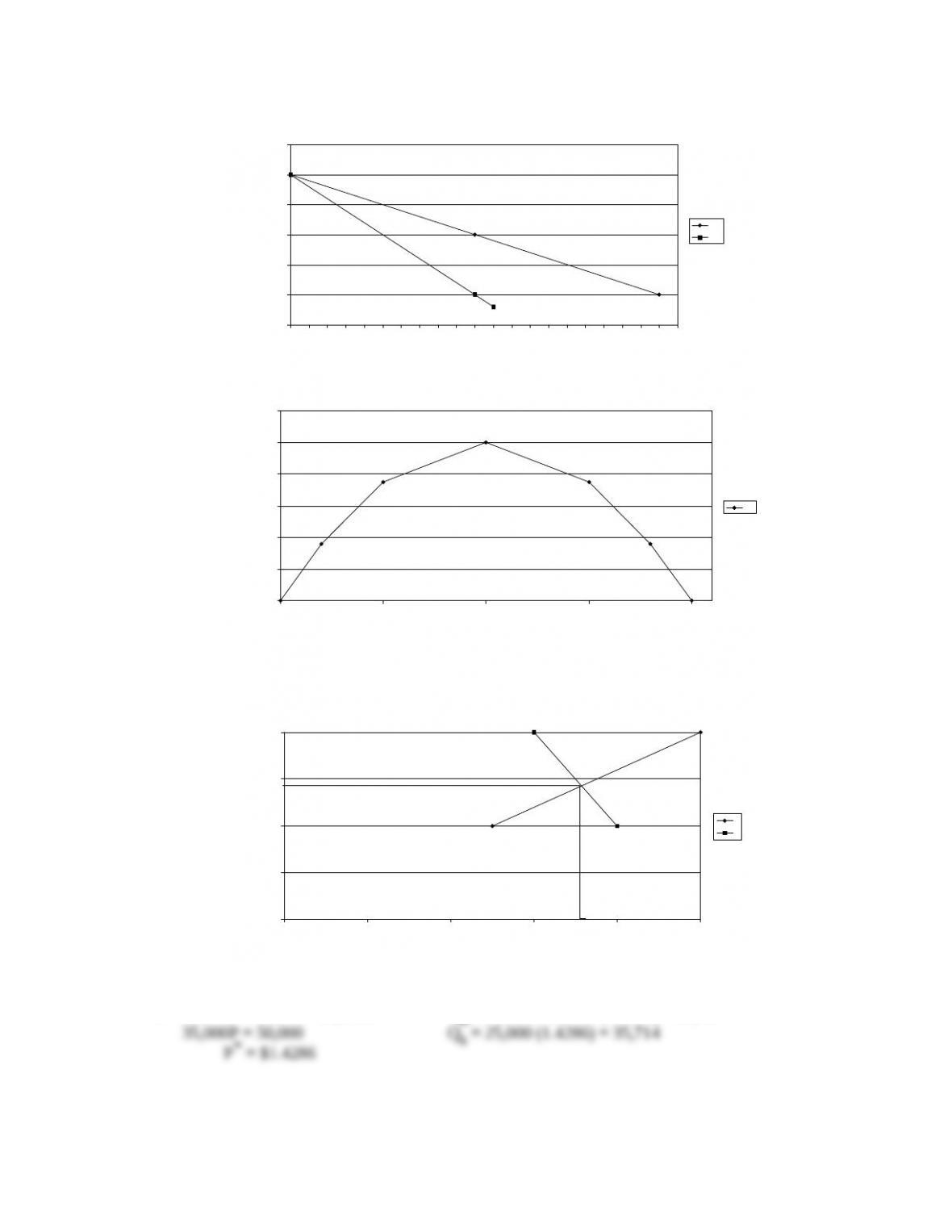

1. a. 800 caps

d. Note to Instructors: If you assign this question, be sure to point out to your students that the

Copyright © 2014 Pearson Education, Inc.

Supply and Demand 12

Figure 3.1

Figure 3.2

2. a.

Figure 3.3

b. 25,000P = 50,000 – 10,000P Qd = 50,000 – 10,000 (1.4286) = 35,714

Copyright © 2014 Pearson Education, Inc.

–5

0

5

10

15

20

25

0 500 1000 1500 2000

Q

$ P, MR

D

MR

0

2

4

6

8

10

12

0 500 1000 1500 2000

Q

$ (Thousands)

TR

0

0.5

1

1.5

2

0 10 20 30 40 50

Q (Thousands)

P ($)

S

D

P* = 1.4286

Q* = 35,714

(approx.)

0

50

100

150

200

250

300

350

0 500 1000 1500 2000 2500 3000 3500 4000

Q

P

D1

D2

S1

S2

Supply and Demand 13

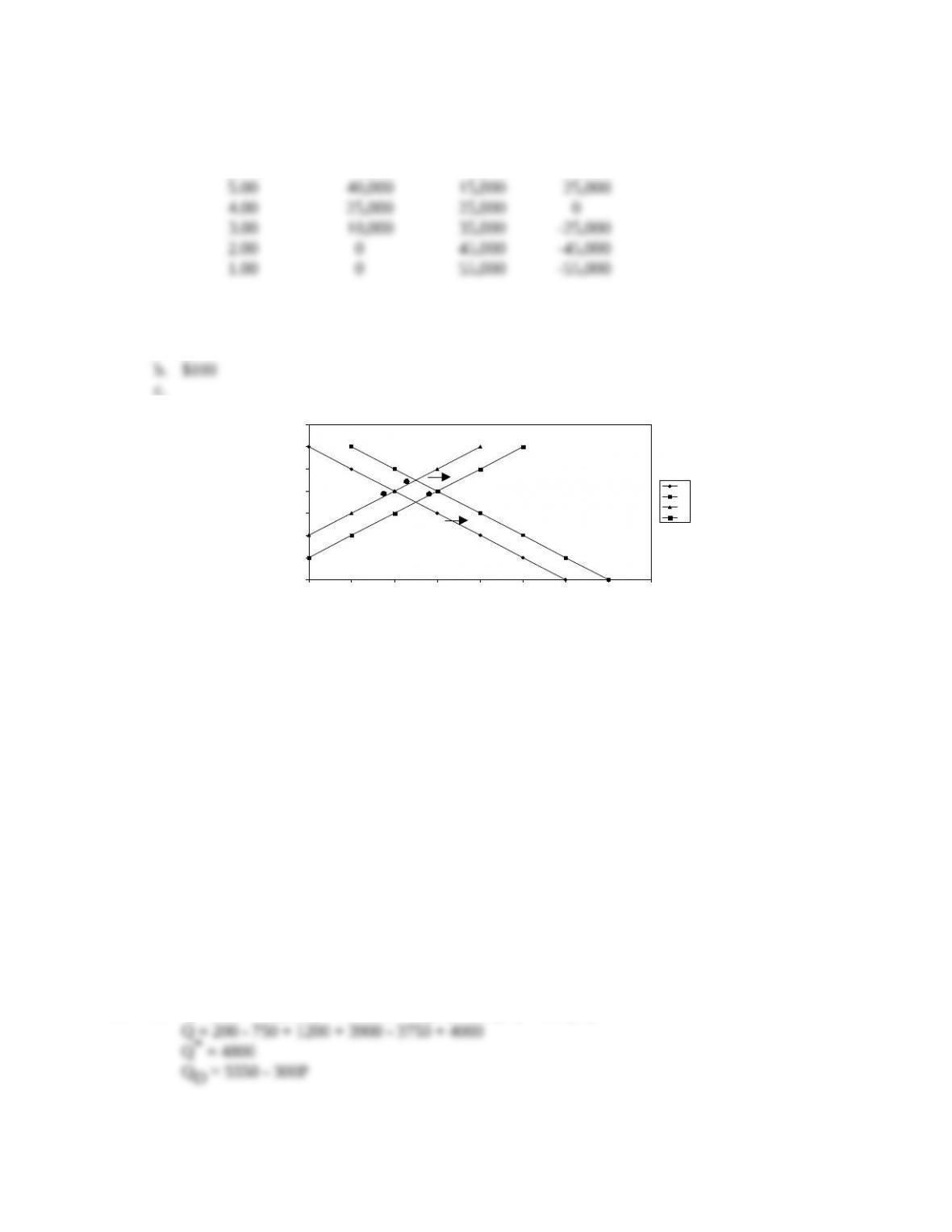

3. a. Surplus or

Price QSQDShortage

$6.00 55,000 5,000 50,000

b. Equilibrium price = $4.00 because it equates QD with QS.

4. a. $300

c.

Figure 3.4

d. P* = $200 Q* = 1000

e. P* = $225 Q* = 1250

f. P* = $200 Q* = 1500

g. See graph above

5. a. Q = 10,000 – 200P + .03(1,000,000) + .6(30,000) + .2(15,000)

QD = 61,000 – 200P

b. P QD

$200 000

175 26,000

150 31,000

125 36,000

c. P = $80.

6. a. Q = 200 – 300(2.50) + 120(10) + 65(60) – 250(15) + 400(10)

Copyright © 2014 Pearson Education, Inc.

Supply and Demand 14

7. Supply curve shifts to right and demand curve shifts to left. The combined shifts drastically reduced

the world market price for sugar.

Figure 3.5

8. The main cause for the increase in the demand for CDs is the decrease in the price of CD players,

9. (To Instructor: This problem is a precursor to the discussion of the elasticity concept, and could

be discussed in conjunction with Chapter 4.)

a. No, because point elasticity is -0.625.

b. Yes. Although the number of units sold would drop from 12,000 to 10,000, the combined

10. a. Q = 1,500 – 4(400) + 25(20) +10(15) + 3(500)

b. Advertising would have to increase by $60,000 in order for the firm to regain the loss of 300

c. The price of substitute products such as cruise packages.

Copyright © 2014 Pearson Education, Inc.

P

1

P

Q

P

2

S

1

S

2

D

1

D

2

Q

1

Supply and Demand 15

d. If time series data were collected on a quarterly basis, then seasonal factors such as summer or

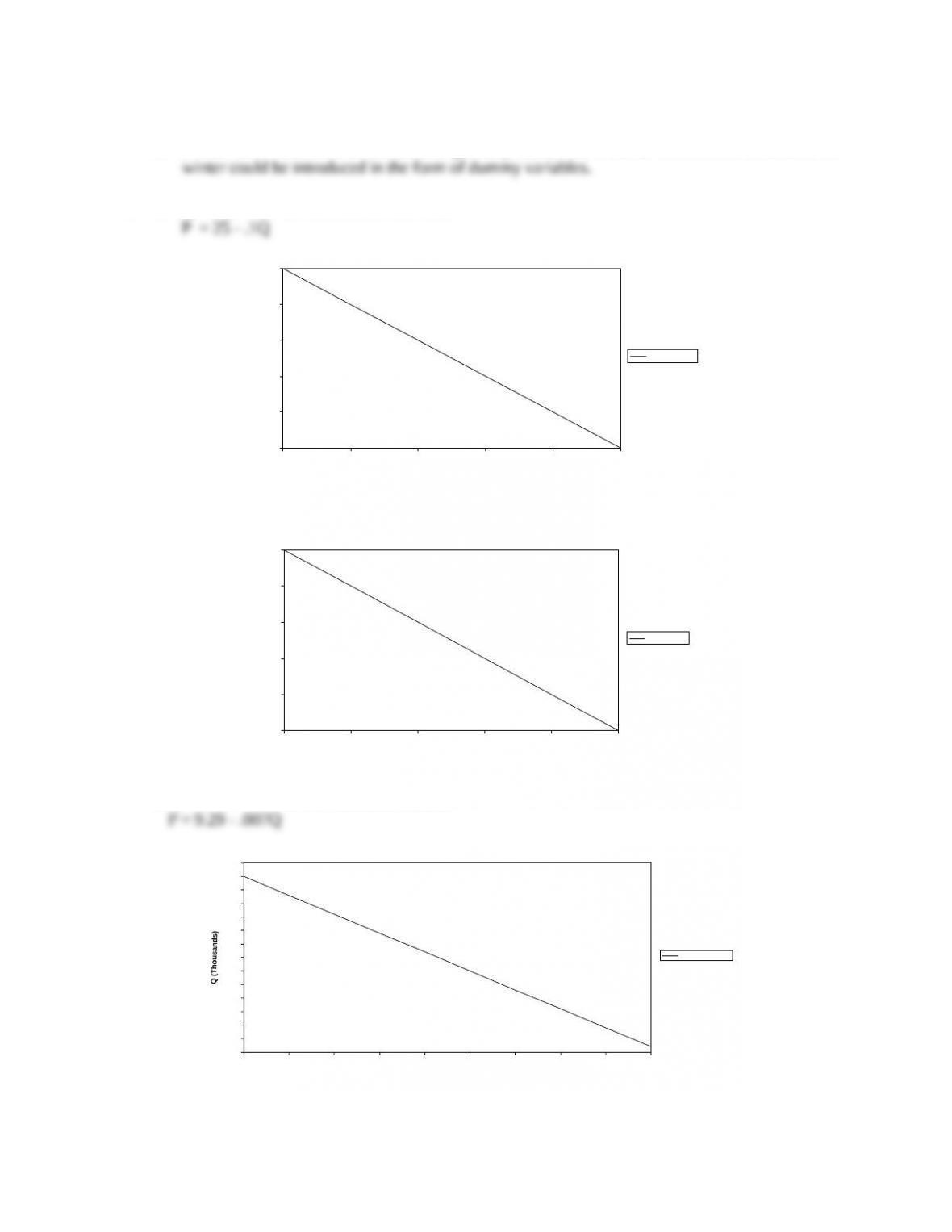

11. a. Q = 250 – 10P can be transformed into:

Figure 3.6

Figure 3.7

b.Q = 1300 – 140P can be transformed into:

Figure 3.8

Copyright © 2014 Pearson Education, Inc.

0

50

100

150

200

250

0 5 10 15 20 25

P

Q

Q = 250 – 10P

0

5

10

15

20

25

0 50 100 150 200 250

Q

P

P = 25 – .1Q

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

0 1 2 3 4 5 6 7 8 9

P

Q = 1300-140P

Supply and Demand 16

Figure 3.9

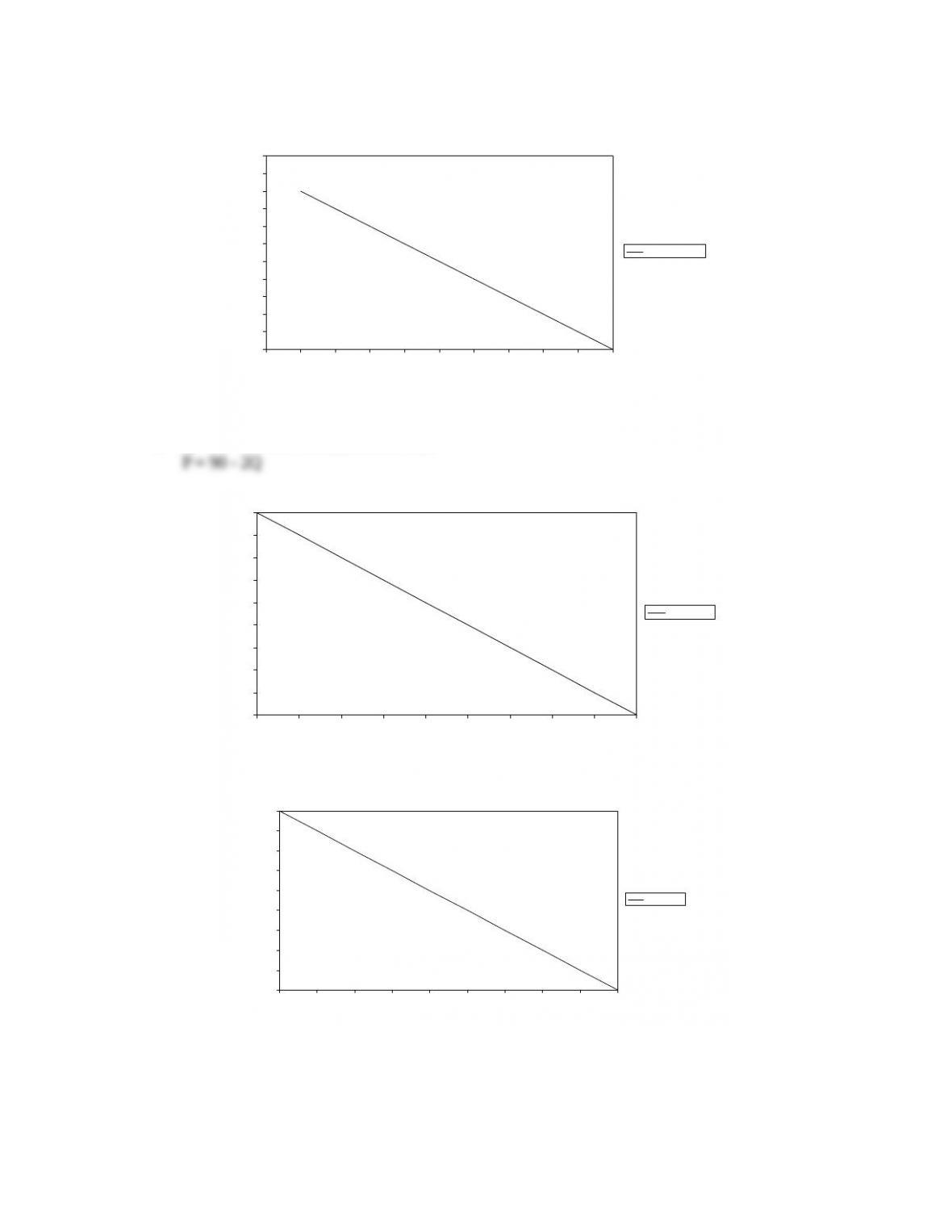

c. Q = 45 – .5P can be transformed into:

Figure 3.10

Figure 3.11

Copyright © 2014 Pearson Education, Inc.

0

1

2

3

4

5

6

7

8

9

10

11

0 40 180 320 460 600 740 880 1020 1160 1300

Q

P

P = 9.29 – .007P

0

5

10

15

20

25

30

35

40

45

0 10 20 30 40 50 60 70 80 90

P

Q

Q = 45 – .5P

0

10

20

30

40

50

60

70

80

90

0 5 10 15 20 25 30 35 40 45

Q

P

P = 90 – 2Q

Supply and Demand 17

12.

Figure 3.12

Certain consumer electronics products could exhibit this type of demand. This curve indicates that

13. The Problem:

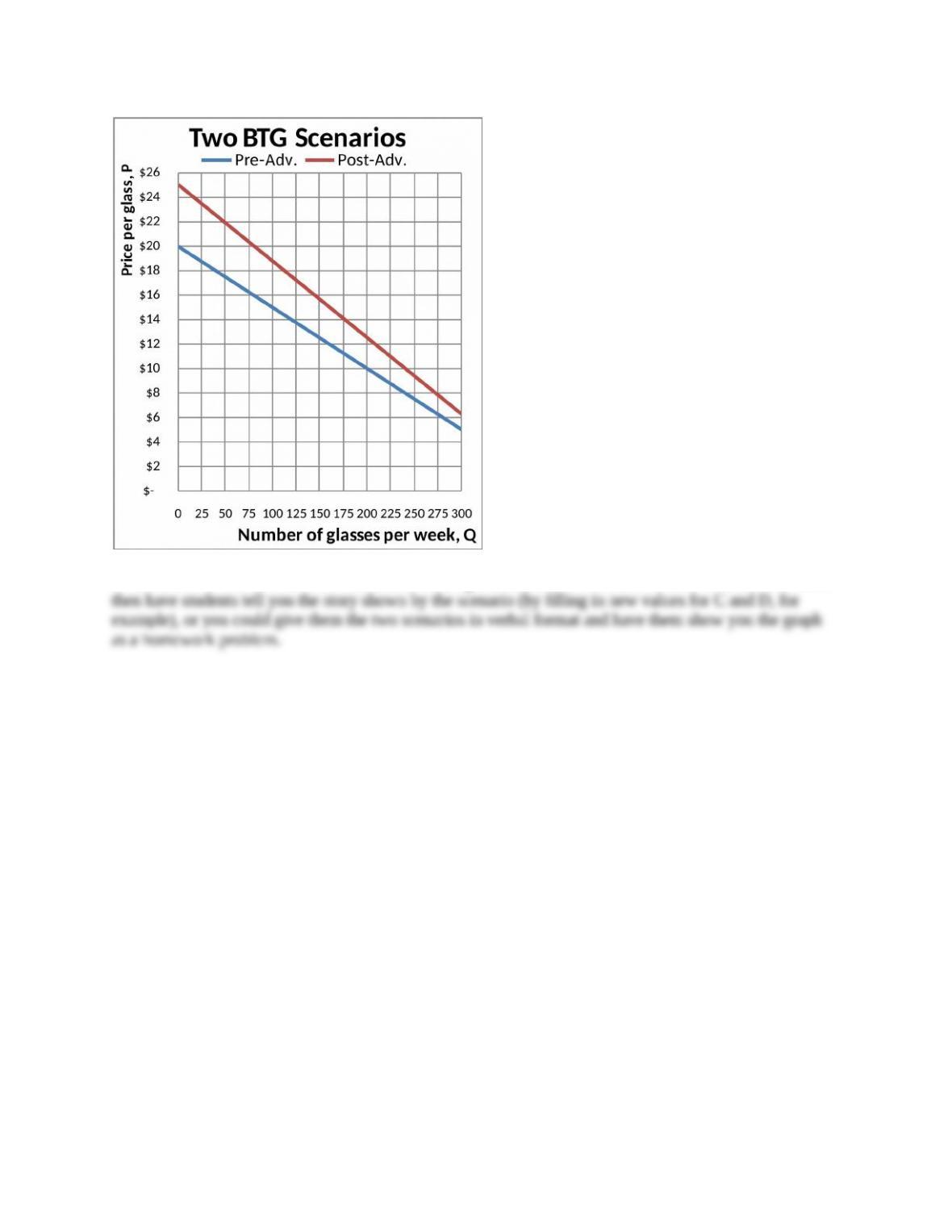

a. Found in the graph itself and in the equation found in cells A6 and A7: P = 20 – 0.5Q

One final scenario: Cells D2=200, D3=12.5, D4=-16.

Copyright © 2014 Pearson Education, Inc.

0

1

2

3

4

5

6

7

8

9

10

11

0 50 100 150 200 250 300 350 400

Q

P

Supply and Demand 18

NOTE TO INSTRUCTORS: You can use the Multiple Demands worksheet to create new scenarios and

Copyright © 2014 Pearson Education, Inc.