Solutions to the End-of-Chapter Questions, Problems, and Data

Exercises

9.1 Obstacles to Matching Savers and Borrowers

Learning objective: Analyze the obstacles to matching savers and borrowers.

Review Questions

1.1 Transactions costs are the costs of a trade or an exchange. Information costs are the costs that savers

1.2 Financial intermediaries, such as commercial banks and mutual funds, channel funds from savers

Problems and Applications

1.3 Financial intermediaries are able to take advantage of economies of scale, such as standardized legal

contracts, specialized loan officers, and sophisticated computer systems, to reduce transactions and

1.4 The Internet has reduced information and transactions costs. The Internet allows many financial

1.5 Writing bank records in ledgers would not have had significant economies of scale because bank

workers would have written in ledgers one by one and there would be little average cost reduction in

9.2 The Problems of Adverse Selection and Moral Hazard

Learning objective: Explain the problems that adverse selection and moral hazard pose for the financial

system.

Review Questions

2.1 Adverse selection is the problem investors experience in distinguishing low-risk borrowers from

Because potential investors have difficulty in distinguishing good borrowers from bad

© 2014 Pearson Education, Inc.

Chapter 9 Transactions Costs, Asymmetric Information, and the Structure of the Financial System 107

2.2 The Securities and Exchange Commission (SEC) is a federal government agency that regulates

U.S. stock and bond markets. The SEC’s primary role is to reduce adverse selection by requiring

2.3 Relationship banking is the ability of banks to assess credit risks on the basis of private information

2.5 Venture capital firms raise funds from investors to invest in start-up firms. Private equity firms raise

Problems and Applications

2.6 a. Yes. Landlords know more about the quality of the property, and therefore its true value, than

b. Landlords with bad apartments will attempt to charge a higher price than they otherwise would

receive in the absence of this information asymmetry, while landlords with good apartments will

c. The rental property market and the used car market are similar in that the landlord and the current

car owner know more about the property or the car than the potential renter or buyer. However, the

2.7 The asymmetric problem in this used car example is adverse selection. It is likely that only a lemon

2.8 a. The problem is adverse selection.

b. The consequences will be that healthy people will have difficulty buying insurance at a reasonable

2.9 a. Banks would be reluctant to lend to startups for two key reasons: 1) There is substantial risk that

© 2014 Pearson Education

Chapter 9 Transactions Costs, Asymmetric Information, and the Structure of the Financial System 108

b. Startups might have an easier time obtaining equity investments from small investors through

2.10 When buying a used car, buyers should always be aware of information asymmetry. The seller

2.11 a. Securitization is the process of combining (bundling) loans, such as mortgages, into securities that

b. When the loans are bundled together and sold off, the bank that issued the loan doesn’t bear the cost

c. The investors did not know that the securities contained bad commercial real estate loans. It is

2.12 You should agree. Only the most financially sound firms are likely to take advantage of the offer. As

2.13 Moral hazard is less likely to be a problem in scenario (b), because when a manager receives a

2.14 a. Stock options provide an incentive for the managers to make decisions that increase the stock’s

b. The exercise price is the price at which the buyer of an option has the right to buy or sell the

c. The information problem involves the principal-agent problem, which is the moral hazard problem

2.15 a. Unlike crowd-funding sites, venture capital funds often take a large ownership stake in a startup firm

b. Crowd-funding sites reduce the transactions costs faced by small investors who want to make equity

investments in startups by acting as a financial intermediary. The crowd-funding sites identify

9.3 Conclusions About the Structure of the U.S. Financial System

© 2014 Pearson Education

Chapter 9 Transactions Costs, Asymmetric Information, and the Structure of the Financial System 109

Learning objective: Use economic analysis to explain the structure of the U.S. financial system.

Review Questions

3.1 The owners’ personal funds and profits are the primary sources of funds for small- to medium-sized

3.3 The three key features are: 1) Loans from financial intermediaries are the most important external

source of funds for small to medium sized firms. Financial intermediaries can reduce the transaction

Problems and Applications

3.4 Insurance companies don’t offer income insurance of this type for two key reasons: 1) Moral

3.5 Being honest would not eliminate the need for financial intermediaries. In a world of perfect

3.6 Asymmetric information makes information costs for external funds higher than for internal funds.

Information costs do not necessarily imply that firms are able to spend less on expansion than is

3.7 a. Investment-grade corporate bonds are not free of default risk. These bonds had less default risk in

3.8 The more complex the product, the more difficult it is for an investor to assess the risk of the product.

When investors buy simpler products, they typically have more information and can make more

Data Exercise

© 2014 Pearson Education

Chapter 9 Transactions Costs, Asymmetric Information, and the Structure of the Financial System 110

D9.1 ScottTrade: $7. Ameritrade: $9.99 E-TRADE: $9.99. With only $200 to invest and a 5% rate of

D9.2

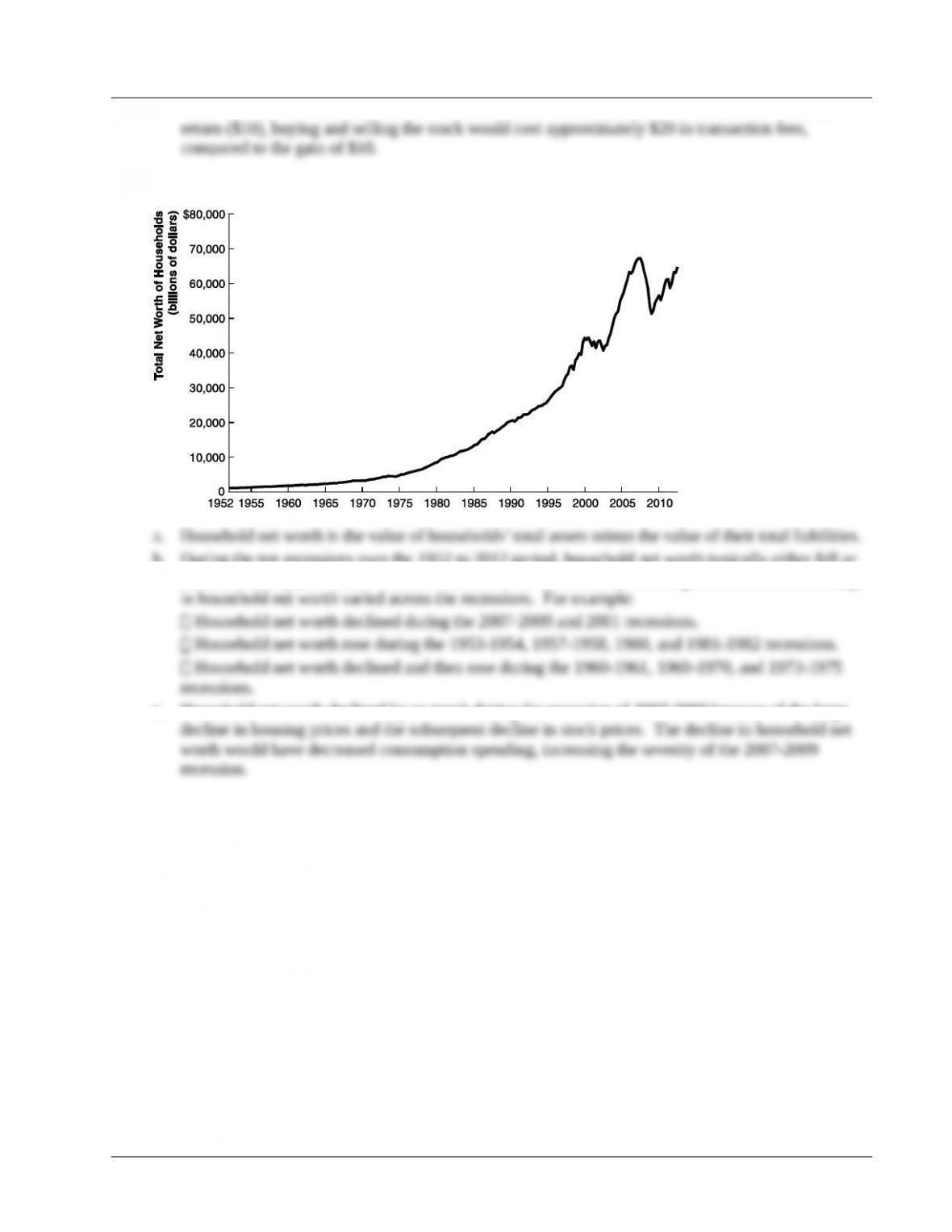

b. During the ten recessions over the 1952 to 2012 period, household net worth typically either fell or

increased slowly just before a recession and rose after a recession. During the recession, the change

c. Household net worth declined by so much during the recession of 2007-2009 because of the large

D9.3

© 2014 Pearson Education

Chapter 9 Transactions Costs, Asymmetric Information, and the Structure of the Financial System 111

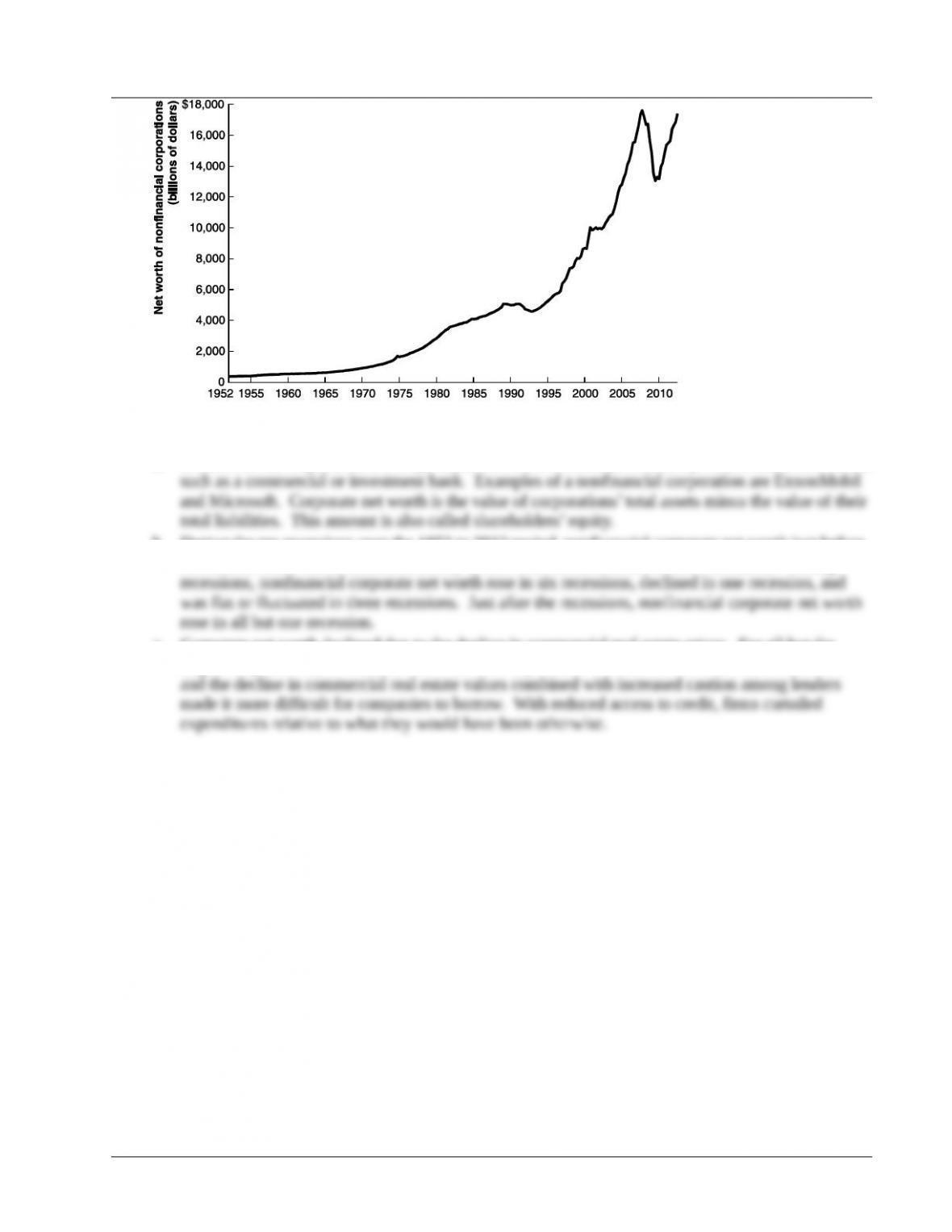

a. A nonfinancial corporation is a corporation that is not a financial firm that provides financial services

b. During the ten recessions over the 1952 to 2012 period, nonfinancial corporate net worth just before

a recession either fell or increased slowly in five recessions, and rose in five recessions. During

c. Corporate net worth declined due to the decline in commercial real estate prices. For all but the

largest corporations, commercial real estate is a key source of collateral. The decline in net worth

© 2014 Pearson Education