Solutions to the End-of-Chapter Questions, Problems, and Data

Exercises

7.1 Derivatives, Hedging, and Speculating

Learning objective: Explain what derivatives are and distinguish between using them to hedge and using

them to speculate.

Review Questions

1.1 Derivatives allow investors to hedge the risk of price changes in underlying assets. Derivatives also

1.2 Hedging is an action to reduce risk, such as purchasing a derivative contract that will increase in

Problems and Applications

1.3 Speculators play two important roles in derivatives markets: 1) Speculators accept risk transferred

1.4 a. The risk involves falling corn prices. The derivative would need to increase in value if corn prices

fall.

7.2 Forward Contracts

Learning objective: Define forward contracts.

Review Question

2.1 Forward contracts give firms and investors an opportunity to hedge the risk on transactions that

2.2 The person or firm on the other side of the forward contract, the counterparty, may be unable or

Problems and Applications

2.3 You could enter into a forward contract to sell oil at some settlement date in the future. If the price

2.4 The buyer in the oil forward contract has an incentive to default because he or she has to buy oil at

7.3 Futures Contracts

© 2014 Pearson Education, Inc.

Chapter 7 Derivatives and Derivative Markets 80

Learning objective: Discuss how futures contracts can be used to hedge and to speculate.

Review Questions

3.1 Futures contracts are traded on exchanges, have a price that changes as a result of trading until the

settlement date, and are standardized in terms of the quantity of the underlying asset to be delivered

and the settlement dates for the available contracts. Futures contracts lack the flexibility of forward

3.2 No. If a firm has a long position in the spot market, then to hedge risk it must take a short position

3.3 Hedging is an action to reduce risk, such as purchasing a derivative contract that will increase in

value when another asset in an investor’s portfolio decreases in value. Speculating is placing a

Problems and Applications

3.4 Futures markets originated in agriculture because the supply of agricultural products depends on

weather and can therefore be subject to wide fluctuations. With demand for agricultural products

3.5 You should disagree. As explained on page 194 of the text, forward contracts have fixed forward

prices, but futures contracts do not. The price in a futures contract fluctuates as the contract is

3.6 a. A long position in the futures market is the buying of futures contracts.

b. Speculators because they were betting that coffee prices would rise. They had been buyers of coffee

3.7 Hedging is taking a long or a short position on a commodity or financial asset to reduce risk. Airlines

hedge against rising oil costs by buying oil futures contracts. If oil prices increase, the airlines offset

© 2014 Pearson Education, Inc.

Chapter 7 Derivatives and Derivative Markets 81

3.9 a. The farmer would want to sell wheat futures. The farmer would sell 10 contracts. The contracts in

b. In November, the farmer closes his position in the futures market by buying back the contracts at the

3.10 a. “Roil” in this context means to dramatically change the market price.

3.12 a. Using the last price of $108 and 18.5/32 or $108.578125 per $100 face value for two contracts, you

would have paid $108.578125 1,000 2 $217,156.25.

3.13 a. You would be worried more about rising interest rates because rising interest rates would cause a

3.14 Volatility in onion prices is driven by changes in the demand and supply for onions, so it is unlikely

7.4 Options

Learning objective: Distinguish between call options and put options and explain how they are used.

Review Questions

4.1 A call option is a derivative contract that gives the buyer the right to buy the underlying asset at a set

4.2 With futures contracts, buyers and sellers have symmetric rights and obligations. In contrast, with

options contracts, the buyer has rights, and the seller has obligations. For example, if the buyer of a

© 2014 Pearson Education, Inc.

Chapter 7 Derivatives and Derivative Markets 82

4.3 The options premium is the price of an option. The option’s intrinsic value is the payoff to the buyer

4.4 Options can be used to hedge risk against commodity price, stock price, interest rate, or foreign

Problems and Applications

4.5 a. A put option is a derivative contract that gives the buyer the right to sell the underlying asset at a set

b. By having the right to sell the stock at the strike price, the investor can ensure that he or she will still

4.6 a. With a put option, the investor can sell at the strike price if stock prices fall.

b. A put option provides insurance against a decline in stock prices, while allowing you to still gain if

c. “Exposure” to the stock market means the chance of realizing gains or losses in stock prices. The put

4.7 Disagree. An investor will maximize her investment in a put option with a strike price of $25 when

b. The put option is out of the money (the strike price of $18 is below the market price of $21.95), so

© 2014 Pearson Education, Inc.

Chapter 7 Derivatives and Derivative Markets 83

4.9 Volatility is an important part of the Black-Scholes options pricing model. The lower the volatility,

4.10 A bullish approach means that investors are expecting prices to go higher and are betting on this by

Investors purchased considerably more call options than put options, indicating a bullish view on

4.11 Investors who had bought put options would have made the greatest profit because the strike price in

the puts is likely to be well above the current market prices of the stocks the put options were written

4.12 The VIX provides a measure of investors’ expectations of the future volatility of stock prices. The

7.5 Swaps

Learning objective: Define swaps and explain how they can be used to reduce risk.

Review Questions

5.1 A swap is an agreement between two or more counterparties to exchange sets of cash flows over some

future period. A swap is different from a futures contract because as a private agreement between

5.2 An interest-rate swap is a contract under which counterparties agree to swap interest payments over

a specified period on a fixed dollar amount, called the notional principle. A credit swap is a contract

5.3 A credit default swap is a derivative that requires the seller to make payments to the buyer if the price of

the underlying security declines in value. Unlike the other swap contracts discussed in this chapter,

Problems and Applications

5.4 a. An increase in inflation causes nominal interest rates to increase as shown by the Fisher effect

© 2014 Pearson Education, Inc.

Chapter 7 Derivatives and Derivative Markets 84

b. The bank could enter into an interest-rate swap contract under which the interest

5.5 Credit default swaps insure the value of the underlying security. The buyer pays premiums to the

5.7 a. Over-the-counter means that the derivative is not sold on an exchange. Instead, the derivative

b. The broader system means those outside the over-the-counter transaction who may be

c. Over-the-counter derivatives are generally less regulated, less standardized, and less

liquid than other assets. Because over-the-counter markets do not collect information or

5.8 a. Counterparty risk is the risk of the other party to the transaction defaulting.

b. Counterparty risk is greater for derivatives because the transaction is only completed

5.9 It depends on the derivative. Those derivatives that are not standardized or traded on exchanges or

© 2014 Pearson Education, Inc.

Chapter 7 Derivatives and Derivative Markets 85

Data Exercises

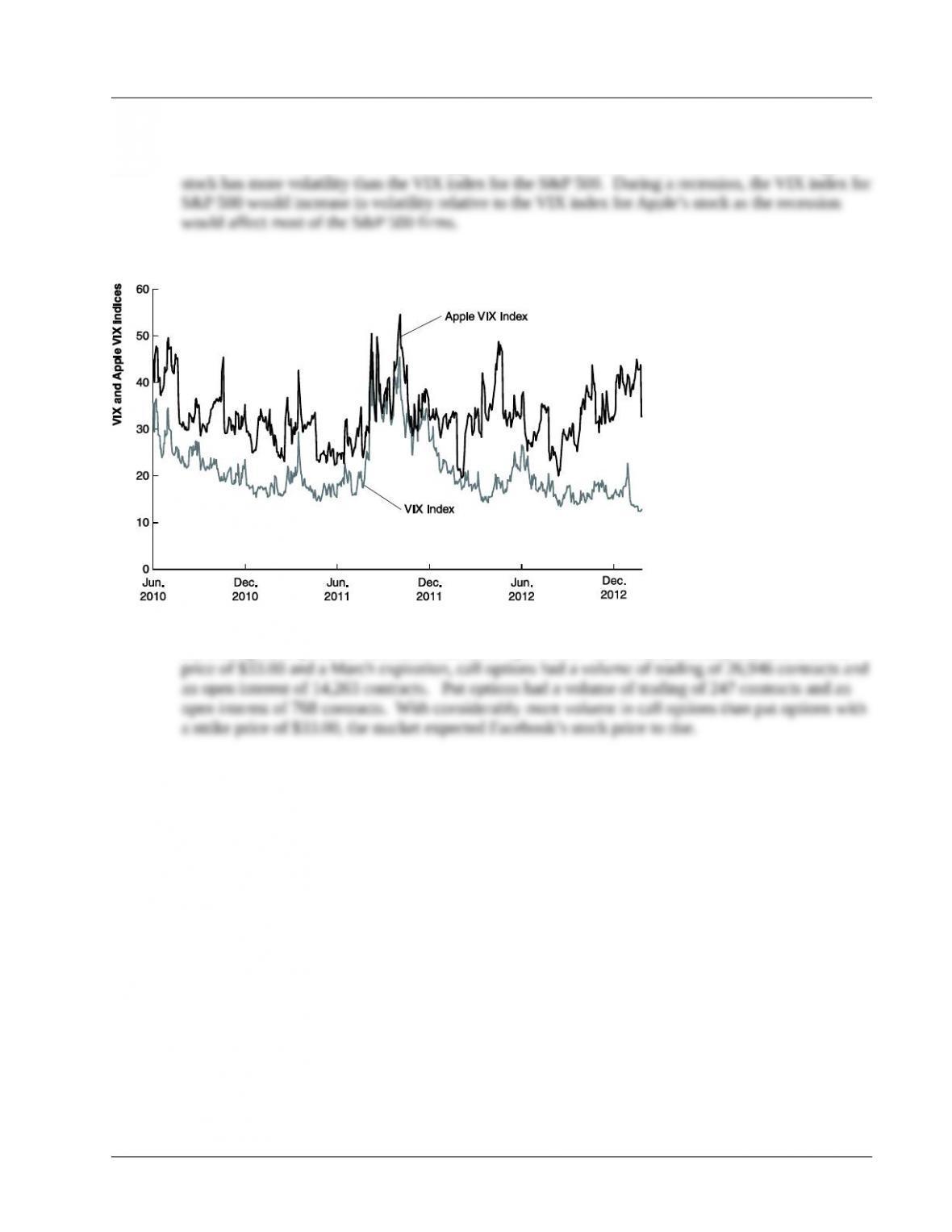

D7.1. The data series for the VIX index for Apple’s stock starts on June 2010. The VIX index for Apple’s

D7.2. Answers will vary by the date on when options quotes are examined. On Friday, January 25, 2013,

the closing stock price for Facebook was $31.54 per share. On Monday, January 28, with a strike

© 2014 Pearson Education, Inc.