15.3 More on the Fed’s Monetary Policy Tools

Learning objective: Trace how the importance of different monetary policy tools has changed over

time.

Review Questions

3.1 An open market sale of Treasury securities decreases the price of Treasury securities, thereby

3.2 Open market operations have the advantages over other policy tools of control, flexibility, and

Fed can make both large and small open market operations, and the Fed can easily implement

3.3 To stimulate the economy, the Fed had already pushed the federal funds rate to near zero by

December 2008. But the economy continued to struggle and the Fed wanted to put further

3.4 Before 1980, only member banks of the Federal Reserve System could receive discount loans.

After 1980, all depository institutions could receive discount loans. During the financial crisis

Problems and Applications

3.5 To hit the target federal funds rate, the account manager adjusts the supply of reserves by using

3.6 a. The Fed’s policy rate is the federal funds rate. “Policy rate” is a general term used to refer to

b. Additional easing refers to additional quantitative easing.

c. The author means that additional monetary easing will not stimulate the economy.

Additional monetary easing will have no more effect than pushing on a string. Economists

d. Answers can vary. Additional quantitative easing will have limited effects in lowering

long-term interest rates, but increases in the monetary base and the money supply have other

3.7 a. Bernanke uses the term monetary accommodation to mean the near zero federal funds rate,

b. Bernanke uses the term easing financial conditions to mean restoring the flow of funds

c. Fed Chairman Bernanke’s letter to Congress mentions three channels the Fed used to ease

financial conditions:

1. Reducing the cost of capital to businesses by reducing interest rates, reducing credit

2. Boosting the aggregate wealth of U.S. households by supporting the housing market

3. Improving the competitiveness of U.S. businesses by allowing businesses to access

3.8 By increasing the interest rate it pays on bank reserves, the Fed can increase the level of

reserves banks are willing to hold, thereby restraining bank lending and increases in the money

3.9 You should disagree. The Fed does not set the federal funds rate. The federal funds rate is

3.10 a. The implications of some financial institutions being able to borrow and lend in the federal

b. If only banks could borrow and lend in the federal funds market, then the actual federal

3.11 The Primary Dealer Credit Facility was designed to help primary dealers—the financial firms

The Term Securities Lending Facility was designed to help financial firms by providing loans of

Treasury securities in exchange for mortgage-backed securities.

The Commercial Paper Funding Facility was designed to help nonfinancial corporations that

The Term Asset-Backed Securities Loan Facility was designed to help firms that raised funds

15.4 Monetary Targeting and Monetary Policy

Learning objective: 15.4: Explain the role of monetary targeting in monetary policy.

Review Questions

4.1 The Fed often faces the key tradeoff between price stability and maximum employment. For

4.2 The two timing difficulties the Fed faces in using its monetary policy tools are the information

4.3 The following is a list of targets, or variables, that the Fed can influence directly. The targets

are listed from the most influence to the least influence:

4.4 The Taylor rule is a monetary policy guideline economist John Taylor developed to help analyze

how the Fed chooses the target for the federal funds rate. The Taylor rule serves as a summary

4.5 The Bank of Canada uses inflation targeting and a focus on the exchange value of the Canadian

dollar. The Bank of England uses inflation targeting. The Bank of Japan has not adopted a

Problems and Applications

4.6

a. M2 is an intermediate target.

b. The monetary base is an intermediate target.

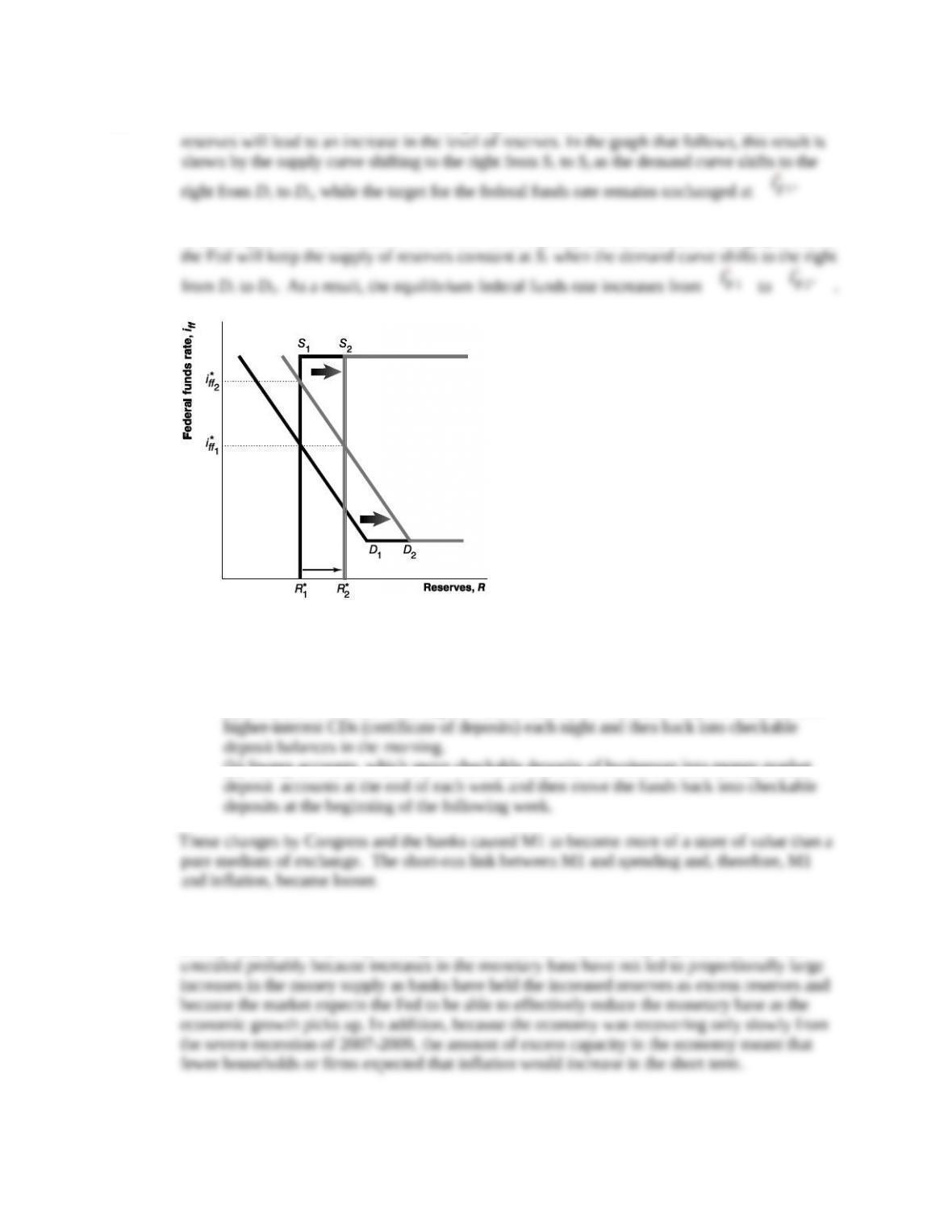

4.7 If the Fed uses the federal funds rate as a policy instrument, then increases in the demand for

Conversely, if the Fed uses the level of reserves as a policy instrument, then in the graph below,

4.8 The following legislative changes and financial innovations occurred after 1979:

1. Congress authorized NOW (negotiable order of withdrawal) accounts on which banks can

pay interest

2. Banks introduced two innovations:

(a) Automated transfer of saving accounts, which move checkable deposit balances into

(b) Sweep accounts, which move checkable deposits of businesses into money market

4.9 a. Increases in the Fed’s balance sheet increase the monetary base and typically increase the

money supply, subsequently causing increased inflation. Inflationary expectations were not

b. Bernanke’s “open-ended round of quantitative easing” refers to a third round of

quantitative easing (QE3), where the Fed pledged to continue purchases of mortgage-backed

4.10 You should agree. The Fed cannot target—which would appear to be what the authors mean by

“manage”—both the level of reserves and the federal funds rate. If the Fed targets the federal

4.11 Using the equation found on page 474 of the text, the Taylor rule federal funds rate target 2%

4.12 a. The Federal Open Market Committee (FOMC) kept the federal funds rate at levels well below

b. Low interest rates encouraged subprime borrowers (borrowers with flawed credit

histories) and Alt-A borrowers (borrowers who did not document their incomes) to acquire

Data Exercises

D15.1 The answers below apply to the Federal Open Market Committee (FOMC) press release of

January 30, 2013.

a. The FOMC did not change the target for the federal funds rate. It kept the target range for

the federal funds rate at 0 to 0.25%.

d. The Fed announced that it would continue purchasing agency mortgage-backed securities

at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45

billion per month. In other words, the Fed would continue quantitative easing. The Fed

D15.2

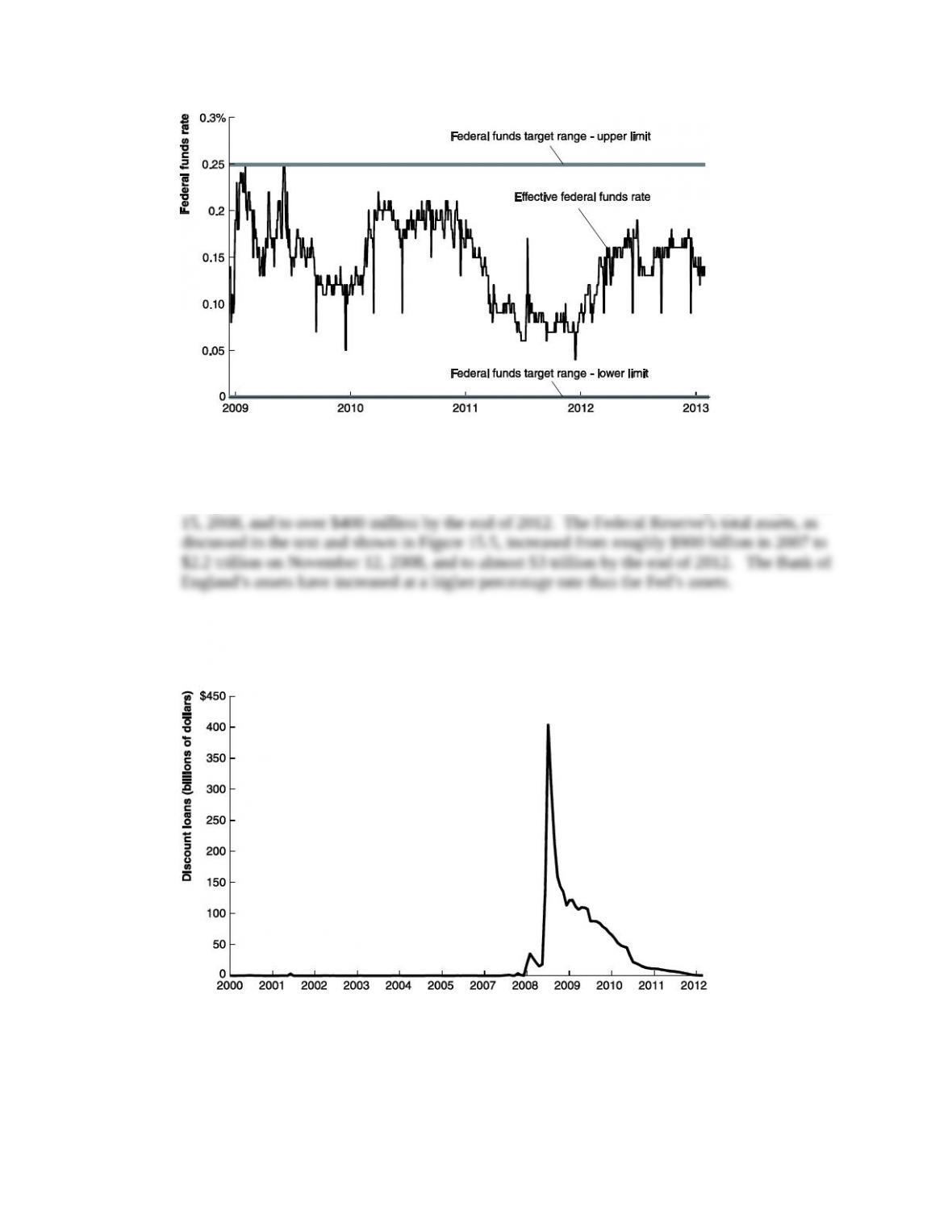

Over this period, the Fed kept the target range for the federal funds rate unchanged at 0-0.25%. Over the

period, the Fed was able to keep the effective federal funds rate within the target range.

D15.3 The Bank of England’s total assets increased from almost $100 million at the end of 2007 to

nearly $300 million on October 22, 2008 after the Lehmann Brothers bankruptcy on September

D15.4

Before the financial-crisis, discount loans were generally below $1 billion. Based only on the data for the