Chapter 15

Monetary Policy

Brief Chapter Summary and Chapter Objectives

15.1 The Goals of Monetary Policy (pages 448–451)

Describe the Goals of Monetary Policy.

15.2 Monetary Policy Tools and the Federal Funds Rate (pages 451–459)

Understand how the Fed uses monetary policy tools to influence the federal funds rate.

Although the Fed sets a target for the federal funds rate, the actual rate is determined by the

interaction of the demand and supply for bank reserves in the federal funds market.

15.3 More on the Fed’s Monetary Policy Tools (pages 459–467)

Trace how the importance of different monetary policy tools has changed over time.

Open market operations have traditionally been the Fed’s preferred tool in conducting monetary policy.

15.4 Monetary Targeting and Monetary Policy (pages 468–480)

Explain the role of monetary targeting in monetary policy.

Traditionally, the Fed has relied on two types of targets:

1. Policy instruments, sometimes called operating targets

2. Intermediate targets

Targeting is no longer the Fed’s favored approach.

© 2014 Pearson Education, Inc.

185 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

Key Terms and Concepts

Chapter Outline

Teaching Tips

This chapter brings together a number of the topics covered in earlier chapters as part of an integrated

discussion of monetary policy. The chapter provides an overview of the Fed’s monetary policy tools,

including the Fed’s heavy use of discount lending during the financial crisis of 2007-2009. The chapter

uses a graph of the demand and supply for reserves in the federal funds market to illustrate many key

points (see Figure 15.1 on page 453 for the basic graph). The chapter includes a discussion of the

debate over the Fed’s choice of targets. Particularly useful here is the Making the Connection that

begins on page 470, which discusses the exchange during the 1980s between Milton Friedman and

Benjamin Friedman over the link between the growth of the money supply and the inflation rate. The

chapter concludes with a discussion of monetary policy in other high-income countries.

Bernanke’s Dilemma

During the financial crisis of 2007–2009, the Fed undertook extraordinary policy actions to keep the

financial system from imploding. Unfortunately, as Fed Chairman Ben Bernanke testified before Congress

in late July 2012, the economy was recovering at a slower rate than the Fed had hoped.

15.1 The Goals of Monetary Policy (pages 448–451)

Learning Objective: Describe the Goals of Monetary Policy.

The Fed has six monetary policy goals that are intended to promote a well-functioning economy.

A. Price Stability

Inflation, or persistently rising prices, erodes the value of money as a medium of exchange and

B. High Employment

© 2014 Pearson Education, Inc.

Discount policy The policy tool of setting the

discount rate and the terms of discount lending.

Discount window The means by which the Fed

makes discount loans to banks, serving as the

channel for meeting the liquidity needs of banks.

Economic growth Increases in the economy’s

output of goods and services over time; a goal of

monetary policy.

Federal funds rate The interest rate that banks

charge each other on very short-term loans;

determined by the demand and supply for

reserves in the federal funds market.

Open market operations The Federal Reserve’s

purchases and sales of securities, usually U.S.

Treasury securities, in financial markets.

Primary credit Discount loans available to healthy

banks experiencing temporary liquidity problems.

Quantitative easing A central bank policy that

attempts to stimulate the economy by buying

long-term securities.

Reserve requirement The regulation requiring

banks to hold a fraction of checkable deposits as

vault cash or deposits with the Fed.

Seasonal credit Discount loans to smaller banks

in areas where agriculture or tourism is important.

Secondary credit Discount loans to banks that are

not eligible for primary credit.

Taylor rule A monetary policy guideline

developed by economist John Taylor for

determining the target for the federal funds rate.

Chapter 15 Monetary Policy 186

High employment, or a low rate of unemployment, is another key monetary policy goal.

C. Economic Growth

Economic growth provides the only source of sustained real increases in household incomes.

D. Stability of Financial Markets and Institutions

The stability of financial markets and institutions makes possible the efficient matching of

E. Interest Rate Stability

Like fluctuations in price levels, fluctuations in interest rates make planning difficult for

F. Foreign-Exchange Market Stability

G. The Fed’s Dual Mandate

15.2 Monetary Policy Tools and the Federal Funds Rate (pages 451–459)

Learning Objective: Understand how the Fed uses monetary policy tools to influence the federal

funds rate.

The Fed’s traditional policy tools include open market operations, discount policy, and reserve

requirements. During the financial crisis, the Fed added new tools including paying interest on

reserve balances and the term deposit facility.

A. The Federal Funds Market and the Fed’s Target Federal Funds Rate

Although the Fed sets a target for the federal funds rate, the actual rate is determined by the

Teaching Tips

It may prove helpful to spend a little extra time developing the graph of the federal funds market, Figure 15.1,

“Equilibrium in the Federal Funds Market,” on page 453. Students can easily gloss over it and treat it as a

standard supply and demand graph (that is, a graph with an upward sloping supply curve). You can help

students understand the graph by making it clear that the supply curve is vertical because the Fed controls the

volume of reserves, which makes the supply of reserves independent of the federal funds rate. Also, carefully

explain the reasoning behind the horizontal portions of each curve to help students gain a better

understanding of the unique shapes of the demand and supply for reserves.

© 2014 Pearson Education, Inc.

187 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

B. Open Market Operations and the Fed’s Target for the Federal Funds Rate

The Fed uses open market operations to hit its target for the federal funds rate. An open market

purchase increases the supply of reserves, which decreases the federal funds rate.

C. The Effect of Changes in the Discount Rate and in Reserve Requirements

Typically, the Fed has raised or lowered the discount rate at the same time that it raises or lowers

the target for the federal funds rate. As a result, changes in the discount rate have no

independent effect on the federal funds rate. The Fed rarely changes the required reserve ratio.

If the other factors underlying the demand and supply curves for reserves are held constant, an

increase in the required reserve ratio increases the demand for reserves because banks have to

hold more reserves, resulting in a higher federal funds rate.

15.3 More on the Fed’s Monetary Policy Tools (pages 459-467)

Learning Objective: Trace how the importance of different monetary policy tools has changed over time.

A. Open Market Operations

When the Fed carries out an open market purchase of Treasury securities, the prices of these

Teaching Tips

Though the first round of quantitative easing was generally supported by most economists, the second and

third rounds announced in November 2010 and September 2012, respectively, were more controversial.

Opponents of quantitative easing see it as a new approach to monetary policy with the risk of

significantly increasing inflation without effectively stimulating economic growth. Some of these

opponents see the policy as monetizing the national debt.

Supporters of quantitative easing argue that it is an extension of the traditional use of open market

operations that the Fed routinely uses to stimulate the economy when it is perceived to be too weak.

The difference is that, typically, open market operations focus on the federal funds rate. In this case,

because the federal funds rate was already near zero, the Fed focused on reducing long-term interest rates.

A potentially worthwhile classroom exercise is to have a brief—10 to 15 minute—debate between two

groups of students: One group is charged with defending quantitative easing, while the other group is

charged with presenting the opposing case.

B. Discount Policy

Since 1980, all depository institutions have had access to the Fed’s discount window. The Fed’s

discount loans to banks fall into three categories:

1. Primary credit, which is available to healthy banks with adequate capital and supervisory

ratings.

2. Secondary credit, which is intended for banks that are not eligible for primary credit because

they have inadequate capital or low supervisory ratings.

3. Seasonal credit, which consists of temporary, short-term loans to satisfy seasonal

requirements of smaller banks in geographic areas where agriculture or tourism are important.

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 188

During the financial crisis of 2007-2009, the Fed set up a variety of temporary lending facilities.

C. Interest on Reserve Balances

Paying interest on reserve balances gives the Fed another monetary policy tool. By increasing

the interest rate, the Fed can increase the level of reserves banks are willing to hold, thereby

restraining bank lending and increases in the money supply.

15.4 Monetary Targeting and Monetary Policy (pages 468-480)

Learning Objective: Explain the role of monetary targeting in monetary policy.

The central bank’s objective in conducting monetary policy is to use its policy tools to achieve

monetary policy goals. But the Fed often faces trade-offs in attempting to reach its goals,

particularly the goals of high economic growth and low inflation. Although it hopes to encourage

economic growth and price stability, it has no direct control over real output or the price level. The

Fed also faces timing difficulties in using its monetary policy tools.

A. Using Targets to Meet Goals

Targets are variables that the Fed can influence directly and that help achieve monetary policy

goals. Traditionally, the Fed has relied on two types of targets:

1. Intermediate targets, which are typically either monetary aggregates or interest rates.

B. The Choice between Targeting Reserves and Targeting the Federal Funds Rate

Traditionally, the Fed has used three criteria—whether a variable is measurable, controllable,

C. The Taylor Rule: A Summary of Fed Policy

Actual Fed deliberations are complex and incorporate many factors about the economy. John

D. Inflation Targeting

In 2012, the Fed joined many other central banks by setting an inflation target. With inflation

Arguments in favor of the Fed using an explicit inflation target focus on four points:

© 2014 Pearson Education, Inc.

189 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

1. Announcing explicit targets for inflation draws the public’s attention to what the Fed can

actually achieve in practice.

Opponents of inflation targets also make four points:

1. Rigid numerical targets for inflation diminish the flexibility of monetary policy to address

other policy goals.

E. International Comparisons of Monetary Policy

Although there are institutional differences in the ways in which central banks conduct monetary

policy, there are two important similarities in recent practices. First, most central banks in industrial

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 190

Solutions to the End-of-Chapter Questions and Problems

15.1 The Goals of Monetary Policy

Learning objective: Describe the goals of monetary policy.

Review Questions

1.1 Monetary policy aims to advance the economic well-being of the country’s citizens. Economic

well-being is typically determined by the quantity and quality of goods and services that

1.2 The Fed seeks to reduce cyclical unemployment. The Fed does not seek to reduce the

1.3 Interest rates represent the cost of borrowing by firms and households. Fluctuating interest rates

1.4 Excess fluctuations in the foreign exchange value of the dollar would make it difficult to know

Problems and Applications

1.5 Deflation, just like inflation, complicates the ability to distinguish overall price changes from

1.6 a. Extraordinary easing measures mean expansionary monetary policy of low interest rates and

b. The expansionary policy of low interest rates would stimulate spending, putting upward

pressure on prices. Deflation would be potentially highly damaging as it causes consumers to

c. Answers will vary. When deflation or high inflation is caused by a demand shock (too

little or too much aggregate spending), then the columnist is correct that the single mandate of

However, when the deflation or inflation is caused by a negative supply shock, such as an

© 2014 Pearson Education, Inc.

191 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

1.7 For its goal of high employment, the Fed seeks an unemployment rate equal to the natural rate of

1.8 The Fisher effect, which was discussed in Chapter 4, indicates that nominal interest rates

1.9 If the exchange rate between the Japanese yen and the U.S. dollar changes from ¥85 $1 to ¥95 $1,

15.2 Monetary Policy Tools and the Federal Funds Rate

Learning objective: Understand how the Fed uses monetary policy tools to influence the federal

funds rate.

Review Questions

2.2 The federal funds rate is the interest rate that banks charge each other on very short-term loans,

2.3 As the federal funds rate increases, the opportunity cost to banks of holding excess reserves

increases because the return they could earn from lending out those reserves goes up. The

2.4 The supply of reserves is determined by the Fed supplying nonborrowed reserves through open

market operations and borrowed reserves in the form of discount loans. The discount rate sets a

Problems and Applications

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 192

© 2014 Pearson Education, Inc.

193 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 194

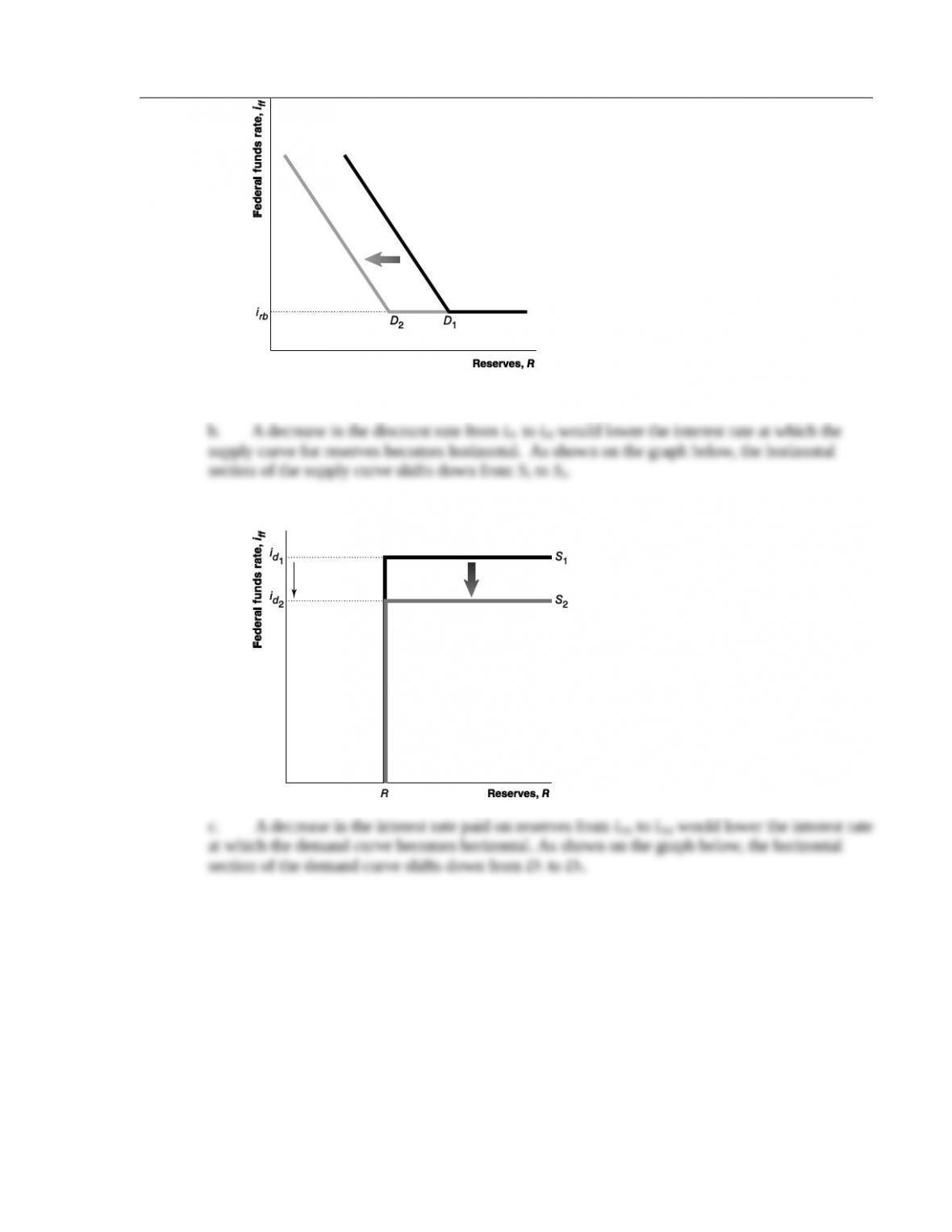

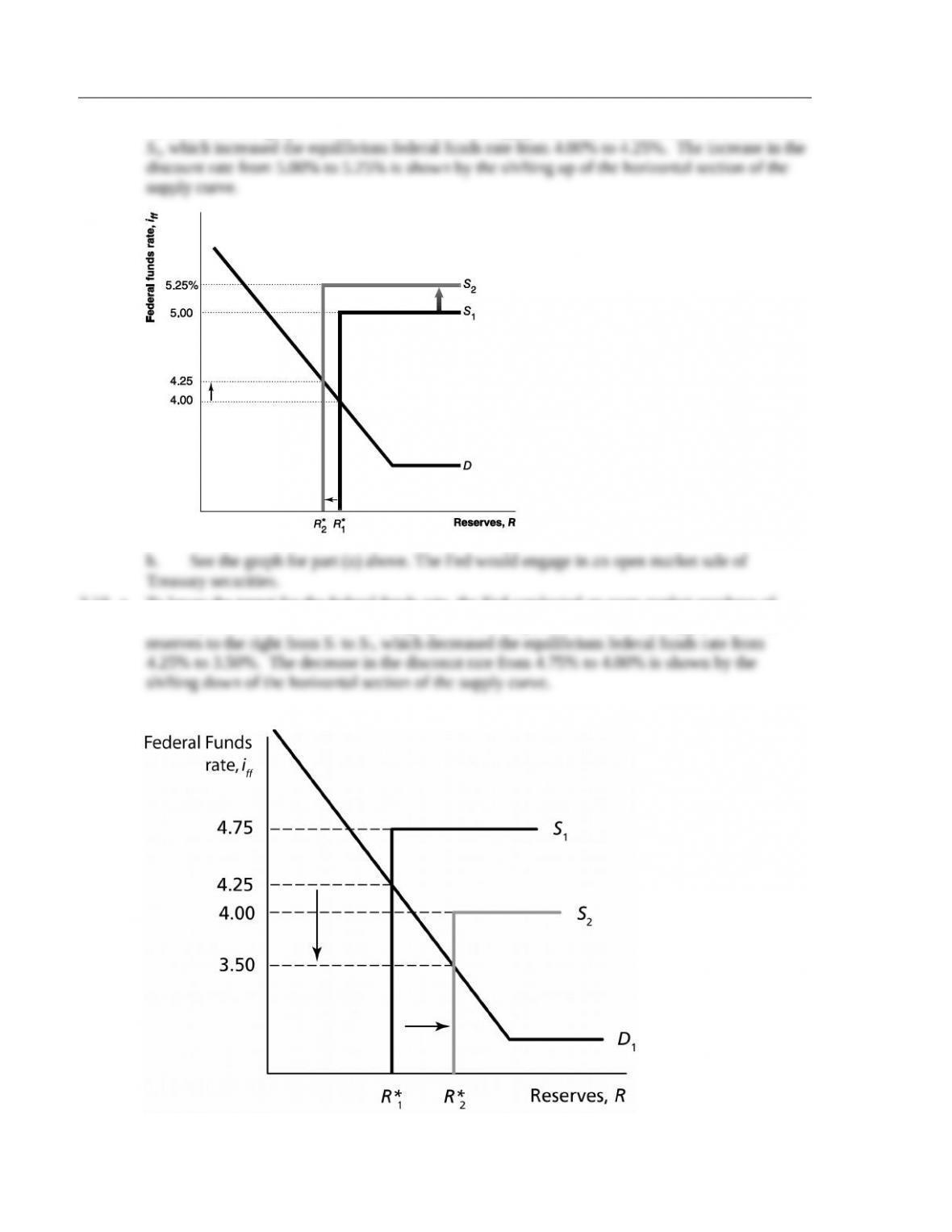

2.6 The graph on the left below shows that to lower its target for the federal funds rate from

iff 1

¿

to

iff 2

¿

, the Fed can conduct an open market purchase of securities. In the graph, the open

The graph on the right below shows that to raise its target for the federal funds rate from

iff 1

¿

iff 2

¿

2.7 a. To raise the federal funds rate, the Fed would sell securities, which shifts the supply curve for

© 2014 Pearson Education, Inc.

195 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

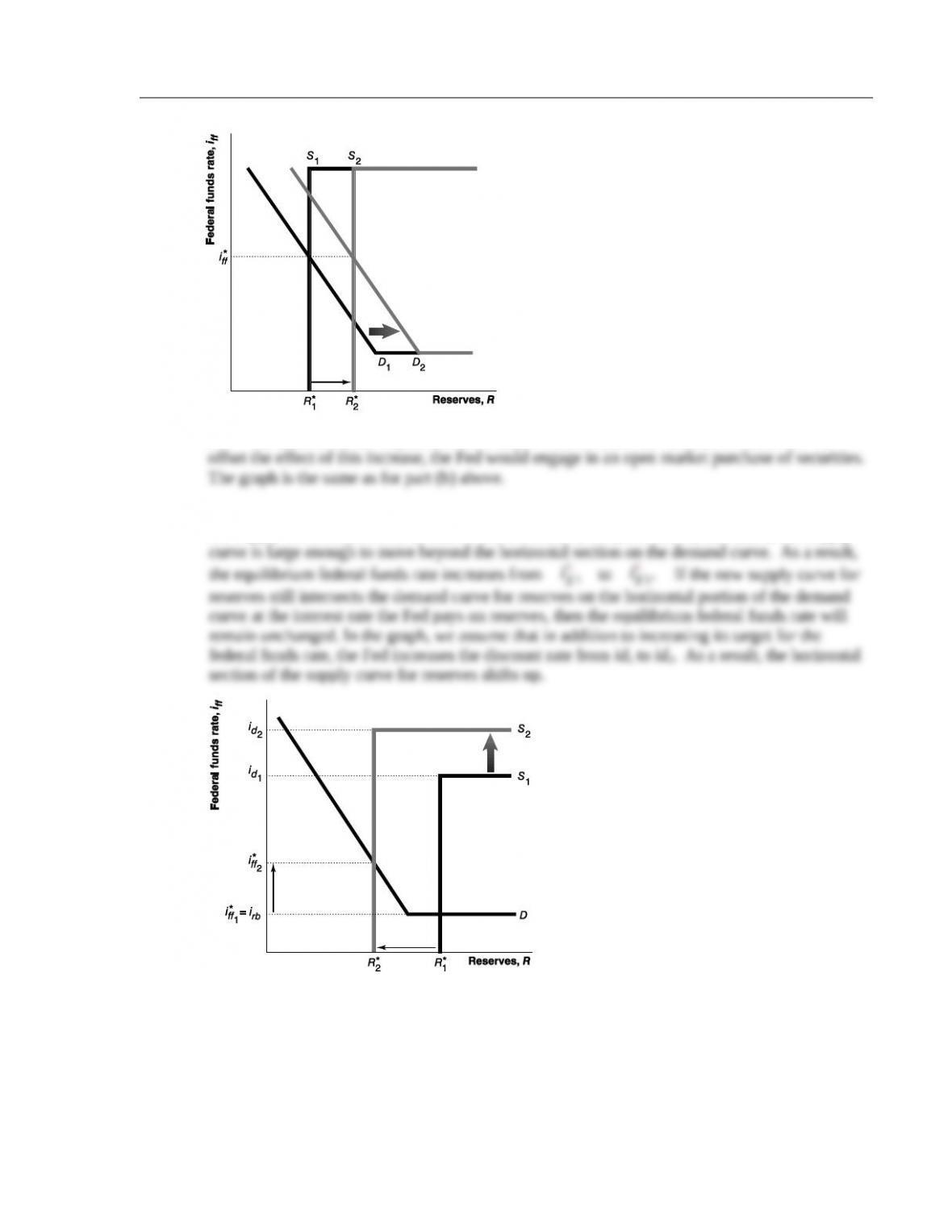

b. Banks’ increased demand for reserves shifts the demand curve to the right from D1 to D2. To offset the effect

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 196

c. An increase in the required reserve ratio would increase the demand for reserves. To

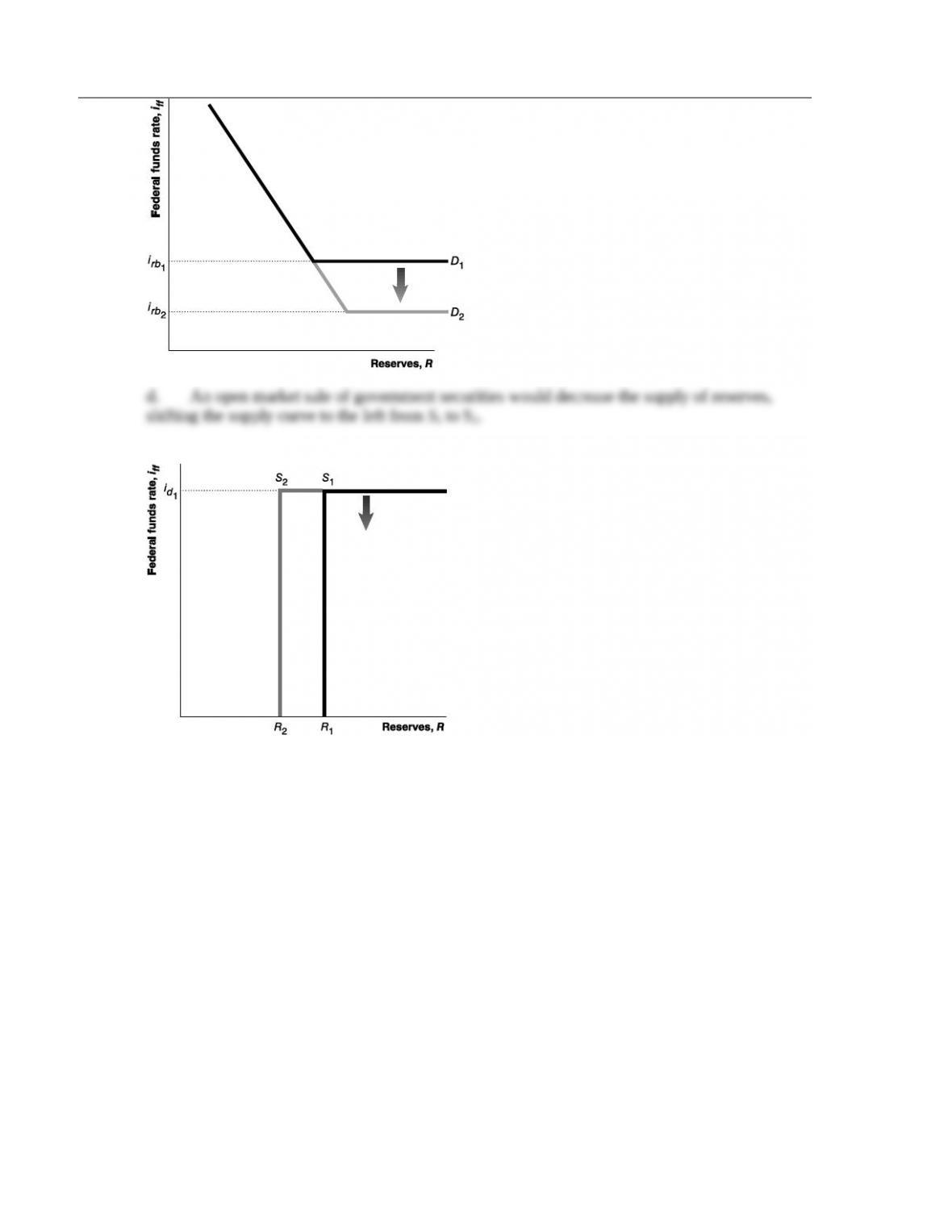

2.8 An open market sale of Treasury securities by the Fed decreases the supply of reserves, causing

the supply curve for reserves to shift to the left from S1 to S2. As shown, the shift in the supply

© 2014 Pearson Education, Inc.

197 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

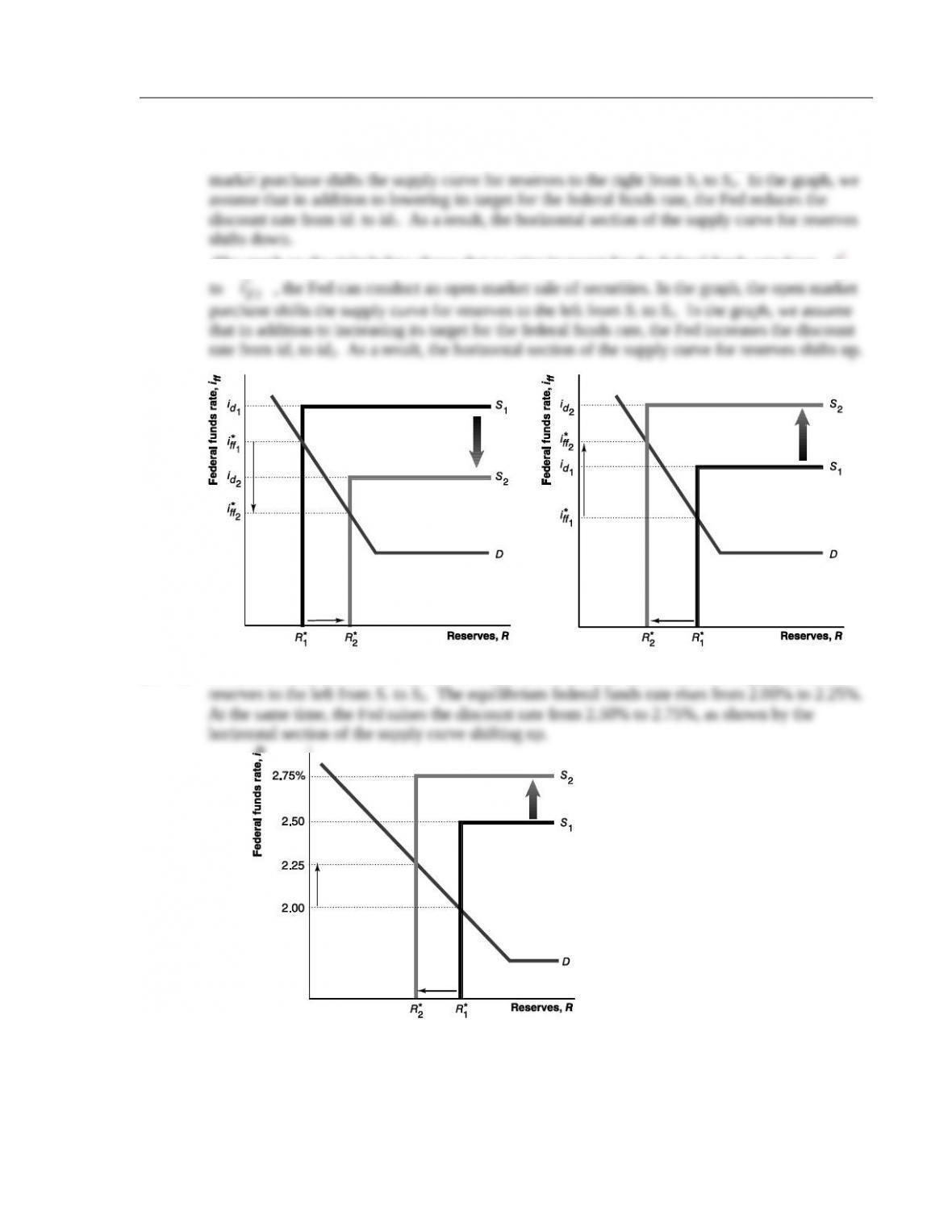

2.9 a. To raise the target for the federal funds rate, the Fed conducted an open market sale of securities.

As shown on the graph below, the sale shifted the supply curve for reserves to the left from S1 to

2.10 a. To lower the target for the federal funds rate, the Fed conducted an open market purchase of

Treasury securities. As shown on the graph below, the purchase shifted the supply curve for

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 198

© 2014 Pearson Education, Inc.

199 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

15.3 More on the Fed’s Monetary Policy Tools

Learning objective: Trace how the importance of different monetary policy tools has changed over

time.

Review Questions

3.1 An open market sale of Treasury securities decreases the price of Treasury securities, thereby

3.2 Open market operations have the advantages over other policy tools of control, flexibility, and

ease of implementation. The Fed initiates open market operations and completely controls the

3.3 To stimulate the economy, the Fed had already pushed the federal funds rate to near zero by

December 2008. But the economy continued to struggle and the Fed wanted to put further

3.4 Before 1980, only member banks of the Federal Reserve System could receive discount loans.

After 1980, all depository institutions could receive discount loans. During the financial crisis of

Problems and Applications

3.5 To hit the target federal funds rate, the account manager adjusts the supply of reserves by using

3.6 a. The Fed’s policy rate is the federal funds rate. “Policy rate” is a general term used to refer to the

c. The author means that additional monetary easing will not stimulate the economy.

Additional monetary easing will have no more effect than pushing on a string. Economists

d. Answers can vary. Additional quantitative easing will have limited effects in lowering

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 200

3.7 a. Bernanke uses the term monetary accommodation to mean the near zero federal funds rate,

c. Fed Chairman Bernanke’s letter to Congress mentions three channels the Fed used to ease

financial conditions:

1. Reducing the cost of capital to businesses by reducing interest rates, reducing credit

2. Boosting the aggregate wealth of U.S. households by supporting the housing market

3. Improving the competitiveness of U.S. businesses by allowing businesses to access

3.8 By increasing the interest rate it pays on bank reserves, the Fed can increase the level of reserves

Additionally, the Fed could use the other new policy tool of the term deposit facility to restrain

3.9 You should disagree. The Fed does not set the federal funds rate. The federal funds rate is

3.10 a. The implications of some financial institutions being able to borrow and lend in the federal funds

b. If only banks could borrow and lend in the federal funds market, then the actual federal

funds rate could not drop below the interest rate the Fed pays on reserve deposits because banks

3.11 The Primary Dealer Credit Facility was designed to help primary dealers—the financial firms

The Term Securities Lending Facility was designed to help financial firms by providing loans of

Treasury securities in exchange for mortgage-backed securities.

The Commercial Paper Funding Facility was designed to help nonfinancial corporations that

The Term Asset-Backed Securities Loan Facility was designed to help firms that raised funds

15.4 Monetary Targeting and Monetary Policy

Learning objective: 15.4: Explain the role of monetary targeting in monetary policy.

© 2014 Pearson Education, Inc.

201 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

Review Questions

4.1 The Fed often faces the key tradeoff between price stability and maximum employment. For

4.2 The two timing difficulties the Fed faces in using its monetary policy tools are the information

4.3 The following is a list of targets, or variables, that the Fed can influence directly. The targets are

listed from the most influence to the least influence:

Policy tools (Fed has most influence),

4.4 The Taylor rule is a monetary policy guideline economist John Taylor developed to help analyze

how the Fed chooses the target for the federal funds rate. The Taylor rule serves as a summary

4.5 The Bank of Canada uses inflation targeting and a focus on the exchange value of the Canadian

dollar. The Bank of England uses inflation targeting. The Bank of Japan has not adopted a

Problems and Applications

4.6

a. M2 is an intermediate target.

b. The monetary base is an intermediate target.

4.7 If the Fed uses the federal funds rate as a policy instrument, then increases in the demand for

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 202

4.8 The following legislative changes and financial innovations occurred after 1979:

1. Congress authorized NOW (negotiable order of withdrawal) accounts on which banks can pay

interest

2. Banks introduced two innovations:

(a) Automated transfer of saving accounts, which move checkable deposit balances into

(b) Sweep accounts, which move checkable deposits of businesses into money market

4.9 a. Increases in the Fed’s balance sheet increase the monetary base and typically increase the money

supply, subsequently causing increased inflation. Inflationary expectations were not unsettled

b. Bernanke’s “open-ended round of quantitative easing” refers to a third round of

quantitative easing (QE3), where the Fed pledged to continue purchases of mortgage-backed

© 2014 Pearson Education, Inc.

203 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

4.10 You should agree. The Fed cannot target—which would appear to be what the authors mean by

“manage”—both the level of reserves and the federal funds rate. If the Fed targets the federal

4.11 Using the equation found on page 474 of the text, the Taylor rule federal funds rate target 2%

4.12 a. The Federal Open Market Committee (FOMC) kept the federal funds rate at levels well below

b. Low interest rates encouraged subprime borrowers (borrowers with flawed credit

histories) and Alt-A borrowers (borrowers who did not document their incomes) to acquire

Data Exercises

D15.1 The answers below apply to the Federal Open Market Committee (FOMC) press release of

January 30, 2013.

a. The FOMC did not change the target for the federal funds rate. It kept the target range for

the federal funds rate at 0 to 0.25%.

d. The Fed announced that it would continue purchasing agency mortgage-backed securities at

a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion

D15.2

© 2014 Pearson Education, Inc.

Chapter 15 Monetary Policy 204

D15.3 The Bank of England’s total assets increased from almost $100 million at the end of 2007 to

nearly $300 million on October 22, 2008 after the Lehmann Brothers bankruptcy on September

D15.4

© 2014 Pearson Education, Inc.

205 Hubbard & O’Brien • Money, Banking, and the Financial System, Second Edition

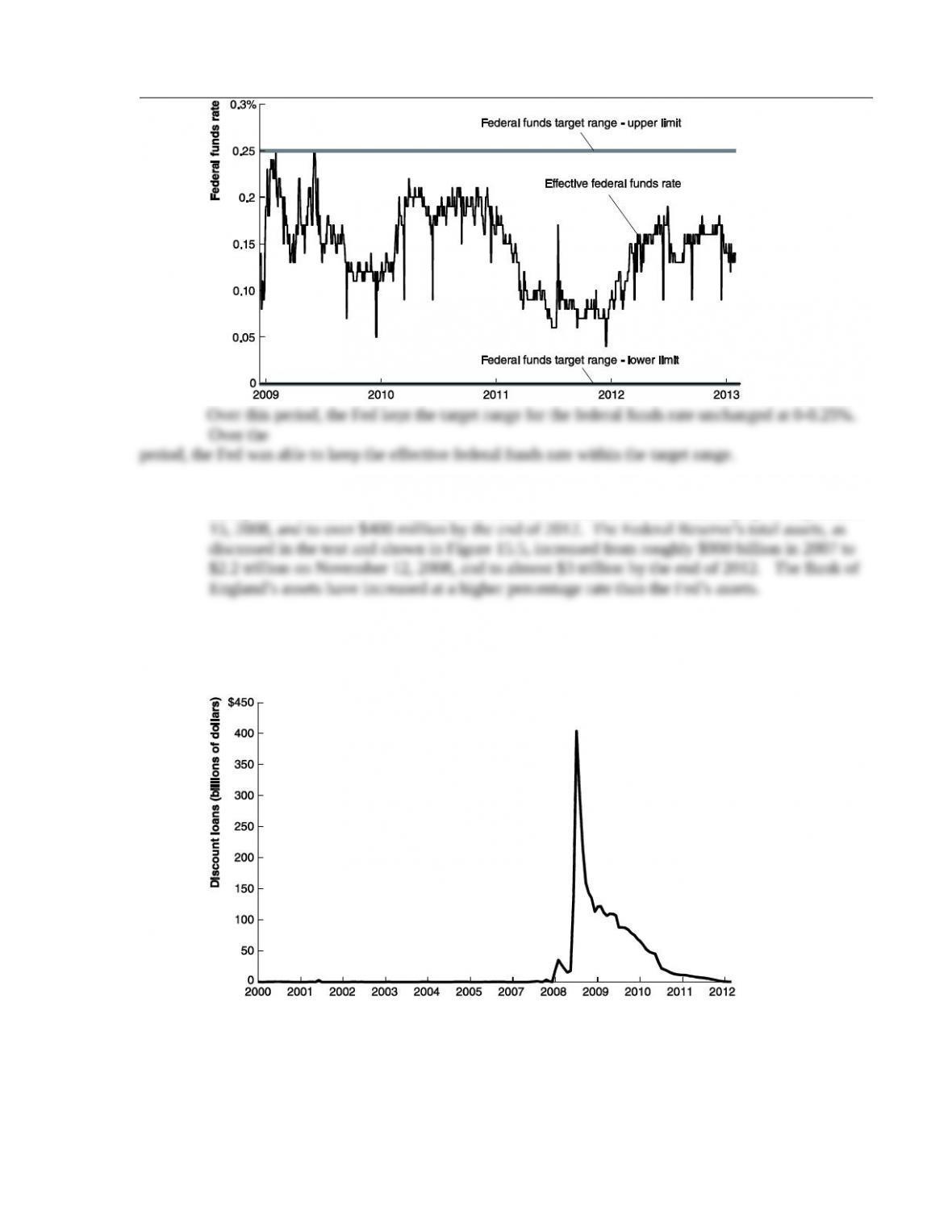

Before the financial-crisis, discount loans were generally below $1 billion. Based only on the

data for the

© 2014 Pearson Education, Inc.