Solutions to the End-of-Chapter Questions, Problems, and Data

Exercises

10.1 The Basics of Commercial Banking: The Bank Balance Sheet

Learning objective: Understand bank balance sheets.

Review Questions

1.1 Assets = Liabilities + Shareholders’ equity. The most important bank assets are reserves and

1.2 A bank’s liabilities, principally deposits and borrowings, are the sources of the funds the bank

1.3 Real estate loans have become a much higher percentage of total loans since 1973, while

Problems and Applications

1.4 On the one hand, banks might be better able to monitor the behavior of the companies they had

made loans to, so moral hazard should decrease. On the other hand, the existence of deposit

1.5 Banks offering interest on checking accounts has not increased the popularity of checking

accounts for several reasons: 1) Banks have created several savings instruments, including

1.6 a. Fannie Mae and Freddie Mac were battling with banks that originated the housing loans

(mortgages) about “put-backs,” which required banks to repurchase defaulted mortgages that

b. Repurchasing bad loans would hurt the financial position of banks and also make banks more

1.7 a.

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 117

Assets Liabilities

1.8 a. No, a loan from the Treasury would not be counted as bank capital. The loan would be counted

10.2 The Basic Operations of a Commercial Bank

Learning objective: Describe the basic operations of a commercial bank.

Review Questions

2.1 A T-account is an accounting tool used to show changes in balance sheet items. We can show the

Bank of America

Assets Liabilities

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 118

2.2 Return on assets (ROA) is the ratio of a bank’s after-tax profit to the value of its assets.

2.3 Bank leverage is the ratio of the value of a bank’s assets to the value of its capital. A bank’s

As a result, a bank’s managers have an incentive to increase the bank’s leverage in order to

Problems and Applications

2.4 Bank of America’s holdings of securities fall by $10 million and its reserves increase by $10

Bank of America

Assets Liabilities

PNC Bank

Assets Liabilities

SunTrust Bank

Assets Liabilities

National City Bank

Assets Liabilities

2.6 National Bank of Guerneville has $3.4 million in required reserves (10% of $34 million), so

initially the bank has $0.6 million in excess reserves. Commonwealth Bank has $4.7 million in

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 119

2.7 a. The new banking regulations put a cap on the amount that banks could charge merchants for

b. Higher-income customers are more likely than low-income customers to use other services of the

2.10 a. Banks increased bank capital and reduced debt to decrease their exposure to risk. The financial

b. Banks take on debt to obtain assets. So, an increase in bank capital and a reduction in bank debt

2.11 This bank has a ratio of assets to capital of ($5,000 million/$300 million) = 16.7. The higher the

ratio of assets to capital, the more leveraged the bank is, and the higher the bank’s ROE for a

10.3 Managing Bank Risk

Learning objective: Explain how banks manage risk.

Review Questions

3.1 Liquidity risk is the possibility that depositors may collectively decide to withdraw more funds

than the bank has immediately on hand. Banks manage this risk by borrowing in the federal funds market

or by using reverse repurchase agreements. Banks can also increase their borrowings from the Federal

3.2 Gap analysis looks at the difference between the dollar value of a bank’s variable-rate assets and

the dollar value of its variable-rate liabilities to gauge how sensitive a bank’s profits are to movements in

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 120

Problems and Applications

3.3 The liquidity risk would have been larger because the absence of deposit insurance created the

3.4 It would appear that the existence of reserve requirements makes it easier for banks to deal with

3.5 a. Agree. When interest rates increase, the bank will be earning more on its rate-sensitive

b. Agree. A fall in interest rates with a positive duration gap will increase a bank’s capital by

c. Disagree. A longer duration of the bank’s liabilities will increase their value when interest rates

3.6 The problem with this bill is that it increases adverse selection in the market for loans. With the high

10.4 Trends in the U.S. Commercial Banking Industry

Learning objective: Explain the trends in the U.S. commercial banking industry.

Review Questions

4.1 A state bank has a charter from a state government. A national bank has a charter from the federal

4.2 The FDIC stands for the Federal Deposit Insurance Corporation. Congress established the FDIC in

4.3 Historically in America, there was a fear of banks having too much power and a belief that banks

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 121

4.4 Off-balance-sheet activities are activities that generate fee income but do not affect a bank’s

balance sheet because they do not increase either the bank’s assets or its liabilities. There are four types of

4.6 Congress originally authorized TARP, or the Troubled Asset Relief Program, in October 2008 in

response to the financial crisis. TARP was originally intended to help restore an active market in

Problems and Applications

4.7 This statement is misleading because state government restrictions on the number of branches a

bank could have and federal government restrictions on nationwide banking resulted in the United States

4.8

a. Amazon has more of a vested interest in the small businesses surviving and growing because the

b. The advantage to a small business is the access to funds (a loan), and the disadvantage is typically

4.9

a. “The current environment” refers to the new government regulations that limit the fees banks can

b. The increased use of debit cards has reduced the demand for currency, thereby reducing the

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 122

c. The number of ATMs is likely to decrease, particularly at non-bank locations given the increased

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 123

4.10 The federal government wanted bank capital to increase in order to keep banks with falling asset

4.11 Stabilizing the banking industry allowed banks to provide more consumer loans to households,

Data Exercise

D10.1

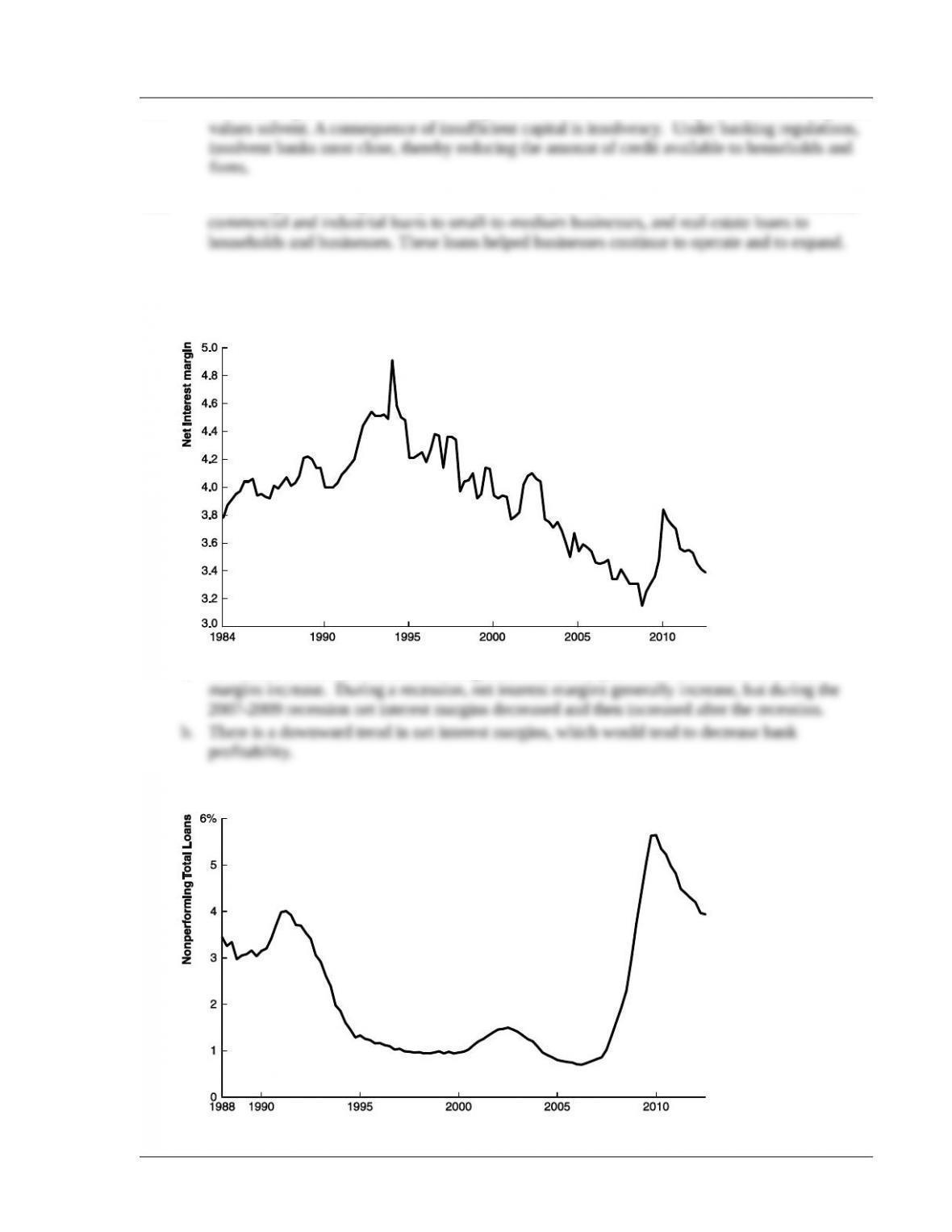

a. Just before a recession net interest margins decrease, and just after a recession net interest

D10.2

© 2014 Pearson Education, Inc.

Chapter 10 The Economics of Banking 124

b. There was a slight downward trend in nonperforming loans up through the beginning of the

D10.3

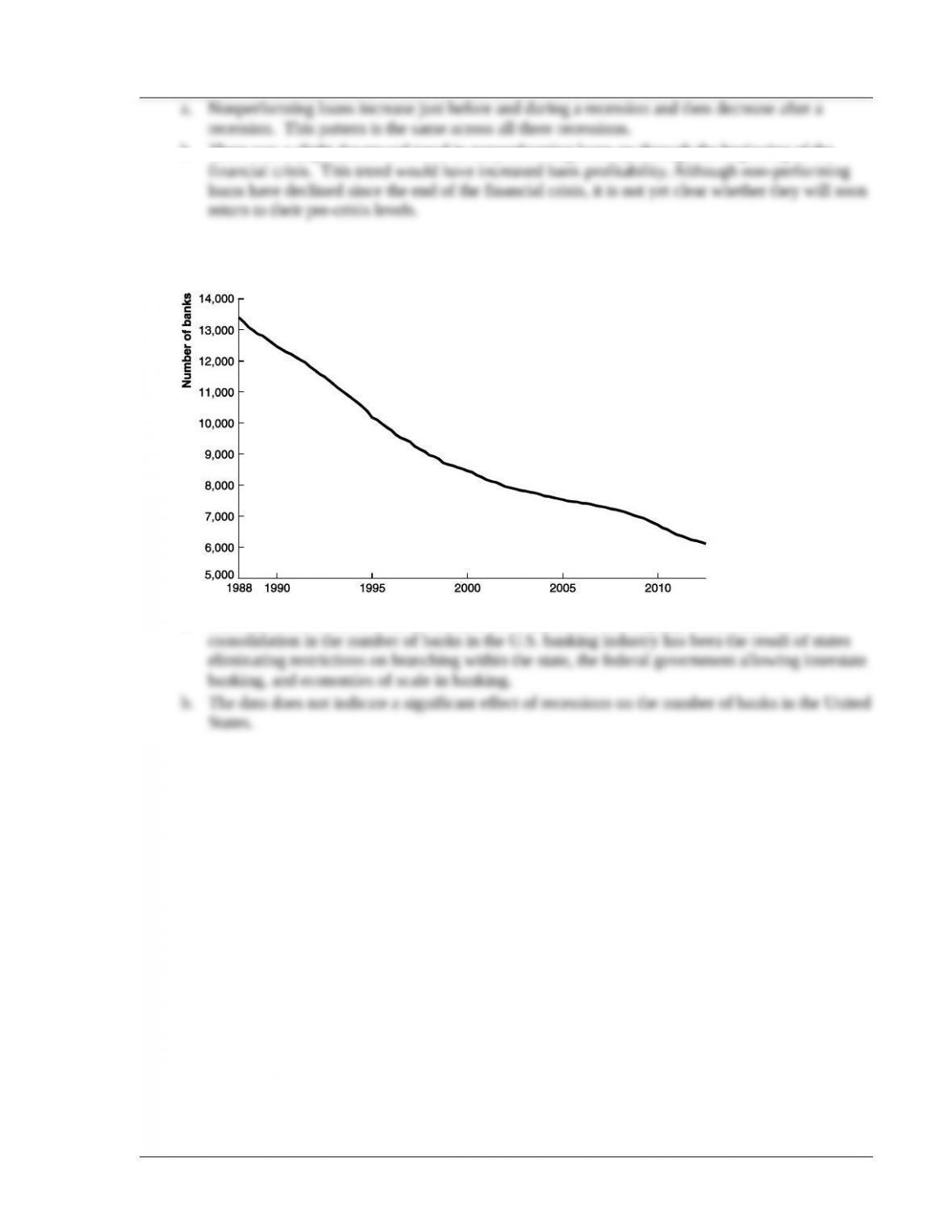

a. The trend from 1988 to 2012 in the number of banks has been rapidly downward. The

© 2014 Pearson Education, Inc.