Solutions to the End-of-Chapter Questions, Problems, and Data

Exercises

1.1 Key Components of the Financial System

Learning Objective: Identify the key components of the financial system.

Review Questions

1.1 a. Money: Anything that people are willing to accept in payment for goods and services or to pay

off debts.

b. Stocks: Financial securities that represent partial ownership of a firm.

1.2 With direct finance, one party lends directly to the other party. Buying the stock of a firm’s IPO

is direct financing. Direct financing requires financial markets. Indirect finance involves three

1.4 The Federal Reserve is the central bank of the United States. The president appoints the

1.5 The financial system provides these services to savers:

i. Risk sharing, which allows savers to spread and transfer risk.

Problems and Applications

1.6 Disagree. Insurance companies specialize in contracts to protect their policyholders from the

1.7 The president singled out banks because of their important role as financial intermediaries in the

1.8 a. “Bad lending” refers to lending to borrowers with flawed credit histories or who might

otherwise have difficulty repaying loans.

1.10 Putting your money in a bank increases your liquidity, decreases your risk, and decreases your

1.11 Direct finance would make the process of an individual buying a car or a house much more

difficult. The car or house buyer would either have to accumulate the savings to pay for the car

1.12 Lenders win because the repayment rate on mortgages would increase. Borrowers win because they

would be more likely to afford their payments. Securitization slices the mortgages into numerous

Moreover, the cost of negotiation with every investor holding the security may be prohibitively

1.2 The Financial Crisis of 2007–2009

Learning objective: Provide an overview of the financial crisis of 2007–2009.

Review Questions

2.1 A bubble is an unsustainable increase in the price of a class of assets. Many economists believe

2.2 Mortgages were routinely packaged together as mortgaged-back securities and sold to investors

2.3 The decline in housing prices led to rising defaults among subprime and Alt-A borrowers,

2.4 The Federal Reserve aggressively lowered interest rates and made loans to commercial banks

Moral hazard is the possibility that managers of a financial firm will take on riskier investments

Problems and Applications

2.5 There can be no bubble in automobiles and refrigerators because they typically do not gain

2.6 The primary issue involved in measuring housing prices is that houses are not homogeneous

goods. Because no two houses are exactly the same, the price of an “average” house can be

2.7 The secondary mortgage market allows banks to transfer the risk of holding a loan to investors

who buy mortgage-backed securities. Access to the funds from these investors allows banks to

Data Exercise

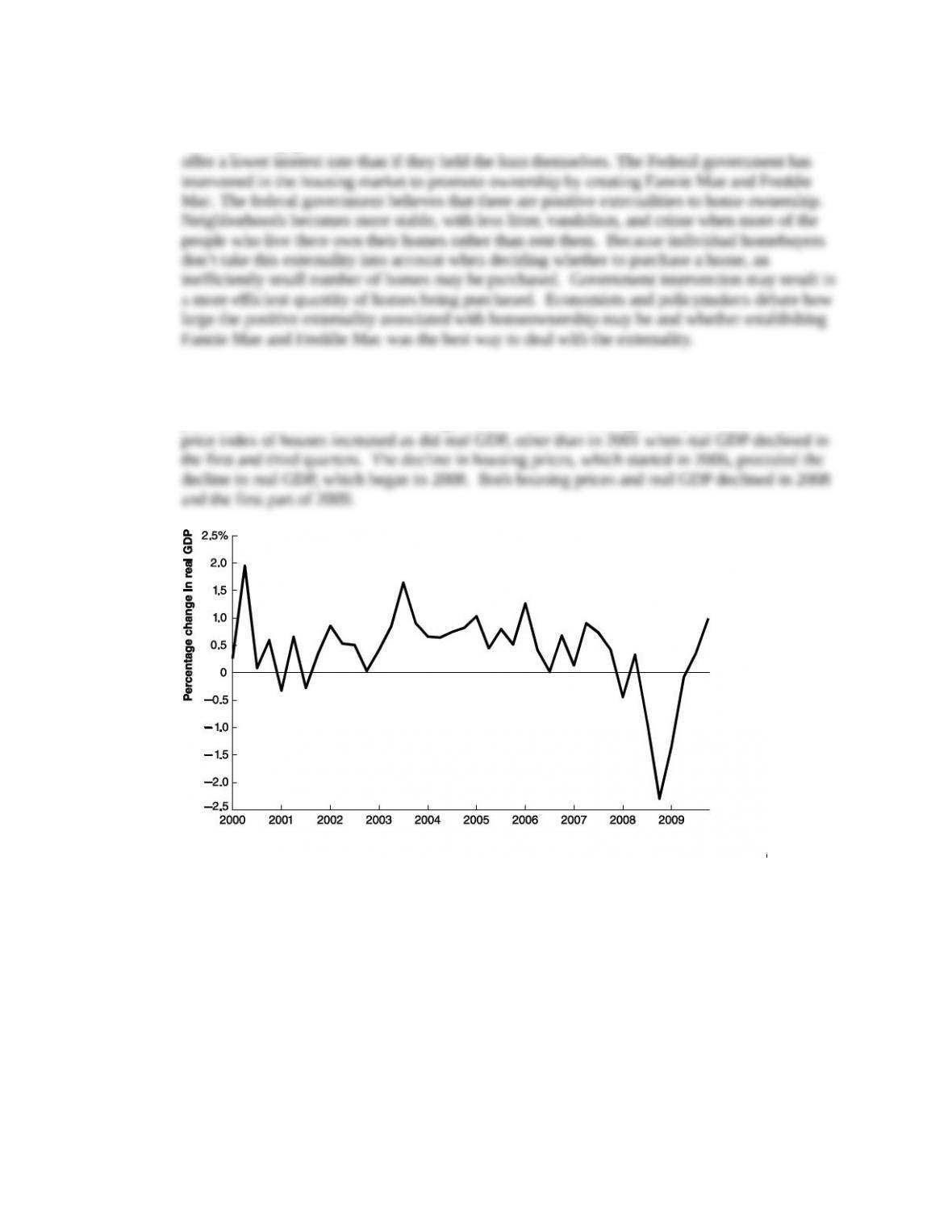

D1.1 Movements in real GDP correspond well, but not perfectly, to movements in the Case-Shiller

price index of houses from 2000 through 2009. From 2000 through 2006, the Case-Shiller