Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Additional Issues for Classroom Discussion

1. Where Would We Be Without Equilibrium Forces?

Economists generally take for granted that markets work so that powerful economic forces return the

2. What Assumptions Are Unrealistic?

In developing our model of the economy, we make a number of assumptions about what variables are

affected by which other variables. Some of those assumptions are pretty obvious, but the reasons for others

are more subtle. Your students may be curious to know how much it matters which variables are affected

by which other ones. Does the precise structure of the model matter a lot for the qualitative exercises that

1. The position of the FE line is determined by the labor market and the production function. Labor

supply and demand determine equilibrium employment. Using equilibrium employment in the

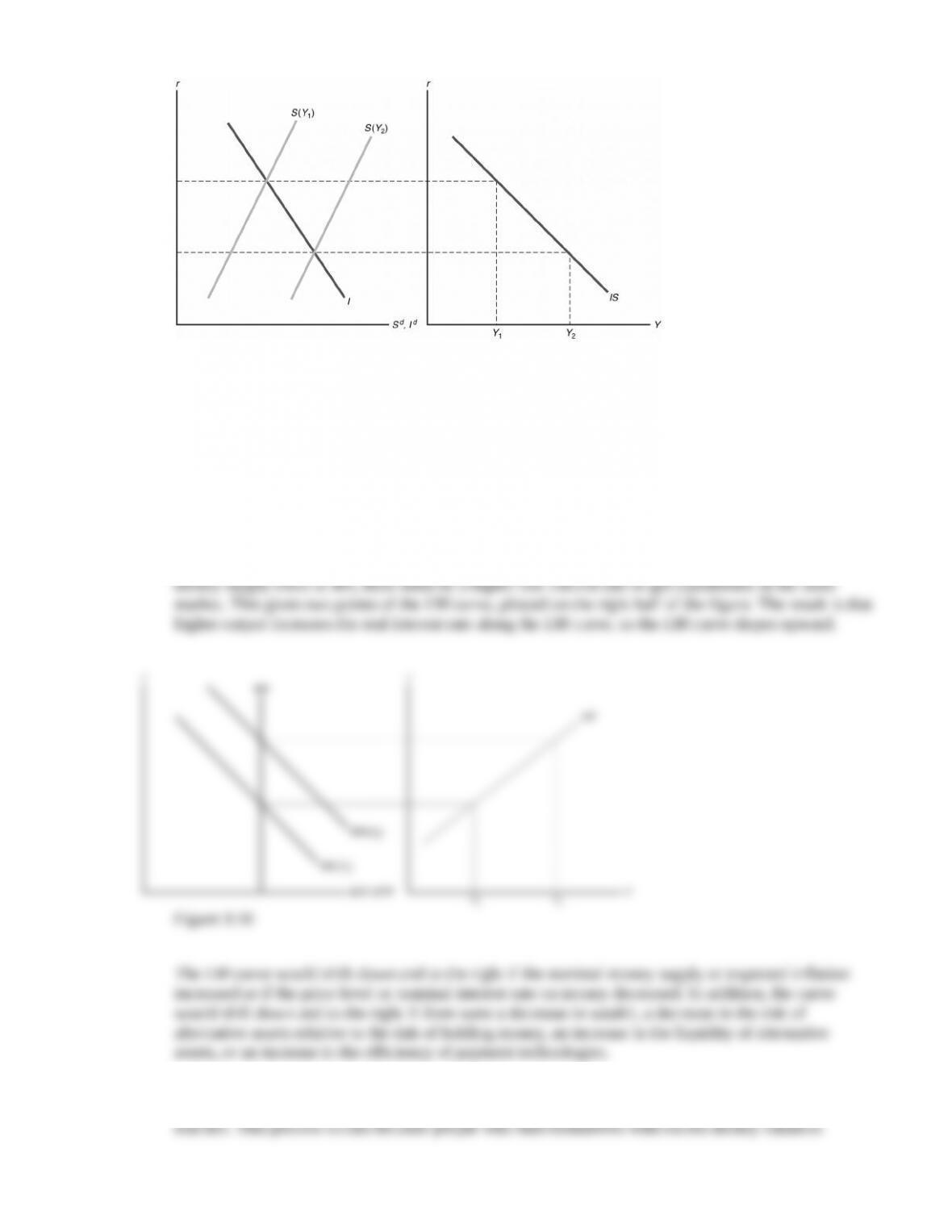

2. The IS curve shows combinations of the real interest rate (r) and output (Y) that leave the goods

market in equilibrium. Equilibrium in the goods market occurs when the aggregate supply of goods

(Y) equals the aggregate demand for goods (Cd Id G). Since desired national saving (Sd) is

Y Cd G, an equivalent condition is Sd Id. Equilibrium is achieved by the adjustment of the real

interest rate to make the desired level of saving equal to the desired level of investment. For different

levels of output, there are different desired saving curves, with different equilibrium interest rates.

When plotted on a figure showing output and the real interest rate, this forms the IS curve, as shown

in Figure 9.15. The curve slopes downward because as output rises, the saving curve shifts along the

investment curve and the real interest rate declines.

3. The LM curve shows the combinations of output and the real interest rate that maintain equilibrium in

the asset market. Equilibrium in the asset market occurs when real money demand equals the real

money supply.

Figure 9.16 shows the derivation of the LM curve and why it slopes upward. An increase in output

from Y1 to Y2 raises money demand, shifting the money demand curve from MD(Y1) to MD(Y2). With

4. For constant output, if real money supply exceeds the real quantity of money demanded, the real

interest rate will decline to increase the real quantity of money demanded until equilibrium is

5. General equilibrium is a situation in which all markets in an economy are simultaneously in

equilibrium. This is shown in Figure 9.17 as the point at which the FE line and the IS and LM curves

6. There is monetary neutrality if a change in the nominal money supply changes the price level but has

no effect on real variables. Once prices adjust, money is neutral in the IS–LM model, because a

change in the money supply that shifts the LM curve is matched by a proportional change in the price

level that returns the real money supply back to its original level and moves the LM curve back to its

7. The aggregate demand curve relates the price level to the aggregate demand for goods and services. It

is downward sloping, because with a fixed nominal money supply, an increase in the price level shifts

the LM curve up, so the level of output at the IS-LM intersection is lower.

Factors that shift the aggregate demand curve up and to the right include (1) an increase in expected

future output, which reduces desired saving, raises desired consumption, and shifts the IS curve up

8. The short-run aggregate supply curve is horizontal and the long-run aggregate supply curve is

vertical. The short-run aggregate supply curve is horizontal because prices remain fixed in the short

9. In the short run, money is not neutral, but in the long run it is neutral. Suppose the economy is

initially in general equilibrium, as shown in Figure 9.18, where LRAS, SRAS1, and AD1 intersect.

Now suppose the money supply declines by 10%, so the aggregate demand curve shifts down and to

the left to AD2. In the short run, the equilibrium occurs at the intersection of AD2 and SRAS1, so output

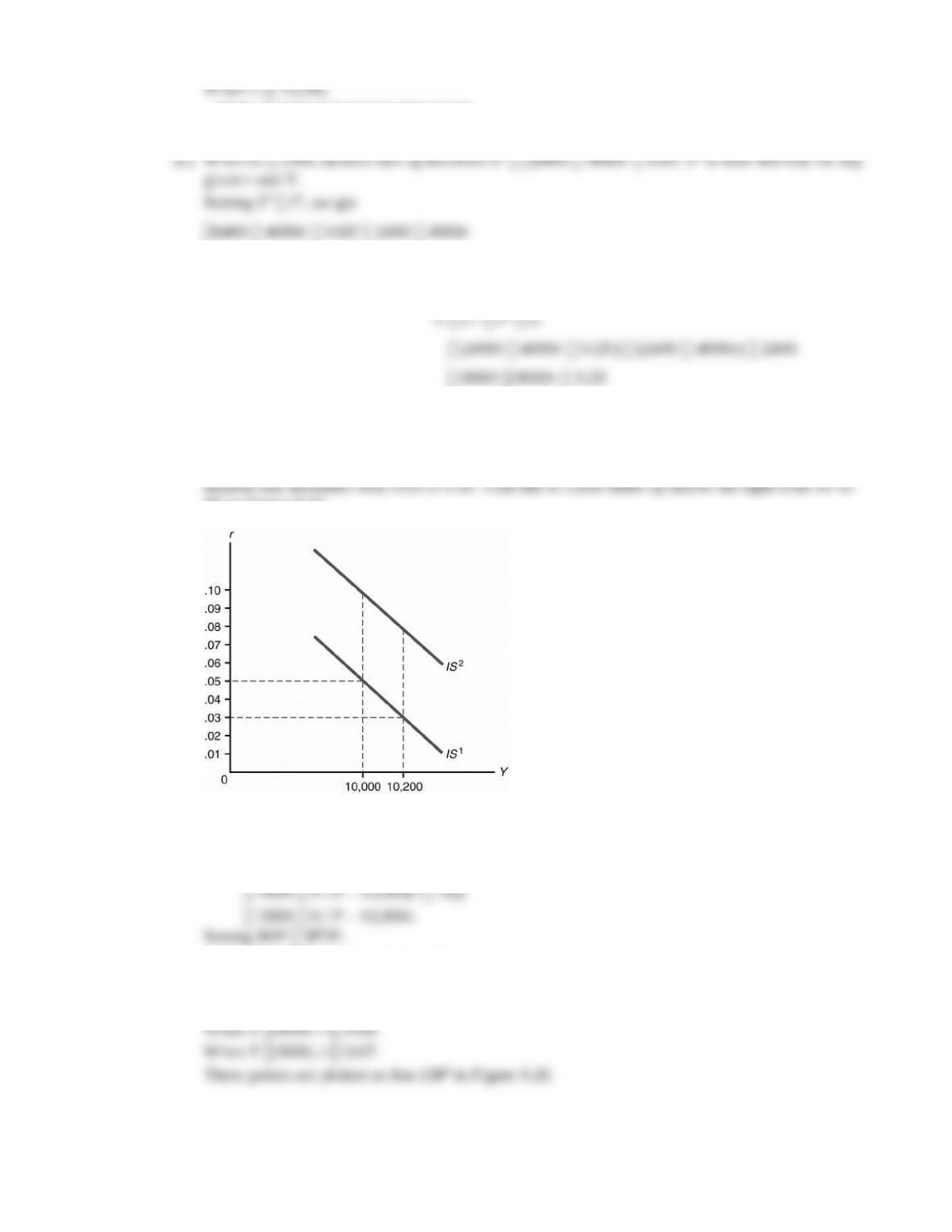

1. (a) Sd Y Cd G

Y (4000 4000r 0.2Y) 2000

So 0.8Y 8400 8000r, or

8000r 8400 0.8Y.

(2) Using the equivalent equation that desired saving equals desired investment gives

0.8Y 8400 8000r, or

8000r 8400 0.8Y.

So we can use either equilibrium condition to get the same result.

8000r 8400 (0.8 10,000) 400,

so r 0.05.

8000r 8400 (0.8 10,200) 240,

so r 0.03.

8000r 8800 0.8Y.

Similarly, using the equation that goods supplied equals goods demanded gives:

So 0.8Y 8800 8000r, or

8000r 8800 0.8Y.

At Y 10,000, this is 8000r 8800 (0.8 10,000) 800, so r 0.10. The market-clearing real

IS2 in Figure 9.19.

Figure 9.19

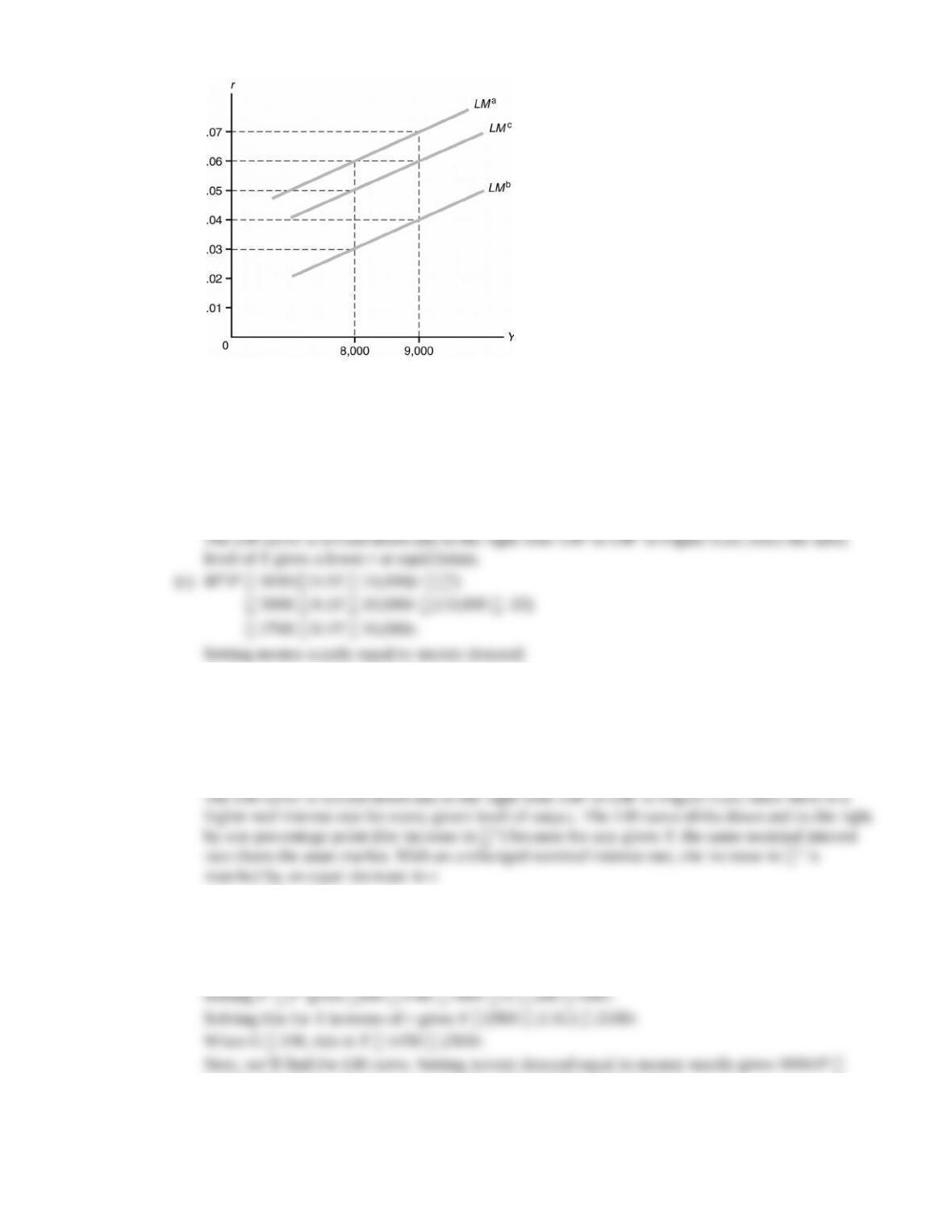

2. (a) Md/P 3000 0.1Y 10,000i

3000 0.1Y – 10,000(r e)

6000/2 2800 0.1Y 10,000r

10,000r 200 0.1Y

r 0.02 (Y/100,000).

3300 2800 0.1Y – 10,000r

10,000r –500 0.1Y

r –0.05 (Y/100,000).

When Y 8000, r 0.03.

When Y 9000, r 0.04.

3000 2700 0.1Y 10,000r

10,000r 300 0.1Y

r 0.03 (Y/100,000).

When Y 8000, r 0.05.

When Y 9000, r 0.06.

3. (a) First, we’ll find the IS curve.

Sd Y – Cd – G Y [200 0.8(Y T) 500r] G Y [200 (0.6Y 16) 500r]

G

184 0.4Y 500r G

0.5Y 250r 25, which can be solved for Y 19,780/P 50 500 r.

With full-employment output of 1000, using this in the IS curve and solving for r gives r 0.18.

4. (a) First, look at labor market equilibrium.

Labor supply is NS 55 10(1 t)w. Labor demand (ND) comes from the equation w 5A

(0.005A ND). Substituting the latter equation into the former, and equating labor supply and

labor demand gives N 100. Using this in either the labor supply or labor demand equation then

gives w 9. Using N in the production function gives Y 950.

20.

(d) With G 72.5, the IS curve becomes r 1.367 – 0.004/3 Y. With Y 950, the IS curve gives

5. The IS curve is found by setting desired saving equal to desired investment. Desired saving is Sd

Y Cd G Y [1275 0.5(Y T) 200r] G. Setting Sd Id gives Y [1275 0.5(Y T)

200r] G 900 200r, or Y 4350 800r 2G T. The LM curve is M/P L 0.5Y 200i

0.5Y 200(r ) 0.5Y 200r.

(a) T G 450, M 9000. The IS curve gives Y 4350 800r 2G T 4350 800r (2

450) 450 4800 800r. The LM curve gives 9000/P 0.5Y 200r. To find the aggregate

demand curve, eliminate r in the two equations by multiplying the LM curve through by 4 and

800r 2Y 36,000/P. IS: Y 4800 800r. Rearranging gives 800r 4800 Y. Setting the

right-hand sides of these two equations to each other (since both equal 800r) gives: 2Y

(36,000/P) 4800 Y, or 3Y 4800 (36,000/P), or Y 1600 (12,000/P); this is the AD

curve.

With Y 4600 at full employment, the AD curve gives 4600 1600 (12,000/P), or P 4. From

330 4680 800r.

LM: 36,000/P 2Y 800r, or 800r 2Y 36,000/P.

IS: Y 4680 800r, or 800r 4680 Y.

AD: 2Y (36,000/P) 4680 Y, or (36,000/P) 4680 3Y, or Y 1560 (12,000/P).

6. (a) A 2, f1 5, f2 0.005, n0 55, nw 10, c0 300, cY 0.8, cr 200, t0 20, t 0.5, i0 258.5,

ir 250, l0 0, lY 0.5, lr 250.

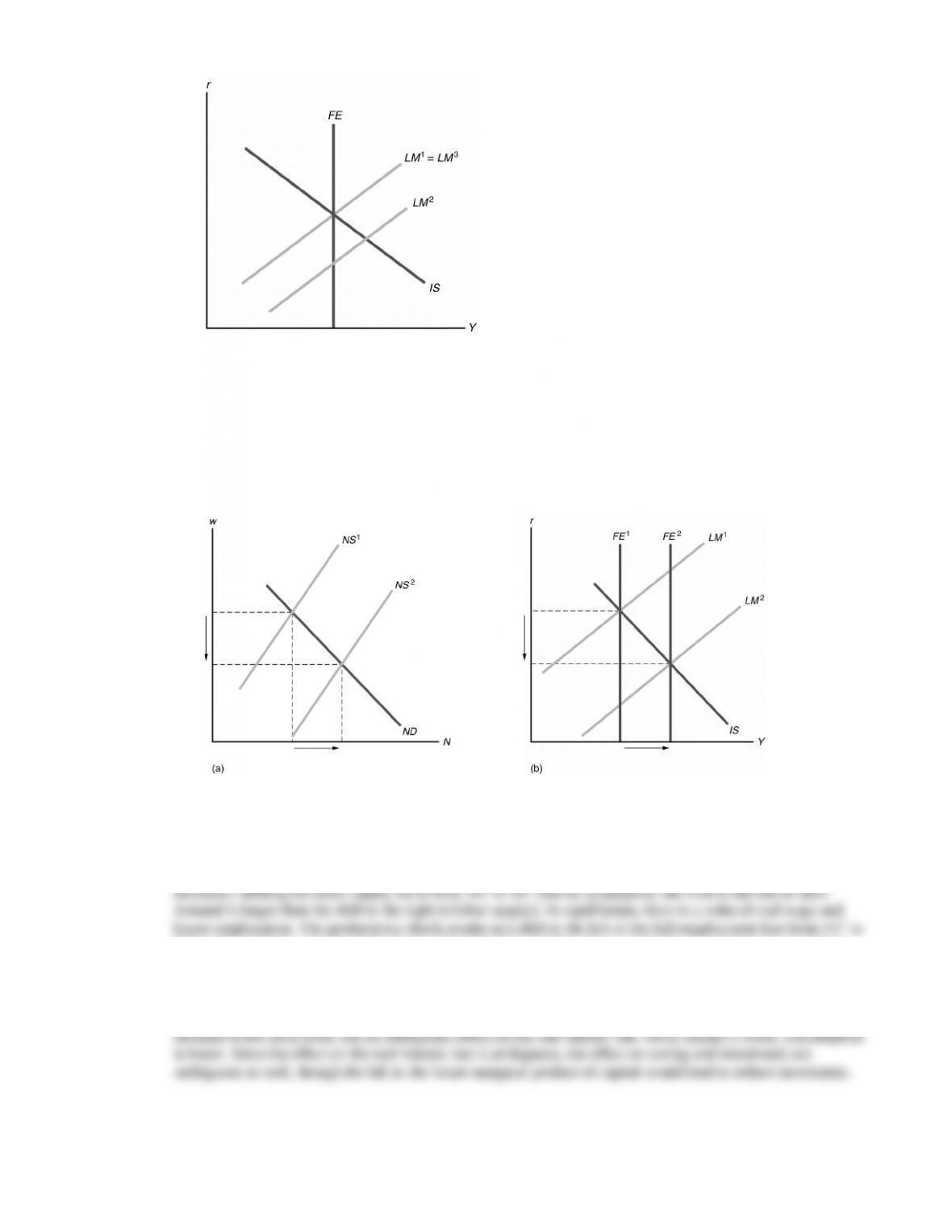

1. (a) The increase in desired investment shifts the IS curve up and to the right, as shown in Figure 9.21.

The price level rises, shifting the LM curve up and to the left to restore equilibrium. Since the real

interest rate rises, consumption declines. In summary, there is no change in the real wage,

employment, or output; there is a rise in the real interest rate, the price level, and investment; and

there is a decline in consumption.

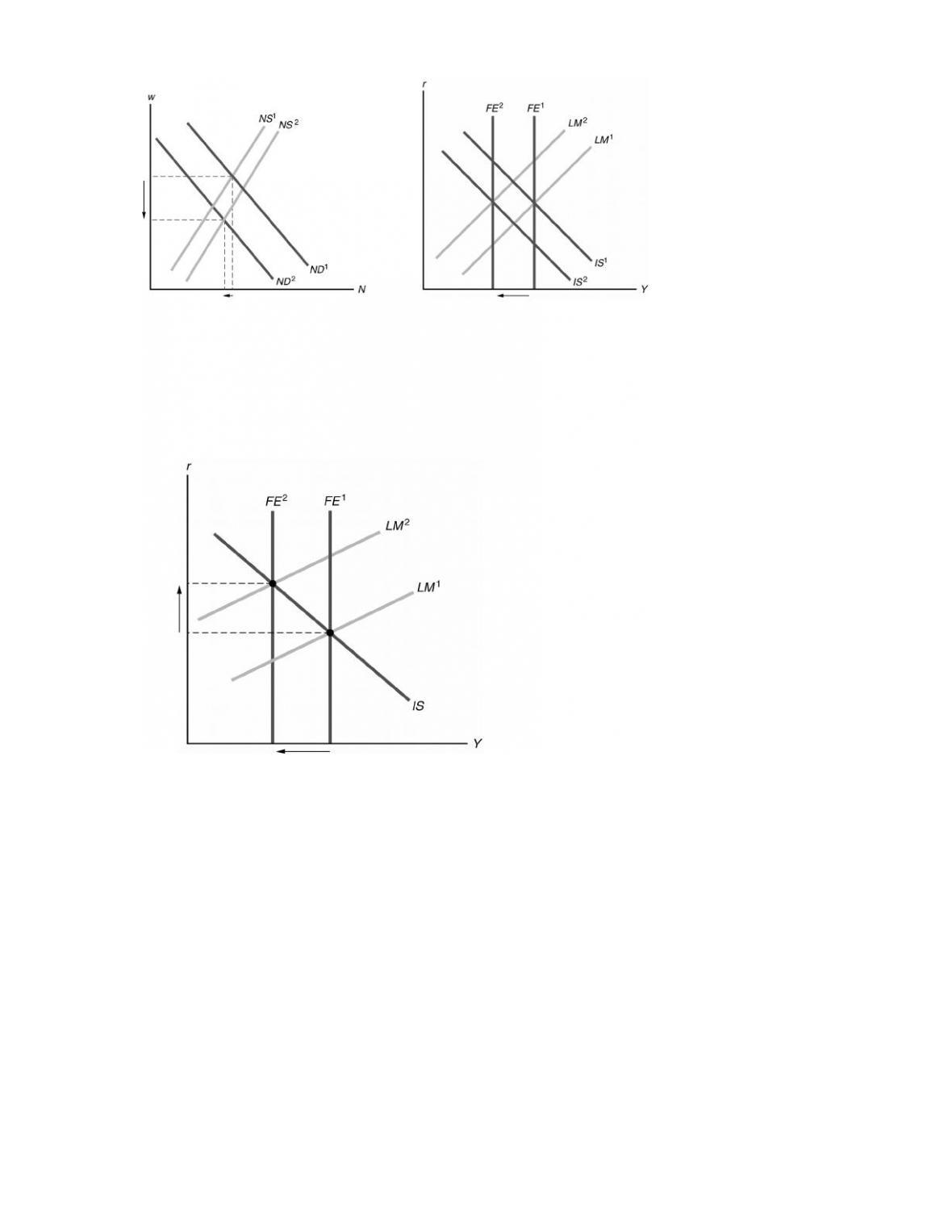

2. The increase in the price of oil reduces the marginal product of labor, causing the labor demand curve to shift to

the left from ND1 to ND2 in Figure 9.24. Since households’ expected future incomes decline, labor supply

FE2 in Figure 9.25, as both employment and productivity decline. Because the shock is permanent, it reduces

future output and reduces the future marginal product of capital, both of which result in a downward shift of the

IS curve. The new equilibrium is located at the intersection of the new IS curve and the new FE line. If, as shown

in the figure, this intersection lies above and to the left of the original LM curve, the price level will increase

and shift the LM curve upward (from LM1 to LM2) to pass through the new equilibrium point. The result is an

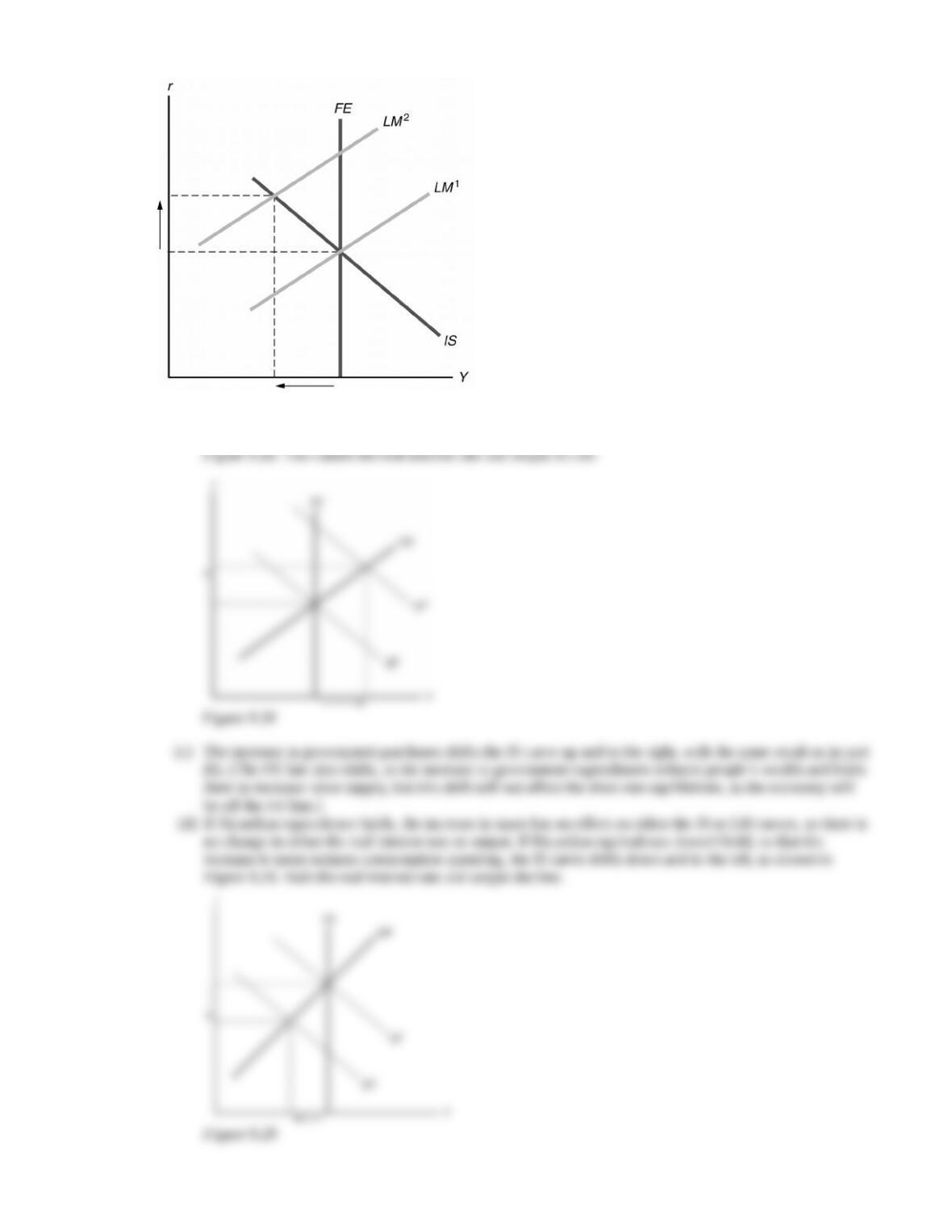

3. (a) The decrease in expected inflation increases real money demand, shifting the LM curve up, as shown in

Figure 9.27. The real interest rate rises and output declines.

Figure 9.27

(b) The increase in desired consumption shifts the IS curve up and to the right, as shown in

4. The change in Eq. (9.B.10) has no effect on employment, the real wage, or output. The only effect this has is on

the term IS, which is now IS [1 (1 t)cY iY]/(cr ir). The real interest rate and price level are still

5. The change in the money demand function affects only the equation determining the price level,

Eq. (9.B.23). It is now

3. The LM curve shows the combinations of output and the real interest rate that maintain equilibrium in

the asset market. Equilibrium in the asset market occurs when real money demand equals the real

money supply.

Figure 9.16 shows the derivation of the LM curve and why it slopes upward. An increase in output

from Y1 to Y2 raises money demand, shifting the money demand curve from MD(Y1) to MD(Y2). With

4. For constant output, if real money supply exceeds the real quantity of money demanded, the real

interest rate will decline to increase the real quantity of money demanded until equilibrium is

5. General equilibrium is a situation in which all markets in an economy are simultaneously in

equilibrium. This is shown in Figure 9.17 as the point at which the FE line and the IS and LM curves

6. There is monetary neutrality if a change in the nominal money supply changes the price level but has

no effect on real variables. Once prices adjust, money is neutral in the IS–LM model, because a

change in the money supply that shifts the LM curve is matched by a proportional change in the price

level that returns the real money supply back to its original level and moves the LM curve back to its

7. The aggregate demand curve relates the price level to the aggregate demand for goods and services. It

is downward sloping, because with a fixed nominal money supply, an increase in the price level shifts

the LM curve up, so the level of output at the IS-LM intersection is lower.

Factors that shift the aggregate demand curve up and to the right include (1) an increase in expected

future output, which reduces desired saving, raises desired consumption, and shifts the IS curve up

8. The short-run aggregate supply curve is horizontal and the long-run aggregate supply curve is

vertical. The short-run aggregate supply curve is horizontal because prices remain fixed in the short

9. In the short run, money is not neutral, but in the long run it is neutral. Suppose the economy is

initially in general equilibrium, as shown in Figure 9.18, where LRAS, SRAS1, and AD1 intersect.

Now suppose the money supply declines by 10%, so the aggregate demand curve shifts down and to

the left to AD2. In the short run, the equilibrium occurs at the intersection of AD2 and SRAS1, so output

1. (a) Sd Y Cd G

Y (4000 4000r 0.2Y) 2000

So 0.8Y 8400 8000r, or

8000r 8400 0.8Y.

(2) Using the equivalent equation that desired saving equals desired investment gives

0.8Y 8400 8000r, or

8000r 8400 0.8Y.

So we can use either equilibrium condition to get the same result.

8000r 8400 (0.8 10,000) 400,

so r 0.05.

8000r 8400 (0.8 10,200) 240,

so r 0.03.

8000r 8800 0.8Y.

Similarly, using the equation that goods supplied equals goods demanded gives:

So 0.8Y 8800 8000r, or

8000r 8800 0.8Y.

At Y 10,000, this is 8000r 8800 (0.8 10,000) 800, so r 0.10. The market-clearing real

IS2 in Figure 9.19.

Figure 9.19

2. (a) Md/P 3000 0.1Y 10,000i

3000 0.1Y – 10,000(r e)

6000/2 2800 0.1Y 10,000r

10,000r 200 0.1Y

r 0.02 (Y/100,000).

3300 2800 0.1Y – 10,000r

10,000r –500 0.1Y

r –0.05 (Y/100,000).

When Y 8000, r 0.03.

When Y 9000, r 0.04.

3000 2700 0.1Y 10,000r

10,000r 300 0.1Y

r 0.03 (Y/100,000).

When Y 8000, r 0.05.

When Y 9000, r 0.06.

3. (a) First, we’ll find the IS curve.

Sd Y – Cd – G Y [200 0.8(Y T) 500r] G Y [200 (0.6Y 16) 500r]

G

184 0.4Y 500r G

0.5Y 250r 25, which can be solved for Y 19,780/P 50 500 r.

With full-employment output of 1000, using this in the IS curve and solving for r gives r 0.18.

4. (a) First, look at labor market equilibrium.

Labor supply is NS 55 10(1 t)w. Labor demand (ND) comes from the equation w 5A

(0.005A ND). Substituting the latter equation into the former, and equating labor supply and

labor demand gives N 100. Using this in either the labor supply or labor demand equation then

gives w 9. Using N in the production function gives Y 950.

20.

(d) With G 72.5, the IS curve becomes r 1.367 – 0.004/3 Y. With Y 950, the IS curve gives

5. The IS curve is found by setting desired saving equal to desired investment. Desired saving is Sd

Y Cd G Y [1275 0.5(Y T) 200r] G. Setting Sd Id gives Y [1275 0.5(Y T)

200r] G 900 200r, or Y 4350 800r 2G T. The LM curve is M/P L 0.5Y 200i

0.5Y 200(r ) 0.5Y 200r.

(a) T G 450, M 9000. The IS curve gives Y 4350 800r 2G T 4350 800r (2

450) 450 4800 800r. The LM curve gives 9000/P 0.5Y 200r. To find the aggregate

demand curve, eliminate r in the two equations by multiplying the LM curve through by 4 and

800r 2Y 36,000/P. IS: Y 4800 800r. Rearranging gives 800r 4800 Y. Setting the

right-hand sides of these two equations to each other (since both equal 800r) gives: 2Y

(36,000/P) 4800 Y, or 3Y 4800 (36,000/P), or Y 1600 (12,000/P); this is the AD

curve.

With Y 4600 at full employment, the AD curve gives 4600 1600 (12,000/P), or P 4. From

330 4680 800r.

LM: 36,000/P 2Y 800r, or 800r 2Y 36,000/P.

IS: Y 4680 800r, or 800r 4680 Y.

AD: 2Y (36,000/P) 4680 Y, or (36,000/P) 4680 3Y, or Y 1560 (12,000/P).

6. (a) A 2, f1 5, f2 0.005, n0 55, nw 10, c0 300, cY 0.8, cr 200, t0 20, t 0.5, i0 258.5,

ir 250, l0 0, lY 0.5, lr 250.

1. (a) The increase in desired investment shifts the IS curve up and to the right, as shown in Figure 9.21.

The price level rises, shifting the LM curve up and to the left to restore equilibrium. Since the real

interest rate rises, consumption declines. In summary, there is no change in the real wage,

employment, or output; there is a rise in the real interest rate, the price level, and investment; and

there is a decline in consumption.

2. The increase in the price of oil reduces the marginal product of labor, causing the labor demand curve to shift to

the left from ND1 to ND2 in Figure 9.24. Since households’ expected future incomes decline, labor supply

FE2 in Figure 9.25, as both employment and productivity decline. Because the shock is permanent, it reduces

future output and reduces the future marginal product of capital, both of which result in a downward shift of the

IS curve. The new equilibrium is located at the intersection of the new IS curve and the new FE line. If, as shown

in the figure, this intersection lies above and to the left of the original LM curve, the price level will increase

and shift the LM curve upward (from LM1 to LM2) to pass through the new equilibrium point. The result is an

3. (a) The decrease in expected inflation increases real money demand, shifting the LM curve up, as shown in

Figure 9.27. The real interest rate rises and output declines.

Figure 9.27

(b) The increase in desired consumption shifts the IS curve up and to the right, as shown in

4. The change in Eq. (9.B.10) has no effect on employment, the real wage, or output. The only effect this has is on

the term IS, which is now IS [1 (1 t)cY iY]/(cr ir). The real interest rate and price level are still

5. The change in the money demand function affects only the equation determining the price level,

Eq. (9.B.23). It is now