1960 3.5% 4.0%

1965 3.5% 4.2%

1970 4.1% 5.5%

1975 5.0% 5.2%

1980 6.0% 5.9%

1985 5.2% 7.6%

1990 7.5% 8.4%

1995 9.3% 10.4%

2000 10.6% 14.6%

2005

2010

10.3%

12.8%

16.1%

16.0%

2. Should We Run Balance of Payments Surpluses?

Because people seem worried that the United States has run continual balance of payments deficits, you

3. Should We Worry About Foreign Ownership of U.S. Assets?

In 1994, Mexico faced severe economic problems when foreign investors began pulling their money out of

the country. Could the United States face a similar crisis? For example, in recent years, foreigners

(especially Japanese and Chinese investors) have purchased a large quantity of U.S. government bonds.

Also, as we’ll see in chapter 7, foreigners hold many U.S. dollars. What would happen if foreign investors

4. Should Countries Cooperate?

As we’ve seen in this chapter, government policies in one country may have effects in others. Fiscal and

monetary policies affect interest rates both at home and abroad. Yet for the most part, countries decide on

their fiscal and monetary policies independently of other countries. The question is, should this fact lead

1. Credit items in the current account are exports of goods and services and income receipts from

abroad. Debit items in the current account are imports of goods and services, income payments to

2. The current account includes only the trade of currently produced goods and services. Trades of

existing assets are counted in the capital and financial account.

3. The sale of books from the United States to Brazil is a credit item in the U.S. current account.

Offsetting transactions include anything that is a debit item in either the current account or the capital

4. In any period, the net amount of new foreign assets that a country acquires equals its current account

surplus, which in turn must equal its capital and financial account deficit. A country with greater net

5. In a small open economy, saving does not have to be equal to investment. Saving can be used to

finance domestic investment or it can be lent abroad. So saving equals investment plus net exports.

6. A small open economy is likely to run a large current account deficit and to borrow abroad if desired

investment increases substantially or if desired national saving declines substantially. Desired

investment could increase if there is an increase in the expected future marginal product of capital or

a decline in the user cost of capital, both of which would shift the desired investment curve to the

7. In a world with two large open economies, the world real interest rate is determined such that desired

international lending by one country equals desired international borrowing by the other country.

8. An increase in desired national saving in a large open economy reduces the world real interest rate.

The shift to the right in the saving curve increases the country’s current account at the current world

real interest rate, so the international asset market is out of equilibrium. To restore equilibrium, the

world real interest rate must fall.

An increase in desired investment has the opposite effect. The increase in investment reduces the

9. An increase in the government budget deficit raises the current account deficit of a small open

economy if and only if the increase in the budget deficit reduces national saving. Since the current

10. The twin deficits are the government budget deficit and the current account deficit. They are

connected because if an increase in the government budget deficit reduces national saving it leads

1.

Current Account Credit () Debits ()

Goods 100 125

Services 90 80

Income from/to foreigners 110 150

2. The following table calculates key variables for this question for different values of the real interest

rate. The column for S is calculated by the equation S Y (Cd G). The column headed S I is

5% 12 3 7 4 21 4

4% 13 4 6 2 23 2

3% 14 5 5 0 25 0

2% 15 6 4 –2 27 –2

Net exports and foreign lending are identical.

3. All variables but interest rates are in billions of dollars.

(a) S 10 (100 0.03) 13

15 (100 0.03) 12

13 12 1

( )

I

NX CA S I

C Y I G NX

= – ´ =

= = – = – =

= – + +

50 (12 10 1)

27

= – + +

=

A C I G

27 12 10

49

(b) S 13, as before.

17 (100 0.03) 14

13 14 1

( )

I

NX CA S I

C Y I G NX

= – ´ =

= = – = – =–

= – + +

50 (14 10 1)

27

= – + –

=

A C I G= + +

27 14 10

51

= + +

=

4. (a) To find the equilibrium interest rate (rw), we must first calculate the current account for each

country as a function of rw. Then we can find the value of rw that clears the goods market, that is,

where CA CAFor 0.

Home:

For 480 0.4(1500 300) 300

480 480 300

960 300

d

w

w

C

r

r

w

r= + – –

= + –

= –

CAFor NXFor SdFor IdFor YFor (CdFor IdFor GFor)

1500 (960 300rw 225 300rw 300)

15 600 rw

At equilibrium, CA CAFor 0, so:

–65 400 rw 15 600 rw 0

–50 1000 rw 0

rw 0.05

C 640 200 rw 630

CFor 960 300 rw 945

S Y C G 1000 630 275 95

SFor YFor CFor GFor 1500 945 300 255

I 150 200 rw 140

IFor 225 300 rw 210

CA S I 95 140 45

CAFor SFor IFor 255 210 45

(b) Cd 320 0.4(1000 250) 200 rw

320 300 200 rw

620 200 rw

CA NX Sd Id Y (Cd Id G)

1000 (620 200 rw 150 200 rw 325)

95 400 rw

At equilibrium, CA CAFor 0, so:

95 400 rw 15 600 rw 0

80 1000 rw 0

rw 0.08

C 620 200 rw 604

CFor 960 300 rw 936

S Y C G 1000 604 325 71

SFor YFor CFor GFor 1500 936 300 264

I 150 200 rw 134

IFor 225 300 rw 201

CA S I 71 134 63

CAFor SFor IFor 264 201 63

So a balanced-budget increase in government spending increases the home country’s current

account deficit.

5. (a) SH YH CH GH

1000 [100 (0.5 1000) 500r] 155

245 500r

SF YF CF GF

1200 [225 (0.7 1200) 600r] 190

1800r 360

r 0.20

(c) CH 100 (0.5 1000) (500 0.20) 500

SH 245 (500 0.20) 345

IH 300 (500 0.20) 200

6. GDP Y $1,000,000 total production of coconuts

GNP $1,025,000 production of coconuts net factor income from abroad

NFP $25,000

I $0

S Y NFP C G $1,000,000 $25,000 $1,025,000 $0 $0

1. (a) Export of merchandise: entry in current account.

(b) No entry: just changes the type of foreigner holding U.S. assets.

2. There are many possible answers; an example for each is given here.

(a) U.S. citizens buy cars from the foreign country: entry in current account.

(b) No transaction needed.

(c) The Federal Reserve sells dollars to, and buys deutsche marks from, the Bundesbank (the central

3. In Figure 5.3, before the capital controls are imposed, the home country has a current account deficit

of the amount CA, while the foreign country has a matching current account surplus. The effect of the

4. In Figure 5.4, suppose initially that both countries have a zero current account. A rise in the

government budget deficit has no effect on desired investment, so it affects the current account only if

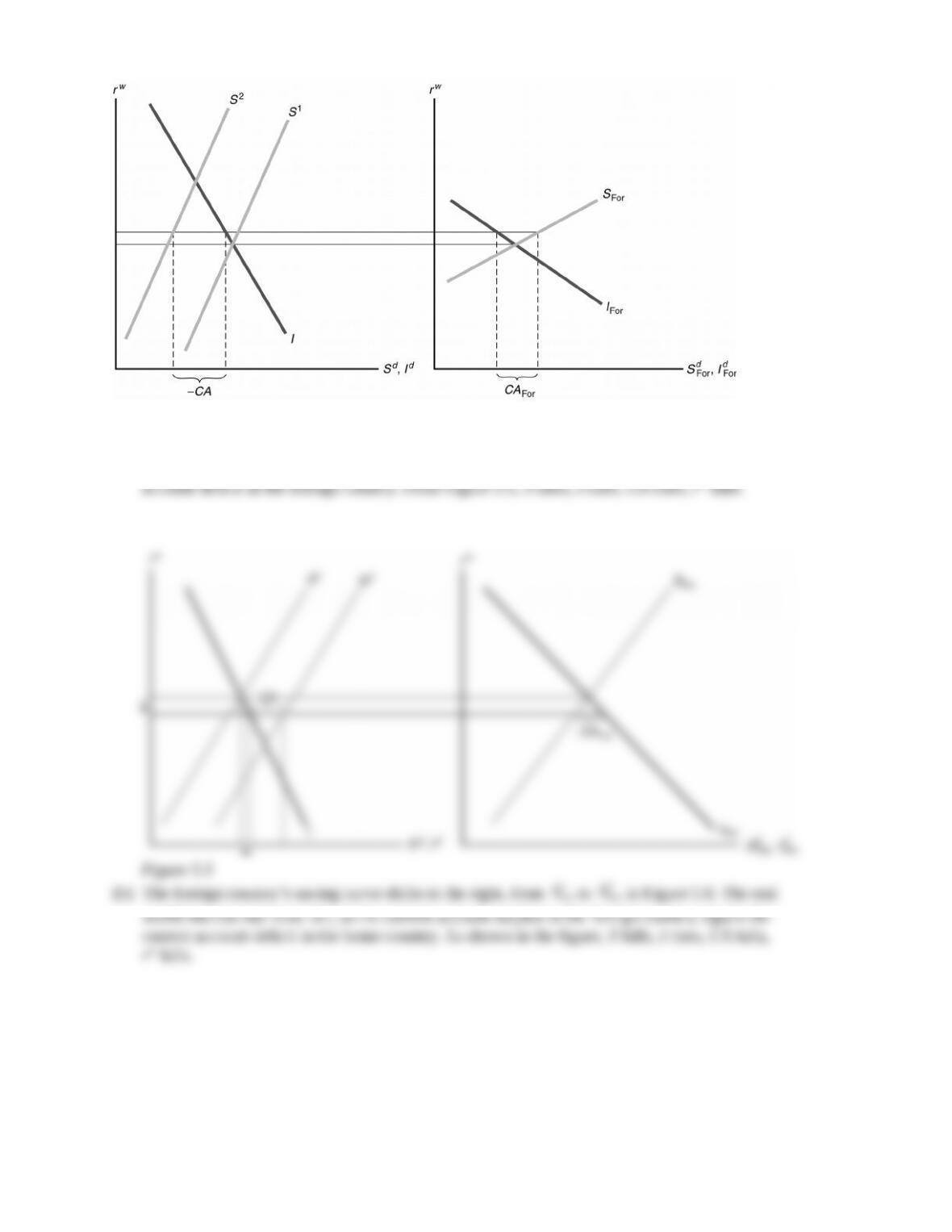

5. (a) The home country’s saving curve shifts to the right, from S1 to S2 in Figure 5.5. The real world

interest rate falls, so that the current account surplus in the home country equals the current

6.A temporary adverse supply shock hitting the foreign economy causes the foreign saving curve

1

2

rate, increasing home country saving and decreasing home country investment. Since saving rises

7. The shock shifts the saving curve to the right, with no change in the investment curve, since the

future marginal product of capital is unaffected. Since income rises and saving rises, consumption

8. Note that when the government of Eastland makes this change, it isn’t changing total government

purchases, so there’s no effect on national saving. Thus the current account balance is unaffected.

How can that be, given that Eastland’s government is now purchasing more goods from Westland?

The answer is that the private sector offsets the government’s actions by increasing its net exports

As we’ve seen in this chapter, government policies in one country may have effects in others. Fiscal and

monetary policies affect interest rates both at home and abroad. Yet for the most part, countries decide on

their fiscal and monetary policies independently of other countries. The question is, should this fact lead

1. Credit items in the current account are exports of goods and services and income receipts from

abroad. Debit items in the current account are imports of goods and services, income payments to

2. The current account includes only the trade of currently produced goods and services. Trades of

existing assets are counted in the capital and financial account.

3. The sale of books from the United States to Brazil is a credit item in the U.S. current account.

Offsetting transactions include anything that is a debit item in either the current account or the capital

4. In any period, the net amount of new foreign assets that a country acquires equals its current account

surplus, which in turn must equal its capital and financial account deficit. A country with greater net

5. In a small open economy, saving does not have to be equal to investment. Saving can be used to

finance domestic investment or it can be lent abroad. So saving equals investment plus net exports.

6. A small open economy is likely to run a large current account deficit and to borrow abroad if desired

investment increases substantially or if desired national saving declines substantially. Desired

investment could increase if there is an increase in the expected future marginal product of capital or

a decline in the user cost of capital, both of which would shift the desired investment curve to the

7. In a world with two large open economies, the world real interest rate is determined such that desired

international lending by one country equals desired international borrowing by the other country.

8. An increase in desired national saving in a large open economy reduces the world real interest rate.

The shift to the right in the saving curve increases the country’s current account at the current world

real interest rate, so the international asset market is out of equilibrium. To restore equilibrium, the

world real interest rate must fall.

An increase in desired investment has the opposite effect. The increase in investment reduces the

9. An increase in the government budget deficit raises the current account deficit of a small open

economy if and only if the increase in the budget deficit reduces national saving. Since the current

10. The twin deficits are the government budget deficit and the current account deficit. They are

connected because if an increase in the government budget deficit reduces national saving it leads

1.

Current Account Credit () Debits ()

Goods 100 125

Services 90 80

Income from/to foreigners 110 150

2. The following table calculates key variables for this question for different values of the real interest

rate. The column for S is calculated by the equation S Y (Cd G). The column headed S I is

5% 12 3 7 4 21 4

4% 13 4 6 2 23 2

3% 14 5 5 0 25 0

2% 15 6 4 –2 27 –2

Net exports and foreign lending are identical.

3. All variables but interest rates are in billions of dollars.

(a) S 10 (100 0.03) 13

15 (100 0.03) 12

13 12 1

( )

I

NX CA S I

C Y I G NX

= – ´ =

= = – = – =

= – + +

50 (12 10 1)

27

= – + +

=

A C I G

27 12 10

49

(b) S 13, as before.

17 (100 0.03) 14

13 14 1

( )

I

NX CA S I

C Y I G NX

= – ´ =

= = – = – =–

= – + +

50 (14 10 1)

27

= – + –

=

A C I G= + +

27 14 10

51

= + +

=

4. (a) To find the equilibrium interest rate (rw), we must first calculate the current account for each

country as a function of rw. Then we can find the value of rw that clears the goods market, that is,

where CA CAFor 0.

Home:

For 480 0.4(1500 300) 300

480 480 300

960 300

d

w

w

C

r

r

w

r= + – –

= + –

= –

CAFor NXFor SdFor IdFor YFor (CdFor IdFor GFor)

1500 (960 300rw 225 300rw 300)

15 600 rw

At equilibrium, CA CAFor 0, so:

–65 400 rw 15 600 rw 0

–50 1000 rw 0

rw 0.05

C 640 200 rw 630

CFor 960 300 rw 945

S Y C G 1000 630 275 95

SFor YFor CFor GFor 1500 945 300 255

I 150 200 rw 140

IFor 225 300 rw 210

CA S I 95 140 45

CAFor SFor IFor 255 210 45

(b) Cd 320 0.4(1000 250) 200 rw

320 300 200 rw

620 200 rw

CA NX Sd Id Y (Cd Id G)

1000 (620 200 rw 150 200 rw 325)

95 400 rw

At equilibrium, CA CAFor 0, so:

95 400 rw 15 600 rw 0

80 1000 rw 0

rw 0.08

C 620 200 rw 604

CFor 960 300 rw 936

S Y C G 1000 604 325 71

SFor YFor CFor GFor 1500 936 300 264

I 150 200 rw 134

IFor 225 300 rw 201

CA S I 71 134 63

CAFor SFor IFor 264 201 63

So a balanced-budget increase in government spending increases the home country’s current

account deficit.

5. (a) SH YH CH GH

1000 [100 (0.5 1000) 500r] 155

245 500r

SF YF CF GF

1200 [225 (0.7 1200) 600r] 190

1800r 360

r 0.20

(c) CH 100 (0.5 1000) (500 0.20) 500

SH 245 (500 0.20) 345

IH 300 (500 0.20) 200

6. GDP Y $1,000,000 total production of coconuts

GNP $1,025,000 production of coconuts net factor income from abroad

NFP $25,000

I $0

S Y NFP C G $1,000,000 $25,000 $1,025,000 $0 $0

1. (a) Export of merchandise: entry in current account.

(b) No entry: just changes the type of foreigner holding U.S. assets.

2. There are many possible answers; an example for each is given here.

(a) U.S. citizens buy cars from the foreign country: entry in current account.

(b) No transaction needed.

(c) The Federal Reserve sells dollars to, and buys deutsche marks from, the Bundesbank (the central

3. In Figure 5.3, before the capital controls are imposed, the home country has a current account deficit

of the amount CA, while the foreign country has a matching current account surplus. The effect of the

4. In Figure 5.4, suppose initially that both countries have a zero current account. A rise in the

government budget deficit has no effect on desired investment, so it affects the current account only if

5. (a) The home country’s saving curve shifts to the right, from S1 to S2 in Figure 5.5. The real world

interest rate falls, so that the current account surplus in the home country equals the current

6.A temporary adverse supply shock hitting the foreign economy causes the foreign saving curve

1

2

rate, increasing home country saving and decreasing home country investment. Since saving rises

7. The shock shifts the saving curve to the right, with no change in the investment curve, since the

future marginal product of capital is unaffected. Since income rises and saving rises, consumption

8. Note that when the government of Eastland makes this change, it isn’t changing total government

purchases, so there’s no effect on national saving. Thus the current account balance is unaffected.

How can that be, given that Eastland’s government is now purchasing more goods from Westland?

The answer is that the private sector offsets the government’s actions by increasing its net exports