Additional Issues for Classroom Discussion

1. Should the Federal Reserve Be More Responsive to the Public?

Central banks in different countries vary dramatically in both their degree of independence from political

pressure and the degree of accountability for their actions. Is the U.S. Federal Reserve sufficiently

independent and accountable for optimal policymaking?

In discussing this topic, you should note that most power in the Fed resides with the Chairman and the

2. Should the Fed Deliberately Reduce Inflation, or Wait for a Recession?

Recently some members of the Federal Open Market Committee have discussed how actively the Fed

should reduce the inflation rate in moving to its long-run goal of zero inflation. Should the Fed actively

tighten monetary policy, or wait for the right circumstances to reduce inflation, since inflation generally

falls in a recession?

1. The monetary base, or high-powered money, consists of the sum of currency held by the non-bank

public and banks’ reserves. In an all-currency economy, the money supply equals the monetary base;

2. The money multiplier is the number of dollars of the money supply that can be created from each

dollar of monetary base. Changes in the desire by the public for holding currency affect the currency-

deposit ratio, thus changing the money multiplier. Similarly, changes in banks’ desire to hold reserves

affect the reserve-deposit ratio, thus changing the money multiplier. Increases in either the currency-

deposit ratio or the reserve-deposit ratio reduce the money multiplier. But these effects do not mean

that the central bank cannot control the money supply, because changes in the money multiplier can

be offset by changes in the monetary base to leave the money supply unchanged.

3. An open-market purchase increases the monetary base. The increase in the monetary base leads to an

increase in the money supply through the multiple expansions of loans and deposits.

4. Monetary policy in the United States is determined by the Federal Reserve System. The President

appoints the seven members of the Board of Governors of the Federal Reserve System, including the

5. Means of controlling the money supply other than open-market operations include:

(1) Reserve requirements. An increase in reserve requirements forces banks to hold more reserves,

increasing the reserve-deposit ratio, thus reducing the money multiplier. With a lower money

multiplier, the money supply is reduced for a given size of the monetary base.

6. Intermediate targets are macroeconomic variables that the Fed cannot directly control, but can

influence fairly predictably, and that are related to the ultimate goals of monetary policy. The ultimate

goals of monetary policy are achieving price stability and promoting stable growth of aggregate

economic activity. Since the Fed can’t control its ultimate goals directly, it influences its intermediate

7. The three main sources of uncertainty that affect monetary policymakers are (1) uncertainty about the

current state of the economy; (2) incompleteness of their models of the economy; and (3) uncertainty

about how the expectations of the public will be affected by economic shocks and policy actions.

Examples of uncertainty about the current state of the economy include the fact that different

economic variables often give conflicting signals about the current strength of the economy and the

8. The three tools the Fed used in the Great Recession to avoid problems caused by the zero lower

bound include forward guidance, credit easing, and quantitative easing. Using forward guidance, the

9. The monetarist response to the argument that discretion is more flexible than following a rule is to

argue that (1) because of information lags, it is difficult for the central bank to tell what the appropriate

policy is at a particular time; (2) there are long and variable lags between monetary policy actions and

their economic results; and (3) the lags mean that by the time a policy change has an effect, it may be

10. The Taylor rule sets the Fed funds rate target depending on recent inflation, the deviation of output

from the level of full-employment output, and the deviation of recent inflation from its target of 2%.

11.Inflation targeting may improve a central bank’s credibility because the public can easily observe

whether the central bank has achieved its goals. The main disadvantage is the long lag between

1. Initial balance sheet of banks (all amounts in dollars):

Assets Liabilities

Reserves 500,000 Deposits 500,000

Banks want to hold reserves equal to only 20% of deposits. This is 0.20 500,000 100,000. So

Loans 400,000

Banks still want reserves to equal just 20% of deposits, or 0.20 700,000 140,000. Since they are

still holding reserves of 300,000, they can lend another 160,000. Of this amount, 80,000 comes back

to the bank in the form of new deposits, and the other 80,000 is held by the public in the form of

2. Dollar amounts are in millions of dollars.

(a) DEP M CU 6 2 4. RES res DEP 0.25 4 1.

3. (a) res 0.4 2(0.10) 0.2.

Multiplier (cu 1)/(cu res) (0.4 1)/(0.4 0.2) 2 1/3.

M multiplier BASE 2 1/3 60 140.

Setting M/P L gives 140/1 0.5Y 10(0.10), or 140 1 0.5Y, which has the solution Y 282.

at 140. Setting M/P L gives 140/1 0.5Y (10 0.05), or 140 0.5 0.5Y, which has the

solution Y 281.

(d) If the reserve-deposit ratio is unaffected by the real interest rate, the LM curve is steeper than

when it is affected by the real interest rate. To see why, consider the effect of a decline in the real

interest rate. If the reserve-deposit ratio is affected by the real interest rate, the fall in the real

4. (a) The Taylor rule is i 0.02 0.5y 0.5 ( 0.02). The inflation rate over the past year is

[(149.2 147.3)/147.3] = 0.013. The percentage deviation of output from potential output is

(12,892.5 13,534.2)/13,534.2 = 0.047. So the Taylor rule suggests a target Fed funds rate

equal to: i 0.02 0.5y 0.5 ( 0.02) 0.013 0.02 [0.5 (0.047)] 0.5[0.013 0.02]

0.041 = –4.1%. The Fed would like to set the Fed funds rate at a negative level, but nominal

interest rates cannot be negative.

1. (a) The increase in banks’ reserve-deposit ratio reduces the money multiplier, causing the money

supply to decline.

(b) The increased holding of cash raises the currency-deposit ratio, reducing the money multiplier

and causing the money supply to decline.

(c) The sale of gold to the public has the same effect as an open-market sale of government securities

2. To examine the Taylor rule, we’ll use the classical model with misperceptions.

(a) An increase in money demand causes the aggregate demand curve to shift down and to the left,

reducing the price level and inflation and decreasing output, if the money supply is unchanged.

In response to these changes in output and inflation, the Taylor rule decreases the nominal Fed

funds rate, which means the money supply is increased. This shifts the aggregate demand curve

3. (a) The investment tax credit causes desired investment to rise, shifting the IS curve up and to

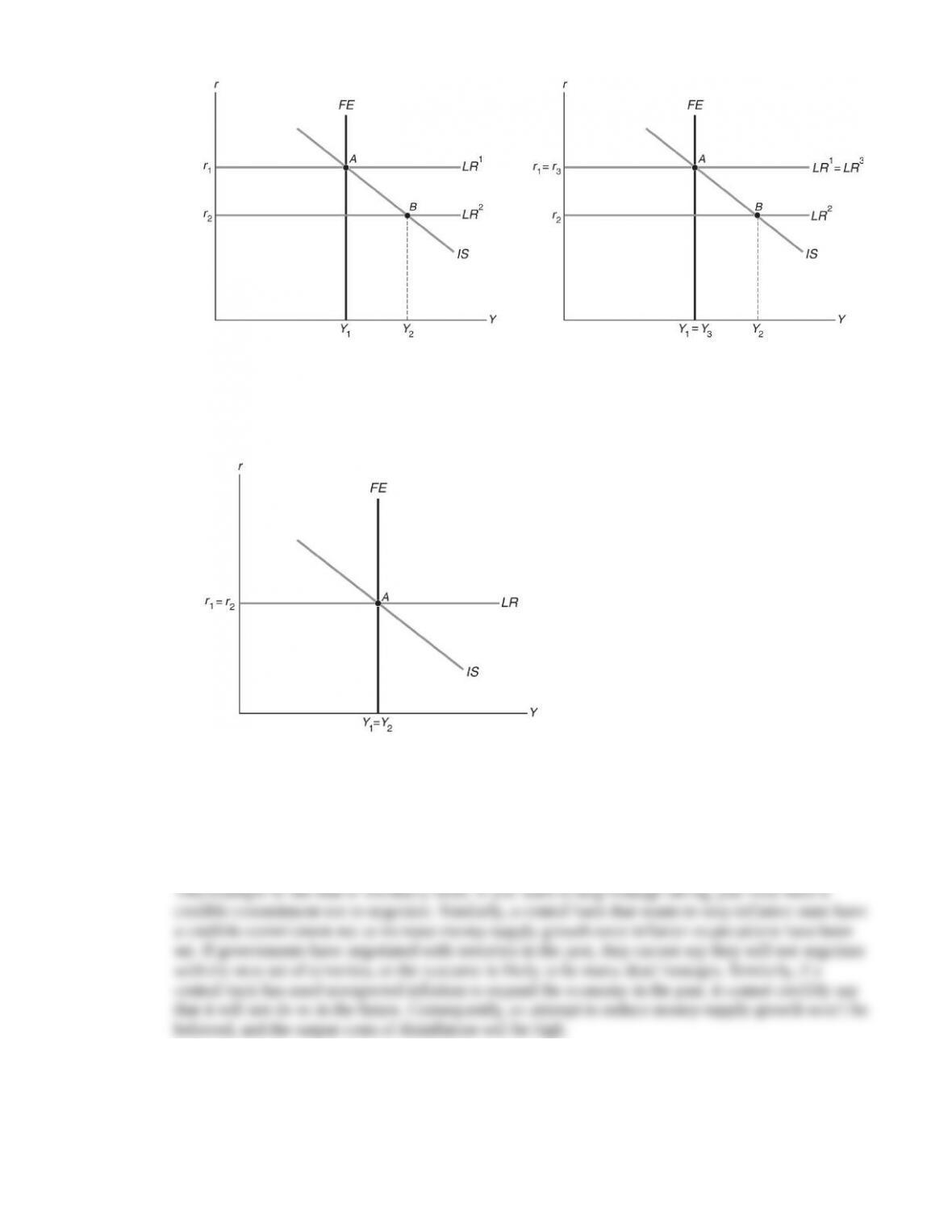

the right (Figure 14.4). The short-run equilibrium occurs at point B, with a higher level of output

and an unchanged real interest rate. In the long run (Figure 14.5), the equilibrium must occur at

the intersection of the FE line and the IS curve, so the existing real interest rate is not tenable; the

price level will increase, causing the LM curve to shift up and to the left, leading the LR curve to

4. Governments have policies against negotiating with hostage-taking terrorists, because if they

negotiate with some terrorists, more terrorists will take hostages in the future. Then they cannot

credibly say they will not negotiate with the next set of terrorists. If the government commits to never

negotiate with terrorists, then there is no gain to the terrorists for taking hostages, so there will be less

terrorism.

3. An open-market purchase increases the monetary base. The increase in the monetary base leads to an

increase in the money supply through the multiple expansions of loans and deposits.

4. Monetary policy in the United States is determined by the Federal Reserve System. The President

appoints the seven members of the Board of Governors of the Federal Reserve System, including the

5. Means of controlling the money supply other than open-market operations include:

(1) Reserve requirements. An increase in reserve requirements forces banks to hold more reserves,

increasing the reserve-deposit ratio, thus reducing the money multiplier. With a lower money

multiplier, the money supply is reduced for a given size of the monetary base.

6. Intermediate targets are macroeconomic variables that the Fed cannot directly control, but can

influence fairly predictably, and that are related to the ultimate goals of monetary policy. The ultimate

goals of monetary policy are achieving price stability and promoting stable growth of aggregate

economic activity. Since the Fed can’t control its ultimate goals directly, it influences its intermediate

7. The three main sources of uncertainty that affect monetary policymakers are (1) uncertainty about the

current state of the economy; (2) incompleteness of their models of the economy; and (3) uncertainty

about how the expectations of the public will be affected by economic shocks and policy actions.

Examples of uncertainty about the current state of the economy include the fact that different

economic variables often give conflicting signals about the current strength of the economy and the

8. The three tools the Fed used in the Great Recession to avoid problems caused by the zero lower

bound include forward guidance, credit easing, and quantitative easing. Using forward guidance, the

9. The monetarist response to the argument that discretion is more flexible than following a rule is to

argue that (1) because of information lags, it is difficult for the central bank to tell what the appropriate

policy is at a particular time; (2) there are long and variable lags between monetary policy actions and

their economic results; and (3) the lags mean that by the time a policy change has an effect, it may be

10. The Taylor rule sets the Fed funds rate target depending on recent inflation, the deviation of output

from the level of full-employment output, and the deviation of recent inflation from its target of 2%.

11.Inflation targeting may improve a central bank’s credibility because the public can easily observe

whether the central bank has achieved its goals. The main disadvantage is the long lag between

1. Initial balance sheet of banks (all amounts in dollars):

Assets Liabilities

Reserves 500,000 Deposits 500,000

Banks want to hold reserves equal to only 20% of deposits. This is 0.20 500,000 100,000. So

Loans 400,000

Banks still want reserves to equal just 20% of deposits, or 0.20 700,000 140,000. Since they are

still holding reserves of 300,000, they can lend another 160,000. Of this amount, 80,000 comes back

to the bank in the form of new deposits, and the other 80,000 is held by the public in the form of

2. Dollar amounts are in millions of dollars.

(a) DEP M CU 6 2 4. RES res DEP 0.25 4 1.

3. (a) res 0.4 2(0.10) 0.2.

Multiplier (cu 1)/(cu res) (0.4 1)/(0.4 0.2) 2 1/3.

M multiplier BASE 2 1/3 60 140.

Setting M/P L gives 140/1 0.5Y 10(0.10), or 140 1 0.5Y, which has the solution Y 282.

at 140. Setting M/P L gives 140/1 0.5Y (10 0.05), or 140 0.5 0.5Y, which has the

solution Y 281.

(d) If the reserve-deposit ratio is unaffected by the real interest rate, the LM curve is steeper than

when it is affected by the real interest rate. To see why, consider the effect of a decline in the real

interest rate. If the reserve-deposit ratio is affected by the real interest rate, the fall in the real

4. (a) The Taylor rule is i 0.02 0.5y 0.5 ( 0.02). The inflation rate over the past year is

[(149.2 147.3)/147.3] = 0.013. The percentage deviation of output from potential output is

(12,892.5 13,534.2)/13,534.2 = 0.047. So the Taylor rule suggests a target Fed funds rate

equal to: i 0.02 0.5y 0.5 ( 0.02) 0.013 0.02 [0.5 (0.047)] 0.5[0.013 0.02]

0.041 = –4.1%. The Fed would like to set the Fed funds rate at a negative level, but nominal

interest rates cannot be negative.

1. (a) The increase in banks’ reserve-deposit ratio reduces the money multiplier, causing the money

supply to decline.

(b) The increased holding of cash raises the currency-deposit ratio, reducing the money multiplier

and causing the money supply to decline.

(c) The sale of gold to the public has the same effect as an open-market sale of government securities

2. To examine the Taylor rule, we’ll use the classical model with misperceptions.

(a) An increase in money demand causes the aggregate demand curve to shift down and to the left,

reducing the price level and inflation and decreasing output, if the money supply is unchanged.

In response to these changes in output and inflation, the Taylor rule decreases the nominal Fed

funds rate, which means the money supply is increased. This shifts the aggregate demand curve

3. (a) The investment tax credit causes desired investment to rise, shifting the IS curve up and to

the right (Figure 14.4). The short-run equilibrium occurs at point B, with a higher level of output

and an unchanged real interest rate. In the long run (Figure 14.5), the equilibrium must occur at

the intersection of the FE line and the IS curve, so the existing real interest rate is not tenable; the

price level will increase, causing the LM curve to shift up and to the left, leading the LR curve to

4. Governments have policies against negotiating with hostage-taking terrorists, because if they

negotiate with some terrorists, more terrorists will take hostages in the future. Then they cannot

credibly say they will not negotiate with the next set of terrorists. If the government commits to never

negotiate with terrorists, then there is no gain to the terrorists for taking hostages, so there will be less

terrorism.