Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

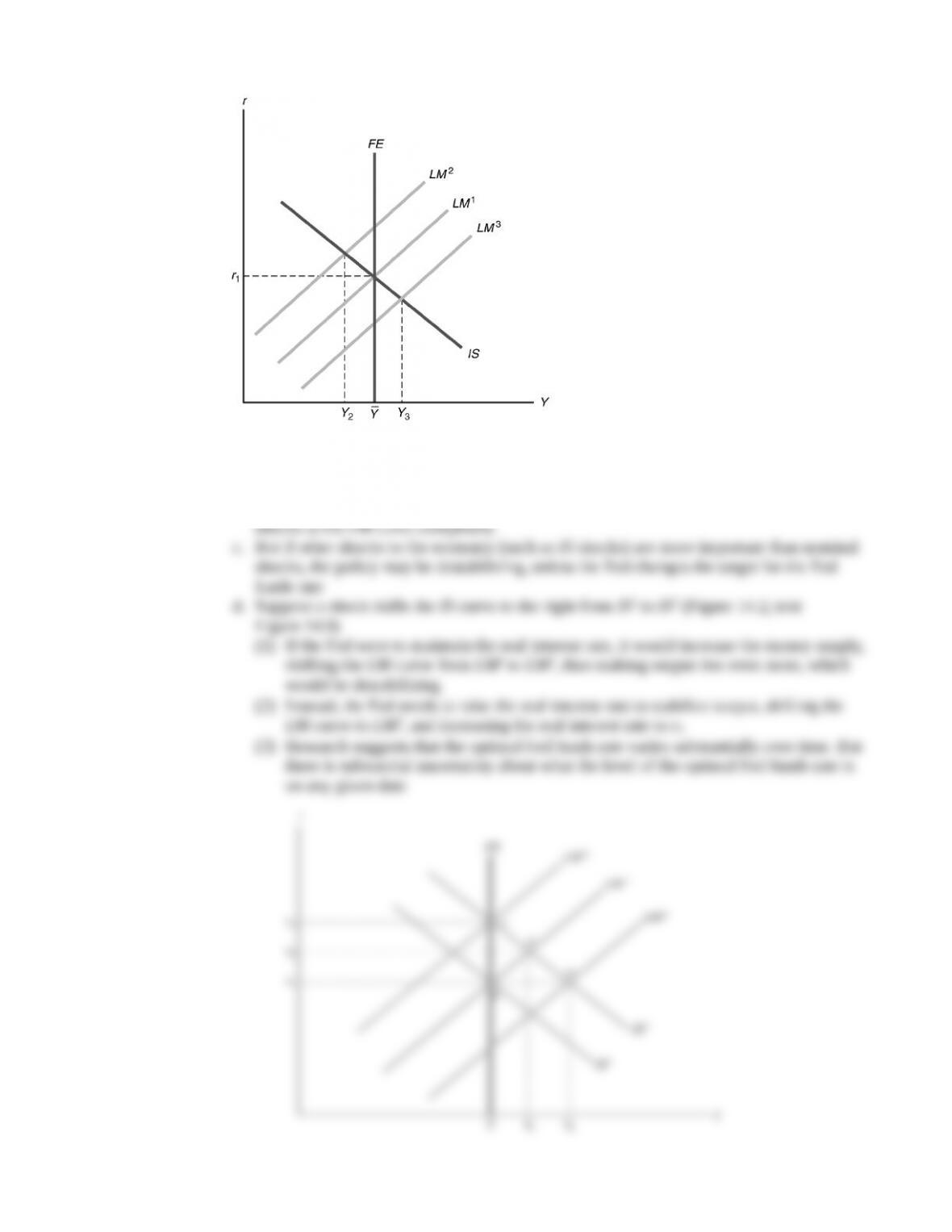

Figure 14.1

a. This strategy works well if the main shocks to the economy are to the LM curve

(shocks to money supply or money demand)

b. The strategy stabilizes output, the real interest rate, and the price level, as it offsets the

there is substantial uncertainty about what the level of the optimal Fed funds rate is

on any given date

6. The LR curve

a. If the Fed is targeting a real interest rate, then a modification of the LM curve will

simplify our analysis

(1) We can replace the LM curve with a horizontal line drawn at the target real interest

rate, rT (Figure 14.3; text Figure 14.10). The horizontal line is labeled LR

1. In fact, it isn’t so easy because of lags in the effect of policy and uncertainty about the state

of the economy, economic models, and expectations

1. It takes a fairly long time for changes in monetary policy to have an impact on

the economy

2. Interest rates change quickly, but output and inflation barely respond in the first four months

after the change in money growth (text Figure 14.11)

3. Tighter monetary policy causes real GDP to decline sharply after about four months, with

the full effect being felt about 16 to 20 months after the change in policy

4. Inflation responds even more slowly, remaining essentially unchanged for the first year,

then declining somewhat

5. These long lags make it very difficult to use monetary policy to control the economy very

precisely

6. Because of the lags, policy must be made based on forecasts of the future, but forecasts are

often inaccurate

7. The Fed has made preemptive strikes against inflation based on forecasts of higher future

inflation

Policy Application

Alan Blinder, an economist from Princeton University who served several years in the Federal

1. Uncertainty about state of economy

a. Conflicting signals from data

2. Incomplete models of the economy

a. No one knows the best model that describes the economy (classical vs. Keynesian,

slopes and locations of curves, levels of full-employment output and natural rate of

unemployment)

3. Uncertainty about how expectations of public will be affected by shocks and policy

actions

1. The housing crisis, which began in 2007, led to losses at financial institutions, but no one

thought it would lead to a major financial crisis

2. In the Great Recession, the economy deteriorated rapidly in late 2008 and early 2009; the

recession rivaled those of 1973-1975 and 1981-1982, and the recovery from the recession

3. The Zero Lower Bound

a. The Fed cut interest rates to near zero by the end of 2008, hitting the zero lower bound

b. In such a liquidity trap, increases in the money supply are held by banks or the public,

and have no effect on spending

c. To escape the problems caused by the zero lower bound, the Fed took unusual policy

1. Financial institution troubles that began in 2007 represented a shock, shifting the IS curve

down and to the left as housing investment declined

2. Banks began to reduce credit availability because of worries that some financial

institutions were no longer viable because of losses on mortgage-backed securities; in

3. The recession that began in December 2007 seemed mild through September 2008, but

then failures at Fannie Mae, Freddie Mac, Lehman Brothers, and AIG led to panic by

4. The panic led to a sharp decline in investment, shifting the IS curve further down and to

the left, so the Fed cut its interest rate target sharply, trying to shift the LM curve down

1. Rules make monetary policy automatic, as they require the central bank to set policy based

on a set of simple, prespecified, and publicly announced rules

2. Examples of rules

a. Increase the monetary base by 1% each quarter

3. The rule should be simple; there shouldn’t be much leeway for exceptions

4. The rule should specify something under the Fed’s control, like growth of the monetary base,

not something like fixing the unemployment rate at 4%, over which the Fed has little control

5. The rule may also permit the Fed to respond to the state of the economy

B. Most Keynesian economists support discretion

1. Discretion means the central bank looks at all the information about the economy and uses its

judgment as to the best course of policy

2. Discretion gives the central bank the freedom to stimulate or contract the economy when

needed; it is thus called activist

3. Since discretion gives the central bank leeway to act, while rules constrain its behavior,

why would anyone suggest that the central bank follow rules?

1. Monetarism is an economic theory emphasizing the importance of monetary factors

in the economy

2. The leading monetarist is Milton Friedman, who has argued for many years (since 1959)

that the central bank should follow rules for setting policy

3. Friedman’s argument for rules comes from four main propositions

a. Proposition 1: Monetary policy has powerful short-run effects on the real economy. In the

longer run, however, changes in the money supply have their primary effect on the price

level

(1) This proposition comes from Friedman’s research with Anna Schwartz on monetary

1. New arguments for rules suggest that rules are valuable even if the central bank has a lot of

information and forms policy wisely

2. Rules, commitment, and credibility

a. How does a central bank gain credibility?

b. One way to get credibility is by building a reputation for following through on its

promises, even if it’s costly in the short run

c. Another, less costly, way is to follow a rule that is enforced by some outside agency

1. John Taylor of Stanford University introduced a rule that allows the Fed to take economic

conditions into account

2. The rule is i 0.02 0.5y 0.5 ( 0.02), (14.6)

where i is the nominal Fed funds rate, is the inflation rate over the last 4 quarters,

( )/y Y Y Y= - =

the percentage deviation of output from full-employment output

3. The rule works by having the real Fed funds rate (i ) respond to:

a. y, the difference between output and full-employment output

4. If either y or increase, the real Fed funds rate is increased, causing monetary policy to

tighten (and vice-versa)

5. Taylor showed that the rule is similar to what the Fed does in practice

6. Taylor advocates the use of the rule as a guideline for policy, not something to be followed

mechanically

7. The data show that in the 1960s and 1970s when the Fed set the Federal funds rate below the

rule’s suggestion, inflation rose; when the Fed set the Federal funds rate fairly close to the

8. In the 2000s, the Fed kept the Federal funds rate below the level suggested by the rule

because of concerns about deflation

9. Economists are experimenting with variations on the original rule, using forecasts rather than

past data and looking at different coefficients in the rule

10. Uncertainty about the output term in the Taylor rule is large because of data revisions and

uncertainty about potential output in real time

1. Appointing a “tough” central banker

a. Appointing someone who has a well-known reputation for being tough in fighting

2. Changing central bankers’ incentives

3. Increasing central bank independence

a. If the executive and legislative branches of government can’t interfere with the central

bank, people are more likely to believe that the central bank is committed to keeping

inflation low and won’t cause a political business cycle

1. Since 1989, some countries have adopted a system of inflation targeting

2. New Zealand was the pioneer, announcing explicit inflation targets that had to be met or else

the central bank’s governor could be fired

1 to 4 years

d. The major disadvantage of inflation targeting is that inflation responds to policy actions

with a long lag, so it’s hard to judge what policy actions are needed to hit the inflation

target and hard for the public to tell if the central bank is doing the right thing, so central

banks may miss their targets badly, losing credibility

6. The LR curve

a. If the Fed is targeting a real interest rate, then a modification of the LM curve will

simplify our analysis

(1) We can replace the LM curve with a horizontal line drawn at the target real interest

rate, rT (Figure 14.3; text Figure 14.10). The horizontal line is labeled LR

1. In fact, it isn’t so easy because of lags in the effect of policy and uncertainty about the state

of the economy, economic models, and expectations

1. It takes a fairly long time for changes in monetary policy to have an impact on

the economy

2. Interest rates change quickly, but output and inflation barely respond in the first four months

after the change in money growth (text Figure 14.11)

3. Tighter monetary policy causes real GDP to decline sharply after about four months, with

the full effect being felt about 16 to 20 months after the change in policy

4. Inflation responds even more slowly, remaining essentially unchanged for the first year,

then declining somewhat

5. These long lags make it very difficult to use monetary policy to control the economy very

precisely

6. Because of the lags, policy must be made based on forecasts of the future, but forecasts are

often inaccurate

7. The Fed has made preemptive strikes against inflation based on forecasts of higher future

inflation

Policy Application

Alan Blinder, an economist from Princeton University who served several years in the Federal

1. Uncertainty about state of economy

a. Conflicting signals from data

2. Incomplete models of the economy

a. No one knows the best model that describes the economy (classical vs. Keynesian,

slopes and locations of curves, levels of full-employment output and natural rate of

unemployment)

3. Uncertainty about how expectations of public will be affected by shocks and policy

actions

1. The housing crisis, which began in 2007, led to losses at financial institutions, but no one

thought it would lead to a major financial crisis

2. In the Great Recession, the economy deteriorated rapidly in late 2008 and early 2009; the

recession rivaled those of 1973-1975 and 1981-1982, and the recovery from the recession

3. The Zero Lower Bound

a. The Fed cut interest rates to near zero by the end of 2008, hitting the zero lower bound

b. In such a liquidity trap, increases in the money supply are held by banks or the public,

and have no effect on spending

c. To escape the problems caused by the zero lower bound, the Fed took unusual policy

1. Financial institution troubles that began in 2007 represented a shock, shifting the IS curve

down and to the left as housing investment declined

2. Banks began to reduce credit availability because of worries that some financial

institutions were no longer viable because of losses on mortgage-backed securities; in

3. The recession that began in December 2007 seemed mild through September 2008, but

then failures at Fannie Mae, Freddie Mac, Lehman Brothers, and AIG led to panic by

4. The panic led to a sharp decline in investment, shifting the IS curve further down and to

the left, so the Fed cut its interest rate target sharply, trying to shift the LM curve down

1. Rules make monetary policy automatic, as they require the central bank to set policy based

on a set of simple, prespecified, and publicly announced rules

2. Examples of rules

a. Increase the monetary base by 1% each quarter

3. The rule should be simple; there shouldn’t be much leeway for exceptions

4. The rule should specify something under the Fed’s control, like growth of the monetary base,

not something like fixing the unemployment rate at 4%, over which the Fed has little control

5. The rule may also permit the Fed to respond to the state of the economy

B. Most Keynesian economists support discretion

1. Discretion means the central bank looks at all the information about the economy and uses its

judgment as to the best course of policy

2. Discretion gives the central bank the freedom to stimulate or contract the economy when

needed; it is thus called activist

3. Since discretion gives the central bank leeway to act, while rules constrain its behavior,

why would anyone suggest that the central bank follow rules?

1. Monetarism is an economic theory emphasizing the importance of monetary factors

in the economy

2. The leading monetarist is Milton Friedman, who has argued for many years (since 1959)

that the central bank should follow rules for setting policy

3. Friedman’s argument for rules comes from four main propositions

a. Proposition 1: Monetary policy has powerful short-run effects on the real economy. In the

longer run, however, changes in the money supply have their primary effect on the price

level

(1) This proposition comes from Friedman’s research with Anna Schwartz on monetary

1. New arguments for rules suggest that rules are valuable even if the central bank has a lot of

information and forms policy wisely

2. Rules, commitment, and credibility

a. How does a central bank gain credibility?

b. One way to get credibility is by building a reputation for following through on its

promises, even if it’s costly in the short run

c. Another, less costly, way is to follow a rule that is enforced by some outside agency

1. John Taylor of Stanford University introduced a rule that allows the Fed to take economic

conditions into account

2. The rule is i 0.02 0.5y 0.5 ( 0.02), (14.6)

where i is the nominal Fed funds rate, is the inflation rate over the last 4 quarters,

( )/y Y Y Y= - =

the percentage deviation of output from full-employment output

3. The rule works by having the real Fed funds rate (i ) respond to:

a. y, the difference between output and full-employment output

4. If either y or increase, the real Fed funds rate is increased, causing monetary policy to

tighten (and vice-versa)

5. Taylor showed that the rule is similar to what the Fed does in practice

6. Taylor advocates the use of the rule as a guideline for policy, not something to be followed

mechanically

7. The data show that in the 1960s and 1970s when the Fed set the Federal funds rate below the

rule’s suggestion, inflation rose; when the Fed set the Federal funds rate fairly close to the

8. In the 2000s, the Fed kept the Federal funds rate below the level suggested by the rule

because of concerns about deflation

9. Economists are experimenting with variations on the original rule, using forecasts rather than

past data and looking at different coefficients in the rule

10. Uncertainty about the output term in the Taylor rule is large because of data revisions and

uncertainty about potential output in real time

1. Appointing a “tough” central banker

a. Appointing someone who has a well-known reputation for being tough in fighting

2. Changing central bankers’ incentives

3. Increasing central bank independence

a. If the executive and legislative branches of government can’t interfere with the central

bank, people are more likely to believe that the central bank is committed to keeping

inflation low and won’t cause a political business cycle

1. Since 1989, some countries have adopted a system of inflation targeting

2. New Zealand was the pioneer, announcing explicit inflation targets that had to be met or else

the central bank’s governor could be fired

1 to 4 years

d. The major disadvantage of inflation targeting is that inflation responds to policy actions

with a long lag, so it’s hard to judge what policy actions are needed to hit the inflation

target and hard for the public to tell if the central bank is doing the right thing, so central

banks may miss their targets badly, losing credibility