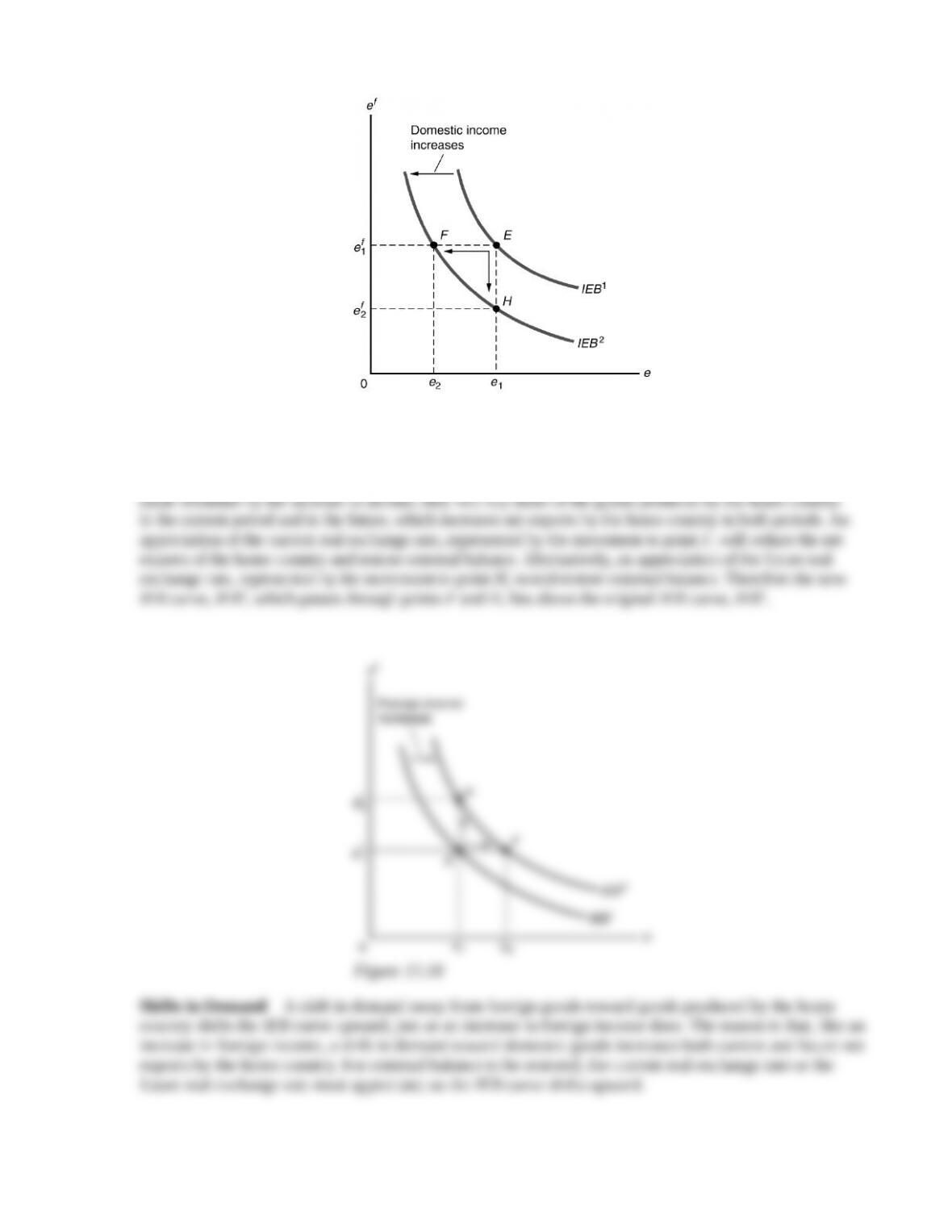

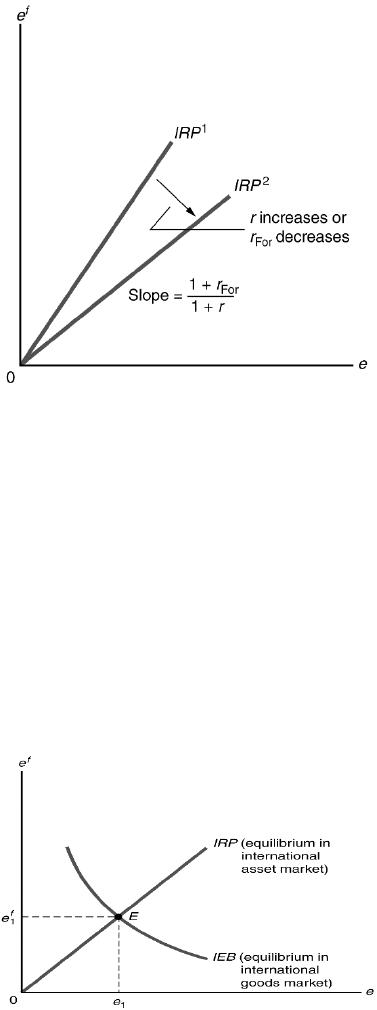

Figure 13.17

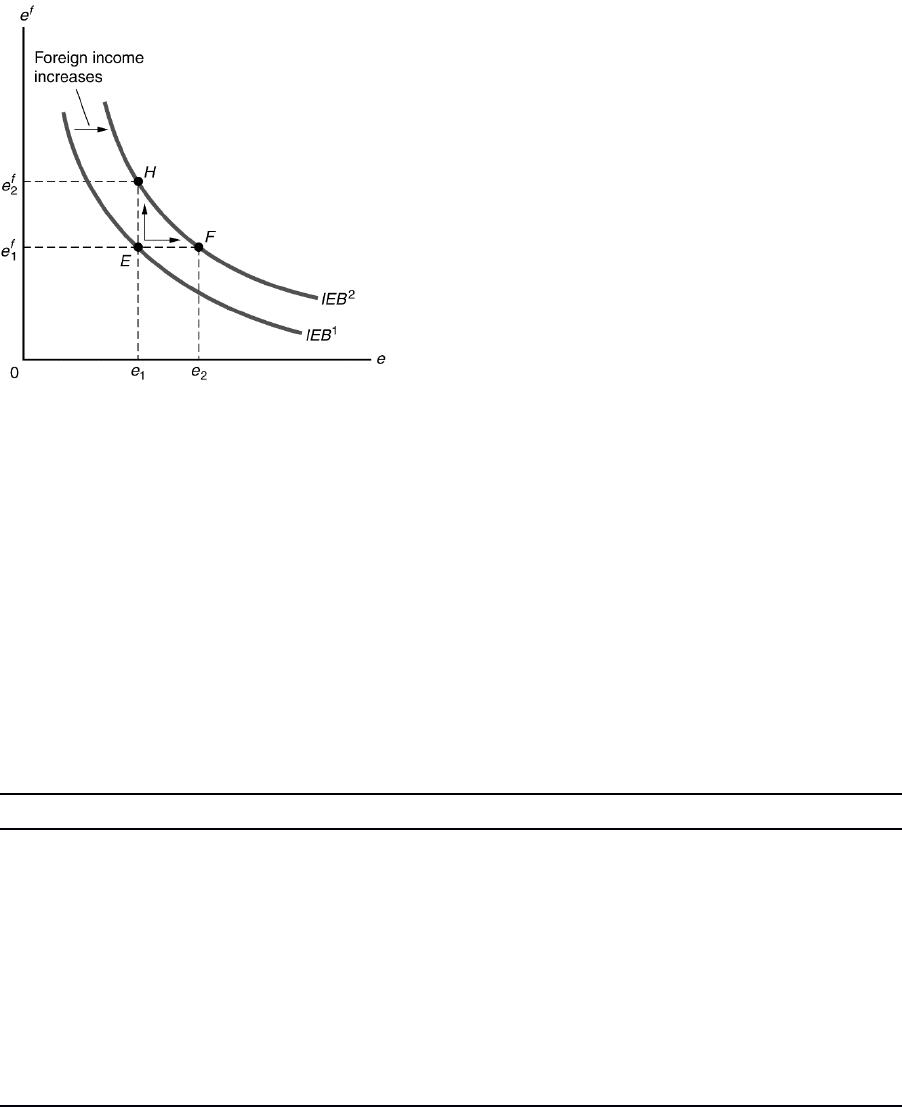

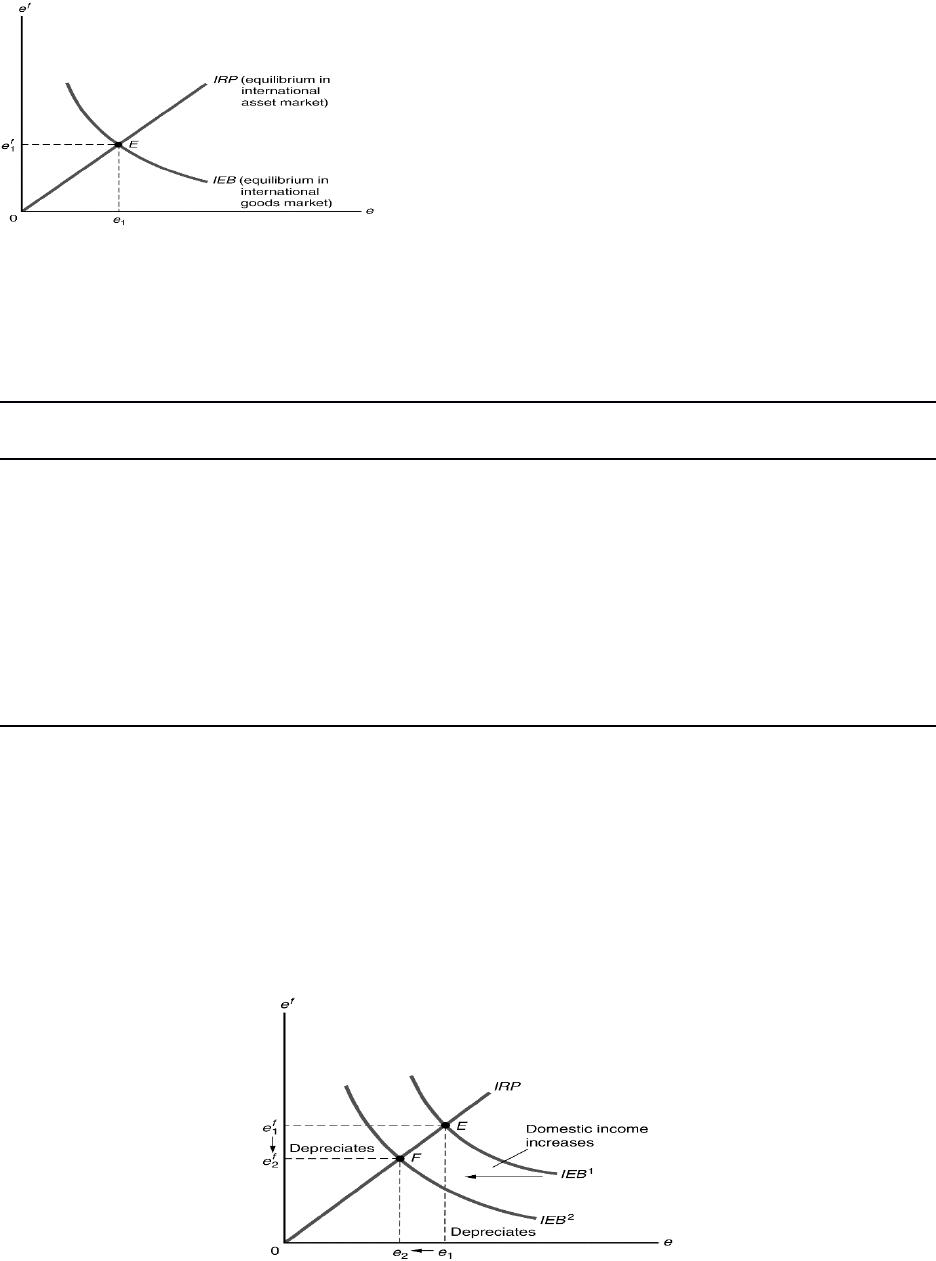

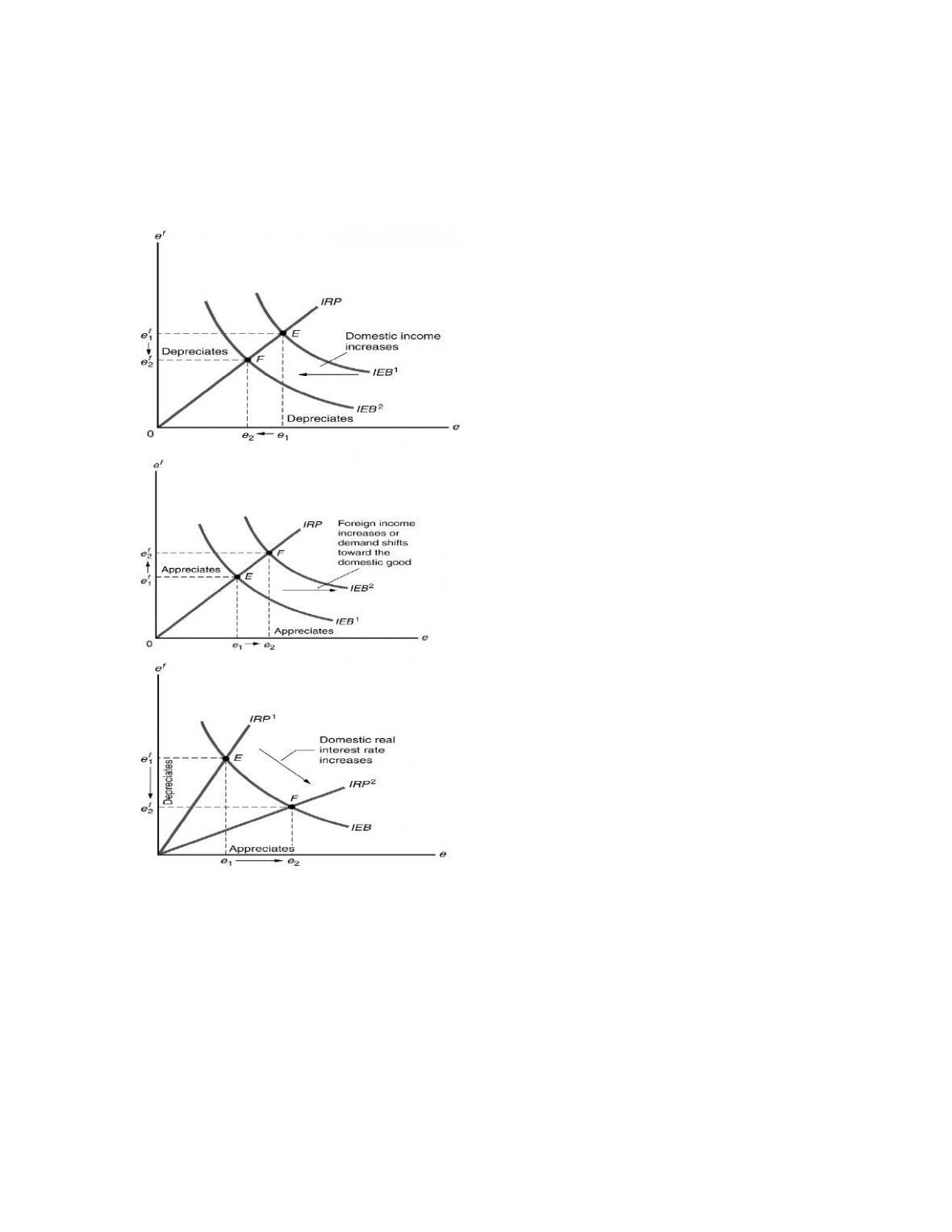

Foreign Income The effect of an increase in foreign income on the IEB curve is just the opposite of the

effect of an increase in domestic income. Suppose that before the increase in foreign income the current and

future real exchange rates are represented by point E on IEB1 in Figure 13.18. Because foreign consumers are

made wealthier by the increase in income, they will buy more of the goods produced by the home country

in the current period and in the future, which increases net exports by the home country in both periods. An

appreciation of the current real exchange rate, represented by the movement to point F, will reduce the net

exports of the home country and restore external balance. Alternatively, an appreciation of the future real

exchange rate, represented by the movement to point H, would restore external balance. Therefore the new

IEB curve, IEB2, which passes through points F and H, lies above the original IEB curve, IEB1.

Figure 13.18

Shifts in Demand A shift in demand away from foreign goods toward goods produced by the home

country shifts the IEB curve upward, just as an increase in foreign income does. The reason is that, like an

increase in foreign income, a shift in demand toward domestic goods increases both current and future net

exports by the home country. For external balance to be restored, the current real exchange rate or the

future real exchange rate must appreciate; so the IEB curve shifts upward.

1.94 euros per dollar (1.94 is 97% of 2.00). Converting $10,000 to euros at an exchange rate of 2 euros

per dollar yields 20,000 euros (step 1 in Table 13.2), which are used to buy a German bond. At a 6%

nominal interest rate the German bond earns 1200 euros interest and is worth 21,200 euros at the end

of one year (step 2). Finally, converting 21,200 euros to dollars at 1.94 euros per dollar yields $10,928

(step 3)—which is higher than the $10,800 that would be obtained from investing in a U.S. bond! Thus

1 unit of enom units of

home currency foreign currency

(1 iFor)enom units of foreign

currency [(1 iFor)enom]/

nom

f

e

units

of home currency

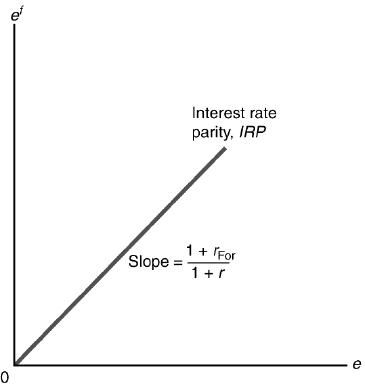

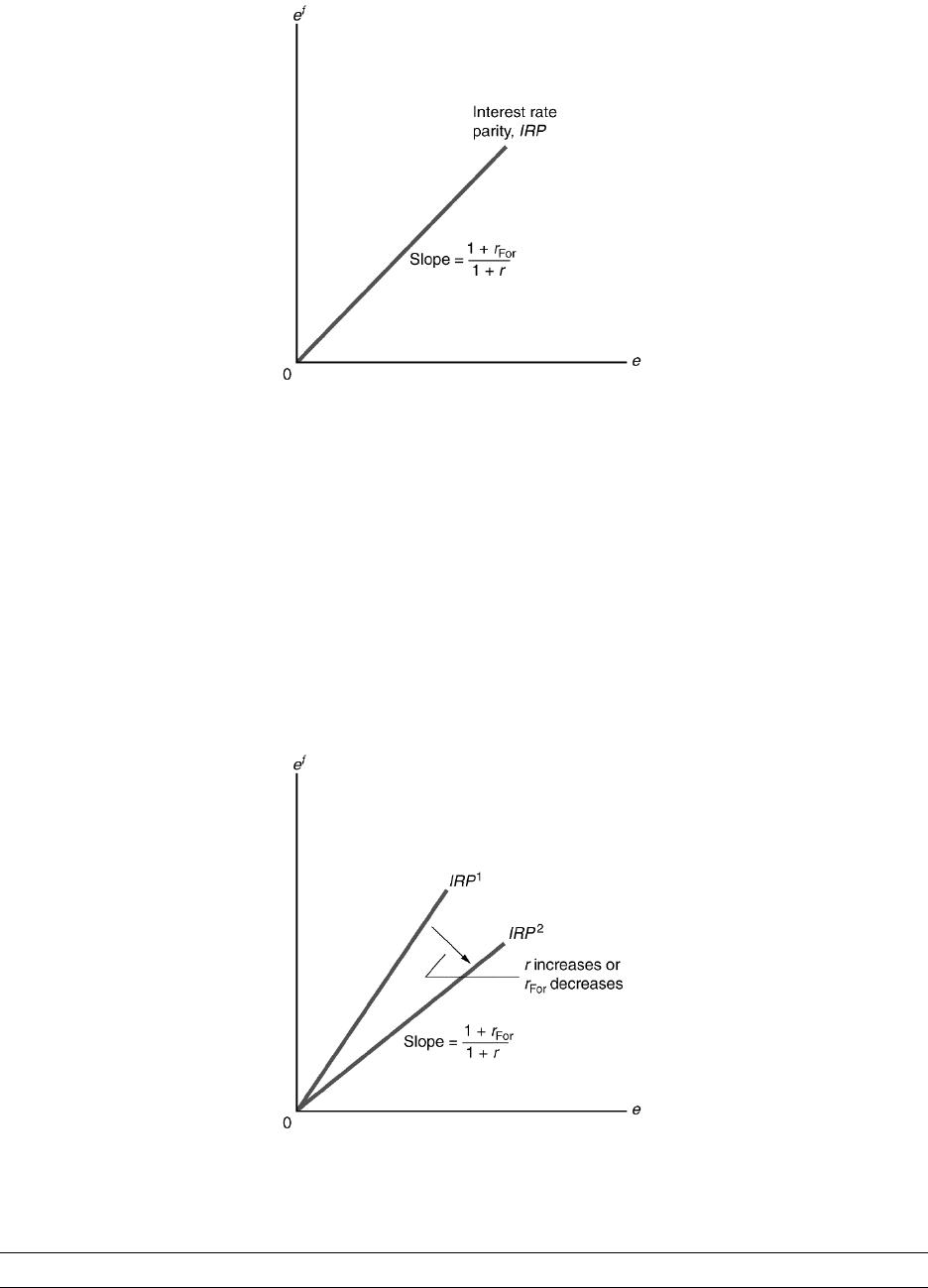

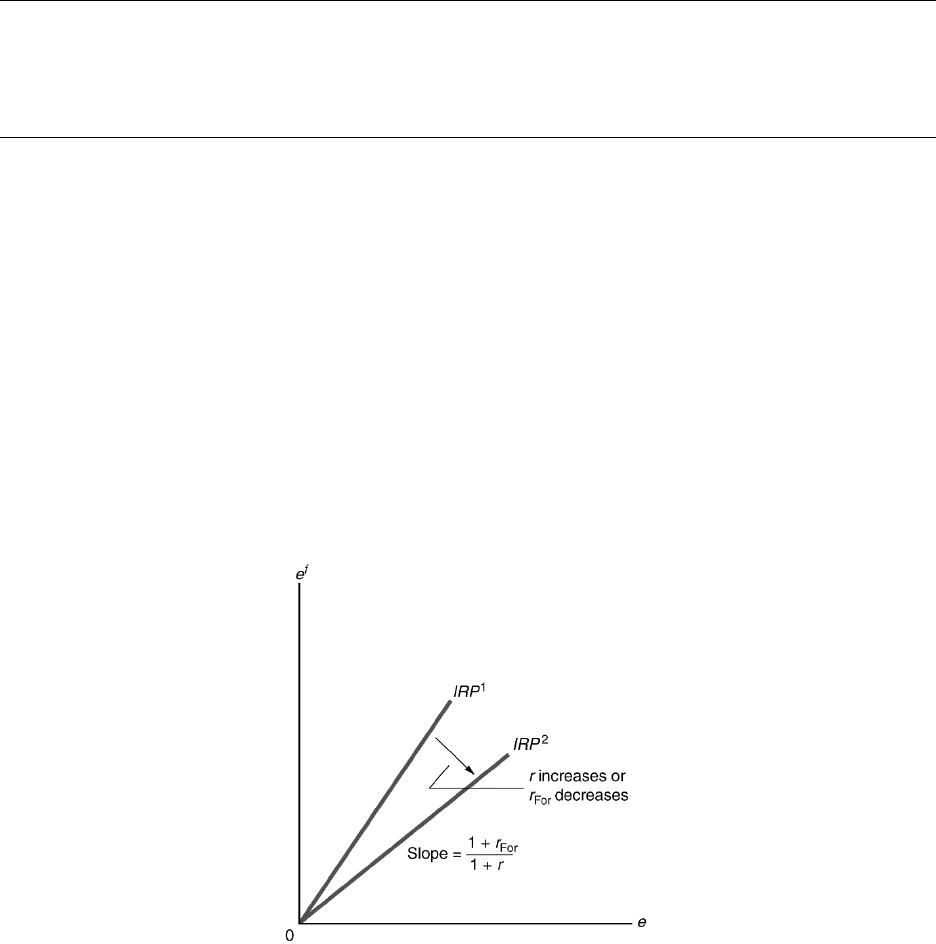

Interest Rate Parity

In our example the gross nominal rate of return expected on the German government bond exceeded the

gross nominal rate of return on the U.S. government bond. However, if both types of government bonds

have the same risk and liquidity, this difference in rates of return would not persist for long. If savers are

free to choose between German bonds and U.S. bonds, they will choose the German bonds as long as they

offer a higher gross nominal rate of return than U.S. bonds. But if investors choose German bonds in

preference to U.S. bonds, the rate of return on German bonds will fall and the rate of return on U.S. bonds

will increase until the two rates of return are equal.

In general, when the international asset market is in equilibrium, the gross nominal rates of return to

domestic and foreign assets of comparable risk and liquidity must be the same. This equilibrium

condition can be written as

nom nom

( / )

f

e e

(1 iFor) 1 i, (13.9)

where the left side is the gross nominal rate of return on the foreign bond (Eq. 13.7) and the right side is

the gross nominal rate of return on the domestic bond. The equilibrium condition in Eq. (13.9) is the

nominal interest rate parity condition, which says that the nominal returns on foreign and domestic

financial investments with equal risk and liquidity, when measured in a common currency, must be the

same. [With the approximation in Eq. (13.8) the nominal interest rate parity condition can also be

expressed more simply as iFor enom/enom i. According to this approximate formula for interest rate

parity, the difference between nominal interest rates in two countries equals the rate at which the currency

of the country with the higher nominal interest rate is expected to depreciate.]

Interest rate parity can also be expressed in terms of real interest rates and real exchange rates as the real

interest rate parity condition:

(e/ef)(1 rFor) 1 r, (13.10)

where rFor is the foreign real interest rate, r is the domestic real interest rate, and e and ef are the current

and future real exchange rates. The real interest rate parity condition, Eq. (13.10), is identical to the

nominal interest parity condition, Eq. (13.9), except that the nominal interest and exchange rates in

1.94 euros per dollar (1.94 is 97% of 2.00). Converting $10,000 to euros at an exchange rate of 2 euros

per dollar yields 20,000 euros (step 1 in Table 13.2), which are used to buy a German bond. At a 6%

nominal interest rate the German bond earns 1200 euros interest and is worth 21,200 euros at the end

of one year (step 2). Finally, converting 21,200 euros to dollars at 1.94 euros per dollar yields $10,928

(step 3)—which is higher than the $10,800 that would be obtained from investing in a U.S. bond! Thus

1 unit of enom units of

home currency foreign currency

(1 iFor)enom units of foreign

currency [(1 iFor)enom]/

nom

f

e

units

of home currency

Interest Rate Parity

In our example the gross nominal rate of return expected on the German government bond exceeded the

gross nominal rate of return on the U.S. government bond. However, if both types of government bonds

have the same risk and liquidity, this difference in rates of return would not persist for long. If savers are

free to choose between German bonds and U.S. bonds, they will choose the German bonds as long as they

offer a higher gross nominal rate of return than U.S. bonds. But if investors choose German bonds in

preference to U.S. bonds, the rate of return on German bonds will fall and the rate of return on U.S. bonds

will increase until the two rates of return are equal.

In general, when the international asset market is in equilibrium, the gross nominal rates of return to

domestic and foreign assets of comparable risk and liquidity must be the same. This equilibrium

condition can be written as

nom nom

( / )

f

e e

(1 iFor) 1 i, (13.9)

where the left side is the gross nominal rate of return on the foreign bond (Eq. 13.7) and the right side is

the gross nominal rate of return on the domestic bond. The equilibrium condition in Eq. (13.9) is the

nominal interest rate parity condition, which says that the nominal returns on foreign and domestic

financial investments with equal risk and liquidity, when measured in a common currency, must be the

same. [With the approximation in Eq. (13.8) the nominal interest rate parity condition can also be

expressed more simply as iFor enom/enom i. According to this approximate formula for interest rate

parity, the difference between nominal interest rates in two countries equals the rate at which the currency

of the country with the higher nominal interest rate is expected to depreciate.]

Interest rate parity can also be expressed in terms of real interest rates and real exchange rates as the real

interest rate parity condition:

(e/ef)(1 rFor) 1 r, (13.10)

where rFor is the foreign real interest rate, r is the domestic real interest rate, and e and ef are the current

and future real exchange rates. The real interest rate parity condition, Eq. (13.10), is identical to the

nominal interest parity condition, Eq. (13.9), except that the nominal interest and exchange rates in