Data Application

3. Why would higher future output cause people to increase money demand?

a. Firms, anticipating higher sales, would need more money for transactions to pay for

materials and workers

b. The Fed would respond to the higher demand for money by increasing money supply;

otherwise, the price level would decline

1. Friedman and Schwartz have extensively documented that often monetary changes have had

an independent origin; they weren’t just a reflection of changes or future changes in

2. More recently, Romer and Romer documented additional episodes of monetary nonneutrality

since 1960

a. One example is the Fed’s tight money policy begun in 1979 that was followed by a minor

recession in 1980 and a deeper one in 1981

3. So money does not appear to be neutral

4. There is a version of the classical model in which money isn’t neutral—the misperceptions

theory discussed next

Numerical Problems 2 and 3 examine price level effects in the classical model.

1. In the classical model, money is neutral since prices adjust quickly

a. In this case, the only relevant supply curve is the long-run aggregate supply curve

2. But if producers misperceive the aggregate price level, then the relevant aggregate supply

curve in the short run isn’t vertical

a. This happens because producers have imperfect information about the general price level

b. As a result, they misinterpret changes in the general price level as changes in relative prices

1. This makes the AS curve slope upward

2. Example: A bakery that makes bread

a. The price of bread is the baker’s nominal wage; the price of bread relative to the general

price level is the baker’s real wage

b. If the relative price of bread rises, the baker may work more and produce more bread

3. Generalizing this example, if everyone expects prices to increase 5% but they actually

increase 8%, they’ll work more

4. So an increase in the price level that is higher than expected induces people to work more

and thus increases the economy’s output

5. Similarly, an increase in the price level that is lower than expected reduces output

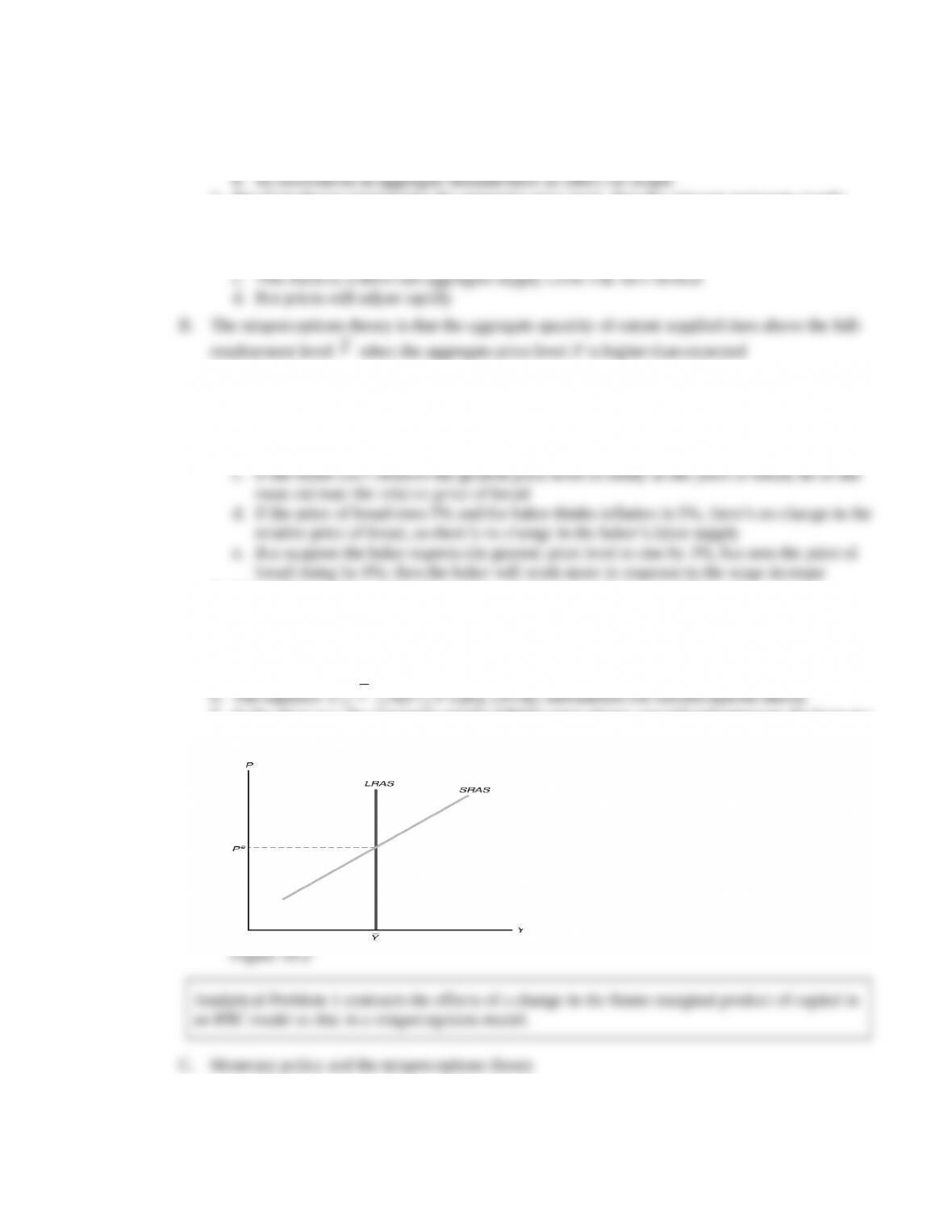

7. In the short run, the aggregate supply (SRAS) curve slopes upward and intersects the long-run

aggregate supply (LRAS) curve at P Pe (Figure 10.2; like text Figure 10.7)

1. Because of misperceptions, unanticipated monetary policy has real effects; but anticipated

monetary policy has no real effects because there are no misperceptions

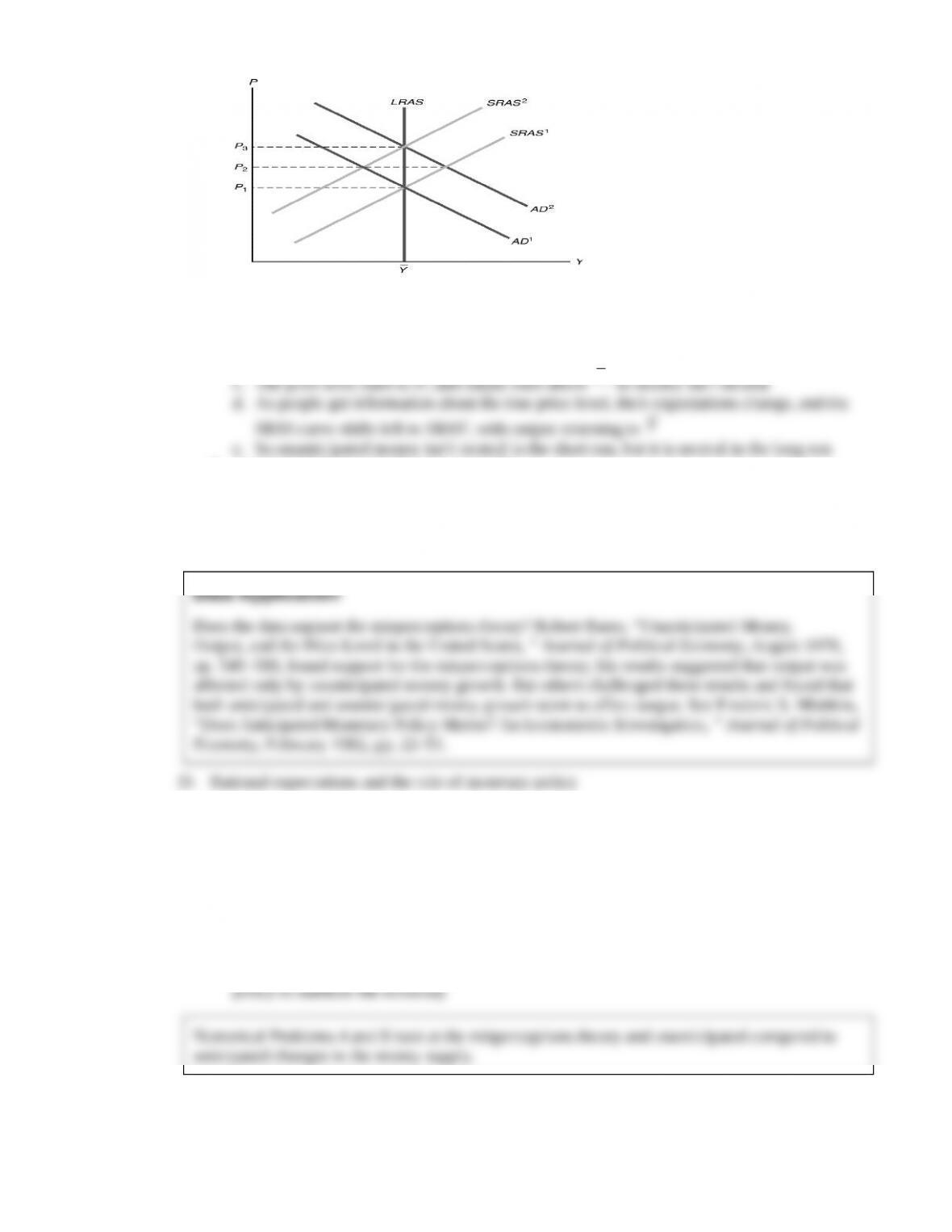

2. Unanticipated changes in the money supply (Figure 10.3; like text Figure 10.8)

Figure 10.3

a. Initial equilibrium where AD1 intersects SRAS1 and LRAS

b. Unanticipated increase in money supply shifts AD curve to AD2

,Y

3. Anticipated changes in the money supply

a. If people anticipate the change in the money supply and thus in the price level, they

aren’t fooled, there are no misperceptions, and the SRAS curve shifts immediately to its

higher level

b. So anticipated money is neutral in both the short run and the long run

1. The only way the Fed can use monetary policy to affect output is to surprise people

2. But people realize that the Fed would want to increase the money supply in recessions and

decrease it in booms, so they won’t be fooled

3. The rational expectations hypothesis suggests that the public’s forecasts of economic

variables are well reasoned and use all the available data

4. If the public has rational expectations, the Fed won’t be able to surprise people in response to

the business cycle; only random monetary policy has any effects

5. So even if smoothing the business cycle were desirable, the combination of misperceptions

theory and rational expectations suggests that the Fed can’t systematically use monetary

6. Propagating the effects of unanticipated changes in the money supply

a. It doesn’t seem like people could be fooled for long, since money supply figures are

reported weekly and inflation is reported monthly

b. Classical economists argue that propagation mechanisms allow short-lived shocks to have

long-lived effects

1. Economists can test whether price forecasts are rational by looking at surveys of people’s

expectations

2. The forecast error of a forecast is the difference between the actual value of the variable and

the forecast value

3. If people have rational expectations, forecast errors should be unpredictable random

numbers; otherwise, people would be making systematic errors and thus not have rational

expectations

Data Application

If you examine a survey of forecasters, like the Livingston Survey, you’ll see that the forecasters

4. Many statistical studies suggest that people don’t have rational expectations

5. But people who answer surveys may not have a lot at stake in making forecasts, so couldn’t

be expected to produce rational forecasts

6. Instead, professional forecasters are more likely to produce rational forecasts

7. Keane and Runkle, using a survey of professional forecasters, find evidence that these

forecasters do have rational expectations

8. Croushore used inflation forecasts made by the general public, as well as economists, and

found evidence broadly consistent with rational expectations, though expectations tend to lag

reality when inflation changes sharply

Data Application

1. In the classical model, money is neutral since prices adjust quickly

a. In this case, the only relevant supply curve is the long-run aggregate supply curve

2. But if producers misperceive the aggregate price level, then the relevant aggregate supply

curve in the short run isn’t vertical

a. This happens because producers have imperfect information about the general price level

b. As a result, they misinterpret changes in the general price level as changes in relative prices

1. This makes the AS curve slope upward

2. Example: A bakery that makes bread

a. The price of bread is the baker’s nominal wage; the price of bread relative to the general

price level is the baker’s real wage

b. If the relative price of bread rises, the baker may work more and produce more bread

3. Generalizing this example, if everyone expects prices to increase 5% but they actually

increase 8%, they’ll work more

4. So an increase in the price level that is higher than expected induces people to work more

and thus increases the economy’s output

5. Similarly, an increase in the price level that is lower than expected reduces output

7. In the short run, the aggregate supply (SRAS) curve slopes upward and intersects the long-run

aggregate supply (LRAS) curve at P Pe (Figure 10.2; like text Figure 10.7)

1. Because of misperceptions, unanticipated monetary policy has real effects; but anticipated

monetary policy has no real effects because there are no misperceptions

2. Unanticipated changes in the money supply (Figure 10.3; like text Figure 10.8)

Figure 10.3

a. Initial equilibrium where AD1 intersects SRAS1 and LRAS

b. Unanticipated increase in money supply shifts AD curve to AD2

,Y

3. Anticipated changes in the money supply

a. If people anticipate the change in the money supply and thus in the price level, they

aren’t fooled, there are no misperceptions, and the SRAS curve shifts immediately to its

higher level

b. So anticipated money is neutral in both the short run and the long run

1. The only way the Fed can use monetary policy to affect output is to surprise people

2. But people realize that the Fed would want to increase the money supply in recessions and

decrease it in booms, so they won’t be fooled

3. The rational expectations hypothesis suggests that the public’s forecasts of economic

variables are well reasoned and use all the available data

4. If the public has rational expectations, the Fed won’t be able to surprise people in response to

the business cycle; only random monetary policy has any effects

5. So even if smoothing the business cycle were desirable, the combination of misperceptions

theory and rational expectations suggests that the Fed can’t systematically use monetary

6. Propagating the effects of unanticipated changes in the money supply

a. It doesn’t seem like people could be fooled for long, since money supply figures are

reported weekly and inflation is reported monthly

b. Classical economists argue that propagation mechanisms allow short-lived shocks to have

long-lived effects

1. Economists can test whether price forecasts are rational by looking at surveys of people’s

expectations

2. The forecast error of a forecast is the difference between the actual value of the variable and

the forecast value

3. If people have rational expectations, forecast errors should be unpredictable random

numbers; otherwise, people would be making systematic errors and thus not have rational

expectations

Data Application

If you examine a survey of forecasters, like the Livingston Survey, you’ll see that the forecasters

4. Many statistical studies suggest that people don’t have rational expectations

5. But people who answer surveys may not have a lot at stake in making forecasts, so couldn’t

be expected to produce rational forecasts

6. Instead, professional forecasters are more likely to produce rational forecasts

7. Keane and Runkle, using a survey of professional forecasters, find evidence that these

forecasters do have rational expectations

8. Croushore used inflation forecasts made by the general public, as well as economists, and

found evidence broadly consistent with rational expectations, though expectations tend to lag

reality when inflation changes sharply

Data Application