CHAPTER 17

DESIGN FOR AFFORDABILITY

(LIFE – CYCLE COSTING)

1) Life–cycle cost (LCC) includes the total cost of a system over its entire life cycle. LCC

includes all of the costs associated with the activities identified in Figure 17.1 (page 568),

including the visible and the not so visible as in Figure 17.2 (page 569). When performing a

LCC analysis, all “future” research and development costs, production and/or construction

costs, operation and maintenance and support costs, retirement and material

recycling/disposal costs are to be identified and considered in the evaluation process. “Past”

(or “sunk”) costs—while providing a good historical view—are not to be considered. Sunk

costs have no place in an analysis as they will have no effect on decisions in the future.

Reference: Section 17.1 (page 567).

© 2011 Pearson Education, Inc., Upper Saddle River, NJ. All rights reserved.

This material is protected by Copyright and written permission should be obtained from the publisher prior to any prohibited

reproduction, storage in a retrieval system, or transmission in any form or by any means, electronic, mechanical, photocopying,

recording, or likewise. For information regarding permission(s), write to:

Rights and Permissions Department, Pearson Education, Inc., Upper Saddle River, NJ 07458.

133

12) Refer to the answer for Problem 8 addressing parametric cost estimating. These

relationships may be developed from data derived from similar systems in the past, wherein

costs can be related to the physical and functional parameters of the systems. Each life–

cycle cost profile shown in Figure 17.13 (page 591) is a “signature” of sort for a particular

type of system and may be used to estimate the cost profile for a similar system. Figure 17.9

(page 581) indicates that parametric cost estimating will be applicable mostly during the

early phase of the life cycles (left portions) shown in Figure 17.13, whereas the other

estimating methods will be applicable later on.

13) Refer to Section 16.3.2 (page 549) and Figure 16.3 (page 551). Learning curves can be

applied to estimating costs for any activity which is repetitious in nature; e.g., the

production of a multiple quantity of products where learning takes place as manufacturing

progresses. In general, learning curves are applied to show a savings in time and cost as

multiple quantities of an item are produced. However, there are instances when a multiple

quantity of items are produced and where the cost of the second is higher than the cost of

the first, the cost of the fourth is higher than the cost of the second, etc. In this situation,

there is a failure to achieve the assumed learning curve savings on which manufacturing

costs estimates were originally based. This can occur when there are numerous design

changes initiated during initial production, when there are changes in management structure

and/or lower–level personnel, and/or when there are numerous changes in procedures.

14) In performing a life–cycle cost analysis, it may be appropriate to first develop a profile

(such as shown conceptually in Figure 7.1 on page 177, or in Figure 17.11 on page 588) in

“constant” units; e.g. in current-year dollars for each year in the life cycle (without

including inflation or making other adjustments). As “cause–and–effect” is analyzed from

year to year, it is often easier to proceed if given a known baseline for comparative

purposes. Then, a second profile should be developed in order to show 2014 dollars in 2014,

2015 dollars in 2015, 2016 dollars in the year 2016, and so on. This “inflated” profile will

include inflationary effects, the effects of learning, projected cost growth from year to year,

and so on. This is similar to a normal “cost–to–complete” exercise for a typical project,

except that the objective is to project all life–cycle costs. The third profile is one where all

future costs are related back to the “present time,” or the common point in time when

decisions are being made (i.e., present equivalent, annual equivalent, or future equivalent).

In the evaluation of alternatives, one must compare the profiles for each on an equivalent

basis to incorporate the “time value of money” as developed in Chapter 8 (page 204).

15) An advantage in presenting the costs in a format similar to what is shown in Figure 17.10 on

page 586 is to be able to relate the costs back to a specific function (or block) in the cost

breakdown structure (CBS), and to be able to quickly determine the “high–cost

contributors.” In some cases, particularly when attempting to implement a continuous

product/process improvement initiative for cost reduction purposes, the presentation of

costs in terms of “percent of total” is often more meaningful than worrying about the

specific “bottom–line” value. Simply pick the highest, then the next highest, etc., initiating

136

16) The goal is to find out how sensitive the results of an LCC analysis are in terms of the input

factors and the underlying assumptions that have been made. On occasion, the input data

may be highly “suspect” (not based on good assumptions or good historical information);

yet, the results of the analysis (and the decision to be made) may be heavily dependent on

126

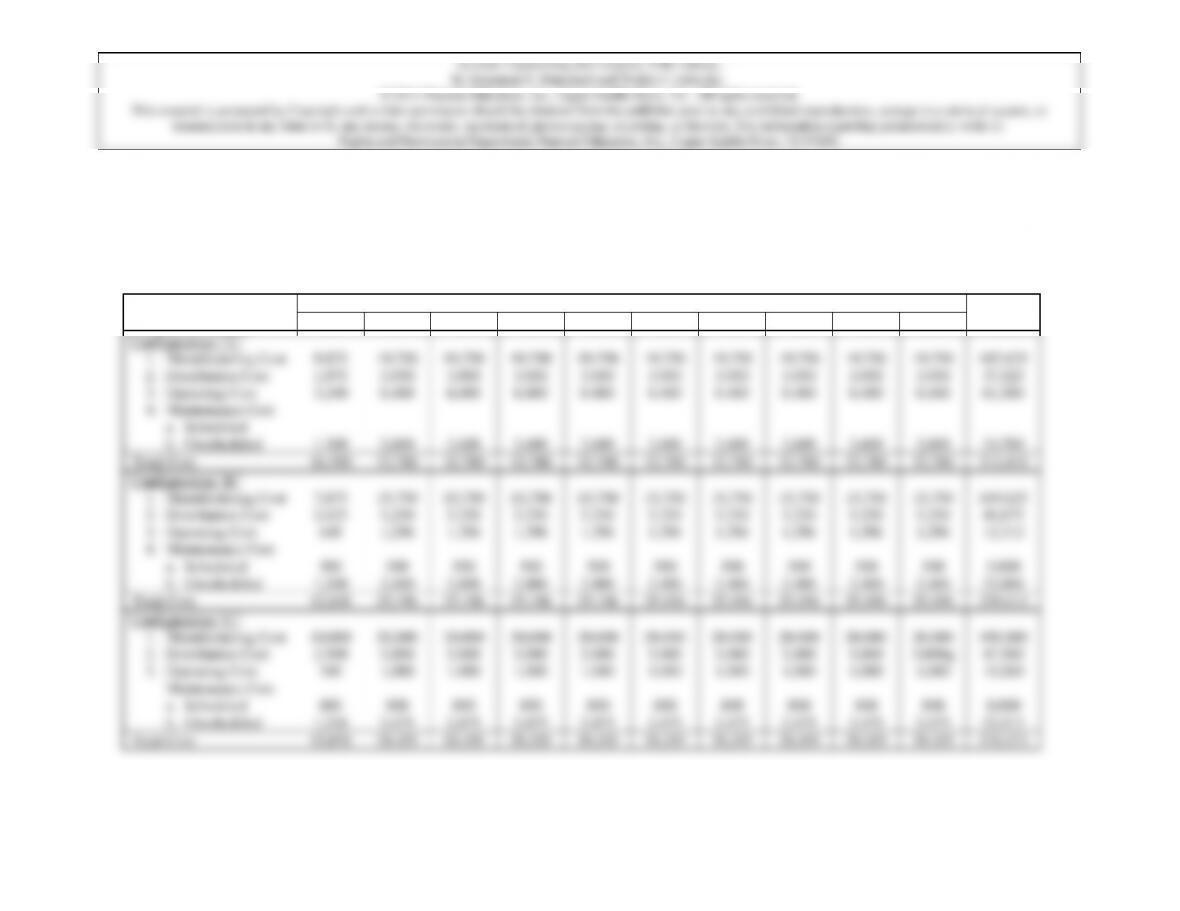

21) Table 1 exhibits the information given in this problem over a 10-year evaluation horizon.

Problem 21 – Table 1. BAF Corporation costs by program year.

Cost by Program Year ($)

Total

Evaluation Category

1

2

3

4

5

6

7

8

9

10

Cost ($)

Configuration “A”

1. Manufacturing Cost

9,875

19,750

19,750

19,750

19,750

19,750

19,750

19,750

19,750

19,750

187,625

2. Distribution Cost

1,975

3,950

3,950

3,950

3,950

3,950

3,950

3,950

3,950

3,950

37,525

3. Operating Cost

3,240

6,480

6,480

6,480

6,480

6,480

6,480

6,480

6,480

6,480

61,560

4. Maintenance Cost

a. Scheduled

b. Unscheduled

1,300

2,600

2,600

2,600

2,600

2,600

2,600

2,600

2,600

2,600

24,700

Total Cost

16,390

32,780

32,780

32,780

32,780

32,780

32,780

32,780

32,780

32,780

311,410

Configuration “B”

1. Manufacturing Cost

7,875

15,750

15,750

15,750

15,750

15,750

15,750

15,750

15,750

15,750

149,625

2. Distribution Cost

2,625

5,250

5,250

5,250

5,250

5,250

5,250

5,250

5,250

5,250

49,875

3. Operating Cost

648

1,296

1,296

1,296

1,296

1,296

1,296

1,296

1,296

1,296

12,312

4. Maintenance Cost

a. Scheduled

500

500

500

500

500

500

500

500

500

500

5,000

b. Unscheduled

1,200

2,400

2,400

2,400

2,400

2,400

2,400

2,400

2,400

2,400

22,800

Total Cost

12,848

25,196

25,196

25,196

25,196

25,196

25,196

25,196

25,196

25,196

239,612

Configuration “C”

1. Manufacturing Cost

10,000

20,000

20,000

20,000

20,000

20,000

20,000

20,000

20,000

20,000

190,000

2. Distribution Cost

2,500

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000q

47,500

3. Operating Cost

540

1,080

1,080

1,080

1,080

1,080

1,080

1,080

1,080

1,080

10,260

Maintenance Cost

a. Scheduled

800

800

800

800

800

800

800

800

800

800

8,000

b. Unscheduled

1,238

2,475

2,475

2,475

2,475

2,475

2,475

2,475

2,475

2,475

23,513

Total Cost

15,078

29,355

29,355

29,355

29,355

29,355

29,355

29,355

29,355

29,355

279,273

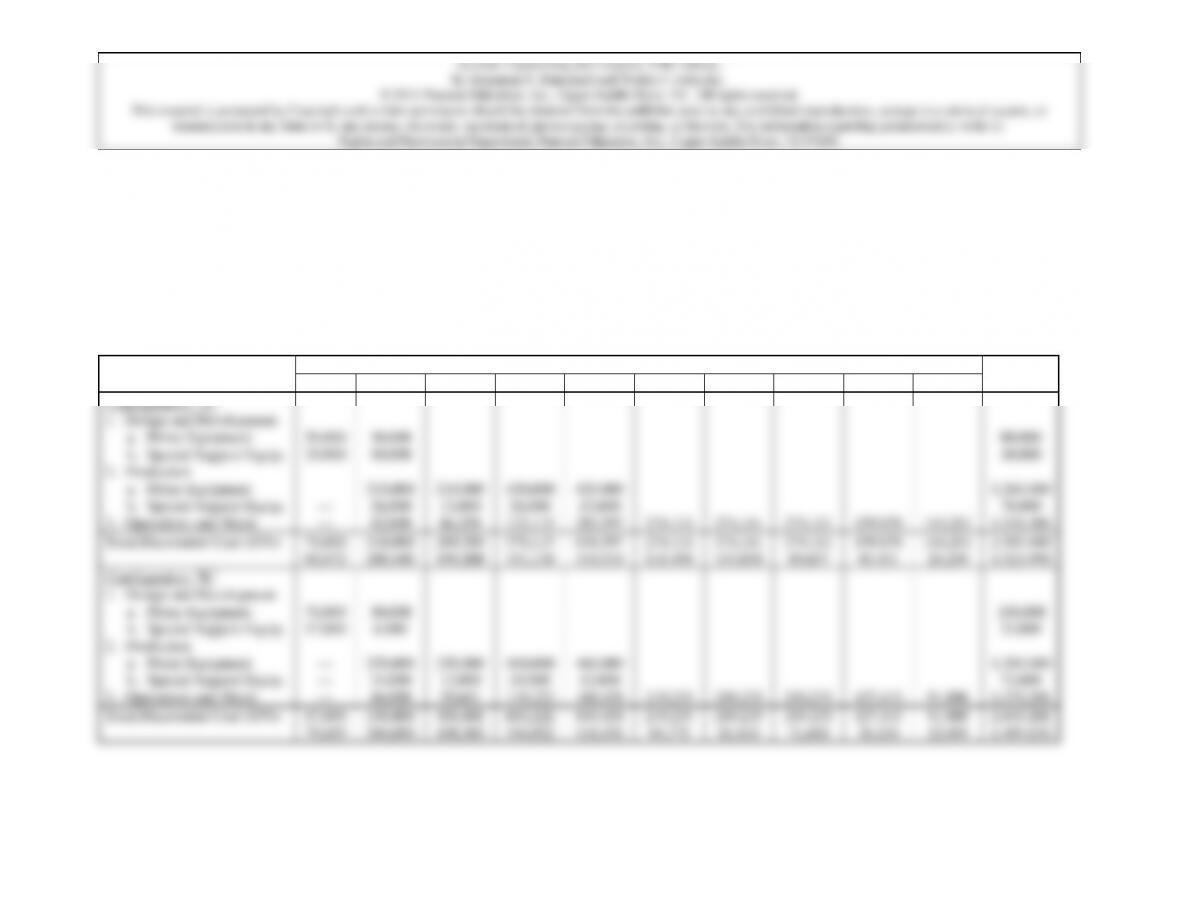

Problem 21 – Table 2. Evaluation of alternative configurations for the BAF Corporation.

4

0.6830

53,957

22,389

72,715

17,209

68,300

20,049

5

0.6209

49,051

20,353

65,195

15,644

62,090

18,227

6

0.5645

44,596

18,504

59,273

14,223

56,450

16,571

7

0.5132

40,543

16,823

53,886

12,931

51,320

15,065

8

0.4665

36,854

15,292

48,983

11,754

46,650

13,694

9

0.4241

33,504

13,902

44,531

10,686

42,410

12,449

10

0.3856

30,462

12,640

40,488

9,716

38,560

11,319

Salvage

0.3505

351

—

876

—

771

—

Totals

449,875

201,524

598,845

171,597

569,786

190,397

Present equivalent value of Configuration “A” = $449,875 – $201,524 = $248,351

Present equivalent value of Configuration “B” = $598,845 – $171,597 = $427,248

Present equivalent value of Configuration “C” = $569,786 – $190,397 = $379,389

Configuration “B” is the recommended Alternative

22) (a) Assume that System XYZ is “isolated” in terms of external interaction affects; address

System XYZ as an entity.

Program

year, n

(P/F,

10%,n)

Configuration “A”

Configuration “B”

Configuration “C”

Revenues

($)

Cost ($)

Revenues

($)

Cost ($)

Revenues

($)

Cost ($)

0

1.0000

—

15,000

—

28,000

—

23,000

1

0.9091

35,910

14,900

47,228

11,680

45,455

13,707

2

0.8265

65,294

27,093

86,783

20,824

82,650

24,262

3

0.7513

59,353

24,628

78,887

18,930

75,130

22,054

6

128

129

An initial step involves developing a matrix for collecting the various costs each year in terms of their inflated values. These costs are

subdivided into: 1. Design and Development; 2. Production; and 3. Operations and Maintenance as shown in the table below.

Problem 22 – Table 1. System XYZ Life Cycle Cost Summary ($)

Life–Cycle Year

Total

Item

1

2

3

4

5

6

7

8

9

10

Cost ($)

Configuration “A”

1. Design and Development

a. Prime Equipment

50,000

30,000

80,000

b. Special Support Equip.

20,000

10,000

30,000

2. Production

a. Prime Equipment

—

210,000

210,000

420,000

420,000

1,260,000

b. Special Support Equip.

—

26,000

13,000

26,000

13,000

78,000

3. Operations and Maint.

—

42,000

66,290

133,115

203,597

274,111

274,111

274,111

159,870

114,201

1,541,406

Total Discounted Cost (15%)

70,000

60,872

318,000

240,440

289,290

190,208

579,115

331,138

636,597

316,516

274,111

118,498

274,111

103,038

274,111

89,607

159,870

45,451

114,201

28,230

2,989,406

1,523,998

Configuration “B”

1. Design and Development

a. Prime Equipment

70,000

30,000

100,000

b. Special Support Equip.

17,000

6,000

23,000

2. Production

a. Prime Equipment

—

230,000

230,000

460,000

460,000

1,380,000

b. Special Support Equip.

—

24,000

12,000

24,000

12,000

72,000

3. Operations and Maint.

—

46,000

59,601

119,222

168,458

219,235

219,235

219,235

127,415

91,800

1,270,201

Total Discounted Cost (15%)

87,000

75,655

336,000

244,050

301,601

198,303

603,222

344,922

640,458

318,436

219,235

94,775

219,235

82,410

219,235

71,668

127,415

36,224

91,800

22,693

2,845,201

1,499,136

130

Problem 22 – Table 2. Production Costs

Year

Item

2

3

4

5

Total

Configuration “A”

(10 Systems)

(10 Systems)

(20 Systems)

(20 Systems)

(60 Systems)

System XYZ

$210,000

$210,000

$420,000

$420,000

$1,260,000

Support Equipment

26,000

13,000

26,000

13,000

78,000

Total

$236,000

$223,000

$446,000

$433,000

$1,338,000

Configuration “B”

(10 Systems)

(10 Systems)

(20 Systems)

(20 Systems)

(60 Systems)

System XYZ

$230,000

$230,000

$460,000

$460,000

$1,380,000

Support Equipment

24,000

12,000

24,000

12,000

72,000

Total

$254,000

$242,000

$484,000

$472,000

$1,452,000

3. Operations and Maintenance Costs

Problem 22 – Table 3. System Operating Hours

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

0

0

14,600

29,200

58,400

87,600

87,600

87,600

51,100

36,500

Rights and Permissions Department, Pearson Education, Inc., Upper Saddle River, NJ 07458.

131

Problem 22 – Table 4. Corrective Maintenance Actions

Year

Configuration

1

2

3

4

5

6

7

8

9

10

Total

Configuration “A”

Unit “A”

0

0

18

37

73

110

110

110

64

46

568

Unit “B”

0

0

29

58

117

175

175

175

102

73

904

Unit “C”

0

0

7

14

29

44

44

44

26

18

226

Total

0

0

54

109

219

329

329

329

192

137

1,698

Configuration “B”

Unit “A”

0

0

18

37

73

110

110

110

64

46

568

Unit “B”

0

0

15

29

58

88

88

88

51

37

454

Unit “C”

0

0

6

12

23

35

35

35

20

15

181

Total

0

0

39

78

154

233

233

233

135

98

1,203

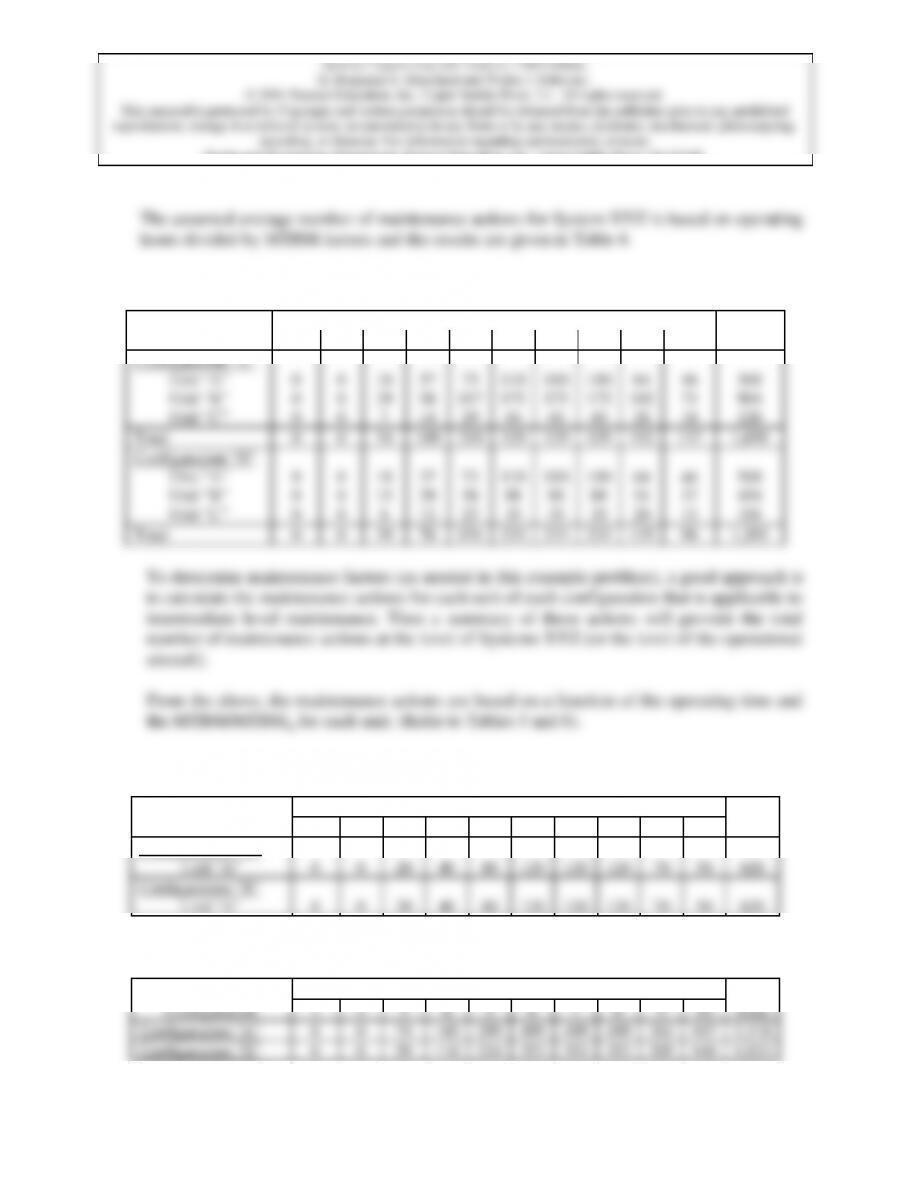

To determine maintenance factors (as needed in this example problem), a good approach is

to calculate the maintenance actions for each unit of each configuration that is applicable to

intermediate level maintenance. Then a summary of these actions will provide the total

number of maintenance actions at the level of Systems XYZ (or the level of the operational

aircraft).

From the above, the maintenance actions are based on a function of the operating time and

the MTBM/MTBMs for each unit. (Refer to Tables 5 and 6).

Problem 22 – Table 5. Preventive Maintenance Actions

Year

Configuration

1

2

3

4

5

6

7

8

9

10

Total

Configuration “A”

Unit “A”

0

0

20

40

80

120

120

120

70

50

620

Configuration “B”

Unit “A”

0

0

20

40

80

120

120

120

70

50

620

Problem 22 – Table 6. Total Maintenance Actions (Systems Level)

Year

Configuration

1

2

3

4

5

6

7

8

9

10

Total

Configuration “A”

0

0

74

149

299

499

499

499

262

187

2,318

Configuration “B”

0

0

59

118

234

353

353

353

205

148

1,823