1. a. Since it takes considerable investment to develop uranium mines, you would want a larger

b. A permanent increase in the world price of copper would cause a short-term current account deficit

c. A temporary increase in the world price of copper would cause a current account surplus. You

d. A temporary rise in the world price of oil would cause a current account deficit if you were an

2. Because the marginal propensity to consume out of income is less than 1, a transfer of income from

B to A increases savings in A and decreases savings in B. Therefore, A has a current account surplus

3. Changes in parities reflected both initial misalignments and balance of payments crises. Attempts to

return to the parities of the prewar period after the war ignored the changes in underlying economic

4. A monetary contraction, under the gold standard, will lead to an increase in the gold holdings of the

contracting country’s central bank if other countries do not pursue a similar policy. All countries cannot

succeed in doing this simultaneously since the total stock of gold reserves is fixed in the short run.

5. The increase in domestic prices makes home exports less attractive and causes a current account

6. An increase in the world interest rate leads to a fall in a central bank’s holdings of foreign reserves as

domestic residents trade in their cash for foreign bonds. This leads to a decline in the home country’s

fail unless bonds are imperfect substitutes. 7. Capital account restrictions insulate the

8. An inflow attack is different from capital flight, but many parallels exist. In an “outflow” attack,

speculators sell the home currency and drain the central bank of its foreign assets. The central bank

could always defend if it so chooses (they can raise interest rates to improbably high levels), but if it

is unwilling to cripple the economy with tight monetary policy, it must relent. An “inflow” attack is

9. a. We know that China has a very large current-account surplus, placing them high above

the XX line. They also have moderate inflationary pressures (described as “gathering” in the

b. China needs to appreciate the exchange rate to move down on the graph toward the balance.

c. China would need to expand government spending to move to the right and hit the overall balance

10. The increase in foreign prices will shift the DD curve out to the right as demand for home products

increases (exports rise, imports fall). If the expected exchange rate also falls, then there will be a

11. An increase in the foreign inflation rate should lead to a short-run appreciation of the domestic

currency as consumers shift their consumption toward relatively cheaper domestic goods. The

appreciation of the domestic currency will mitigate the effects of foreign inflation by reducing the

price of imported goods. Thus, the flexible exchange rate does a better job of insulating the economy

12. An increase in the risk premium on domestic assets will shift the AA curve to the right, reflecting

the fact that asset market equilibrium is now attained at a higher exchange rate (depreciated domestic

currency). With floating exchange rates, the depreciated currency will stimulate export demand,

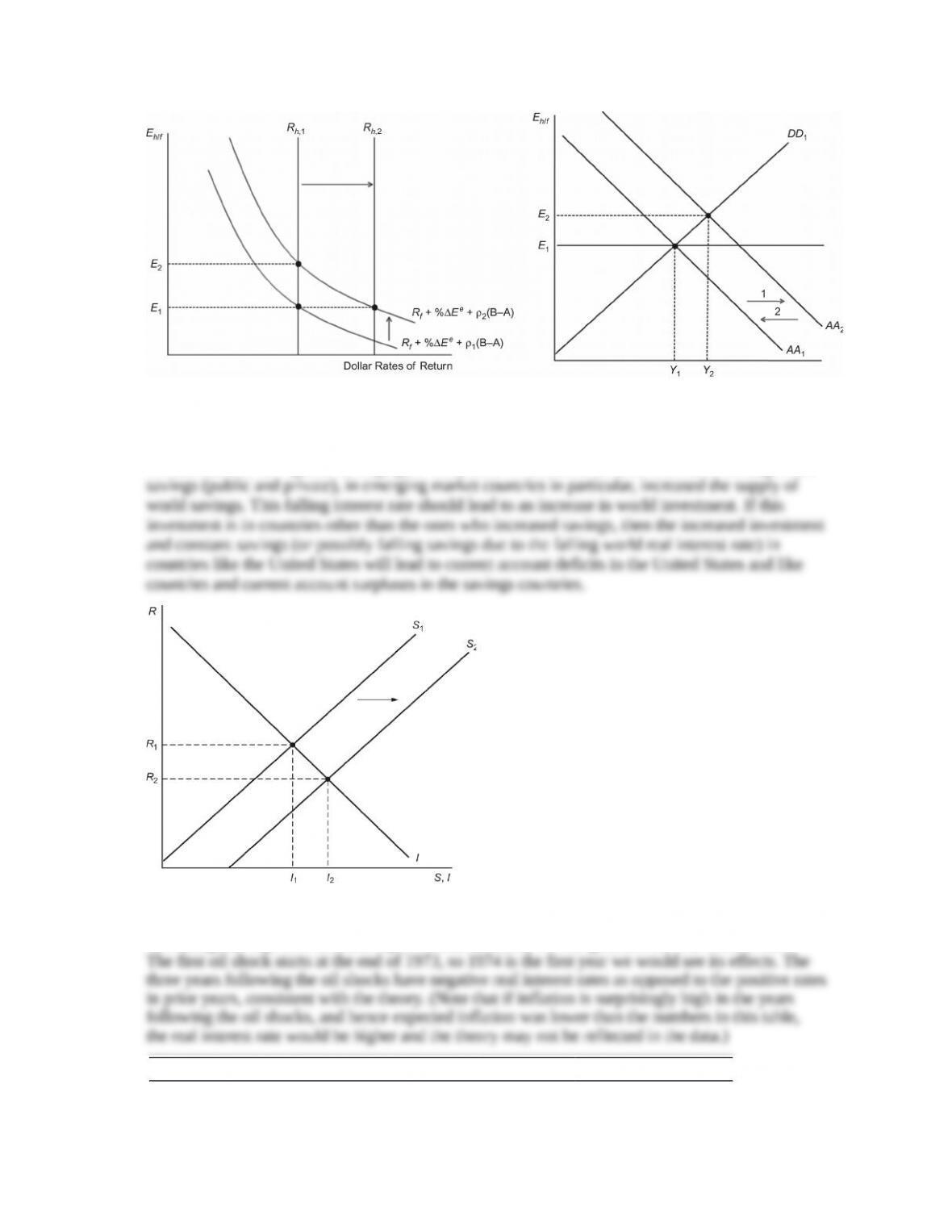

13. The simple model of savings and investment against the real interest rate can be drawn as

follows below. The increase in world savings can be shown as a rightward shift in the savings

schedule.

The result is that the world real interest rate falls and the amount of savings and investment rises.

We can think of the “global savings glut” story here. World interest rates went down as large-scale

14. The table below shows U.S. money market interest rates and inflation rates from 1970 to 1976.

You can find these data in the IMF’s International Financial Statistics, available in most libraries.

Assuming that expected inflation equals actual inflation, we can generate the real interest rates.

Year Nominal Interest Rate Inflation Real Interest Rate

1970 7.2% 5.9% 1.3%

15. If other central banks sell dollars for euros, then it is equivalent to a sterilized sale of dollars because

neither the United States nor any other central bank’s asset side of the balance sheet has changed.

Thus, the money supply is unchanged everywhere. On the other hand, there is a larger supply of