Chapter 19 International Monetary Systems: An Historical Overview 107

Overview of Section IV:

International Macroeconomic Policy

Section IV of the text consists of four chapters:

Chapter 19 International Monetary Systems: An Historical Overview

Chapter 20 Optimum Currency Areas and the European Experience

Chapter 21 Financial Globalization: Opportunity and Crisis

Chapter 22 Developing Countries: Growth, Crisis, and Reform

.1 nSection IV Overview

This final section of the book, which discusses international macroeconomic policy, provides historical

and institutional background to complement the theoretical presentation of the previous section. These

chapters also provide an opportunity for students to hone their analytic skills and intuition by applying and

extending the models learned in Section III to a range of current and historical issues.

The first two chapters of this section discuss various international monetary arrangements. These chapters

describe the workings of different exchange rate systems through the central theme of internal and external

balance. The model developed in the previous section provides a general framework for analysis of gold

standard, reserve currency, managed floating, and floating exchange-rate systems.

Chapter 19 chronicles the evolution of the international monetary system from the gold standard of

1870–1914, through the interwar years, and up to and including the postwar Bretton Woods period. These

historical episodes are put into the context of the international economics trilemma, the observation that

you can simultaneously achieve two, but never three of the following policy goals: exchange rate stability,

independent monetary policy, and open capital markets.

The chapter discusses the price-specie-flow mechanism of adjustment in the context of the discussion

of the gold standard. Conditions for internal and external balance are presented through diagrammatic

analysis based upon the short-run macroeconomic model of Chapter 17. This analysis illustrates the

strengths and weaknesses of alternative fixed exchange rate arrangements. The chapter also draws upon

earlier discussions of balance of payments crises to make clear the interplay between “fundamental

disequilibrium” and speculative attacks. There is a detailed analysis of the Bretton Woods system that

includes a case study of the experience during its decline beginning in the mid-1960s and culminating

with its collapse in 1973.

Europe’s switch to a single currency, the euro, is the subject of Chapter 20, and provides a particular example

of a single currency system. The chapter discusses the history of the European Monetary System and its

precursors. The early years of the E.M.S. were marked by capital controls and frequent realignments.

By the end of the 1980s, however, there was marked inflation convergence among E.M.S. members,

few realignments and the removal of capital controls. Despite a speculative crisis in 1992–1993, leaders

pressed on with plans for the establishment of a single European currency as outlined in the Maastricht

Treaty which created the Economic and Monetary Union (EMU). The single currency was viewed as an

important part of the EC 1992 initiative which called for the free flow within Europe of labor, capital,

goods, and services. The single currency, the euro, was launched on January 1, 1999 with 11 original

participants. These countries have ceded monetary authority to a supranational central bank and constrained

their fiscal policy with agreements on convergence criteria and the stability and growth pact. A single

currency imposes costs as well as confers benefits. The theory of optimum currency areas suggests

conditions which affect the relative benefits of a single currency. The chapter provides a way to frame

this analysis using the GG-LL diagram which compares the gains and losses from a single currency.

Finally, the chapter examines the prospects of the EU as an optimal currency area compared to the

United States and considers the future challenges EMU will face.

The international capital market is the subject of Chapter 21. This chapter draws an analogy between the

gains from trade arising from international portfolio diversification and international goods trade. There

is discussion of institutional structures that have arisen to exploit these gains. The chapter discusses

the Eurocurrency market, the regulation of offshore banking, and the role of international financial

supervisory cooperation. The chapter examines policy issues of financial markets, the policy trilemma of

the incompatibility of fixed rates, independent monetary policy, and capital mobility as well as the tension

between supporting financial stability and creating a moral hazard when a government intervenes in

financial markets. The chapter also considers evidence of how well the international capital market has

performed by focusing on issues such as the efficiency of the foreign exchange market and the existence

of excess volatility of exchange rates. The chapter also includes a thorough discussion of how increased

capital mobility and the difficulty of regulating international banking contributed to the 2007–2009

financial crisis.

Chapter 22 discusses issues facing developing countries. The chapter begins by identifying characteristics

of the economies of developing countries, characteristics that include undeveloped financial markets,

pervasive government involvement, and a dependence on commodity exports. The macroeconomic

analysis of previous chapters again provides a framework for analyzing relevant issues, such as inflation

in or capital flows to developing countries. Borrowing by developing countries is discussed as an attempt

to exploit gains from intertemporal trade and is put in historical perspective. Latin American countries’

problems with inflation and subsequent attempts at reform are detailed. Finally, the East Asian economic

miracle is revisited (it is discussed in Chapter 10), and the East Asian financial crisis is examined. This

final topic provides an opportunity to discuss possible reforms of the world’s financial architecture.

Chapter 19

International Monetary Systems:

An Historical Overview

.2 nChapter Organization

Macroeconomic Policy Goals in an Open Economy

Internal Balance: Full Employment and Price Level Stability

External Balance: The Optimal Level of the Current Account

Classifying Monetary Systems: The Open-Economy Trilemma

International Macroeconomic Policy under the Gold Standard, 1870–1914

Chapter 19 International Monetary Systems: An Historical Overview 109

Origins of the Gold Standard

External Balance Under the Gold Standard

The Price-Specie-Flow Mechanism

The Gold Standard “Rules of the Game”: Myth and Reality

Internal Balance Under the Gold Standard

Box: Hume versus the Mercantilists

Case Study: The Political Economy of Exchange Rate Regimes:

Conflict Over America’s Monetary Standard During the 1890s

The Interwar Years, 1918–1939

The Fleeting Return to Gold

International Economic Disintegration

Case Study: The International Gold Standard and the Great Depression

The Bretton Woods System and the International Monetary Fund

Goals and Structure of the IMF

Convertibility and the Expansion of Private Capital Flows

Speculative Capital Flows and Crises

Analyzing Policy Options for Reaching Internal and External Balance

Maintaining Internal Balance

Maintaining External Balance

Expenditure-Changing and Expenditure-Switching Policies

The External Balance Problem of the United States Under Bretton Woods

Case Study: The End of Bretton Woods, Worldwide Inflation, and the Transition to Floating Rates

The Mechanics of Imported Inflation

Assessment

The Case for Floating Exchange Rates

Monetary Policy Autonomy

Symmetry

Exchange Rates as Automatic Stabilizers

Exchange Rates and External Balance

Case Study: The First Years of Floating Rates, 1973–1990

Macroeconomic Interdependence Under a Floating Rate

Case Study: Transformation and Crisis in the World Economy

What Has Been Learned Since 1973?

Monetary Policy Autonomy

Symmetry

The Exchange Rate as an Automatic Stabilizer

External Balance

The Problem of Policy Coordination

Are Fixed Exchange Rates Even an Option for Most Countries?

Summary

APPENDIX TO CHAPTER 19: International Policy Coordination Failures

.3 nChapter Overview

This is the first of four international monetary policy chapters. These chapters complement the preceding

theory chapters in several ways. They provide the historical and institutional background students require

to place their theoretical knowledge in a useful context. The chapters also allow students, through study of

historical and current events, to sharpen their grasp of the theoretical models and to develop the intuition

those models can provide. (Application of the theory to events of current interest will hopefully motivate

students to return to earlier chapters and master points that may have been missed on the first pass.)

Chapter 19 chronicles the evolution of the international monetary system from the gold standard of

1870–1914, through the interwar years, the post-World War II Bretton Woods regime that ended in March

1973, and the system of managed floating exchange rates that have prevailed since. The central focus of

the chapter is the manner in which each system addressed, or failed to address, the requirements of internal

and external balance for its participants. A country is in internal balance when its resources are fully

employed and there is price level stability. External balance implies an optimal time path of the current

account subject to its being balanced over the long run. Other factors have been important in the definition

of external balance at various times, and these are discussed in the text. The basic definition of external

balance as an appropriate current-account level, however, seems to capture a goal that most policy makers

share regardless of the particular circumstances.

Underlying each of these exchange rate systems is the “open economy trilemma,” the observation that you

can have two, but never three, of the following: exchange rate stability, independent monetary policy, and

free capital mobility. Whereas the gold standard traded independent monetary policy for exchange rate

stability and capital mobility, the Bretton Woods system allowed for autonomous monetary policy by

limiting capital flows and the modern floating era sacrifices exchange rate stability for the other two goals.

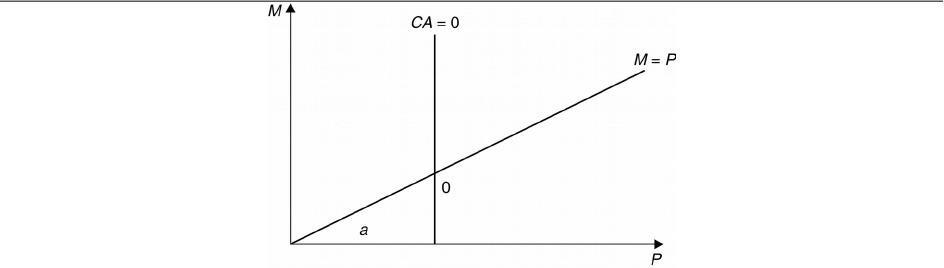

The price-specie-flow mechanism described by David Hume shows how the gold standard could ensure

convergence to external balance. You may want to present the following model of the price-specie-flow

mechanism. This model is based upon three equations:

1. The balance sheet of the central bank. At the most simple level, this is just gold holdings equals the

money supply: G M.

2. The quantity theory. With velocity and output assumed constant and both normalized to 1, this yields

the simple equation M P.

3. A balance of payments equation where the current account is a function of the real exchange rate and

there are no private capital flows: CA f(E P*/P).

These equations can be combined in a figure like the one below. The 45 line represents the quantity theory,

and the vertical line is the price level where the real exchange rate results in a balanced current account.

The economy moves along the 45 line back toward the equilibrium point 0 whenever it is out of equilibrium.

For example, the loss of four-fifths of a country’s gold would put that country at point a with lower prices

and a lower money supply. The resulting real exchange-rate depreciation causes a current account surplus,

which restores money balances as the country proceeds up the 45 line from a to 0.

Chapter 19 International Monetary Systems: An Historical Overview 111

Figure 19-1

The automatic adjustment process described by the price-specie-flow mechanism is expedited by following

“rules of the game” under which governments contract the domestic source components of their monetary

bases when gold reserves are falling (corresponding to a current-account deficit) and expand when gold

reserves are rising (the surplus case).

In practice, there was little incentive for countries with expanding gold reserves to follow the “rules of the

game.” This increased the contractionary burden shouldered by countries with persistent current account

deficits. The gold standard also subjugated internal balance to the demands of external balance. Research

suggests price level stability and high employment were attained less consistently under the gold standard

than in the post-1945 period.

The interwar years were marked by severe economic instability. The monetization of war debt and of reparation

payments led to episodes of hyperinflation in Europe. An ill-fated attempt to return to the prewar gold

parity for the pound led to stagnation in Britain. Competitive devaluations and protectionism were pursued

in a futile effort to stimulate domestic economic growth during the Great Depression. These

beggar-thy-neighbor policies provoked foreign retaliation and led to the disintegration of the world

economy. As one of the case studies shows, strict adherence to the gold standard appears to have hurt

many countries during the Great Depression.

Determined to avoid repeating the mistakes of the interwar years, Allied economic policy makers met

at Bretton Woods in 1944 to forge a new international monetary system for the postwar world. The

exchange-rate regime that emerged from this conference had at its center the U.S. dollar. All other

currencies had fixed exchange rates against the dollar, which itself had a fixed value in terms of gold.

An International Monetary Fund was set up to oversee the system and facilitate its functioning by lending

to countries with temporary balance of payments problems.

A formal discussion of internal and external balance introduces the concepts of expenditure-switching and

expenditure-changing policies. The Bretton Woods system, with its emphasis on infrequent adjustment

of fixed parities, restricted the use of expenditure-switching policies. Increases in U.S. monetary growth to

finance fiscal expenditures after the mid-1960s led to a loss of confidence in the dollar and the termination

of the dollar’s convertibility into gold. The analysis presented in the text demonstrates how the Bretton

Woods system forced countries to “import” inflation from the United States and shows that the breakdown

of the system occurred when countries were no longer willing to accept this burden.

Following the breakdown of the Bretton Woods system, many countries moved toward floating exchange

rates. In theory, floating exchange rates have four key advantages: they allow for independent monetary

policy, they are symmetric in terms of the costs of adjustment faced by deficit and surplus countries, they

act as automatic stabilizers that mitigate the effects of economic shocks, and they help maintain external

balance through stabilizing speculation that depreciates the currency of a country with a large

current-account deficit.

These advantages must be matched with the experience of countries running floating exchange rate regimes.

First, exchange rates have become less stable. For example, in the mid 1970s, the United States chose to

pursue monetary expansion to fight a recession, whereas Germany and Japan contracted their money supplies

to counter inflation. As a result, the dollar sharply depreciated against these currencies. The symmetry

benefit of floating rates is also limited by the fact that the dollar still serves as the world’s reserve currency,

much as it did under Bretton Woods. While floating rates do work as automatic stabilizers, the effects may

be unevenly distributed within countries. For example, the U.S. fiscal expansion of the 1980s appreciated

the dollar, limiting inflation overall. However, U.S. farmers were hurt by this action as the stronger dollar

weakened exports. With immobile factors of production, these asymmetric effects can have long-run

consequences. Finally, empirical evidence suggests that external imbalances have actually increased since

the adoption of floating exchange rates. The chapter concludes with a discussion of policy coordination

under floating exchange rates. For example, a large country with a current-account deficit that attempts

to reduce their imbalance could cause global deflation. There is also a market failure at work here in that

policies by one country have external effects. For example, the 2007–2009 financial crisis sparked a

number of fiscal expansions in countries. Increased government spending in the United States for example,

helped lift demand not just in the United States but in other countries as well. Since the benefits of fiscal

expansion are not fully internalized (though the costs are through accumulated budget deficits), there will

be an inefficiently small expansion from a global perspective. Thus, international policy coordination,

even in a world of flexible exchange rates, may still be warranted.