Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

n Answers to Textbook Problems

1. A decline in investment demand decreases the level of aggregate demand for any level of the

2. A tariff is a tax on the consumption of imports. The demand for domestic goods, and thus the level

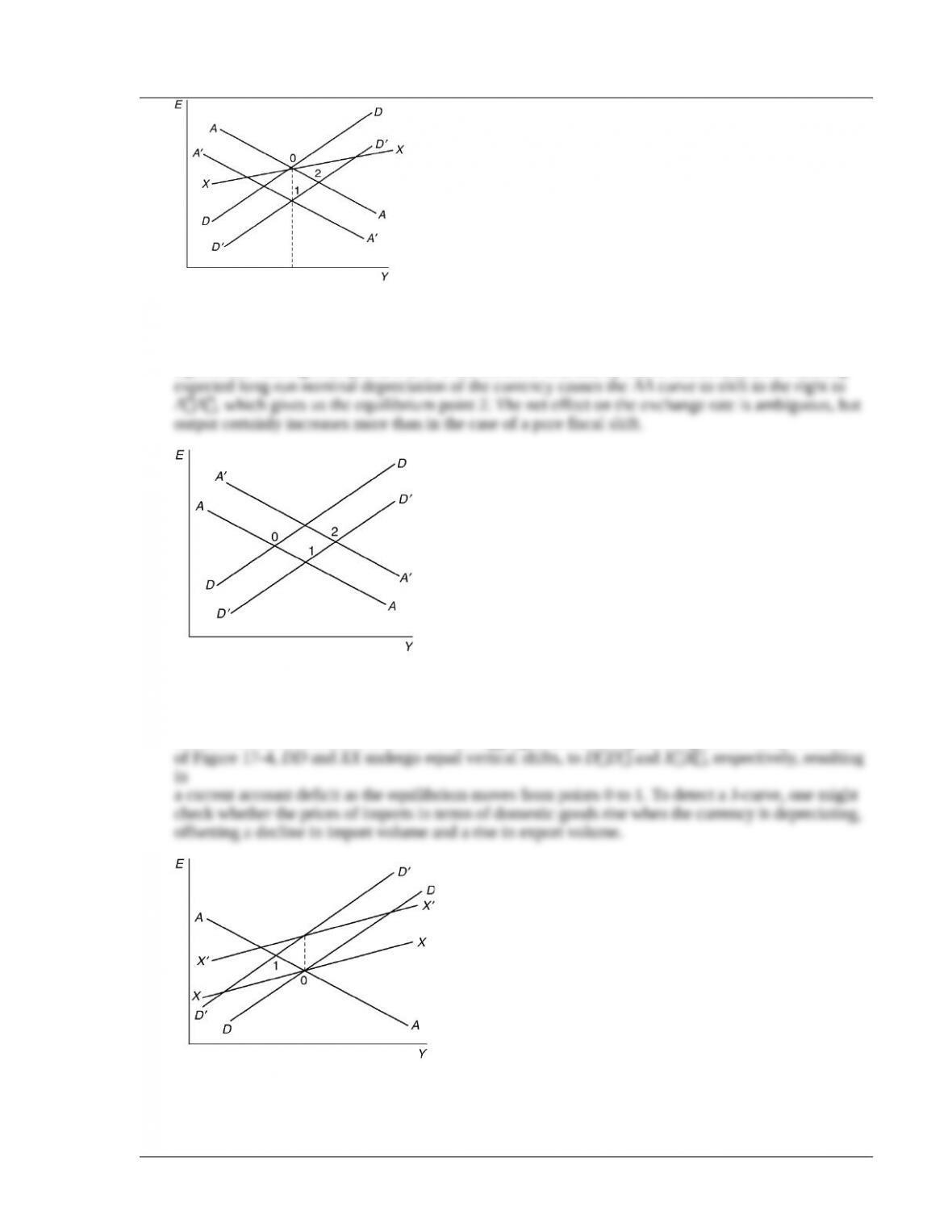

Figure 17-1

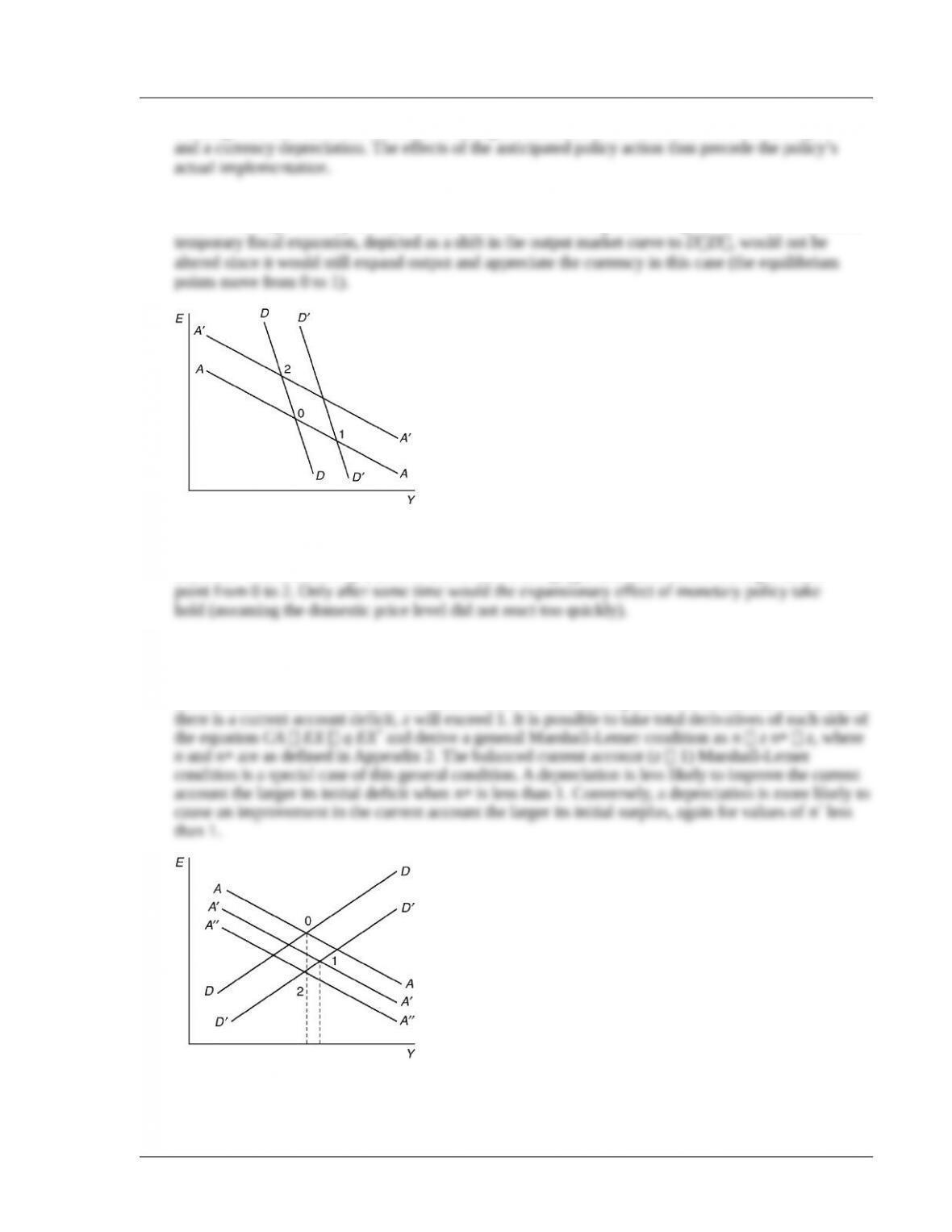

3. A temporary fiscal policy shift affects employment and output, even if the government maintains a

balanced budget. An intuitive explanation for this relies upon the different propensities to consume

of the government and of taxpayers. If the government spends $1 more and finances this spending

4. A permanent fall in private aggregate demand causes the DD curve to shift inward and to the left and,

because the expected future exchange rate depreciates, the AA curve shifts outward and to the right.

5. Figure 17-2 can be used to show that any permanent fiscal expansion worsens the current account.

In this diagram, the schedule XX represents combinations of the exchange rate and income for which

the current account is in balance. Points above and to the left of XX represent current account surplus,

and points below and to the right represent current account deficit. A permanent fiscal expansion shifts

© 2012 Pearson Education, Inc. Publishing as Addison-Wesley

Chapter 17 Output and the Exchange Rate in the Short Run 89

Figure 17-2

6. A temporary tax cut shifts the DD curve to the right and, in the absence of monetization, has no effect

on the AA curve. In Figure 17-3, this is depicted as a shift in the DD curve to DD, with the

equilibrium moving from points 0 to 1. If the deficit is financed by future monetization, the resulting

Figure 17-3

7. A currency depreciation accompanied by a deterioration in the current account balance could be

caused by factors other than a J-curve. For example, a fall in foreign demand for domestic products

worsens the current account and also lowers aggregate demand, depreciating the currency. In terms

Figure 17-4

© 2012 Pearson Education, Inc. Publishing as Addison-Wesley

Chapter 17 Output and the Exchange Rate in the Short Run 90

8. The expansionary money supply announcement causes a depreciation in the expected long-run

exchange rate and shifts the AA curve to the right. This leads to an immediate increase in output

9. The DD curve might be negatively sloped in the very short run if there is a J-curve, though the absolute

value of its slope would probably exceed that of AA. This is depicted in Figure 17-5. The effects of a

Figure 17-5

Monetary expansion, however, while depreciating the currency, would reduce output in the very

short run. This is shown by a shift in the AA curve to AA and a movement in the equilibrium

10. The derivation of the Marshall-Lerner condition uses the assumption of a balanced current account to

substitute EX for (q EX*). We cannot make this substitution when the current account is not initially

zero. Instead, we define the variable z (q EX*)/EX. This variable is the ratio of imports to exports,

denominated in common units. When there is a current account surplus, z will be less than 1, and when

Figure 17-611. If imports constitute part of the CPI, then a fall in import prices due to an

appreciation of the currency will cause the overall price level to decline. The fall in the price level

raises the real money supply. As shown in Figure 17-6, the permanent fiscal expansion will shift the

© 2012 Pearson Education, Inc. Publishing as Addison-Wesley

Chapter 17 Output and the Exchange Rate in the Short Run 91

12. An increase in the risk premium shifts the asset market curve out and to the right, all else being equal.

A permanent increase in government spending shifts the asset market curve in and to the right since

it causes the expected future exchange rate to appreciate. A permanent rise in government spending also

causes the goods market curve to shift down and to the right since it raises aggregate demand. In the

13. Suppose output is initially at full employment. A permanent change in fiscal policy will cause both

the AA and DD curves to shift such that there is no effect on output. Now consider the case where the

economy is not initially at full employment. A permanent change in fiscal policy shifts the AA curve

because of its effect on the long-run exchange rate and shifts the DD curve because of its effect on

expenditures. There is no reason, however, for output to remain constant in this case since its initial

value is not equal to its long-run level, and thus an argument like the one in the text that shows the

14. If some of the currency appreciation is temporary due to the current account effects, we will see a slightly

different process after a permanent fiscal expansion. We would not necessarily still jump from points 0

to 2 in Figure 17-2 above. We know that over time, the shift in consumption preferences away from

© 2012 Pearson Education, Inc. Publishing as Addison-Wesley

Chapter 17 Output and the Exchange Rate in the Short Run 92

16. It is difficult to see how government spending can rise permanently without increasing taxes or how

taxes can be cut permanently without cutting spending. Thus, a truly permanent fiscal expansion is

17. High inflation economies should have higher pass-through as price setters are used to making adjustments

faster (menu costs fall over time as people learn how to change prices faster). Thus, a depreciation in

18. A “buy American” provision would have resulted in a larger rightward shift in the DD curve than an

unconstrained increase in government spending since there will be a greater demand for U.S. output

© 2012 Pearson Education, Inc. Publishing as Addison-Wesley