4-2. (1 + i)20 > 3

20log(1 + i) > log 3

4-3. [a] 8% simple interest

I = P x s x N = $5,000 x 0.08 x 10 = $4,000

4-5. A = $2,000,000(A/F,0.5%,360)

4-6. $250(P/A,1%,N) = $15,000

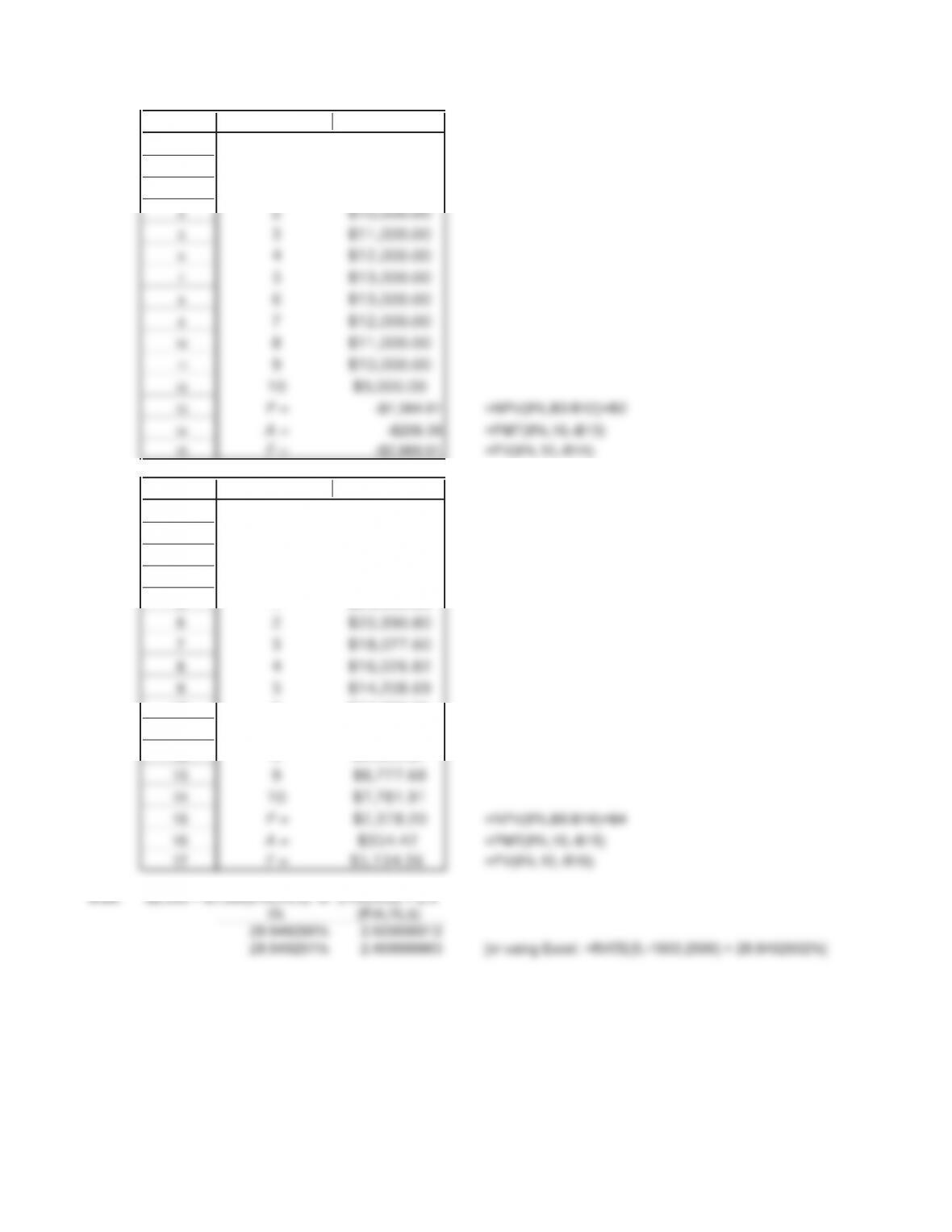

4-7. $15,000 = $5,000(F/P,i%,10)

(1 + i)10 = 3.0 0.047712125

10log(1 + i) = log 3

log (1 + i) = 0.0047712125 [or using Excel: =RATE(10,,-5000,15000) = 11.612%]

(1 + i) = 1.116123174

11.612% annual compound interest will cause money to triple in value in 10 years.

Chapter 4

29

4-8. [a] $3,000(F/A,5%,25) = $3,000(47.7271) = $143,181.30 (Excel solution yielded $143,181.30)

4-9. [a] A = $50,000(A/P,6%,10) = $50,000(0.1359) = $6,795.00

4-10. [a] P = $2,000(P/A,8%,10) = $2,000(6.7101) = $13,420.20.

4-11. Since money has a time value, receiving money sooner is preferred to receiving it later. Hence,

prefer to receive $10,000/year for 5 years.

4-12. F2010 = $5,000(F/P,6%,5) + $4,500(F/P,6%,4) + $4,000(F/P,6%,3) + $3,500(F/P,6%,2) +

4-13. F2010 = (((($5,000(1.05) + $4,500)(1.055) + $4,000)(1.06) + $3,500)(1.065) + $3,000)(1.07) +

$2,500 = $26,955.11

4-14. F = $3,000(F/P,6%,2)(F/P,5%,2)(F/P,4%,2)(F/P,3%,2) + $3,000(F/P,6%,1)(F/P,5%,2)(F/P,4%,2)

4-15. F = $3,000(F/A,4.5%,9) = $3,000[((1.045)9 – 1)/0.045] = $32,406.34

4-16. F = P(F/P,i%,N), where F = 37¢, P = 6¢, N = 32; solve for i%.

4-17. A = $10,000(A/P,6%,5) = $10,000(0.2374) = $2,374 (Will use Excel solution: $2,373.96)

Amount Owed After PaymentPayment

Principal

Payment

Interest

Payment

30

4-18. A = $15,000(A/P,8%,10) = $15,000(0.1490) = $2,235

After 1st payment, still owe P = $2,235(P/A,8%,9) = $2,235(6.2469) = $13,961.82.

4-19. Delaying payment for four years results in $15,000(F/P,8%,4), or $15,000(1.3605) = $20,407.50 owed.

Hence, the new payment size will equal $20,407.50(A/P,8%,10) = $20,407.50(0.1490) = $3,040.72.

4-20. F = $5,000(F/A,6%,40) = $5,000(154.762) = $773,810. (Excel solution yielded $773,809.83)

4-23. A = $773,810(A/F,6%,30) = $773,810(0.0126) = $9,750.01 (Excel solution yielded $9,787.85)

4-25. $2,859,700 = X[(F/P,6%,30) – (F/P,8%,30)]/(-0.02) = -50X(5.7435 – 10.0627)

X = $2,859,700/215.96 = $13,241.80 (Excel solution yielded $13,241.91)

4-27. A = $2,859,700(A/F,6%,40) = $2,859,700(0.0065) = $18,588.05 (Excel solution yielded $18,478.05)

4-28. $100,000 = $1,000(F/A,i%,60) or (F/A,i%,60) = 100

i% (F/A,i%,60)

1.615020% 99.99977766

31

4-30. P = -$100,000+$23,000(P/A,8%,10)-$2,000(P/G,8%,10) = -$100,000+$23,000(6.7101)-$2,000(25.98)

Excel solution shown below

AB

1

MARR =

8%

2EOY CF(A)

30 -$100,000

41 $23,000

52 $21,000

63 $19,000

AB

1

MARR =

8%

2EOY CF(A)

30 -$100,000.00

41 $23,000.00

96 $12,137.83

10 7 $10,681.29

11 8 $9,399.54

32

4-32. AB

1EOP Cash Flow

20 -$75,000.00

31 $9,000.00

4-33. AB

1

i =

8.00%

2

j

= -11.34433% (Trial and error solution)

3EOP Cash Flow

40 -$100,000.00

51 $23,000.00

10 6 $12,596.81

11 7 $11,167.78

12 8 $9,900.87

33

4-35. AB

1

i =

8.00%

2

G

= $1,000.00

3EOP Cash Flow

40 -$60,000.00

4-36. [a] Effective rate = (1.05)2 – 1 = 10.25000000%

[b] Effective rate = (1.025)4 – 1 = 10.38128906%

4-37. [a] P = $100,000(P/F,6%,25) = $100,000(0.2330) = $23,300

(From Excel’s PV function, $23,299.86)

4-38. [a] Effective rate = (1.08)1 – 1 = 8%

[b] Effective rate = (1.04)2 – 1 = 8.16%

4-39. P = $2,500(P/A,9.53%,5) = $2,500[(e0.0953(5) – 1)/(e0.0953(5)(e0.0953 – 1))]

P = $9,477.24

34

4-41. [a] 10% compounded annually is equivalent to ln1.10, or 9.531018% compounded continuously.

P = $150,000(er-1)/rer; however, in this case, er = 1+i, or 1.10.

4-42. [a] $10,000 = (($X(P/F,6%,1)+$X)(P/F,5%,1)+$X)(P/F,4%,1)

$10,000 = (0.9434)(0.9524)(0.9615)X + (0.9524)(0.9615)X + (0.9615)X 4% 5% 6%

[b] $10,000 = (($X(P/F,4%,1)+$X)(P/F,5%,1)+$X)(P/F,6%,1) $X

4-43.

0 -$50,000.00

1 4.00%

2 4.25%

3 4.50%

4-44. P = $5,000(P/A,8%,5)(P/F,8%,4) 8% compounded annually

$X

$10,000

$10,000

Cumulative

Balance

$50,000.00

End of

Year Cash Flow Interest Earned

$52,000.00

$54,210.00

$56,649.45

$5,000

$P

35

4-46. P = [$5,000(P/A,8%,5) + $500(P/G,8%,5)](P/F,8%,4)

4-47. P = {$5,000[1 – (P/F,8%,5)(F/P,12%,5)]/(0.08 – 0.12)}(P/F,8%,4)

4-48. P = [$5,000(P/A,8%,5) – $500(P/G,8%,5)](P/F,8%,4)

4-49. P = {$5,000[1 – (P/F,8%,5)(1-0.12)5]/(0.08 + 0.12)}(P/F,8%,4)

4-50. The cash flow diagram can be represented as a $200 uniform series over [0,9] combined with a $300

uniform series over [4,5] and over [10,12]. To solve for all parts, it is convenient to compute the present

worth equivalent of the cash flows.

4-51. i = 8%

EOY Cash Flow

0 -$45,000

1 $10,000

4-52. A = $4,944.74(A/P,8%,8) = $4,944.74(0.1740) = $860.38 (Excel solution yielded $860.46)

4-55. i = 8%

j = -4.60096% (Trial and error solution required)

EOY Cash Flow

0 -$45,000

1 $10,000

37