SOLUTIONS TO CHAPTER 18 PROBLEMS

Activity Based Costing and Management

18-1. Successes and failures in ABC implementation have indicated that to succeed in this endeavor, firms need to

have a series of characteristics and commitments: Two of the most important are enjoying top management

commitment and involvement, and clear relevance of the ABC initiative for the whole organization. If the

18-2. There are many answers, mostly focused on change and people’s resistance to change

18-3. Firms and environments that characterize themselves as “we’re really not sure how much it costs us to

manufacture X are prime candidates for an activity- based cost system. It may be a bit arrogant to think that

18-4. In many ways ABC has already gone through the “fad” stage as tar as “the latest management program on the

block” is concerned, having been first introduced commercially over 10 years ago. Many of the “acronym

18-5. A list of potential monetary and other attributes might include items

such as:

• Investment costs in computers, etwork1ng, software, data collection devices

• Software development and integration costs

• Cost of training

• Documentation costs

214

18-6. Direct costs are those that can be reasonably measured and allocated to a specific output or work activity.

Indirect costs are those that are difficult to attribute or allocate to a specific output or work activity. Indirect costs

are also commonly referred to as overhead.

The focus of ABC is to find a way to measure and capture all costs associated with a product or activity, as

direct costs. Based on this assumption and the definitions above, all costs are indirect costs until we find a way

to isolate those costs or portions of costs that are created as a direct result of the work activity undertaken.

Similarly, all costs have the potential to be captured as a direct cost, if we can determine a way to measure

18-7 Example cost pools are:

Sales and promotion Maintenance

215

18-8

Activities Some Appropriate Cost Drivers (others could be found

depending of data availability)

Oven set up Number of production lots

Oven maintenance Number of units produced

216

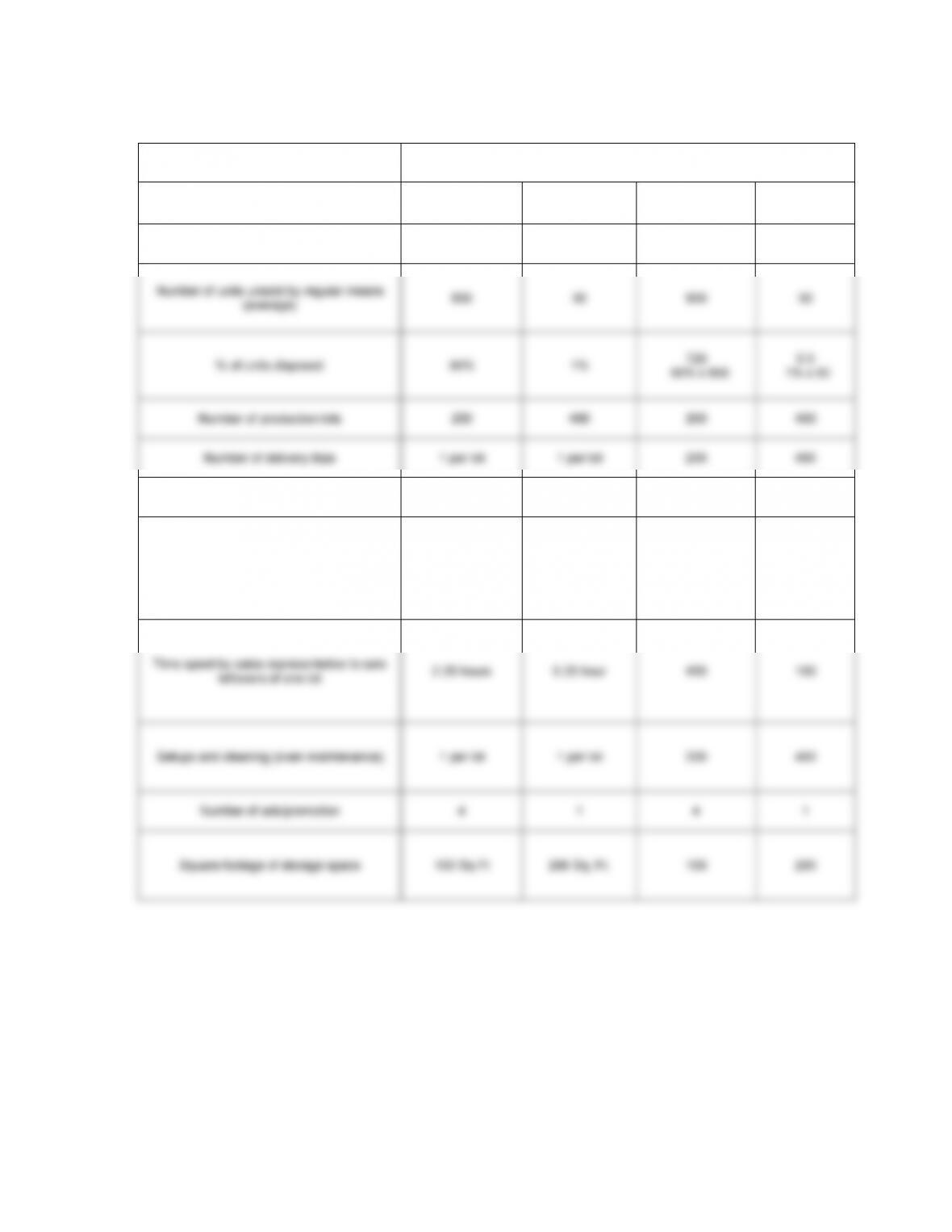

18-9

Cost Drivers’ Information

Cost Drivers

French Bread Wheat Bread French Bread Wheat Bread

Number of units produced 2,000 8,000 2,000 8,000

Number of disposal trips 1 per lot none 200 0

Time spent on the phone by sales

representative to sell one lot 3 hours 0.5 hour 240 200

217

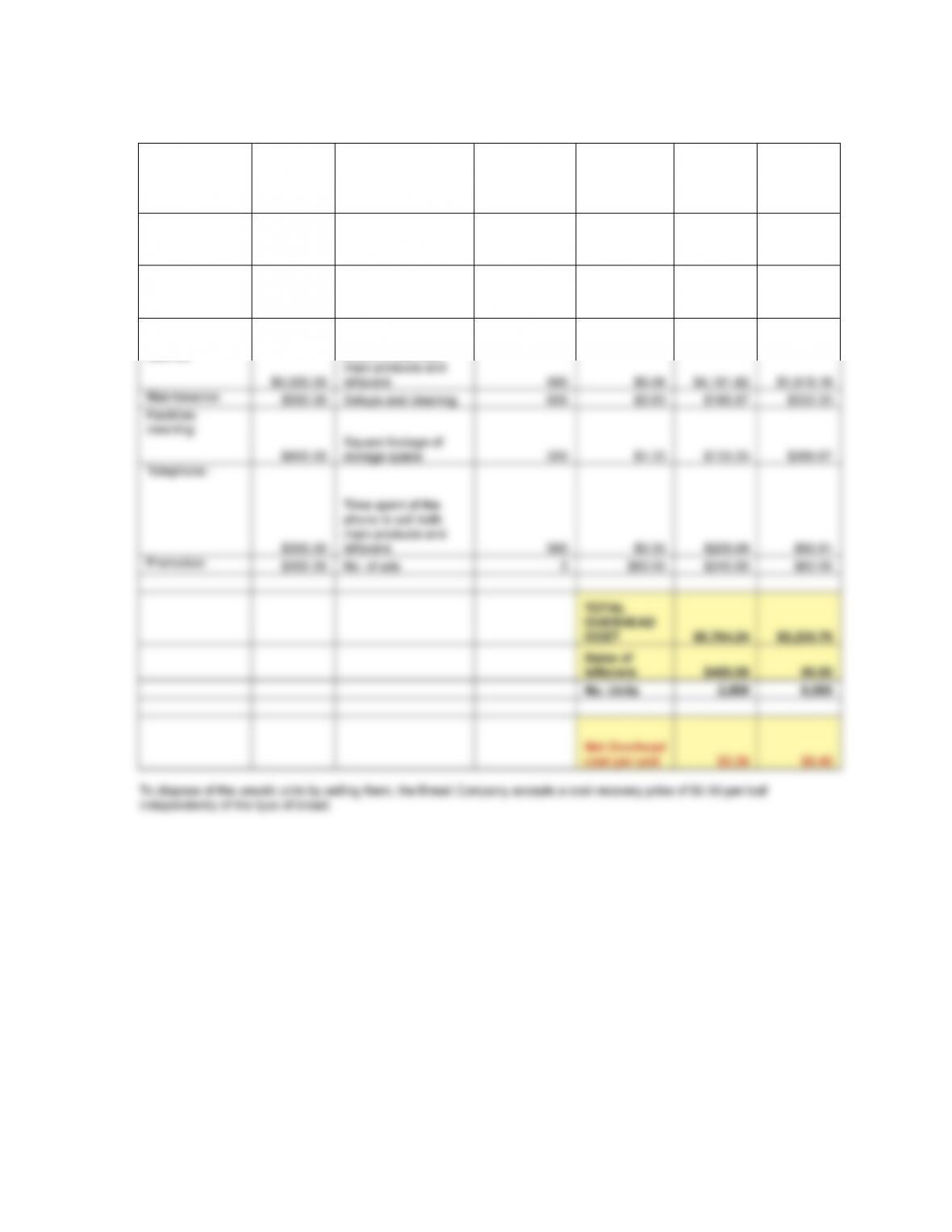

18-9 .(Continued)

Cost

Information: Cost Driver

No. Annual

transactions

Cost per

transaction

French

Bread

Wheat

Bread

Transportation of

sold products:

$1,000.00

Number of delivery

trips

600 $1.67 $333.33 $666.67

Transportation

and disposal of

unsold products: $1,500.00

Number of disposal

trips

200 $7.50 $1,500.00 $ –

Sales

department

salaries:

Time spent on the

phone to sell both

218

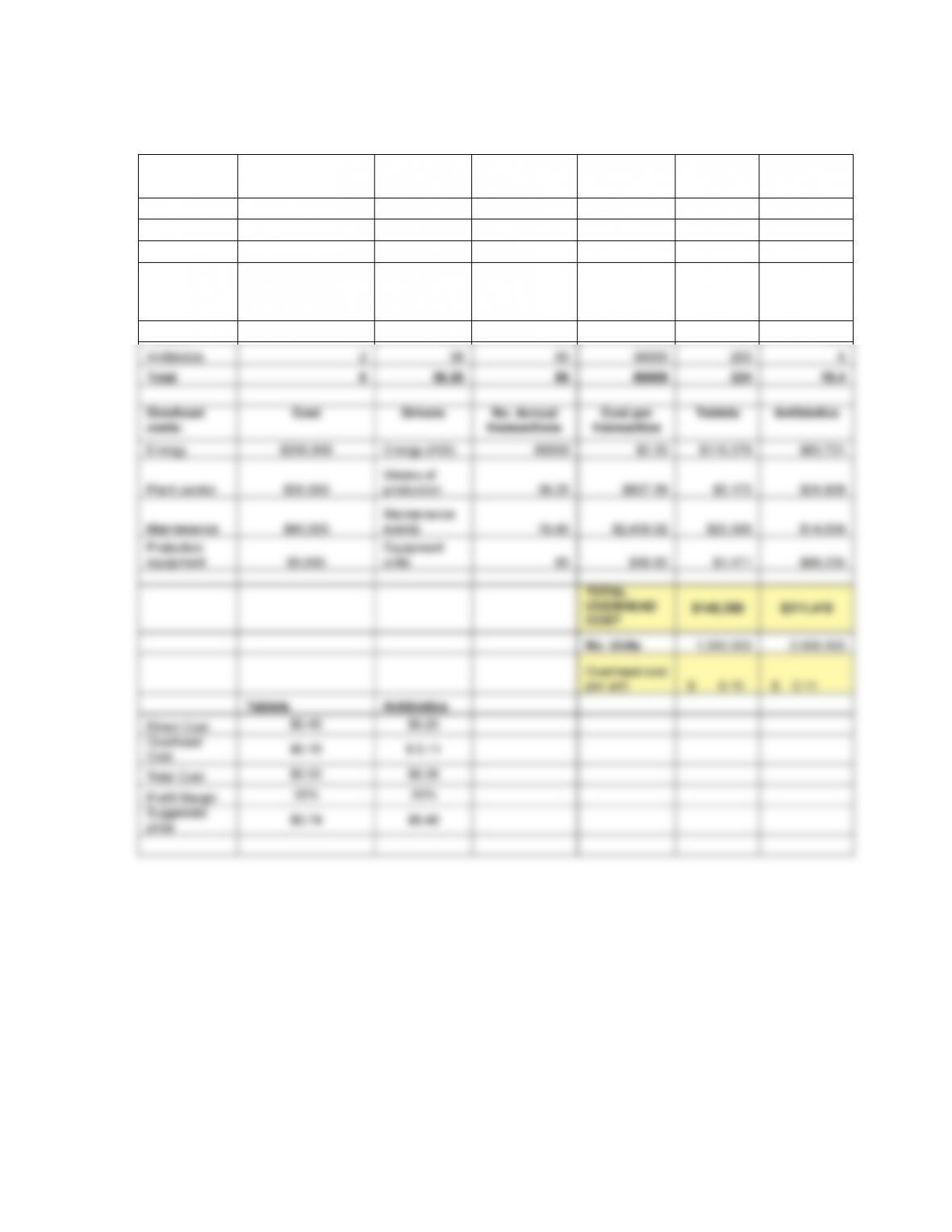

18-9 .(Continued)

a

French

Bread

Wheat

Bread

No. Units 2,000 8,000

Direct cost per

unit $0.75 $1.25

219

18-10 There are several possible ways to create a flow chart that reflects the operations and processes necessary to

deliver a service or manufacture a product. This first step helps the analyst realize the number of activities and processes

involved in the operation. Each node in the flow chart is an activity to which resources can be allocated. The level of detail

A

nswer the phone and

ask for customer

Look for customer

account in the system

220

18-11.

Production in units Direct costs: Kg of

production

Energy per

hour of

production

Production

Rate

Production

Hrs

Tablets 1,000,000 $400,000 $50,000 200KW 24 kg/hr 250

Antibiotics 2,000,000 $500,000 $120,000 30KW 100 kg/hr 1200

Operators production

weeks

No. of

protection

equipment

units

Energy

consumption

(KW-HR)

cycles events

Tablets 4 6.25 25 50000 24 10.4

221

18-12.

Cost Item Cost Drivers No. of transactions Cost per

transaction Service A Service B

Sales

representatives

salaries $140,000

Estimated % of

effort 100% $140,000 $35,000 $105,000

18-13 Manufacturing Costs under current system

Direct Costs :

222

Manufacturing Costs under ABC

Direct Costs :

Direct materials $100.000

Direct Labor 300,000

Overhead

223