SOLUTIONS TO CHAPTER 16 PROBLEMS

Decision Tree Analysis

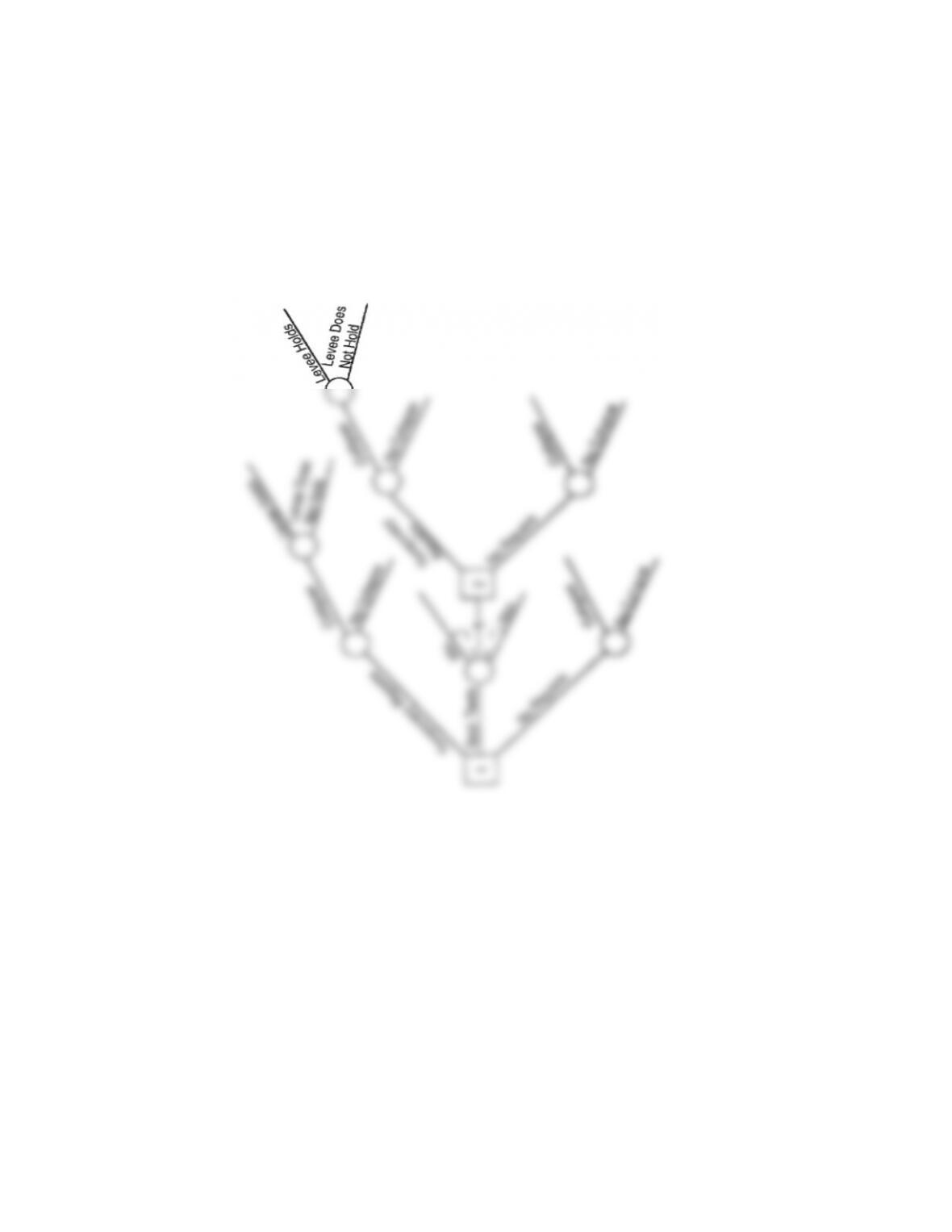

16-1.

195

16-2.

196

16-3. (a) M – thousands

197

16-3. (continued)

(b) Posterior Probabilities, Given Prediction Price Will Go Up, (u)

(1) (2) (3) (4)=(2)(3)

(5)=(4)/ ∑(4)

(Price) P(Price) P(u l Price) Joint Probab. P (Price l u)

High 0.3 0.9 0.27 0.43

Dec. 2:

Stock: $100M(0.43) – $10M(0.32) – $100M(0.25) = $14,800 Å Better

No Stock: = $0

198

16-4. (a)

PW(Success) = $100,000(P/A,20%,8) = $383,700

PW(Fail) = -$30,000(P/A,20%,2) = -$45,800

Market:

E(PW) = $383,700(0.25) – $45,800(0.75) – $50,000 = $11,575

(b) Outcome SYMBOL

Actual Outcome Prediction

Successful S s

199

16-4. (continued)

Posterior Probabilities, Given Prediction of Failure, (f):

Outcome P(Outcome) P(f l Outcome) Joint Probab. P(Outcome l f)

S 0.25 0.2 0.05

F 0.75 0.9 0.675

∑ = 0.725

0.07

0.93

200

16-4 (continued)

M — thousands

201

16-5. M ≡ thousands

202

16-5. (continued)

203

16-6. First, analyzing the alternatives at Decision Point 2:

For Alternative NC the present worth of costs is

$1,000(P/A,12%,7)(0.2) + $18,000(P/A,12%,7)(0.8)

204

16-6. (continued)

For alternative RLW the present worth of costs is

= $18,000(P/A,12%,10)(0.15) + [$18,000(P/A,12%,3)

205

16-7. (a) Decision tree diagram showing outlays (costs) as negative numbers.

(continued)

(b) Dec. 2:

16-7.

Manual: = -$20M – $14M(P/A, 10%,5)

Dec. 1:

Automatic: = -$50M – $10M(P/A,10%,10)

= –$50M – $1 0M(6.114)

(c) Find i’ at which present worths are equal (or ∆ PW = 0)

-$20M – $14M(P/A,i’%,5) = -$40M – $11 M(P/A, i’ %,5) + $20M(P/F, i %,5)

Interest PW

(Manual)

PW

(Semi-Auto) ∆ PW

207

16-8. P(h)

P(H) H)|P(h

P(D)D)|P(h P(H)H)|P(h

P(H) H)|P(h

h)|P(H •

=

•+•

•

=

0.48

0.60.80 ==

•

M ≡ thousands

Dec. Pt. Alt. Expected Monetary Outcome

2a Old $45M(0.75)+$27.5M(0.25)-$1 0M = $30.62M

New $75M(0.75)+$43M(0.25)-$35M = $32.0M Å Better

208

$10M(P/A,0%,10) = $1 0M(10) = $100M Å Better

$20M(P/F,0%,10) = $20M(1) = $ 20M

16-9. Note: M ≡ thousands

Dec. 4:

Keep:

Abandon:

Dec. 5:

209

16-9. (continued)

Dec. 1:

Buy: [$220M(P/F,0%,10)+$10M(P/A,0%,10)](0.6)

+ $20M(P/A,0%,25)(0.4) – $100M

16-10. Note: MM = millions

Dec. 3 Start Commercialization:

Yes: $2.00MM(P/A,20%,6)(0.9) + $0MM(0.1) – $1.50MM

16-10. (continued)

Dec. 1 Start Applied Research:

Yes: $1.94MM(P/F,20%,1)(0.5) + $0MM(0.5) – $0.10MM

16-11. Posterior Probabilities, Given Seismic Sounding is “No Structure:”

(4)=(2)(3)

Joint Probab.

(3)

P(No l Outcome)

(1)

Outcome

(2)

P(Outcome)

(5)=(4)/ ∑ (4)

P(Outcome l No)

N: Dry

Wet

.5

.3

.6

.3

.30

.09

.73

.22

211

SOLUTIONS TO CHAPTER 17 PROBLEMS

Capital Investment Decisions as Options

17-1. (a) The NPV of 1 million is positive but not over whelmingly so given the size of the proposed investment. Very minor

changes in the estimated costs could make this NPV negative.

17-2. The risk free rate impacts the value of NPVq .

17-3. S =41

X = 60

PV(X) =

t

)2.01/(60 +

17-4. t=1

σ

= 0.4 according to Luehrman

X = 500

S = PV of $150 per year over 19 years

rf = 0.02

212

Option value (0.37)(808)

≈298.96, using 37% as the table value.

0.37 estimated from table 17.1

808 Value of S

17-5. $112M = S

$6M $ 106M = X

17-6. See the concluding section of the chapter, How Far Can You Extend The Framework for many comments on assumptions

and limitations.

213