13-12 Let X = annual Btu requirement (in 103 Btu)

AC(oil) = $80,000(A/P,10%,20) – $4,000 + X($1.10) / (140 x 103 Btu) =

$5,400 + $0.008X

Annual Costs ($)

% chan

g

e in X Oil Gas

-30 7,430 6,125

-20 7,720 6,850

-10 8,010 7,575

0 8,300 8,300

10 8,590 9,025

161

13–13. x =change in initial investment cost of heat exchanger

y = change in annual leasing expense

AC (purchase) = $10,000(1+x)(A/P,5%,5) + $1,000 + $500(A/G,5%,5)

-$2,000(A/F,5%,5) = $3,899.25 + 2,310x

162

b) +10% change in average operating cost :

Annual Operating Costs = ($1 8.50 / ton)(1. 10)(2,000,000 tons) •$40,700,000

Annual Gross Income = $25,300,000

Annual Depletion Allowance = ($25,300,000)(0.10) = $2,530,000

A B C D E F

13–14 a) Price of Property

Equipment Investment

Workin

g

Ca

p

ital

$24,000,000

$60,000,000

$5,000,000

Total Capital Invested $89,000,000

Annual Revenues ($38/ton)(2,000,000 tons) =$ 76,000,000

163

13-14. b) (continued.)

-10% change in average operating cost :

Annual Operating Costs = ($18.50/ton)(0.90)(2,000,000 tons) = $33,300,000

164

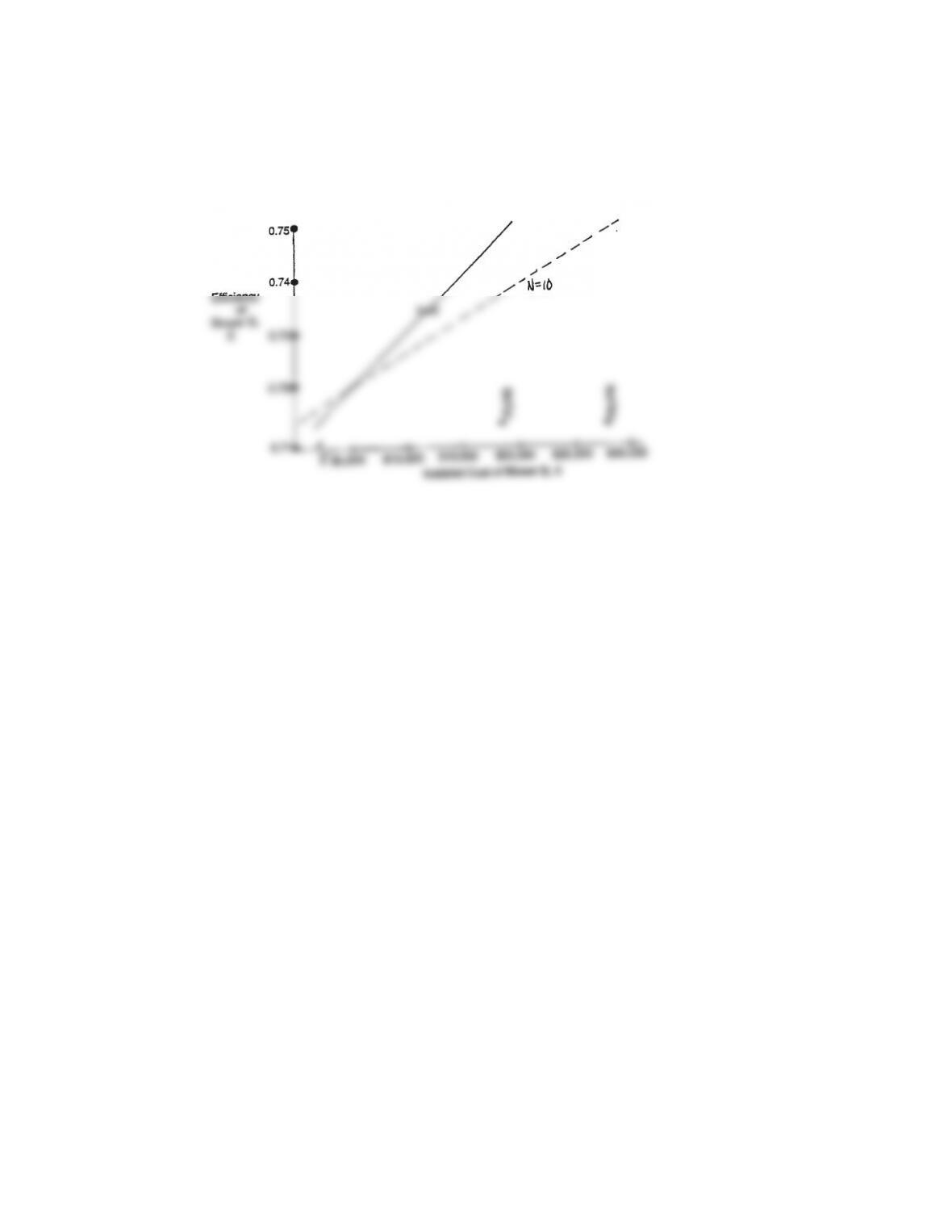

13-15

(1) Assume the two blowers are equally desirable and have the same life, N years. Let the

installed cost of Blower B equal $X. Their price difference, $5,000 versus $X, must be

balanced against energy savings arising because of the difference in operating efficiency. Also

assume continuous operation for 8760 hours per year, in addition to negligible salvage

values.

(2) Let the efficiency of the more expensive Blower B be “Z” and let

W = 200(0.746)(8,760). Then

X (A/P, 10%, N) + yW/Z = 5,000 (A/P, 10%, N) + yW/0.72

165

13-15. (continued)

The plot is shown below.

166

13-16 a) AC(A) = $2,000(A/P,10%,6) + $3,500 = $3,959

AC(B) = $6,000(A/P,10%,3) + $1,000 – $4,000(A/F,10%,3) = $2,204

c) Project A is preferred if AC(A) <= AC(B). Let x =proportion change in Project A

investment cost and y = proportion change in Project A annual disbursements.

$2,000(1+x)(A/P,10%,6) + $3,500(1+y) <= $2,204

$3,959 + $459.2x + $3,500y <=$2,204

167

13-17 a) Alternative A

Year BTCF

MACRS

Depreciation

Taxable

Income

Cash Flow

for Income

Taxe

s

ATCF

0 -108

,

000

,

000 – – -108

,

000

,

000

1 -3

,

460

,

000 5

,

400

,

000 -8

,

860

,

000 3

,

544

,

000 84

,

000

2 -3

,

460

,

000 10

,

260

,

000 -13

,

720

,

000 5

,

488

,

000 2

,

028

,

000

3 -3

,

460

,

000 9

,

234

,

000 -12

,

694

,

000 5

,

077

,

600 1

,

617

,

600

4 -3

,

460

,

000 8

,

316

,

000 -11

,

776

,

000 4

,

710

,

400 1

,

250

,

400

5 -3

,

460

,

000 7

,

484

,

400 -10

,

944

,

400 4

,

377

,

760 917

,

760

6 -3

,

460

,

000 6

,

728

,

400 -10

,

188

,

400 4

,

075

,

360 615

,

360

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

PW(A) = -$99,472,154

Alternative B:

Year BTCF

MACRS

Depreciation

Taxable

Income

Cash Flow

for Income

Taxes ATCF

0

–

17,000,000

— –

17,000,000

1 -12

,

400

,

000 850

,

000 -13

,

250

,

000 5

,

300

,

000 -7

,

100

,

000

2 -12

,

400

,

000 1

,

615

,

000 -14

,

015

,

000 5

,

606

,

000 -6794

,

000

3 -12

,

400

,

000 1

,

453

,

500 -13

,

853

,

500 5

,

541

,

400 -6

,

858

,

600

4 -12

,

400

,

000 1

,

309

,

000 -13

,

709

,

000 5

,

483

,

600 -6

,

916

,

400

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

168

,

,

,

,

,

,

,

,

,

13-17 (continued)

Alternative B (revised to include extra investment permissible to breakeven):

Year BTCF

MACRS

Depreciation Taxable

Income

Cash Flow

for Income

Taxes ATCF

0 -42,731,490 – – — — -42,731,490

10 -15,400,000 2,521,158 -17,921,158 7,168,463 -8,231,537

11 -12,400,000 2,525,431 -14,925,431 5,970,172 -8,429,828

12 -12,400,000 2,521,158 -14,921,158 5,968,463 -8,431,537

13 -12,400,000 2,525,431 -14,925,431 5,970,172 -6,429,828

14 -12,400,000 2,521,158 -14,921,158 5,968,463 -5,431,537

169

b) Alternative A:

Year BTCF

MACRS

Depreciation Taxable

Income

Cash Flow

for Income

Taxes ATCF

0 -108,000,000 – – -108,000,000

1 -3,460,000 5,400,000 -8,860,000 3,544,000 84,000

170

13-17 (continued)

Alternative B:

Year BTCF

MACRS

Depreciation

Taxable

Income

Cash Flow

for Income

Taxes ATCF

0 -17,000,000 — -17,000,000

1 -12,400,000 850,000 –13,250,000 5,300,000 -7,100,000

2 -12,400,000 1,615,000 -14,015,000 5,808,000 –8,794,000

3 -12,400,000 1,453,500 -13,853,500 5,541,400 -8,858,600

4 -12,400,000 1,309,000 -13,709,000 5,483,600 -8,916,400

171

13-18 The following equations represent the present worths of the defender

(D) and the challenger (C) as a function of the effective income tax

rate, t:

PW(0) = –150,000 + 38450(t / 2) – 578,000(1 – t)(P/A,10%,8)

Defender:

Year BTCF

MACRS

Depreciation

Taxable

Income

Cash

Flow

for ATCF

0 -150

,

000 -38

,

450 15

,

380 -134

,

620

1 -578

,

000 44

,

600 -622

,

600 249

,

040 -328

,

960

2 -578

,

000 44

,

650 -622

,

650 249

,

060 -328

,

940

3 -578

,

000 22

,

300 -600

,

300 240

,

120 -337

,

880

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

Challenger:

Year BTCF

MACRS

Depreciation

Taxable

Income

Cash Flow

for Income

Taxes ATCF

0 — — — — —

172

Present Worth

% change Defender Challenger

–50% -2,573,192 -1,920,573

–40% -2,445,778 -1,824,545

–30% -2,318,364 –2,728,516

–20% -2,190,950 –1,632,487

173