SOLUTIONS TO CHAPTER 10 PROBLEMS

New Product and Expansion Analysis

Note to instructor: Advise students to use a 40% income tax rate unless directed otherwise.

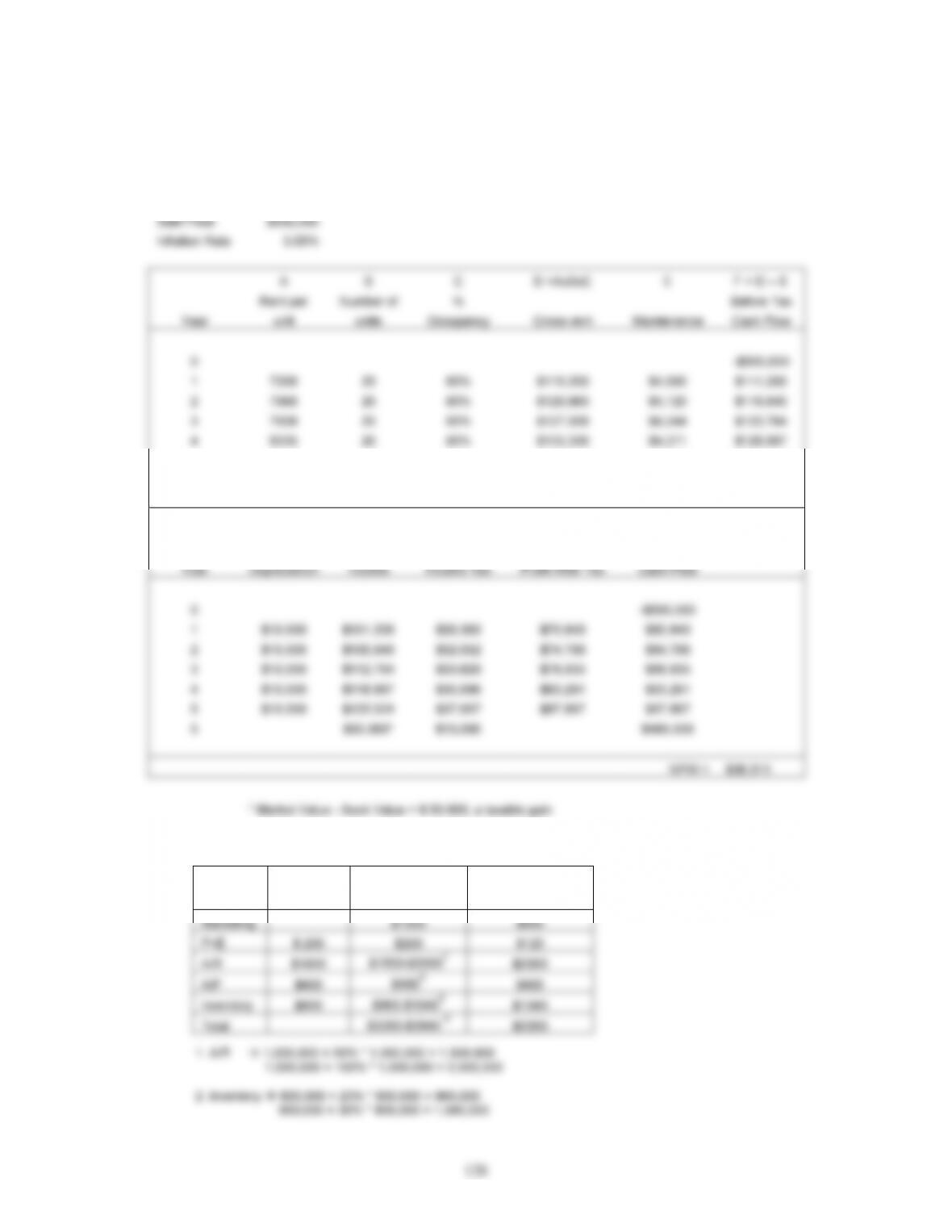

10-1 (a)

Interest Rate 15.00%

Purchase Price $ 500,000

Tax Rate 30.00%

Sale Price $500,000

A B C D =AxBxC E F = D – E

Rent per Number of % Before Tax

Year unit units occupancy Gross rent Maintenance Cash Flow

0 -$500,000

1 $7,200 20 90% $129,600 $4,000 $125,600

2 $7,200 20 90% $129,600 $4,000 $125,600

Taxable

Year Depreciation Income Income

Tax

Profit After

Tax

Cash Flow

0 -$500,000

1 $10,000 $115,600 $34,680 $80,920 $90,920

2 $10,000 $115,600 $34,680 $80,920 $90,920

126

10-1. (continued)

(b)

Interest Rate 15.00%

Purchase

Price $ 500,000

Tax Rate 30.00%

4 $7,200 20 60% $86,400 $4,000 $82,400

5 $7,200 20 60% $86,400 $4,000 $82,400

5 $500,000

G H =D -E – G

I=H x Tax

rate J = H – I

K =F – I

=J+G

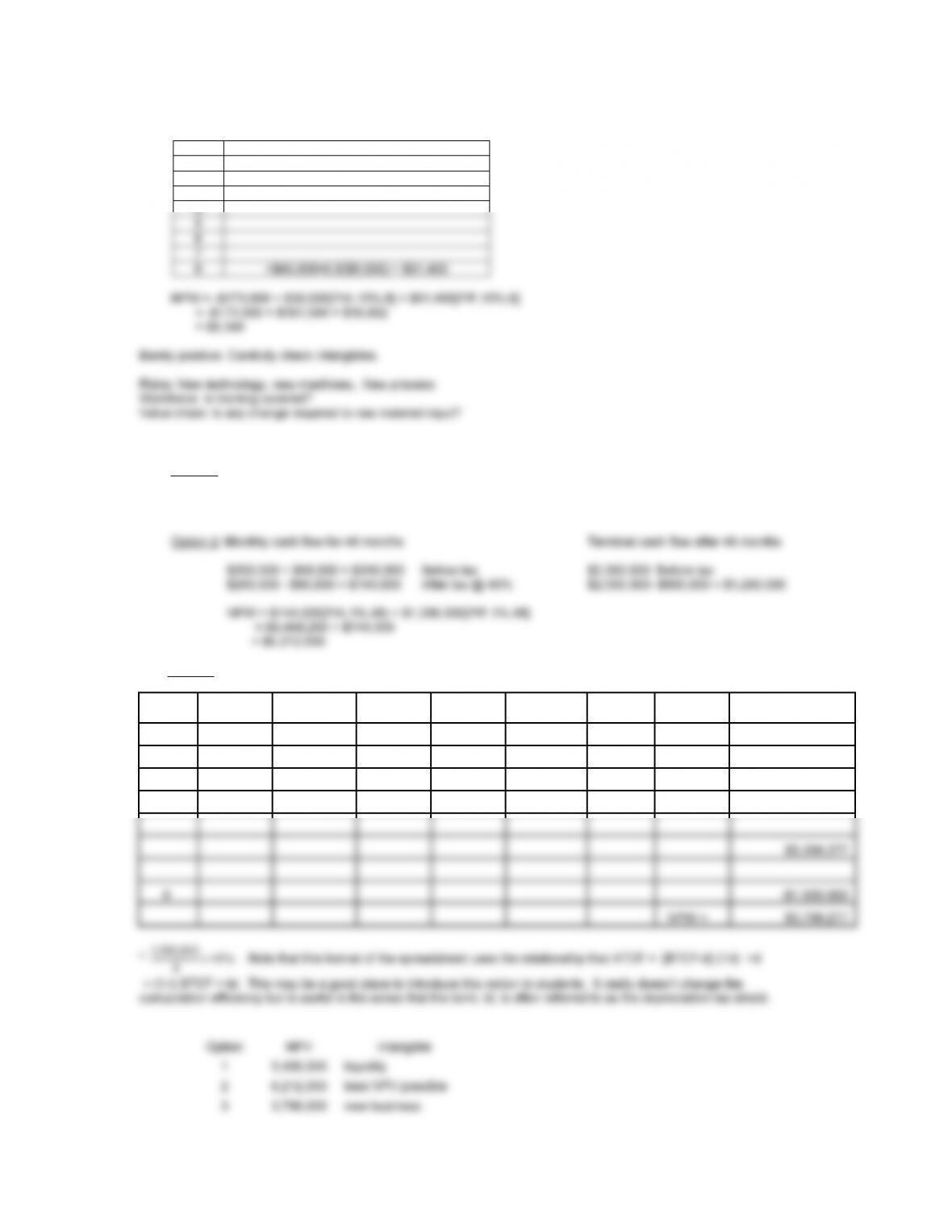

10-2. Starr Rental Revisited

Interest Rate 15.00%

Purchase

Price $ 500,000

Tax Rate 30.00%

5 8752 20 80% $140,026 $4,502 $135,524

5 $500,000

G H =F – G I=H x Tax rate J = H – I

K =F – I

=J+G

Taxable Net Operating After Tax

10-3. All $ In Thousands

Existing

Investment

Required New

Investment

Before tax

Worst Case Net

After Tax (for

problem 10-4)

10-4. Net After Tax Cash Flows in Thousands of $

10-5. Value Chain Factors + Stake holders impacted

Following are some examples of questions that should be asked and an example of an approximate analysis in

response to the last question

Questions are the same as those faced by Ajax for new product plus the need to test the following assumptions:

0 -$3360a

1

129

10-6.

0 -$165,000-$8000 = -$173,000

1 $50,000(1-0.4) + $15,000(0.4) = $36,000

2

3

10-7.

Option 1: Sell at $9,000,000

Taxable gain =$9,000,000

Tax on gain = 0.4($9,000,000) = $3,600,000

Net after Tax = $ 5,400,000

Option 3:

Year

Sales

Units Contribution Overhead BTCF (1-t) BTCF td*

After Tax

Salvage

After-Tax

Cash Flow

1 200,000 $1,800,000 $200,000 $1600000 $960000 $150000 1110000

2 300,000 2,700,000 200,000 2500000 1500000 150000 1650000

3 400,000 3,600,000 200,000 3400000 2040000 150000 2190000

4 100,000 900,000 200,000 700000 420000 150000 1800000 2370000

130

10-8.

Working

Capital

Net ATCF

or

10-9.

Year Sales Operating Depreciation Taxable Tax NOPAT ATCF

Working

Capital

Increase

Net ATCF

or

FCF

10-10.

Year Sales Operating Depreciation Taxable Tax NOPAT ATCF

Working

Capital

Increase

Net ATCF

or

FCF

10-11.

(a) All numbers in thousands

Rev CGS SGA CFBT D Tax ATCF ∆WC Capex ATNCF

0

(Ref) $2,000 $1,000 $200 $800 $200 $240 $560 -$24 -$180 $356

1 2,200 1,100 220 880 220 264 616 -26 -198 392

2 2,530 1,265 253 1,012 242 290 722 -29 -218 475

132

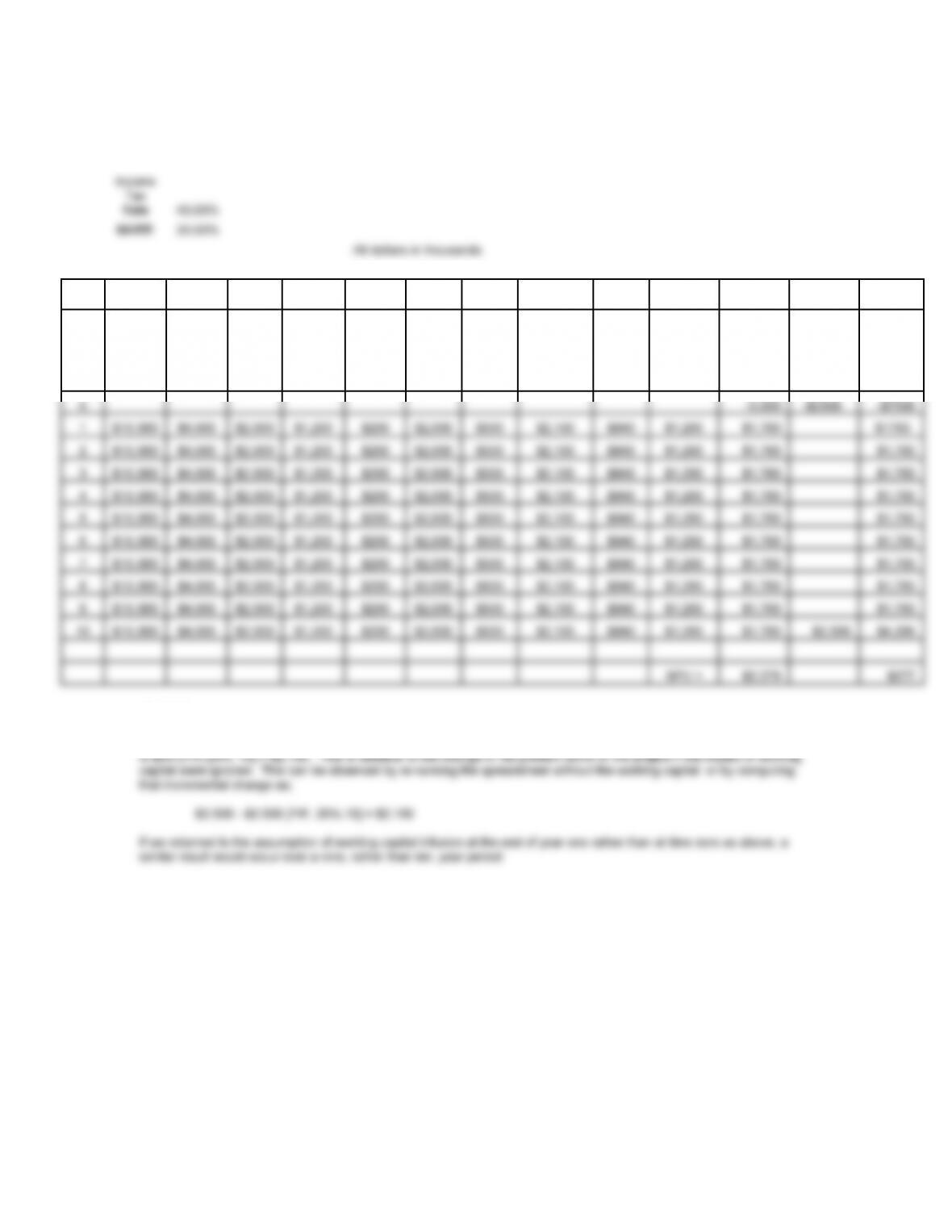

10-12.(a) The spreadsheet below is identical to example 10-3 in the text except that the timing of the working capital

infusion has been shifted from the end of year 1 to year 0 or immediately

A B C D E F

G = A-B-

C-D-E-F

H =

.4G I= G – H J = I + F K

L = J +

K

Year

Sales

Material

Labor

Variable

OH

Plant

Costs

BTCF

Depre.

Taxable

Income

Taxes

NOPAT

After Tax

Cash

Flow

Change

in

working

capital

Net

cash

Flow

10-12 (b)

Interest on the $2506 invested at time 0, is 20% of $2506 = $501 per year for 10 years. The Present worth of this interest

133

10-12 (c)

All dollars in thousands

A B C D E F

G = A-B-

C-D-E-F

H =

.4G I= G – H J = I + F K

L = J +

K

Year

Sales

Material

Labor

Variable

OH

Plant

Costs

BTCF

Depre.

Taxable

Income

Taxes

NOPAT

After Tax

Cash

Flow

Change

in

working

capital

Net

cash

Flow

0 -5,000 0 -$5000

1 $10,000 $4,000 $2,000 $1,200 $200 $2,600 $500 $2,100 $840 $1,260 $1,760 -$2,506 $746

2 $10,000 $4,000 $2,000 $1,200 $200 $2,600 $500 $2,100 $840 $1,260 $1,760 $1,760

10-12 (d)

The assumptions which make the most sense should be determined on a case by case basis. However, the most realistic

ones would involve an end-of-year assumption, rather than a time 0 assumption, for working capital infusion. This is

134