overpayment for EDS, HP announced in August 2012 that it would take an accounting charge of $8 billion related to

its EDS acquisition four years earlier. The write down amounted to a staggering 58% of what the firm had paid for

EDS.

What went wrong? Was it due to poor planning, a bad strategy, or poor execution? Probably each had a role.

important tool supplementing but not replacing executive judgment.

Mars Buys Wrigley in One Sweet Deal

Under considerable profit pressure from escalating commodity prices and eroding market share, Wrigley

Corporation, a U.S.-based leader in gum and confectionery products, faced increasing competition from Cadbury

Schweppes in the U.S. gum market. Wrigley had been losing market share to Cadbury since 2006. Mars

Corporation, a privately owned candy company with annual global sales of $22 billion, sensed an opportunity to

achieve sales, marketing, and distribution synergies by acquiring Wrigley Corporation.

worldwide. The merger of the two family–controlled firms represents a strategic blow to competitor Cadbury

Schweppes’s efforts to continue as the market leader in the global confectionary market with its gum and chocolate

business. Prior to the announcement, Cadbury had a 10 percent worldwide market share.

As of the September 28, 2008 closing date, Wrigley became a separate stand–alone subsidiary of Mars, with $5.4

billion in sales. The deal is expected to help Wrigley augment its sales, marketing, and distribution capabilities. To

categories: chocolate, nonchocolate confectionary, gum, food, drinks, and pet care products. While there is little

product overlap between the two firms, there is considerable geographic overlap. Mars is located in 100 countries,

while Wrigley relies heavily on independent distributors in its growing international distribution network.

Furthermore, the two firms have extensive sales forces, often covering the same set of customers.

While mergers among competitors are not unusual, the deal’s highly leveraged financial structure is atypical of

Hathaway, a nontraditional source of high-yield financing. Historically, such financing would have been provided

by investment banks or hedge funds and subsequently repackaged into securities and sold to long-term investors,

such as pension funds, insurance companies, and foreign investors. However, the meltdown in the global credit

markets in 2008 forced investment banks and hedge funds to withdraw from the high-yield market in an effort to

strengthen their balance sheets. Berkshire Hathaway completed the financing of the purchase price by providing

$2.1 billion in equity financing for a 9.1 percent ownership stake in Wrigley.

Discussion Questions:

1. Why was market share in the confectionery business an important factor in Mars’ decision to acquire

Wrigley?

Answer: Firm’s having substantial market relative to their next largest competitor are likely to have lower

2. It what way did the acquisition of Wrigley’s represent a strategic blow to Cadbury?

3. How might the additional product and geographic diversity achieved by combining Mars and Wrigley

benefit the combined firms?

4. Speculate as to the potential sources of synergy associated with the deal. Based on this speculation what

additional information would you want to know in order to determine the potential value of this synergy?

Answer: The product offerings of the two firms show little duplication. Therefore, there is significant

potential for cross-selling each firm’s products into the other’s customers. This would require training the

sales forces in each firm’s product offering. The cost of this training would need to be estimated and

deducted from cash flows generated by cross-selling.

5. Given the terms of the agreement, Wrigley shareholders would own what percent of the combined

companies? Explain your answer

Tribune Company Acquires the Times Mirror Corporation

in a Tale of Corporate Intrigue

Background: Oh, What Tangled Webs We Weave. .

.

CEO Mark Willes had reason to be optimistic about the future. Operating profits had grown at a double–digit rate,

and earnings per share had grown at a 55% annual rate between 1995 to 1999. Many shareholders appeared to be

satisfied. However, some were not. Although pleased with the improvement in profitability, they were concerned

about the long-term growth prospects of the firm. Reflecting this disenchantment, Times Mirror’s largest

shareholder, the Chandler family, was contemplating the sale of the company and along with it the crown jewel Los

with the Tribune.

Following months of secret negotiations, the Chicago-based Tribune Company and the Times Mirror Corporation

announced a merger of the two companies in a cash and stock deal valued at approximately $7.2 billion, including

$5.7 billion in equity and $1.5 billion in assumed debt. The transaction, announced March 13, 2000, created a media

giant that has national reach and a major presence in 18 of the nation’s top 30 U.S. markets, including New York,

Los Angeles, and Chicago. The combined company has 22 television stations, four radio stations, and 11 daily

newspapers—including the Los Angeles Times, the nation’s largest metropolitan daily newspaper and flagship of the

Times Mirror chain.

Transaction Terms: Tribune Shareholders Get Choice of Cash or Stock

The Tribune agreed to buy 48% of the outstanding Times Mirror stock, about 28 million shares, through a tender

offer. After completion of the tender offer, each remaining Times Mirror share would be exchanged for 2.5 shares of

Tribune stock. Under the terms of the transaction, Times Mirror shareholders could elect to receive $95 in cash or

(Table 1).

Table 1. Times Mirror Transaction Terms

As of June 12, 2000 Transaction Value

Times Mirror Shares Outstanding @ 3/13/00 59,700,000

No. of Times Mirror Shares Exchanged for 2.3

Shares of Tribune Stock 27,238,253 $2,587,634,0351

Times Mirror Shares Outstanding after Tender Offer 21,813,429

No. of New Tribune Shares Issued for Remaining

Times Mirror Shares 54,533,5735 $2,072,275,7743

Equity Value of Offer $5,671,446,777

127,238,253 2.5 $38/share of Tribune stock.

2$41.70 in cash + 1.4025 shares of Tribune stock $38 per share for each Times Mirror share remaining

10,648,318.

3Equals 2.5 shares 21,813,429 $38 per Tribune share.

4Times Mirror share price on announcement date of $47 times 59,700,000.

5The total number of new Tribute shares issued equals 27,238,318 2.5 + 10,648,318 2.5 + 54,533, 573 or

137,537,013.

Newspaper Advertising Revenues Continue to Shrink

Most U.S. newspapers are mired in the mature or declining phase of their product life cycle. For the past half-

century, newspapers have watched their portion of the advertising market shrink because of increased competition

2000).

Tribune Company Profile: The Face of New Media?

Unlike the Times Mirror, Tribune has built its strategy around four business groups: broadcasting, publishing,

education, and interactive. The Tribune is also an equity investor in America Online and other leading internet

Financial Analysis

The present values of the Tribune, Times Mirror, and the combined firms are $8.5 billion, $2.4 billion, and $16.5

billion, respectively; the estimated present value of synergy is $5.6 billion (Table 3). This assumes that pretax cost

savings are phased in as follows: $25 million in 2000, $100 million in 2001, and $200 million thereafter. The cost

Table 2. Annual Merger-Related Cost Savings

Total Annual Savings $200,000,000

1Assumes Tribune will close overlapping bureaus in United States (9) and most of the Times Mirror’s foreign

bureaus (21 abroad).

2As a result of bulk purchasing and more favorable terms with different suppliers, 15% of the newsprint expense of

the combined companies is expected to be saved.

3Layoffs of 120 L.A. Times Mirror Corporate Office personnel at an average salary of $125,000 and benefits equal

to 30% of base salaries. Total payroll expenses equal $19,500,000 (i.e., $125,000 1.3 120). Lease, travel and

entertainment, and other support expenses added another $14.5 million.

Source: Moore, Kathryn, Tim Schnabel, and Mark Yemma, “A Media Marriage,” paper prepared for Chapman

University, EMBA 696, May 18, 2000, p. 9.

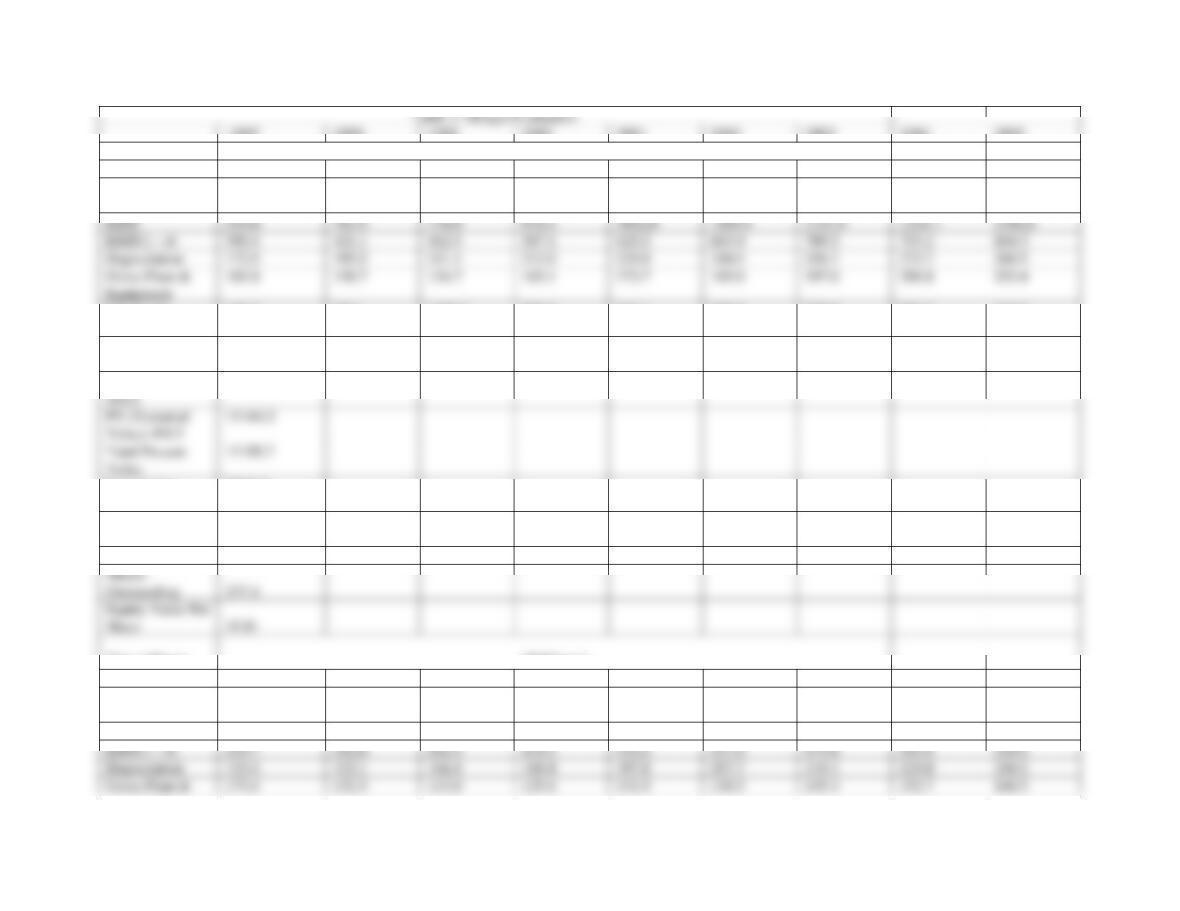

Table 3. Merger Evaluation

1997

1998

1999

2000

2001

2002

2003

2004

2005

Tribune

($ Millions)

Sales

2891.5

2980.9

3221.9

3261.5

3473.5

3699.3

3939.7

4195.8

4468.5

Operating

Expenses

2232.5

2279.0

2451.0

2283.1

2431.4

2589.5

2757.8

2937.1

3128.0

EBIT

559.0

701.9

770.9

978.5

1042.0

1109.8

1181.9

1258.7

1340.6

EBIT(1 – t)

395.4

421.1

462.5

587.1

625.2

665.9

709.2

755.2

804.3

Depreciation

172.5

195.5

221.1

212.0

225.8

240.5

256.1

272.7

290.5

Equipment

Change in

Working Capital

147.7

49.0

1107.0

260.9

243.1

258.9

275.8

293.7

312.8

Free Cash Flow

to Firm

511.8

427.9

-558.1

375.1

434.2

462.4

492.5

524.5

558.6

PV (2001–2005)

@8.5

51.5

PV (Terminal

Value) @8.5

11144.2

Less: Long-

Term Debt

2694.2

Plus: Excess

Cash Balances

0

Equity Value

8501.5

Shares

Outstanding

237.4

Equity Value Per

Share

35.81

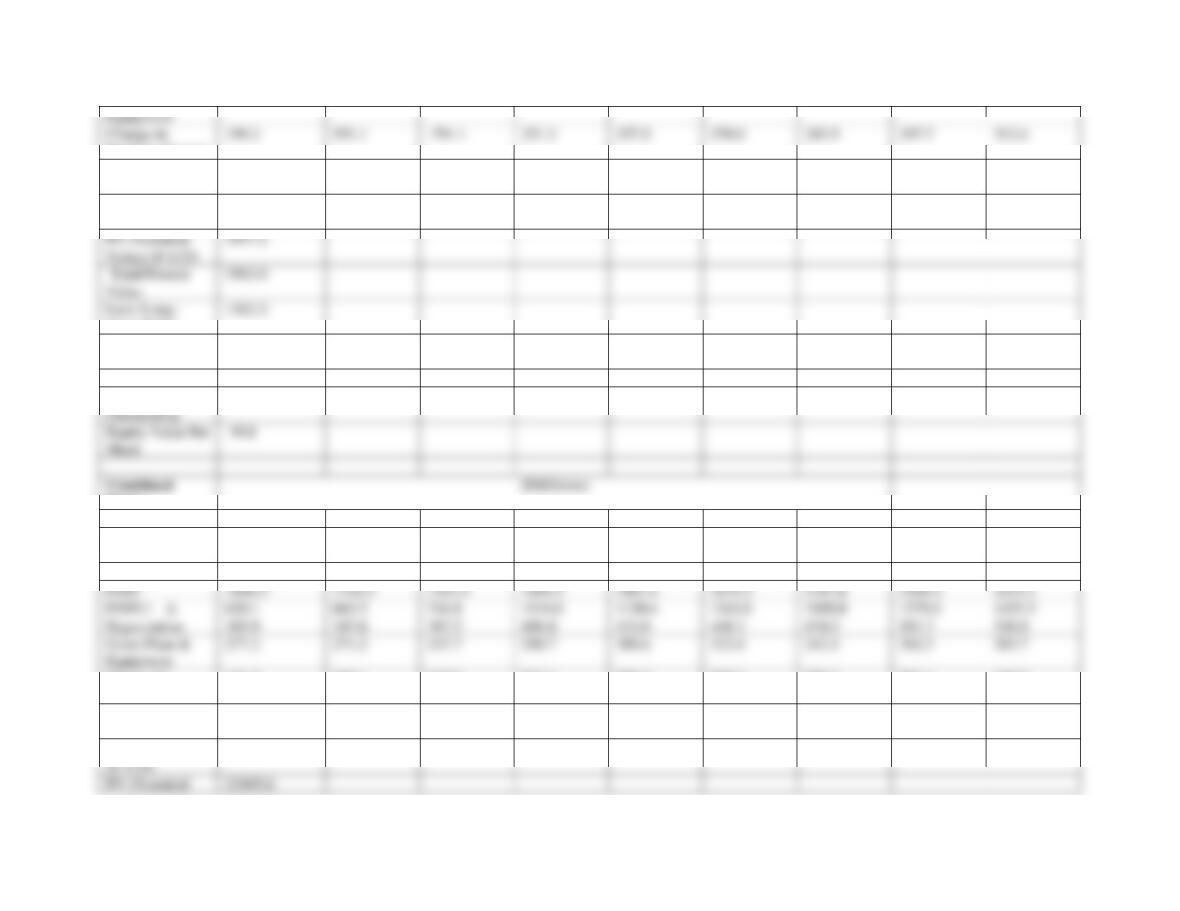

Times Mirror

($Millions)

Sales

2728.2

2783.9

3029.2

3140.0

3297.0

3461.9

3634.9

3816.7

4007.5

Operating

Expenses

2337.0

2380.5

2558.7

2449.2

2571.7

2700.2

2835.3

2977.0

3125.9

EBIT

391.2

403.4

470.5

690.8

725.3

761.6

799.7

839.7

881.7

EBIT(1 – t)

234.7

242.0

282.3

414.5

435.2

457.0

479.8

503.8

529.0

Depreciation

133.4

152.1

166.4

188.4

197.8

207.7

218.1

229.0

240.5

Gross Plant &

173.4

131.5

113.0

125.6

131.9

138.5

145.4

152.7

160.3

Equipment

Working Capital

Change in

199.2

551.1

-791.1

251.2

257.2

270.0

283.5

297.7

312.6

Free Cash Flow

to Firm

-4.5

-288.5

1126.8

226.1

244.0

256.2

269.0

282.4

296.6

PV (2001–2005)

@ 9.5%

25.8

PV (Terminal

Value) @ 9.5%

Value

Less: Long-

1562.2

3937.2

Term Debt1

Plus: Excess

Cash Balances

0

Equity Value

2375.0

Shares

Outstanding

59.7

Equity Value Per

Share

39.8

Firms

Sales

5619.7

5764.8

6251.1

6401.5

6770.5

7161.1

7574.7

8012.5

8476.1

Operating

Expenses

4569.5

4659.5

5009.7

4732.3

5003.1

5289.7

5593.1

5914.1

6253.8

Synergy

25.0

100.0

200.0

200.0

200.0

200.0

EBIT

1050.2

1105.3

1241.4

1694.3

1867.4

2071.4

2181.6

2298.4

2422.2

EBIT(1 – t)

630.1

663.2

744.8

1016.6

1120.4

1242.8

1309.0

1379.0

1453.3

Depreciation

305.9

347.6

387.5

400.4

423.6

448.2

474.2

501.7

530.9

Change in

Working Capital

151.5

600.1

315.9

512.1

500.3

529.0

559.3

591.4

625.4

Free Cash Flow

to Firm

507.3

139.5

568.7

616.2

738.2

838.6

881.5

926.9

975.1

PV (2001–2005)

@ 9.5%

88.1

PV (Terminal

22805.6

Value) @ 9.5%

22893.8

Less: Long-

4256.4

Term Debt

Less:

Acquisition-

Related Debt

2193.7

Plus: Excess

Cash Balances

0

Equity Value

16443.7

Equity Value Per

Share

43.9

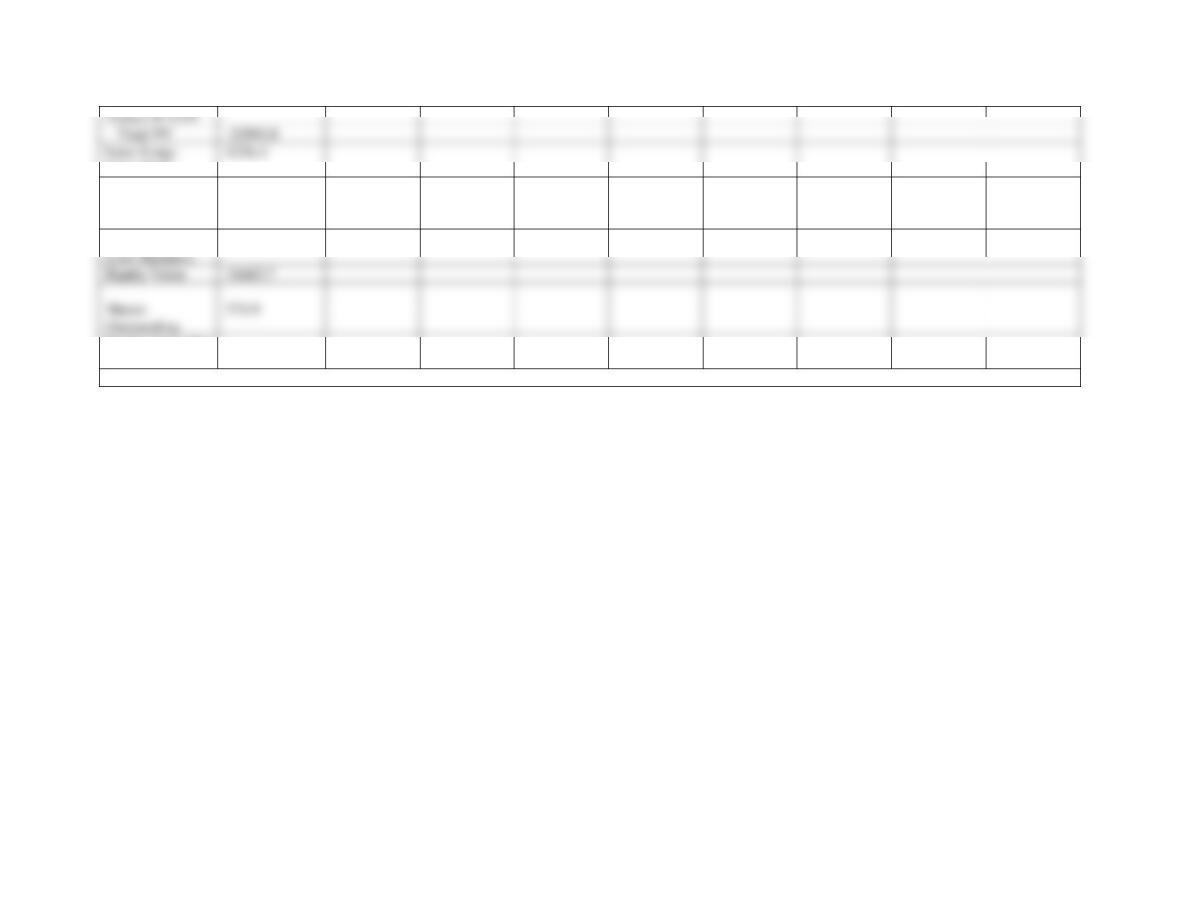

1Book values for long-term debt may be used if the coupon rate on the debt approximates competitive market rates.

Table 4. Offer Price Determination

Tribune

Times Mirror

Combined Incl.

Synergy

Value of Synergy

Equity Valuations

8501.5

2375.0

16443.7

5567.3

Minimum Offer

Price1

2805.9

Maximum Offer

Price

Actual Offer Price

5671.4

% Maximum Offer

Price

67.7%

Premium

New Tribune Shares

Ownership

Distribution

8373.2

TM Shareholders

0.37

Tribune

Shareholders

0.63

1Market value of Times Mirror on the merger announcement date.

Epilogue

Only time will tell if actual returns to shareholders in the combined Tribune and Times Mirror company exceed the

expected financial returns provided in the valuation models in this case study. Times Mirror shareholders earned a

substantial 102% purchase price premium over the value of their shares on the day the merger was announced. Some

portion of those undoubtedly “cashed out” of their investment following receipt of the new Tribune shares.

However, for those former Times Mirror shareholders continuing to hold their Tribune stock and for Tribune

shareholders of record on the day the transaction closed, it is unclear if the transaction made good economic sense.

Discussion Questions:

1. In your judgment, did it make good strategic sense to combine the Tribune and Times Mirror?

corporations? Why? / Why not?

Yes, the combination of the two firms offers substantial cost savings in closing overlapping news bureaus

2. Using the Merger Evaluation table given in the case, determine the estimated equity values of Tribune,

Times Mirror and the combined firms. Why is long-term debt deducted from the total present value

estimates in order to obtain equity value?

3. Despite the merger having closed in mid-2000, the full effects of synergy are not expected until 2002.

Why? What factors could account for the delay?

The full effects of synergy are not realized immediately because of bureau leases that must expire or be

4. The estimated equity value for the Times Mirror Corporation on the day the merger was announced was

about $2.8 billion. Moreover, as shown in the offer price evaluation table, the equity value estimated using

discounted cash flow analysis is given has $2.4 billion. Why is the minimum offer price shown as $2.8

billion rather than the lower $2.4 billion figure? How is the maximum offer price determined in the Offer

Price Evaluation Table? How much of the estimated synergy value generated by combining the two

businesses is being transferred to the Times Mirror shareholders? Why?

5. Does the Times Mirror-Tribune Corporation merger create value? If so, how much? What percentage of

this value goes to Times Mirror shareholders and what percentage to Tribune shareholders? Why?

Ford Acquires Volvo’s Passenger Car Operations

This case illustrates how the dynamically changing worldwide automotive market is spurring a move toward

consolidation among automotive manufacturers. The Volvo financials used in the valuation are for illustration

only— they include revenue and costs for all of the firm’s product lines. For purposes of exposition, we shall

assume that Ford’s acquisition strategy with respect to Volvo was to acquire all of Volvo’s operations and later to

divest all but the passenger car and possibly the truck operations. Note that synergy in this business case is

determined by valuing projected cash flows generated by combining the Ford and Volvo businesses rather than by

subtracting the standalone values for the Ford and Volvo passenger car operations from their combined value

including the effects of synergy. This was done because of the difficulty in obtaining sufficient data on the Ford

passenger car operations.

$3 billion, companies were finding mergers and joint ventures an attractive means to distribute risk and maintain

market share in this highly competitive environment.

By acquiring Volvo, Ford hoped to expand its 10% worldwide market share with a broader line of near-luxury

Volvo sedans and station wagons as well as to strengthen its presence in Europe. Ford saw Volvo as a means of

improving its product weaknesses, expanding distribution channels, entering new markets, reducing development

size.

Historical and Projected Data

The initial review of Volvo’s historical data suggests that cash flow is highly volatile. However, by removing

nonrecurring events, it is apparent that Volvo’s cash flow is steadily trending downward from its high in 1997. Table

9-10 displays a common-sized, normalized income statement, balance sheet, and cash–flow statement for Volvo,

including both the historical period from 1993 through 1999 and a forecast period from 2000 through 2004.

Although Volvo has managed to stabilize its cost of goods sold as a percentage of net sales, operating expenses as a

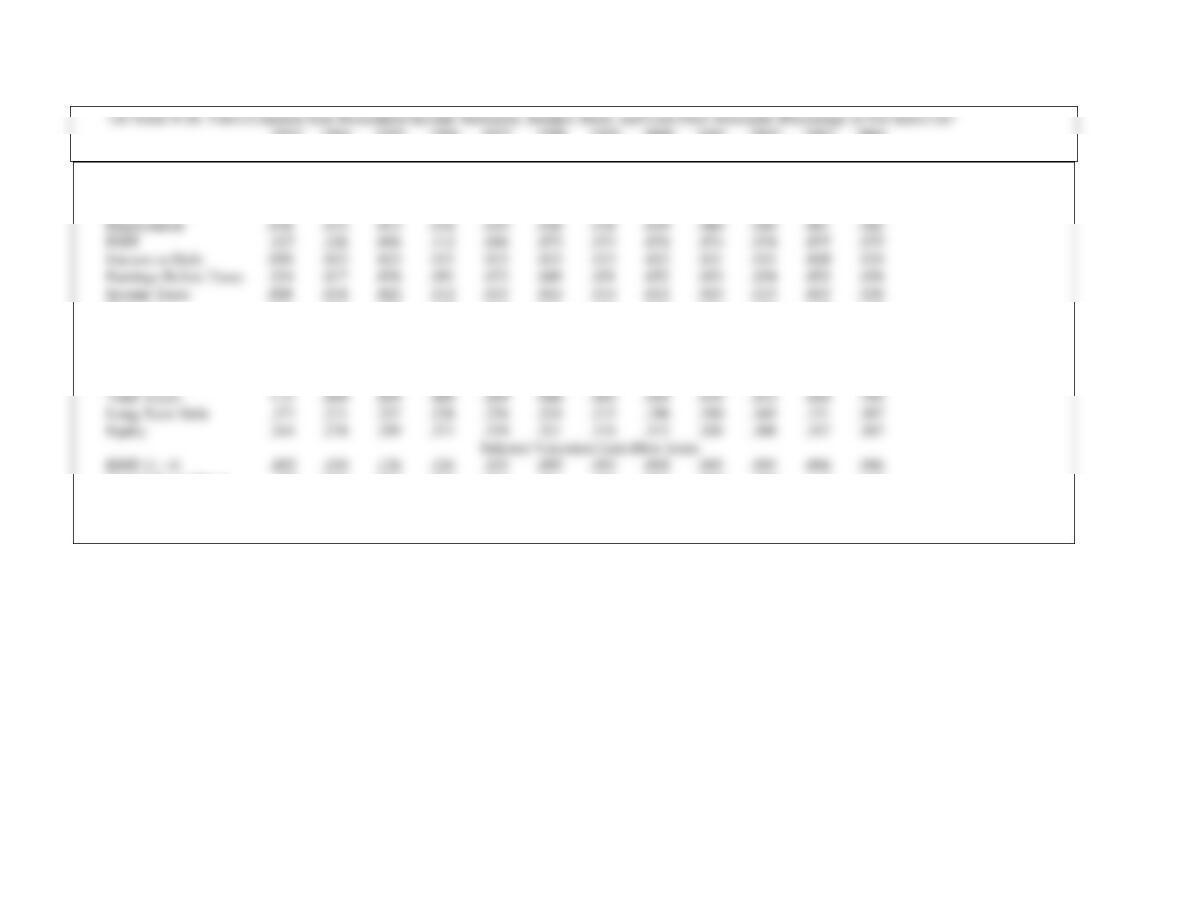

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Income Statement

Net Sales 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Cost of Goods Sold .772 .738 .749 .777 .757 .757 .757 .757 .757 .757 .757 .757

Operation Expense .167 .101 .120 .077 .119 .133 .132 .131 .129 .128 .127 .126

Net Income .028 .087 .054 .079 .057 .035 .036 .037 .038 .039 .040 .040

Balance Sheet

Current Assets .632 .503 .444 .524 .497 .500 .500 .500 .500 .500 .500 .500

Current Liabilities .596 .400 .283 .298 .304 .350 .350 .350 .350 .350 .350 .350

Working Capital .036 .103 .161 .226 .192 .150 .150 .150 .150 .150 .150 .150

Capital Expenditures .031 .027 .033 .053 .054 .061 .069 .078 .088 .099 .112 .126

Working Capital .025 .077 .068 .049 .000 .017 .020 .020 .020 .020 .020 .020

Free Cash Flow .047 .079 .053 .059 .088 .087 .044 .036 .027 .017 .005 (.008)

to the Firm (FCFF)

Determining the Initial Offer Price

reflecting only about one-fourth of the total potential synergy resulting from combining the two businesses. Other valuation

methodologies tended to confirm this purchase price estimate. The market value of Volvo was $11.9 billion on January 29, 1999. To

gain a controlling interest, Ford had to pay a premium to the market value on January 29, 1999. Applying the 26% premium Ford paid

for Jaguar, the estimated purchase price including the premium is $15 billion, or $34 per share. This compares to $34.50 per share

estimated by dividing the initial offer price of $15.25 billion by Volvo’s total common shares outstanding of 442 million.

return, including the effects of synergy, exceeds the cost of capital. Moreover, by using this excess cash, Ford also is making itself less

attractive as a potential acquisition target. The acquisition is expected to increase Ford’s EPS. The loss of interest earnings on the

excess cash balances would be more than offset by the addition of Volvo’s pretax earnings.

Epilogue

Seven months after the megamerger between Chrysler and Daimler-Benz in 1998, Ford Motor Company announced that it was

Discussion Questions and Answers:

1. What is the purpose of the common–size financial statements developed for Volvo (see Table 8–8 in the textbook)? What

insights does this table provide about the historical trend in Volvo’s historical performance? Based on past performance,

how realistic do you think the projections are for 2000–2004?

Answer: The common size financial statements for Volvo reveal the historical relationship between key operating variables

2. Ford anticipates substantial synergies from acquiring Volvo. What are these potential synergies? As a consultant hired to

value Volvo, what additional information would you need to estimate the value of potential synergy from each of these areas?

Answer: By acquiring Volvo, Ford hoped to expand its global market share with a broader product offering as well as to

3. How was the initial offer price determined according to this case study? Do you find the logic underlying the initial offer

price compelling? Explain your answer.

4. What was the composition of the purchase price? Why was this composition selected according to this case study?