18

6. What are the key valuation assumptions underlying this valuation of St. Jude Medical? Be specific.

Answer: With respect to the standalone valuation, it is assumed that both the valuation multiples are appropriate and that the

7. What is the maximum amount Abbott Labs could have paid for St. Jude’s Medical and still earned its cost of capital? Did Abbott

overpay for St. Jude? Explain your answer.

VALUING THE TWITTER IPO

Case Study Objectives: To Illustrate

• Valuation is far more an art than a science.

• Understanding the limitations of individual valuation methods is critical.

• Averaging multiple valuation methods is often the most reliable means of valuing a firm.

• The credibility of any valuation ultimately rests on the credibility of its key underlying assumptions.

In the now infamous “dotcom” era, firms like Yahoo, Lycos, Excite and others evolved into portals in a desperate attempt to find ways to

make money from providing users the ability to search the web. Enter Google and the competitive landscape changed quickly. Google

invented the concept of paid search and contextual, pay–to-click advertising models.

Today, social networks like Twitter and Facebook, while attracting new users at an astonishing pace, have not fully defined their

business models. In fact, the eventual winners in the social networking space may not even exist today. Nonetheless, investor expectations

for the growth potential of social networking firms remained very optimistic during 2013. This investor enthusiasm prompted Twitter’s

financial backers and founders to take the firm public late in 2013, at a time when the firm’s valuation was likely to be high.

Per the IPO prospectus, Twitter’s projected revenue from advertising in 2013 was $600 million based on what Twitter call “promoted

Tweets.” Revenue projections for 2014 were $1 billion. Using this information, investors in anticipation of the November 6, 2013 IPO

turned to estimating the market value of Twitter based on comparable publicly traded firms. Firms believed to be similar to Twitter were

those in the social networking space and which seemed to display similar growth, risk and profitability characteristics. As is often the

case, there were no firms that were both publicly traded and truly similar in size, product offering, and which satisfied the same customer

needs. Investors used valuation multiples for Facebook, LinkedIn, and Yelp as Twitter’s foremost peers.

19

Without detailed financial statements, investors groped for rudimentary valuation estimates based simply on revenue, the easiest metric

to find. Just prior to the IPO, Facebook traded at 18 times estimated 2013 sales. LinkedIn and Yelp traded for about 22 and 23 times

estimated 2013 sales, respectively. Multiples of projected 2014 revenue just prior to the Twitter IPO were 11, 14, and 13 times revenue

for 2014. Yelp, with a negative EBITDA for 2013, did not have a meaningful enterprise to EBITDA ratio. Twitter’s estimated EBITDA

for 2013 was $230 million and $260 million in 2014.

These valuation multiples implied a very high valuation (market capitalization) and price per share for the IPO. But investors remained

cautious, as valuation estimates too often prove wrong. For every successful IPO like LinkedIn, there is a Groupon or Zynga that were

duds. Groupon, the provider of online discount coupons, went public in November 2011 at $20 per share. After accounting

investigations, slowing growth and a CEO firing, its shares traded at $11.50 at the time of the Twitter IPO. Online game maker Zynga,

modest 240 million.

Investors also had reason to question how similar Twitter actually was to its presumed peers. For example, the differences between

Twitter and Facebook are enormous in that they purport to satisfy substantially different user needs. Twitter is focused and simple while

Facebook offers users a portal interface. Facebook appeals to people looking to reconnect with friends and family or find new friends

online and offers email, instant messaging, image and video sharing. Most people can grasp how to use Facebook quickly. In contrast, the

shares outstanding. The basic share count excludes options, warrants, and restricted stock. Altogether, Twitter has 150 million such shares

according to the IPO filing bringing the total share count to 705 million. Failure to include these shares can result in investors ignoring

their impact on dilution of EPS and ownership stake. Such investors pay more than they should.

Another adjustment must be made in calculating fully diluted shares outstanding for options and warrants. When options and warrants

are exercised by their holders, Twitter received cash equal to the number of options multiplied by their weighted average exercise price.

Using fully diluted shares outstanding, the multiple rises to 31.6 times (i.e., $31.6 billion in market value/$1 billion in revenue). That gap

should close over time since firms like Twitter tend to issue fewer options and restricted stock following the IPO.

Discussion Questions

1. Based on the information given in the case, how would you estimate the value of Twitter at the time of the IPO based on a simple

average of comparable firm revenue multiples based on projected 2014 revenue?

2. Based on the information given in the case, how would you estimate the value of Twitter at the time of the IPO based on a simple

average of comparable firm enterprise to EBITDA multiples based on projected 2014 EBITDA?

3. The valuation estimates in the preceding two questions are substantially different. What are the key assumptions underlying each

valuation method? Be specific. How can an analyst combine the two valuation estimates assuming she believes that the enterprise to

EBITDA ratio is twice as reliable as the valuation based on a revenue multiple?

Answer: Relative valuation methods assume that the peer firms selected to compute the valuation multiple are substantially similar to

the target firm at a moment in time. These multiples in turn reflect investor assumptions about continued user growth and the ability

4. Scenario analysis involves valuing businesses based on different sets assumptions about the future. What are the advantages and

disadvantages of applying this methodology in determining an appropriate purchase price using relative valuation methods to

estimate firm value?

China’s CNOOC Acquires Canadian Oil and Gas Producer Nexen Inc.

______________________________________________________________

Key Points

• DCF valuation assumes implicitly that management has little decision-making flexibility once an investment decision is made.

• In practice, management may accelerate, delay, or abandon the original investment as new information is obtained.

_____________________________________________________________________________

In its largest foreign takeover ever, China’s state owned energy company CNOOC acquired Canadian oil and gas company Nexen Inc. in

2013 for $15.1 billion. The acquisition gives CNOOC new offshore production in the North Sea, the Gulf of Mexico, offshore of western

Africa, and oil and gas properties in the Middle East and Canada. The deal also gives CNOOC control of major oil sands reserves in

Canada.

export to China. Continued opposition to further development of these properties could reduce their value significantly. Given these

uncertainties what options does CNOOC have with respect to these reserves?

Standard discounted cash flow analysis assumes implicitly that once CNOOC made this investment decision to buy Nexen, CNOOC’s

management could do little to alter the investment stream it had included in the calculation of future cash flows used to value Nexen. In

reality, management has a series of so-called real options enabling changes to be made to their original investment decisions. Which

option would be pursued was contingent on certain future developments. These options include the decision to expand (i.e., accelerate

investment), delay investment, or abandon an investment.

Is Texas Instruments Overpaying for National Semiconductor? As Always, It depends.

Key Points

Valuation is far more an art than a science, and understanding the limitations of individual valuation methods is critical.

Averaging multiple valuation methods is often the most reliable means of valuing a firm.

Evaluating success of an individual acquisition is best viewed in the context of an acquirer’s overall business strategy.

Value is in the eye of the beholder. Various indicators often provide a wide range of estimates. No single method seems to provide

consistently accurate valuation estimates. Which method the analyst ultimately selects often depends on the availability of data and on the

analyst’s own biases. Whether a specific acquisition should be viewed as successful depends on the extent to which it helps the acquirer

realize a successful business strategy.

2.25% immediately following the announcement. While it is normal for the target’s share price to rise sharply to reflect the magnitude of

the premium, the acquirer’s share price sometimes remains unchanged or even declines. The increase in TI’s share price seems to suggest

agreement among investors that the acquisition made sense. However, within days, analysts began to ask the question that bedevils so

many takeovers. Did Texas Instruments overpay for National Semiconductor?

22

growth rate of earnings. At 1.28 prior to the TI takeover, NS was trading at a premium to its growth rate according to this measure. After

the acquisition, the PEG ratio jumped to 2.09.

While suggesting strongly that TI overpaid, these measures may be seriously biased. A large percentage of TI’s and NS’s revenue

comes from the production and sale of analog chips, a rapidly growing segment of the semiconductor industry. Part of the growth in

analog chips is expected to come from the explosive growth of smartphones and tablets, where their use in regulating electricity

consumption is crucial to longer battery life. Consequently, many of the previous acquisitions in the semiconductor industry are of firms

relatively rare. Finally, in the highly fragmented semiconductor industry, consolidation among competitors may lead to higher average

selling prices than would have been realized otherwise.

The acquisition of NS by TI should be viewed in the context of a longer-term strategy in which TI is seeking an ever-increasing share

of the $42 billion analog chip market, which many analysts expect to outgrow the overall semiconductor market during the next three to

five years. Following the financial crisis in 2008, TI acquired analog chip manufacturing facilities at “fire–sale” prices to boost the firm’s

capacity. The NS acquisition will give TI a 17% share of this rapidly growing market segment.

Discussion Questions

1. Most studies purporting to measure the success or failure of acquisitions base their findings of the performance of acquiring

share prices around the announcement date of the acquisition or on accounting performance measures during the three to

five years following the acquisition. This requires that acquisitions be evaluated on a “standalone” basis. Do you agree or

disagree with this methodology? Explain your answer.

Answer: While event studies have merit to the extent markets are efficient, they often fail to recognize that acquisitions

usually are undertaken as part of a larger strategy. If the acquisition enables the implementation of the larger strategy and

that strategy makes sense, then the success of the acquisition should be considered in the context of the larger strategy. This

2. Despite their limitations, why is the judicious application of the various valuation methods critical to the acquirer in

determining an appropriate purchase price?

Answer: Individual valuation methods routinely provide significantly different valuations because they are estimated using

substantially different approaches, with some incorporating both the risk and timing of future cash flows (i.e., DCF) and

others reflecting investor sentiment at a moment in time (i.e., relative valuation). Nevertheless, depending on the availability

of data, multiple methods should be employed and then averaged to provide a reality check to limit the tendency for the

3. Scenario analysis involves valuing businesses based of different sets assumptions about the future. What are the advantages

and disadvantages of applying this methodology in determining an appropriate purchase price?

Answer: Scenario analyses require a range of estimates based on alternative sets of assumptions. The offer price is then

based on the expected value of the estimates associated with the scenarios. This methodology is prone to generate a more

4. Do you agree or disagree with the following statement: Valuation is more an art than a science. Explain your answer.

Answer: The scientific method requires that repetition of the same experiment will result in an identical outcome. It is clear

from the variation of estimates derived from the various methods reflecting different time periods and data limitations that

Bristol-Myers Squibb Places a Big Bet on Inhibitex

___________________________________________________________

Key Points

DCF valuation assumes implicitly that management has little decision–making flexibility once an investment decision is made.

In practice, management may accelerate, delay, or abandon the original investment as new information is obtained.

______________________________________________________________________________________________________________

Pharmaceutical firms in the United States are facing major revenue declines during the next several years because of patent expirations for

many drugs that account for a substantial portion of their annual revenue. The loss of patent protection will enable generic drug makers to

sell similar drugs at much lower prices, thereby depressing selling prices for such drugs across the industry. In response, major

pharmaceutical firms are inclined to buy smaller drug development companies whose research and developments efforts show promise in

order to offset the expected decline in their future revenues as some “blockbuster” drugs lose patent protection.

Aware that its top-selling blood thinner, Plavix, would lose patent protection in May 2012, Bristol-Myers Squibb (Bristol-Myers)

operating loss of $22.7 million in 2011. The lofty purchase price reflected Bristol–Myers’ growth expectations for the firm’s hepatitis C

treatment INX-189, based on very early phase one clinical testing trials, with larger trials scheduled for 2013. The all–cash deal for $26

per share represented a 164% premium to Inhibitex’s closing price on January 10, 2012.

Bristol-Myers valued Inhibitex in terms of the expected cash flows resulting from the commercialization of hepatitis C treatment INX–

189. Standard discounted cash flow analysis assumes implicitly that once Bristol-Myers makes an investment decision, it cannot change

24

These options include the decision to expand (i.e., accelerate investment at a later date), delay the initial investment, or abandon an

Google Buys YouTube: Valuing a Firm Without Cash Flows

YouTube ranks as one of the most heavily utilized sites on the Internet, with one billion views per day, 20 hours of new video uploaded

every minute, and 300 million users worldwide. Despite the explosion in usage, Google continues to struggle to “monetize” the traffic on

the site five years after having acquired the video sharing business. 2010 marked the first time the business turned marginally profitable.

Whether the transaction is viewed as successful depends on whether it is evaluated on a stand-alone basis or as part of a larger strategy

designed to steer additional traffic to Google sites and promote the brand.

This case study illustrates how a value driver approach to valuation could have been used by Google to estimate the potential value of

YouTube by collecting publicly available data for a comparable business. Note the importance of clearly identifying key assumptions

$9 billion in cash, and a net profit margin of about 25 percent, Google was in remarkable financial health for a firm growing so rapidly.

The acquisition was by far the most expensive acquisition by Google in its relatively short eight-year history. In 2005, Google spent

$130.5 million in acquiring 15 small firms. Google seemed to be placing a big bet that YouTube would become a huge marketing hub as

its increasing number of viewers attracts advertisers interested in moving from television to the Internet.

Started in February 2005 in the garage of one of the founders, YouTube displayed in 2006 more than 100 million videos daily and had

about.com. Acquired by The New York Times in February 2005 for $410 million, about.com is a website offering consumer information

and advice and is believed to be one of the biggest and most profitable websites on the Internet, with estimated 2006 revenues of almost

$100 million. With a monthly average number of unique visitors worldwide of 42.6 million, about.com’s revenue per unique visitor was

estimated to be about $0.15, based on monthly revenues of $6.4 million.2

tax profits.

1 Unique visitors are those whose IP addresses are counted only once no matter how many times they visit a website during a given period.

2 Aboutmediakit, September 17, 2006, http://beanadvertiser.about.com/archive/news091606.html.

25

Recall that a firm earns its cost of equity on an investment whenever the net present value of the investment is zero. Assuming a risk–

free rate of return of 5.5 percent, a beta of 0.82 (per Yahoo! Finance), and an equity premium of 5.5 percent, Google’s cost of equity

would be 10 percent. For Google to earn its cost of equity on its investment in YouTube, YouTube would have to generate future cash

flows whose present value would be at least $1.65 billion (i.e., equal to its purchase price). To achieve this result, YouTube’s free cash

Google strategy involving multiple acquisitions to attract additional traffic to Google and to promote the brand, the purchase may indeed

make sense.

.

Discussion Questions:

1. What alternative valuation methods could Google have used to justify the purchase price it paid for YouTube? Discuss the

advantages and disadvantages of each.

Answer: Alternative methods include comparable recent transactions (e.g., News Corp’s purchase of MySpace in 2005),

comparable recent transactions, and discounted cash flow. Advantages of using the recent comparable transactions method is

that it shows what investors are actually willing to pay for a similar company; however, this method is limited by the paucity of

2. The purchase price paid for YouTube represented more than one percent of Google’s then market value. If you were a Google

shareholder, how might you have evaluated the wisdom of the acquisition?

3. To what extent might the use of stock by Google have influenced the amount they were willing to pay for YouTube? How might

the use of “overvalued” shares impact future appreciation of Google stock?

4. What is the appropriate cost of equity for discounting future cash flows? Should it be Google’s or YouTube’s? Explain your

answer.

5. What are the key valuation assumptions implicit in the valuation method discussed in this case study?

A REAL OPTIONS’ PERSPECTIVE ON MICROSOFT’S DEALINGS WITH YAHOO

In a bold move to transform two relatively weak online search businesses into a competitor capable of challenging market leader Google,

Microsoft proposed to buy Yahoo for $44.6 billion on February 2, 2008. At $31 per share in cash and stock, the offer represented a 62

percent premium over Yahoo’s prior day closing price. Despite boosting its bid to $33 per share to offset a decline in the value of

Microsoft could have continued to slug it out with Yahoo and Google, as it has been for the last five years, but this would have given

Google more time to consolidate its leadership position. Despite having spent billions of dollars on Microsoft’s online service (Microsoft

Network or MSN) in recent years, the business remains a money loser (with losses exceeding one half billion dollars in 2007).

Furthermore, MSN accounted for only 5 percent of the firm’s total revenue at that time.

Microsoft argued that its share of the online Internet search (i.e., ads appearing with search results) and display (i.e., website banner

The two firms have very different cultures. The iconic Silicon Valley–based Yahoo often is characterized as a company with a free-

wheeling, fun-loving culture, potentially incompatible with Microsoft’s more structured and disciplined environment. Melding or

eliminating overlapping businesses represents a potentially mind-numbing effort given the diversity and complexity of the numerous sites

available. To achieve the projected cost savings, Microsoft would have to choose which of the businesses and technologies would survive.

Moreover, the software driving all of these sites and services is largely incompatible.

As an independent or stand-alone business, the market valued Yahoo at approximately $17 billion less than Microsoft’s valuation.

major uncertainties dealt with the actual timing of an acquisition and whether the two businesses could be integrated successfully. For

Microsoft’s attempted takeover of Yahoo, such options included the following:

Base case. Buy 100 percent of Yahoo immediately.

Option to expand. If Yahoo were to accept the bid, accelerate investment in new products and services contingent on the successful

integration of Yahoo and MSN.

27

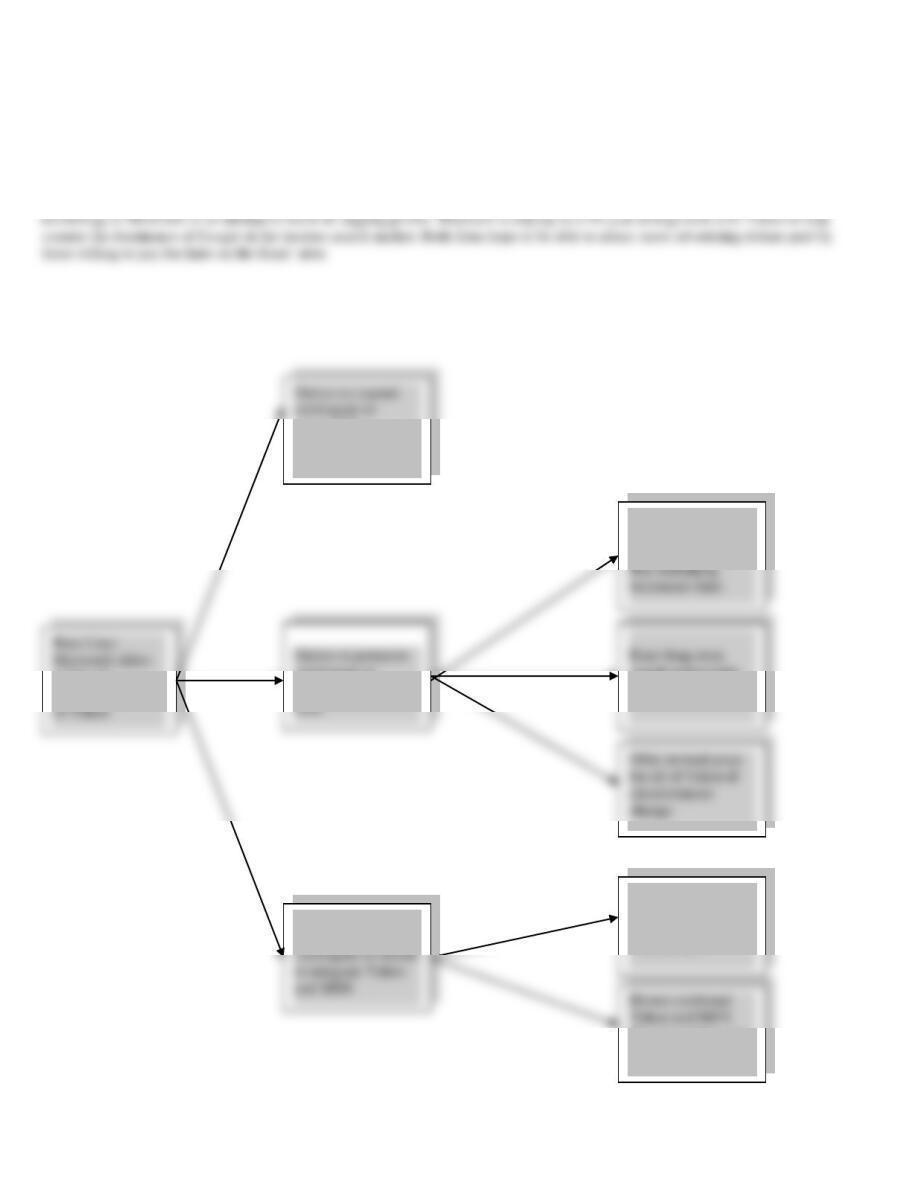

The decision tree in the following exhibit illustrates the range of real options (albeit an incomplete list) available to the Microsoft

board at that time. Each branch of the tree represents a specific option. The decision-tree framework is helpful in depicting the significant

flexibility senior management often has in changing an existing investment decision at some point in the future.

With neither party making headway against Google, Microsoft again approached Yahoo in mid-2009, which resulted in an

announcement in early 2010 of an internet search agreement between the two firms. Yahoo transferred control of its internet search

Base Case:

Microsoft offers

Option to postpone

Enter long-term

businesses later.

to integrate Yahoo

and MSN

to buy all

outstanding share

of Yahoo

successful

integration of Yahoo

and MSN

contingent on

Yahoo’s rejection of

offer

Option to abandon

contingent on failure

search partnership

with option to buy.

Spin off combined

Yahoo and MSN to

Microsoft

shareholders

Use proceeds to pay

dividend or buy

back stock.

Microsoft Real Options Decision Tree

Purchase Yahoo

online search only.

Buy remaining

Option to expand

contingent on

Merrill Lynch and BlackRock Agree to Swap Assets

During the 1990s, many financial services companies began offering mutual funds to their current customers who were pouring money

into the then booming stock market. Hoping to become financial supermarkets offering an array of financial services to their customers,

these firms offered mutual funds under their own brand name. The proliferation of mutual funds made it more difficult to be noticed by

potential customers and required the firms to boost substantially advertising expenditures at a time when increased competition was

reducing mutual fund management fees. In addition, potential customers were concerned that brokers would promote their own firm’s

mutual funds to boost profits.

This trend reversed in recent years, as banks, brokerage houses, and insurance companies are exiting the mutual fund management

business. Merrill Lynch agreed on February 15, 2006, to swap its mutual funds business for an approximate 49 percent stake in money–

respectively. Under the terms of the transaction, BlackRock would issue 65 million new common shares to Merrill. Based on BlackRock’s

February 14, 2005, closing price, the deal is valued at $9.8 billion. The common stock gave Merrill 49 percent of the outstanding

BlackRock voting stock. PNC Financial and employees and public shareholders owned 34 percent and 17 percent, respectively. Merrill’s

ability to influence board decisions is limited, since it has only 2 of 17 seats on the BlackRock board of directors. Certain “significant

matters” require a 70 percent vote of all board members and 100 percent of the nine independent members, which include the two Merrill

representatives. Merrill (along with PNC) must also vote its shares as recommended by the BlackRock board.

Discussion Questions:

1. Merrill owns less than half of the combined firms, although it contributed more than one– half of the combined firms’ assets and

net income. Discuss how you might use DCF and relative valuation methods to determine Merrill’s proportionate ownership in

the combined firms.

a. Answer using DCF methods:

PV(Merrill) = $397/(.10 – .04) = $6,617

PV(BlackRock) = $270/(.10 – .06) = $6,750

2. Why do you believe Merrill was willing to limit its influence in the combined firms?

29

3. What method of accounting would Merrill use to show its investment in BlackRock?

BlackRock equal to $9.8 billion.

Valuation Methods Employed in Investment Bank Fairness Opinion Letters

Background

A fairness opinion letter is a written third-party certification of the appropriateness of the price of a proposed transaction such as a merger,

acquisition, leveraged buyout, or tender offer. A typical fairness opinion provides a range of what is believed to be fair values, with a

presumption that the actual deal price should fall within this range. The data used in this case study is found in SunGard’s Schedule 14A

Proxy Statement submitted to the SEC in May 2005.

On March 27, 2005, the investment banking behemoth Lazard Freres (Lazard) submitted a letter to the board of directors of SunGard

Corporation pertaining to the fairness of a $10.9 billion bid to take the firm private made by an investor group. Lazard employed a variety

systems are disrupted.

Comparable Company Analysis

Using publicly available information, Lazard reviewed the market values and trading multiples of the selected publicly held companies

for each business segment. Multiples were based on stock prices as of March 24, 2005 and specific company financial data on publicly

available research analysts’ estimates for 2005. In the case of SunGard’s software business, Lazard reviewed the market values and

trading multiples of four publicly traded financial services companies and three publicly traded securities trading companies. In the case

Similarly, price–to-earnings ratios were created by dividing equity values per share by earnings per share for each comparable company

for calendar 2005. See Tables 8-1 and 8.2.

Table 8-1 Enterprise Value Multiples for

Comparable Recovery Availability Companies

Enterprise Value as a Multiple of

EBITDA

Price-to-Earnings

Multiple (P/E)

2005E

2005E

High

9.0x

38.1x

6.7x

18.2x

Median

6.5x

15.3x

Low

3.8x

12.6x

E = estimate.

30

Based on this analysis, Lazard determined an enterprise value to estimated 2005 EBITDA multiple range for SunGard’s recovery

availability services business of 5.5x to 7.0x. Lazard also determined a 2005 estimated P/E range for this segment of 14.0x to 16.0x.

Multiplying SunGard’s projected EBITDA and earnings per share for 2005 by these ranges, Lazard calculated an enterprise value range

Low

7.3x

16.9x

Based on the results in Table 8-2, Lazard determined an enterprise value to estimated 2005 EBITDA multiple range for SunGard’s

software business of 7.5x to 9.5x. Lazard also determined a 2005 estimated P/E range for SunGard’s software business of 17.0 to 19.0x.

Multiplying SunGard’s projected EBITDA and earnings per share for 2005 by these ranges, Lazard calculated an enterprise value range

for SunGard’s software business of approximately $4.3 billion to $5.2 billion.

enterprise values of the recent transactions as a multiple of the last twelve months EBITDA for the period ending on the recent transaction

announcement date. See Table 8-3.

Table 8-3. Enterprise Value as a Multiple of Last Twelve Months EBITDA

for Recovery Availability Business

High

10.8x

Mean

7.37x

Median

6.4x

Low

5.4x

Based on Table 8-3, Lazard determined an EBITDA multiple range of 6.5x to 7.5x and multiplied this range by the last twelve months

EBITDA for SunGard’s recovery availability business to calculate an implied enterprise value range of approximately $3.4 billion to $4.0

billion.

High

11.6x

Mean

9.8x

Median

9.9x

Low

6.8x

High

13.8x

21.5x

Mean

9.7x

18.8x

Median

9.0x

18.1x

Based on the information contained in Table 8-5, Lazard determined an EBITDA multiple range of 9.0x to 11.0x and multiplied this

range by the last twelve month EBITDA for SunGard’s software business to calculate an implied enterprise value range for this business

segment of approximately $5.0 billion to $6.1 billion.

Lazard then summed the enterprise value ranges for SunGard’s software business and recovery availability services business to

2009 and beyond were then discounted to present value using discount rates ranging from 10.0% to 12.0%. Based on this analysis, Lazard

calculated an implied enterprise value range for the software business of approximately $5.6 billion to $7.4 billion.

For SunGard’s recovery availability services business, in calculating the terminal value Lazard assumed perpetual growth rates of

2.0% to 3.0% for the projected free cash flows for periods subsequent to 2009. The projected cash flows were then discounted to present

value using discount rates ranging from 10.0% to 12.0%. Lazard then calculated an implied enterprise value range for SunGard’s recovery

availability business of approximately $2.6 billion to $3.3 billion.

Lazard then aggregated the enterprise value ranges for SunGard’s two business segments to calculate a consolidated enterprise value

8-5.

Table 8-5. Premiums Paid Analysis

Greater Than $1 Billion1

Greater Than $5 Billion

1 Day

1 Week

1 Month

1 Day

1 Week

1 Month

High

69.8%

67.8%

80.2%

33.4%

38.3%

44.0%

Mean

23.8%

26.6%

27.0%

15.3%

23.1%

26.2%

Median

21.3%

24.0%

25.7%

13.0%

25.4%

23.7%

Low

(8.0)%

(19.6)%

0.0%

(1.2)%

5.4%

1The larger premiums paid for smaller transaction may reflect their potentially higher growth potential .

2Negative premiums may be a result of target firms whose expected financial performance had been

deteriorating during the month prior to the announcement date.

32

Summary and Conclusions

33% (i.e., $36/$32.19). Consequently, Lazard Freres viewed the investor group’s offer price for SunGard as fair.

Table 8-6. Valuation Range Summary

Valuation Method

Valuation Range ($/Common

Share)

(Max. Valuation less Min.

Valuation)/Min. Valuation

Comparable Companies

24.20-29.00

19.8%

Recent Transactions

27.60-32.70

18.5%

Discounted Cash Flow

26.70-34.60

29.6%

Premiums Paid

29.94-32.44

27.11-32.19

18.7%

Discussion Questions:

1. Discuss the strengths and weaknesses of each valuation method employed by these investment banks in constructing estimates of

SunGard’s value for the Fairness Opinion Letter. Be specific.

Answer:

a. Discounted cash flow: Strengths include consideration of differences of the magnitude and timing of cash flows, the

adjustment for risk, and a clear statement of valuation assumptions. Weaknesses include the requirement to forecast

cash flows for each period, a terminal value, and a discount rate using limited or unreliable data. DCF methods are also

2. Why do you believe that the percentage difference between the maximum and minimum valuation estimates varies so much from

one valuation method to another? See Table 8–7.

Answer: Each method the comparable companies, recent transactions, and premiums paid methods rely on the accuracy of the