3. Why would lenders be willing to lend to a firm emerging from Chapter 11? How did the lenders

attempt to manage their risks? Be specific.

4. In view of the substantial loss of jobs, as well as wage and benefit reductions, do you believe that

firms should be allowed to reorganize in bankruptcy? Explain your answer.

Answer: While it is clear that many employees suffer job losses and salary and benefit reductions

as a result of the bankruptcy process, these costs must be weighed against the benefits of

5. How does Chapter 11 potentially affect adversely competitors of those firms emerging from

bankruptcy? Explain your answer.

The General Motors’ Bankruptcy—The Largest Government-Sponsored Bailout in U.S. History

Rarely has a firm fallen as far and as fast as General Motors. Founded in 1908, GM dominated the car

industry through the early 1950s with its share of the U.S. car market reaching 54 percent in 1954, which

proved to be the firm’s high water mark. Efforts in the 1980s to cut costs by building brands on common

platforms blurred their distinctiveness. Following increasing healthcare and pension benefits paid to

employees, concessions made to unions in the early 1990s to pay workers even when their plants were shut

down reduced the ability of the firm to adjust to changes in the cyclical car market. GM was increasingly

burdened by so-called legacy costs (i.e., healthcare and pension obligations to a growing retiree

population). Over time, GM’s labor costs soared compared to the firm’s major competitors. To cover these

costs, GM continued to make higher margin medium to full-size cars and trucks, which in the wake of

higher gas prices could only be sold with the help of highly attractive incentive programs. Forced to

support an escalating array of brands, the firm was unable to provide sufficient marketing funds for any one

of its brands.

With the onset of one of the worst global recessions in the post–World War II years, auto sales

worldwide collapsed by the end of 2008. All automakers’ sales and cash flows plummeted. Unlike Ford,

GM and Chrysler were unable to satisfy their financial obligations. The U.S. government, in an

unprecedented move, agreed to lend GM and Chrysler $13 billion and $4 billion, respectively. The intent

was to buy time to develop an appropriate restructuring plan.

Having essentially ruled out liquidation of GM and Chrysler, continued government financing was

contingent on gaining major concessions from all major stakeholders such as lenders, suppliers, and labor

unions. With car sales continuing to show harrowing double-digit year over year declines during the first

half of 2009, the threat of bankruptcy was used to motivate the disparate parties to come to an agreement.

With available cash running perilously low, Chrysler entered bankruptcy in early May and GM on June 1,

employees, the elimination of most “legacy costs,” and a reduced number of dealerships and brands, GM

found itself operating in an environment in 2009 in which U.S. vehicle sales totaled an anemic 10.4 million

units. This compared to more than 16 million in 2008. GM’s 2009 market share slipped to a post–World

War II low of about 19 percent.

While the bankruptcy option had been under consideration for several months, its attraction grew as it

became increasingly apparent that time was running out for the cash-strapped firm. Having determined

from the outset that liquidation of GM either inside or outside of the protection of bankruptcy would not be

considered, the government initially considered a prepackaged bankruptcy in which agreement is obtained

among major stakeholders prior to filing for bankruptcy. The presumption is that since agreement with

many parties had already been obtained, developing a plan of reorganization to emerge from Chapter 11

would move more quickly. However, this option was not pursued because of the concern that the public

would simply view the post–Chapter 11 GM as simply a smaller version of its former self. The government

redundant equipment. In recent years, so-called 363 sales have been used to completely restructure

businesses, including the 363 sales of entire companies. A 363 sale requires only the approval of the

bankruptcy judge, while a plan of reorganization in Chapter 11 must be approved by a substantial number

of creditors and meet certain other requirements to be approved. A plan of reorganization is much more

comprehensive than a 363 sale in addressing the overall financial situation of the debtor and how its exit

strategy from bankruptcy will affect creditors. Once a 363 sale has been consummated and the purchase

price paid, the bankruptcy court decides how the proceeds of sale are allocated among secured creditors

with liens on the assets sold.

Total financing provided by the U.S. and Canadian (including the province of Ontario) governments

amounted to $69.5 billion. U.S. taxpayer-provided financing totaled $60 billion, which consisted of $10

billion in loans and the remainder in equity. The government decided to contribute $50 billion in the form

of equity to reduce the burden on GM of paying interest and principal on its outstanding debt. Nearly $20

billion was provided prior to the bankruptcy, $11 billion to finance the firm during the bankruptcy

proceedings, and an additional $19 billion in late 2009. In exchange for these funds, the U.S. government

owns 60.8 percent of the “new GM’s common shares, while the Canadian and Ontario governments own

11.7 percent in exchange for their investment of $9.5 billion. The United Auto Workers’ new voluntary

employee beneficiary association (VEBA) received a 17.5 percent stake in exchange for assuming

54,000 UAW workers it employed prior to declaring bankruptcy in the United States and close 12 to 20

plants. GM did not include its foreign operations in Europe, Latin America, Africa, the Middle East, or

Asia Pacific in the Chapter 11 filing. Annual vehicle production capacity for the firm will decline to 10

million vehicles in 2012, compared with 15 to 17 million in 1995. The firm exited bankruptcy with

14 states. Another $300 million was set aside for property taxes, plant security, and other shutdown

expenses. A second trust will handle claims of the owners of GM’s prebankruptcy debt, who are expected

to get 10 percent of the equity in General Motors when the firm goes public and warrants to buy additional

shares at a later date. The remaining two trusts are intended to process litigation such as asbestos-related

Assuming a corporate marginal tax rate of 35 percent, the government would lose another $15.75 in future

tax payments as a result of the loss carryforward. The government also is providing $7,500 tax credits to

buyers of GM’s new all-electric car, the Chevrolet Volt.

2 Lattman and de la Merced, 2010

Discussion Questions

1. Do you agree or disagree that the taxpayer financed bankruptcy represented the best way to save

jobs. Explain your answer.

Answer: As many as 54,000 jobs may be lost in order to restore the new GM to prosperity. It

is unclear at this point if the government will recover much of its investment and loans to the

firm. If the firm had been liquidated, others would have acquired GM brands as they did with

Hummer, Saturn, and Opel. Consequently, jobs associated with the GM brands would have

2. Discuss the relative fairness to the various stakeholders in a bankruptcy of a

more traditional Chapter 11 bankruptcy in which a firm emerges from the protection of the

bankruptcy court following the development of a plan of reorganization versus an expedited

sale under Section 363 of the federal bankruptcy law. Be specific.

Answers: A Chapter 11 plan of reorganization offers substantially more time to develop a

viable plan for enabling the debtor firm to emerge from bankruptcy and one which treats the

Consolidat

U.S. &

Canadian

Operations

Attractive

Assets

“New GM”

U.S. &

Canadian

Ope ti

Consolidat

Pre-Bankruptcy Bankruptcy Post-Bankruptcy

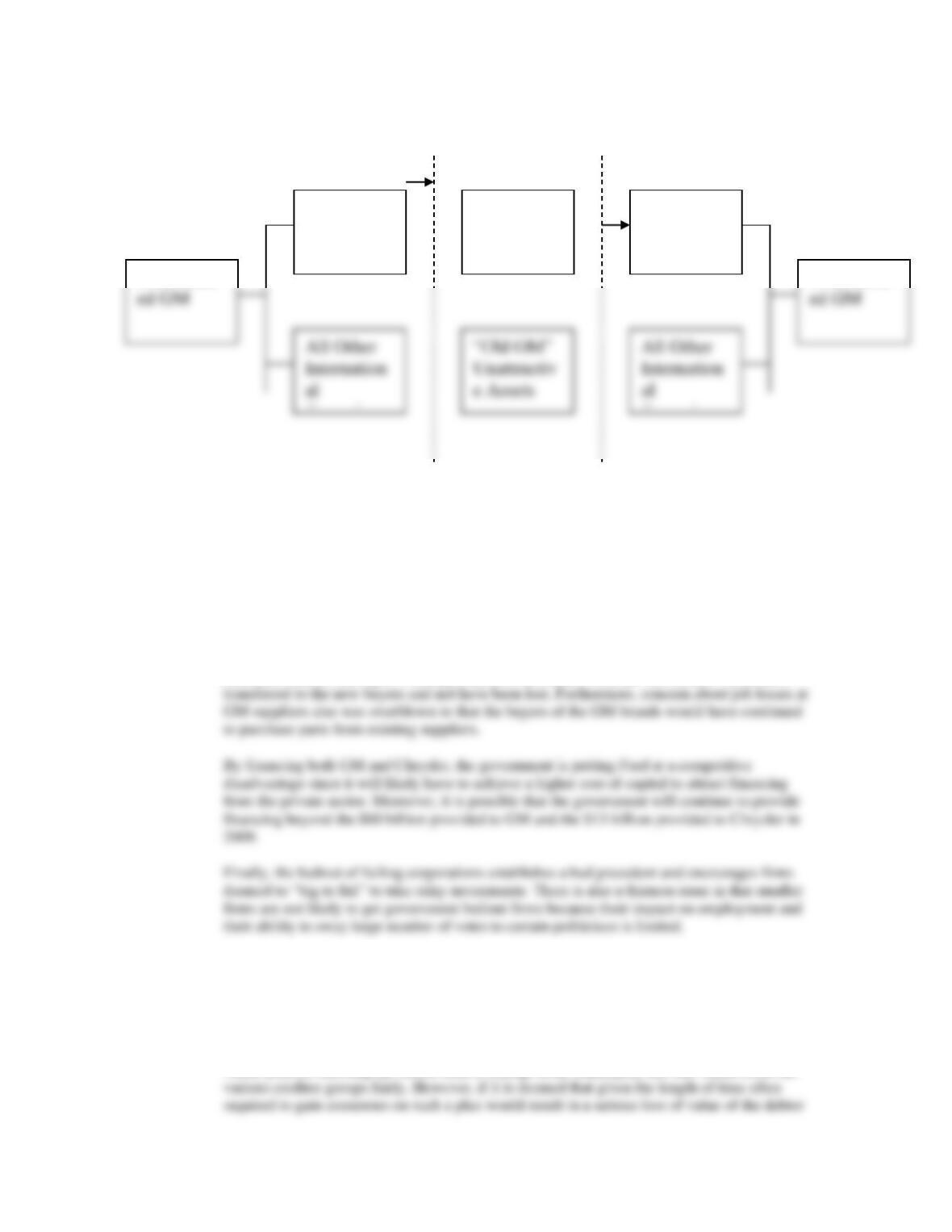

Figure 16.2 General Motors Bankruptcy

3. Identify what you believe to be the real benefits and costs of the bailout of General Motors?

Be specific.

Answer: The benefits appear to be the preservation of jobs and income at a time when the

economy was suffering from a severe recession. It is impossible to know how many jobs

would have been lost at GM and its suppliers had the firm undertaken a more conventional

reorganization. However, even if it had been liquidated, other firms would have acquired the

portions of GM that ultimately emerged from bankruptcy, thereby limiting the loss of jobs.

4. The first round of government loans to GM occurred in December 2008. The

firm did not file for bankruptcy until June 1, 2009. Discuss the advantages and disadvantages

of the firm having filed for bankruptcy much earlier in 2009. Be specific.

Answer: The major advantages of seeking Chapter 11 protection earlier in 2009 would have

been the immediate improvement in GM’s operating cash flow as it would have been able to

5. What alternative restructuring strategies do you believe may have been

considered for GM? Of these, do you believe that the 363 sale in bankruptcy

represented the best course of action? Explain your answers.

Answer: The range of options no doubt included the renegotiation of labor contracts to

reduce GM’s labor cost disparity with its major competitors and the transfer of so-called

legacy costs including retiree healthcare and pension obligations to the UAW managed trust.

Such negotiations would also have included the so-called jobs bank in which workers were

Lehman Brothers Files for Chapter 11 in the Biggest Bankruptcy in U.S. History

A casualty of the 2008 credit crisis that shook Wall Street to its core, Lehman Brothers Holdings, Inc., a

holding company, announced on September 15, 2008, that it had filed a petition under Chapter 11 of the

U.S. Bankruptcy Code. Lehman’s board of directors decided to opt for court protection after attempts to

find a buyer for the entire firm collapsed. With assets of $639 billion and liabilities of $613 billion, Lehman

is the largest bankruptcy in history in terms of assets. The next biggest bankruptcies were WorldCom and

Enron with $126 billion and $81 billion in assets, respectively.

None of the holding company’s subsidiaries was included in the filing, enabling customers of Lehman’s

brokerage, Neuberger Berman Holdings, to continue to use their accounts to trade. Furthermore, by

excluding its units from the bankruptcy filing, customers of its broker–dealer operations would not be

subject to claims by LBHI’s more than 100,000 creditors in the bankruptcy case.

operations for $250 million and paid an additional $1.5 billion for the firm’s New York headquarters

building and two New Jersey–based data centers. Coming just five days after Lehman filed for bankruptcy,

the deal reflected the urgency to find buyers for those businesses whose value consisted primarily of their

employees. Barclays did not buy any of Lehman’s commercial real estate assets or private equity and hedge

fund investments. However, Barclays did agree to take $47.4 billion in securities and assume $45.5 billion

in trading liabilities. On September 24, 2008, Japanese brokerage Nomura Securities acquired Lehman’s

Japanese and Australian operation for $250 million. Lehman’s investment management group, Neuberger

Berman, was sold in late December 2008 to a Neuberger management group for $922 million. Under the

deal, Neuberger‘s management would own 51 percent of the firm, and Lehman’s creditors would control the

bondholders $366 billion (i.e., 0.915 × $400 billion). Purchasers of this debt were betting that, following

Lehman’s liquidation, holders of this debt would receive more than 8.5 cents on the dollar and the insurers

would be able to satisfy their obligations.

Hedge funds also were affected by the Lehman bankruptcy. Hedge funds borrowed heavily from

Lehman, putting up certain assets as collateral for the loans. While legal, Lehman was using this collateral

to borrow from other firms. By using its customers’ collateral as its own collateral, Lehman and other firms

could borrow more money, using the proceeds to make additional investments. When Lehman filed for

bankruptcy, the court took control of such assets until who was entitled to the assets could be determined.

the regulators and credit rating agencies could not. See the Inside M&A case study at the beginning of

Chapter 2 for more details on Lehman’s accounting practices.

Discussion Questions

1. Why did Lehman choose not to seek Chapter 11 protection for its subsidiaries?

2. How does Chapter 11 bankruptcy protect Lehman’s creditors? How does it potentially hurt them?

Explain your answers.

3. Do you believe the U.S. bankruptcy process was appropriate in this instance? Explain your answer.

4. Do you believe the U.S. government’s failure to bail out Lehman, thereby forcing the firm to file for

bankruptcy, exacerbated the global credit meltdown in October 2008? Explain your answer.

A Reorganized Dana Corporation

Emerges from Bankruptcy Court

Dana Corporation, an automotive parts manufacturer, announced on February 1, 2008, that it had emerged

from bankruptcy court with an exit financing facility of $2 billion. The firm had entered Chapter 11

reorganization on March 3, 2006. During the ensuing 21 months, the firm and its constituents identified,

agreed on, and won court approval for approximately $440 million to $475 million in annual cost savings

and the elimination of unprofitable products. These annual savings resulted from achieving better plant

utilization due to changes in union work rules, wage and benefit reductions, the reduction of ongoing

obligations for retiree health and welfare costs, and streamlining administrative expenses.

million of the convertible preferred shares. The preferred shares were issued as an inducement to get

creditors to support the plan of reorganization. Under the reorganization plan, Dana sold some businesses,

cut plants in the United States and Canada, reduced its hourly and salaried workforce, and sought price

increases on parts from customers.

Discussion Questions

1. Does the process outlined in this business case seem equitable for all parties to the bankruptcy

proceedings? Why? Why not? Be specific.

2 Why did Centerbridge receive convertible preferred rather than common stock?

Calpine Emerges from the Protection of Bankruptcy Court

Following approval of its sixth Plan of Reorganization by the U.S. Bankruptcy Court for the Southern

District of New York, Calpine Corporation was able to emerge from Chapter 11 bankruptcy on January 31,

2008. Burdened by excessive debt and court battles with creditors on how to use its cash, the electric utility

had sought Chapter 11 protection by petitioning the bankruptcy court in December 2005. After settlements

with certain stakeholders, all classes of creditors voted to approve the Plan of Reorganization, which

provided for the discharge of claims through the issuance of reorganized Calpine Corporation common

stock, cash, or a combination of cash and stock to its creditors.

reflecting the number of shares of “old common stock” held at the time of cancellation. These warrants

carried an exercise price of $23.88 per share and expired on August 25, 2008. Relisted on the New York

Stock Exchange, the reorganized Calpine Corporation common stock began trading under the symbol CPN

on February 7, 2008, at about $18 per share.

The firm had improved its capital structure while in bankruptcy. On entering bankruptcy, Calpine

billion of these funds were used to satisfy cash payment obligations under the Plan of Reorganization.

These obligations included the repayment of a portion of unsecured creditor claims and administrative

claims, such as legal and consulting fees, as well as expenses incurred in connection with the “exit

facilities” and immediate working capital requirements. On emerging from Chapter 11, the firm carried

$10.4 billion of debt with an average interest rate of 8.1 percent.

The Enron Shuffle—A Scandal to Remember

What started in the mid-1980s as essentially a staid “old-economy” business became the poster child in the

late 1990s for companies wanting to remake themselves into “new-economy” powerhouses. Unfortunately,

what may have started with the best of intentions emerged as one of the biggest business scandals in U.S.

history. Enron was created in 1985 as a result of a merger between Houston Natural Gas and Internorth

Natural Gas. In 1989, Enron started trading natural gas commodities and eventually became the world‘s

largest buyer and seller of natural gas. In the early 1990s, Enron became the nation’s premier electricity

marketer and pioneered the development of trading in such commodities as weather derivatives, bandwidth,

pulp, paper, and plastics. Enron invested billions in its broadband unit and water and wastewater system

management unit and in hard assets overseas. In 2000, Enron reported $101 billion in revenue and a market

to remove everything from telecommunications fiber to water companies from the firm‘s balance sheet and

into partnerships. What distinguished Enron’s partnerships from those commonly used to share risks were

their lack of independence from Enron and the use of Enron’s stock as collateral to leverage the

partnerships. If Enron’s stock fell in value, the firm was obligated to issue more shares to the partnership to

restore the value of the collateral underlying the debt or immediately repay the debt. Lenders in effect had

Enron management seems to have exerted disproportionate influence in some instances over partnership

decisions, although its ownership interests were very small, often less than 3 percent. Curiously, Enron’s

outside auditor, Arthur Andersen, had a dual role in these partnerships, collecting fees for helping to set

them up and auditing them.

Time to Pay the Piper

prices. Margins also suffered from poor cost containment.

Dynegy Corp. agreed to buy Enron for $10 billion on November 2, 2001. On November 8, Enron

announced that its net income would have to be restated back to 1997, resulting in a $586 million reduction

in reported profits. On November 15, chairman Kenneth Lay admitted that the firm had made billions of

dollars in bad investments. Four days later, Enron said it would have to repay a $690 million note by mid–

result of its secrecy and complex financial maneuvers, forcing the firm into bankruptcy in early December.

Enron’s stock, which had reached a high of $90 per share on August 17, 2001, was trading at less than $1

by December 5, 2001.

In addition to its angry creditors, Enron faced class-action lawsuits by shareholders and employees,

whose pensions were invested heavily in Enron stock. Enron also faced intense scrutiny from congressional

Questions remain as to why Wall Street analysts, Arthur Andersen, federal or state regulatory

authorities, the credit rating agencies, and the firm’s board of directors did not sound the alarm sooner. It is

surprising that the audit committee of the Enron board seems to have somehow been unaware of the firm’s

highly questionable financial maneuvers. Inquiries following the bankruptcy declaration seem to suggest

that the audit committee followed all the rules stipulated by federal regulators and stock exchanges

Enron may be the best recent example of a complete breakdown in corporate governance, a system

intended to protect shareholders. Inside Enron, the board of directors, management, and the audit function

failed to do the job. Similarly, the firm’s outside auditors, regulators, credit rating agencies, and Wall Street

analysts also failed to alert investors. What seems to be apparent is that if the auditors fail to identify

incompetence or fraud, the system of safeguards is likely to break down. The cost of failure to those

and may account for the proliferation of specific accounting rules applicable only to certain transactions to

insulate both the firm engaging in the transaction and the auditor reviewing the transaction from subsequent

litigation. In one sense, the Enron debacle represents a failure of the free market system and its current

shareholder protection mechanisms, in that it took so long for the dramatic Enron shell game to be revealed

to the public. However, this incident highlights the remarkable resilience of the free market system. The

2001. The resulting reorganization has been one of the most costly and complex on record, with total legal

and consulting fees exceeding $500 million by the end of 2003. More than 350 classes of creditors,

18.3 cents on the dollar. The money came in cash payments and stock in two holding companies,

CrossCountry containing the firm’s North American pipeline assets and Prisma Energy International

containing the firm’s South American operations.

After losing its auditing license in 2004, Arthur Andersen, formerly among the largest auditing firms in

37.4 cents on each dollar owed to them. This lawsuit followed the settlement of a $40 billion class action

Case Study Discussion Questions:

1. In your judgment, what were the major factors contributing to the demise of Enron? Of these

factors, which were the most important?

Answer: The major contributing to the debacle include blind ambition, greed, and arrogance.

Enron grew aggressively beyond its original gas pipeline business into a series on trading and risk

management businesses in an effort to transfer tangible assets off the balance sheet to transform

2. In what way was the Enron debacle a break down in corporate governance (oversight)? Explain

your answer.

3. How were the Enron partnerships used to hide debt and inflate the firm’s earnings? Should

partnership structures be limited in the future? If so, how?

Answer: The mechanism involved creating a series of partnerships that would buy the assets (e.g.,

power generating companies) and then sell their output through Enron’s trading operations.

Enron’s stock was often used as collateral to enable the partnerships to borrow to purchase

4. What should (or can) be done to reduce the likelihood of this type of situation arising in the

future? Be specific.

Answer: Raise the cost of non-compliance with laws and regulations. This has been partly

achieved through the passage of the Sarbanes-Oxley bill in 2002 in which gross negligence or

fraud can be subject to criminal as well as civil penalties. Other reforms include increasing the

PG&E SEEKS BANKRUPTCY PROTECTION

Pacific, Gas, and Electric (PG&E), the San Francisco-based utility, filed for bankruptcy on April 7, 2001,

citing nearly $9 billion in debt and un-reimbursed energy costs. The utility, one of three privately owned

utilities in California, serves northern and central California. The intention of the Chapter 11

reorganization was to make the utility solvent again by protecting the firm from lawsuits or any other action

by those who are owed money by the utility. The bankruptcy will also allow the utility to deal with all of

the firm’s debts in a single forum rather than with individual debtors in what had become a highly

politicized venue. The following time line outlines the firm’s road to bankruptcy.

P&G Bankruptcy Timeline

September 1996:

Wholesale power prices begin to rise as demand surges past supply in the buoyant

economy. However, the 1996 law prohibits the utilities from passing rising costs on

to customers until March 1, 2002.

May 2000:

California’s power restructuring efforts signed into law by then Governor Pete

Wilson.

January 4, 2001:

California Public Utility Commission (PUC) disallows PG&E’s request to recover

the full amount of their cost increases and approves an average 10% increase in retail

rates, about two-thirds of what had been requested. The PUC institutes internal

audits of the state’s private utilities.

January 5, 2000:

Credit rating agencies downgrade PG&E and Southern California Edison (SCE) to

one notch above junk bonds.

January 10, 2000:

PG&E asks then Governor Grey Davis for help to buy natural gas for customers,

saying it does not have enough cash to pay its bills.

January 12, 2000:

PG&E lays off 1000 workers.

January 17, 2000:

Rolling blackouts are ordered for the first time to avoid overloading the state’s

power grid. PG&E defaults on $76 million in commercial paper.

January 19, 2000:

President Clinton declares a natural gas supply emergency and orders out–of-state

suppliers to continue selling gas to PG&E despite concerns about getting paid.

January 23, 2000:

The Bush administration extends emergency orders through February 6.

March 27, 2000:

The PUC approves an increase in retail electricity prices by 3 cents per kilowatt-hour

April 6, 2000:

PG&E files for bankruptcy

.

Utility industry analysts saw PG&E’s move as largely an effort to escape the political paralysis that had

befallen the state’s regulatory apparatus. The bankruptcy filing came one day after Governor Davis

dropped his opposition to raising retail rates. However, the Governor’s reversal came after five month’s of

negotiations with the state’s privately owned utilities on a rescue plan.

PG&E’s common shares fell 37 percent on the day the firm filed for reorganization. Fearing a similar

By September, a slowing economy pushed the wholesale price of electricity well below the level the state

was required to pay in the “take or pay” contracts the state had just signed. Estimates suggest that

California taxpayers will have to pay between $40 and $45 billion in power costs over the next decade

depending on what happens to future energy costs. PG&E has continued to supply its customers without

disruption or blackout while being under the protection of the bankruptcy court.

reassuring because it did not include a timetable for repayment of outstanding debt, others viewed the

agreement as a voluntary reorganization plan without going through the expensive process of filing for

bankruptcy with the federal court.

Discussion Questions:

1. In your judgment, did regulators attenuate or exacerbate the situation? Explain your answer.

Answer: Regulators exacerbated the situation.. By not allowing the utilities to raise retail

2. PG&E pursued bankruptcy protection, while Southern California Edison did not. What could

PG&E have been done differently to avoid bankruptcy?